Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

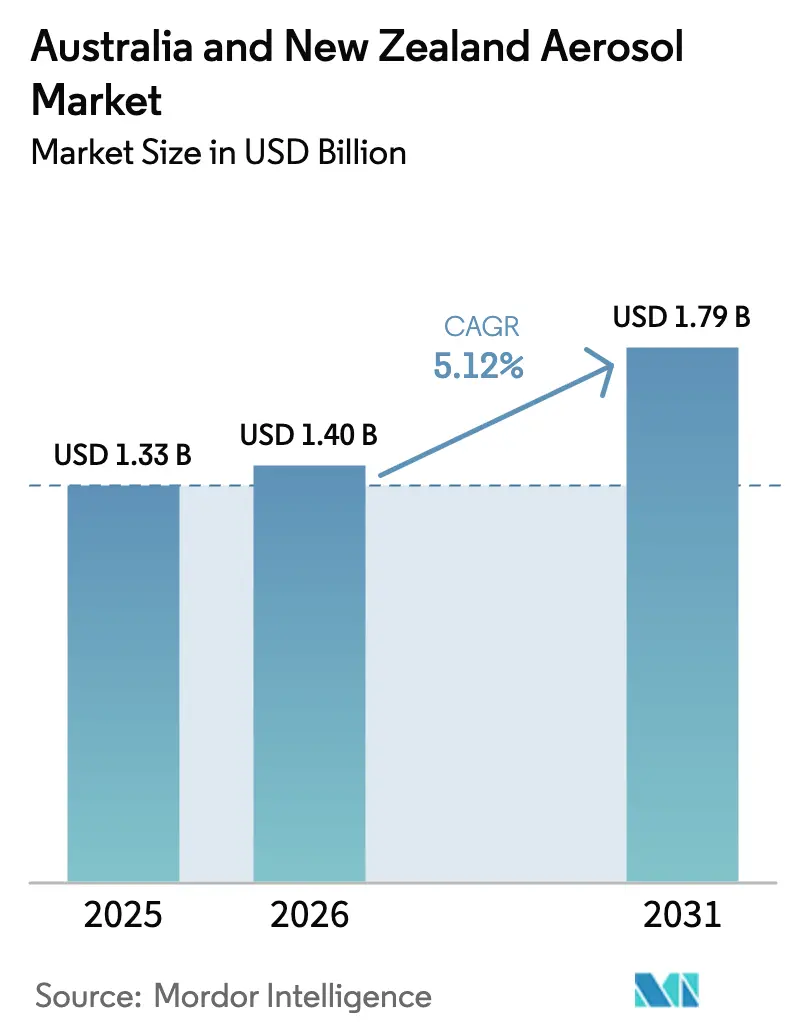

| Base Year Market Size (2025) | USD 1.33 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

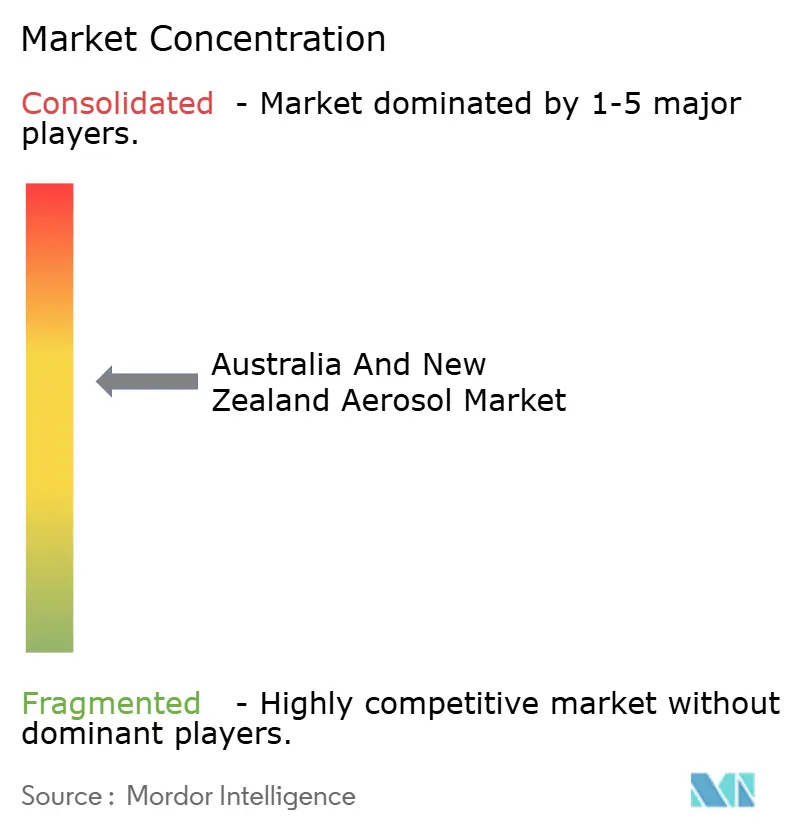

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia And New Zealand Aerosol Market Analysis by Mordor Intelligence

The Australia and New Zealand Aerosol Market size is expected to increase from USD 1.33 billion in 2025 to USD 1.40 billion in 2026 and reach USD 1.79 billion by 2031, growing at a CAGR of 5.12% over 2026-2031. Brand owners are switching from steel to lighter-weight aluminum cans to satisfy retailer recycled-content mandates, while medical inhaler demand is rising under new clinical guidelines that favor anti-inflammatory reliever therapy. Retail private-label lines now specify minimum recyclability and carbon scores, making packaging choices a competitive lever. Propellant policy is equally influential; Australia’s HFC phase-down caps tighten again in 2026, accelerating the shift to hydrocarbon blends and opening a technology window for low-GWP alternatives. Meanwhile, construction-related spray-paint consumption benefits from infrastructure outlays in New South Wales, Victoria, and Queensland, albeit with margins pressured by volatile aluminum and tinplate prices linked to global tariff regimes.

Key Report Takeaways

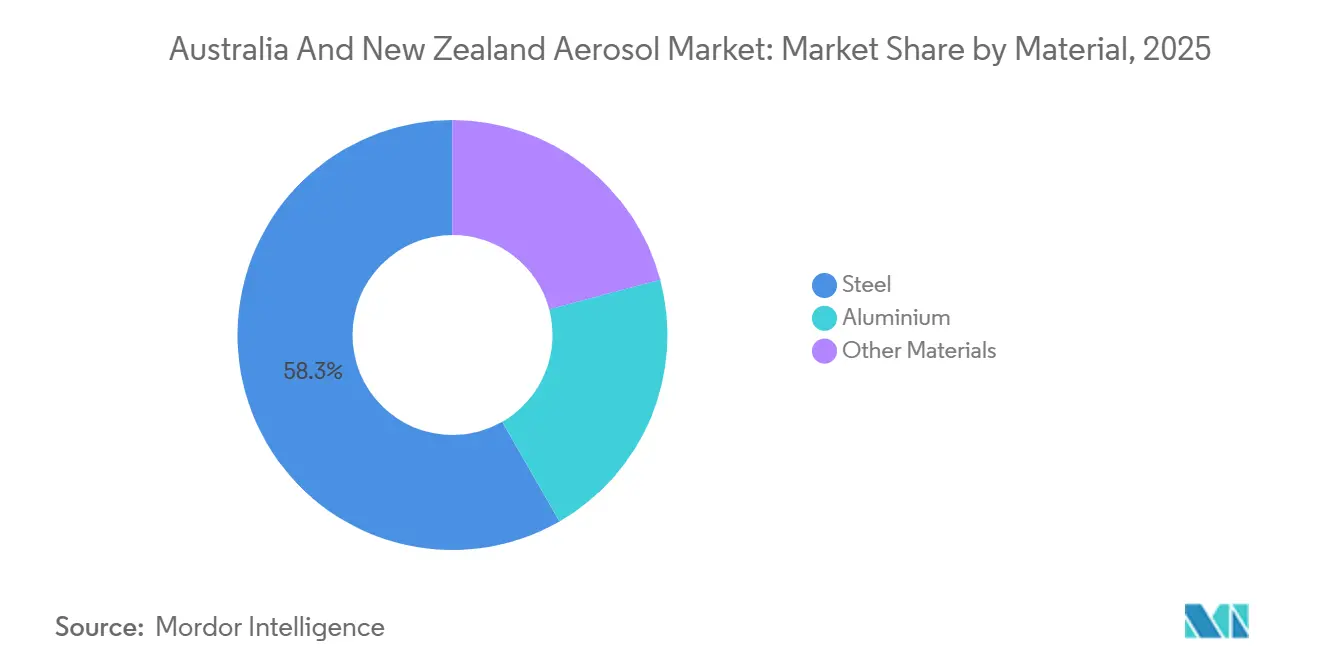

- By materials, steel cans led with 58.28% revenue share in 2025, whereas aluminum is forecast to post the fastest 5.27% CAGR through 2031.

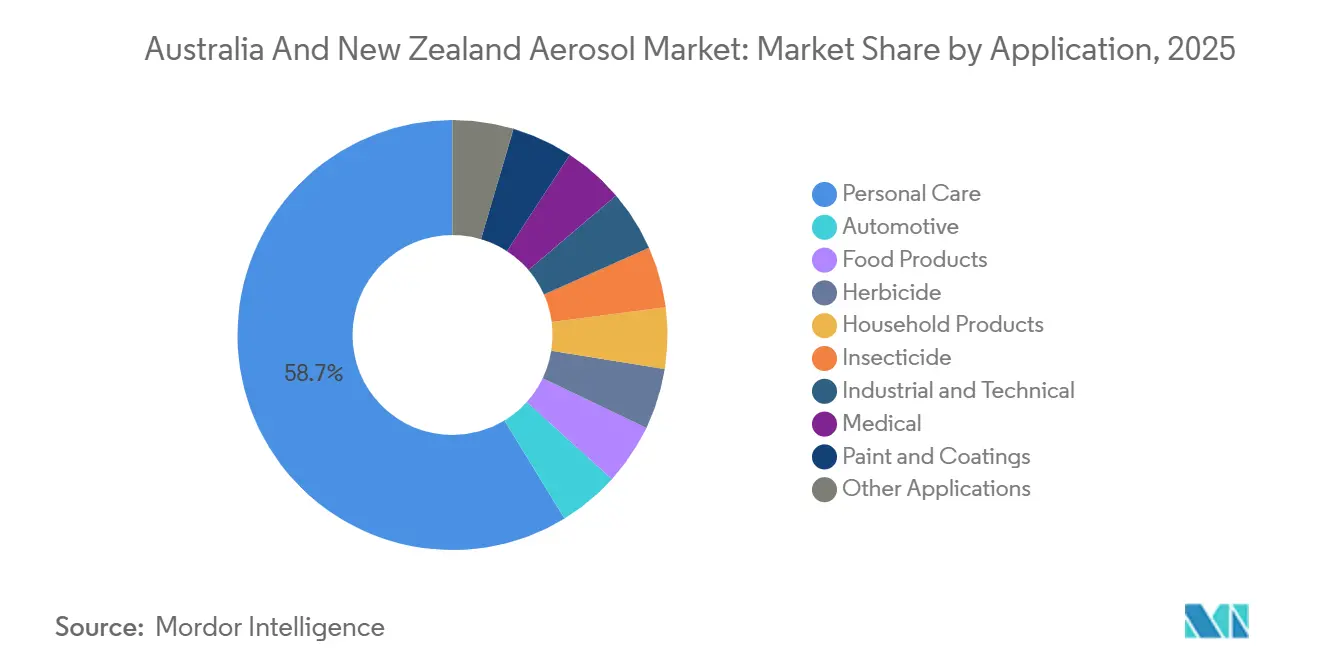

- By application, personal care aerosols captured 58.71% share in 2025 and are projected to advance at a 5.35% CAGR to 2031.

- By geography, Australia accounted for 87.17% of regional sales in 2025 and is growing at a 5.12% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia And New Zealand Aerosol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising eco-friendly, low-GWP propellant adoption | +1.2% | Australia and New Zealand | Medium term (2-4 years) |

| Gen-Z-focused male grooming aerosol launches | +0.9% | Major metro areas | Short term (≤ 2 years) |

| Uptick in metered-dose inhalers for asthma care | +1.5% | Both countries | Medium term (2-4 years) |

| Construction boom driving quick-dry spray paints | +0.8% | Infrastructure corridors | Short term (≤ 2 years) |

| Supermarket private-label aerosol cleaners surge | +0.7% | All retail channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Eco-Friendly, Low-GWP Propellant Adoption

Australia’s HFC quota falls from 5.25 million tons CO₂-e in 2024-2025 to 4.25 million tons CO₂-e for 2026-2027, restricting HFC-134a and HFC-152a supply and nudging formulators toward butane, isobutane, and propane blends[1]Department of Climate Change, Energy, the Environment and Water, “HFC Phase-Down Schedule,” climatechange.gov.au. CSIRO monitoring shows HFC-152a growth slowing to 1.2% annually, an early sign of market substitution. Dove Advanced Care deodorant now highlights hydrocarbon propellants and a recyclable metal can, aligning with Woolworths’ 52% average recycled-content target. Parallel regulatory moves in refrigeration hint at progressively tighter controls that will further squeeze HFC availability. Pharmaceutical inhaler platforms remain an outlier, yet early pilots of dry-powder devices suggest future momentum toward propellant-free options.

Gen-Z-Focused Male Grooming Aerosol Launches

Unilever’s February 2026 Rexona RIVALS line deploys QR-code gamification tied to local sports, leveraging Woolworths’ 25.7 million weekly shoppers for rapid trial. The 220 ml cans command a premium AUD 10.50 shelf price but sell through quickly during match weekends. Limited-edition cycles shorten development timelines, enabling frequent design refreshes without long-run tooling costs. Retail scorecards oblige aluminum formats with verifiable recycled content, so suppliers integrate mass-balance approaches to hit the 60% threshold due by 2025. Younger consumers respond to interactive packaging and sustainability cues, a mix that drives repeat purchase and lifts category value.

Uptick in Metered-Dose Inhalers for Asthma Care

The Australian Asthma Handbook v3.0, issued September 2025, moves 2.8 million patients from SABA monotherapy to budesonide-formoterol combos, displacing roughly 15 million legacy inhalers each year. New Zealand mirrored the shift in October 2025 via bpacnz audit guidance. Combination pMDIs fit existing scripts and pharmacy workflows, preserving the aerosol format while boosting the can demand. The carbon footprint of each HFA-134a inhaler, 25.2 kg CO₂-e, remains under scrutiny, prompting procurement teams to open tenders to low-GWP device alternatives. Spacer accessory sales also rise, as guidelines recommend annual replacement to maximize drug deposition.

Construction Boom Driving Quick-Dry Spray Paints

Federal and state infrastructure pipelines worth more than AUD 200 billion over 2024-2029 expand demand for touch-up coatings that cut downtime on site. PPG’s 2024 buy-out of Barloworld Coatings grants capacity in New South Wales and Victoria to deliver aerosol SKUs through Bunnings’ network of 318 Australian warehouses. Formulations tout fast-drying resins and lead-free pigments to comply with occupational exposure limits. DIY (Do-It-Yourself) uptake is equally brisk, as approvals for home renovations climb in tandem with softening mortgage rates. Raw-material cost swings, however, cap margin expansion despite top-line growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter 2027 VOC-limit compliance costs | -0.6% | Export-oriented fillers | Medium term (2-4 years) |

| Volatile aluminum and tinplate prices | -0.9% | Import-dependent converters | Short term (≤ 2 years) |

| Retailer carbon-scorecard penalties | -0.4% | Supplier networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter 2027 VOC-Limit Compliance Costs

The United States Environmental Protection Agency (EPA) extended the aerosol-coatings VOC deadline to January 2027, but Australian and New Zealand exporters must still retool formulas, run shelf-life trials, and absorb certification fees[2]U.S. Environmental Protection Agency, “National VOC Emission Standards for Aerosol Coatings,” federalregister.gov. Smaller fillers lack in-house toxicology labs, so they outsource, lengthening time-to-market. In parallel, domestic Safe Work Australia exposure limits only partly overlap with the EPA’s reactivity-based caps, adding paper-chase overhead. The scheduling clash with HFC quota cuts compounds compliance budgeting.

Volatile Aluminum and Tinplate Prices

The US Midwest Premium breached USD 1.00 per pound in January 2026, an all-time high that rippled through spot markets used by Australasian converters. Middle East supply disruptions, covering 21% of unwrought aluminum imports in 2025, inject further price risk. With aluminum cans growing faster than steel, converters bid aggressively for rolling-mill slots, eroding spreads. Hedge contracts cushion multinationals, yet independents face cash-flow squeezes when premiums spike without retail pass-through.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Aluminum Gains on Lightweighting and Recycled-Content Mandates

Steel retained 58.28% of Australia and New Zealand aerosol market share in 2025, owing to cost-effective supply into insecticides and technical sprays. Yet aluminum’s 5.27% CAGR through 2031 signals a structural pivot in the Australia and New Zealand aerosol market as retailers enforce packaging scorecards that favor lighter, endlessly recyclable metals. Confirming the trend, Dove Advanced Care deodorant now advertises a recyclable-metal can and hydrocarbon propellants to meet low-GWP goals.

Volatile pricing clouds the outlook; the January 2026 Midwest Premium spike fed through to Asia-Pacific offers within days, testing converter margins. Even so, brand owners keep specifying aluminum for premium deodorant, shaving, and hair-styling lines to differentiate on the shelf. Steel cans remain dominant in budget cleaners and paints, making the Australia and New Zealand aerosol market size sensitive to commodity swings across both substrates.

By Application: Personal Care Leads Volume and Growth on Sports-Themed Launches

Personal care commanded 58.71% share in 2025 and leads all categories with a 5.35% CAGR, anchoring the Australia and New Zealand aerosol market size expansion. Unilever’s Rexona RIVALS and Lynx limited editions illustrate how QR-code engagement and sports licensing lift basket value among Gen-Z males.

Medical aerosols form the fastest-growing niche inside the Australia and New Zealand aerosol industry, driven by budesonide-formoterol protocols. Household cleaners and insecticides track supermarket private-label momentum, while construction paints follow infrastructure spend. Each vertical faces the same packaging and propellant pressures, underlining the integrated nature of growth levers across the Australia and New Zealand aerosol market.

Geography Analysis

Australia delivered 87.17% of regional turnover in 2025 and sustains a 5.12% CAGR as deeper retail penetration and larger population push per-capita deodorant and inhaler usage. HFC import quotas tighten again in 2026, hastening adoption of hydrocarbon blends and sparking early trials of ultra-low-GWP propellants. Construction outlays and Bunnings’ store roll-out amplify demand for DIY sprays.

New Zealand, though smaller, benefits from regulatory harmonization, allowing cross-border SKU pooling. bpacnz’s 2025 clinical update mirrors Australia’s inhaler shift, ensuring parallel volume bumps. Both countries absorb aluminum-price volatility similarly, given shared converter supply chains. Retailer sustainability rules apply identically on either side of the Tasman, giving suppliers one framework to meet.

Competitive Landscape

The Australia and New Zealand Aerosol market is moderately consolidated. Upstream, Ball and Crown supply most aluminum and steel cans, though neither discloses local shipment splits. Emerging opportunities include mass-balance recycled aluminum and refillable pressure vessels. Contract fillers that invest in digital printing and small-lot automation are well placed to capture limited-edition orders, yet face capex strain from raw-material price swings and tightening VOC rules.

Australia And New Zealand Aerosol Industry Leaders

Unilever

Henkel AG & Co. KGaA

PPG Industries Inc.

Reckitt Benckiser Group plc

S.C. Johnson & Son, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rexona unveiled its special-release 220ml sprays or aerosols in Australia, featuring three striking can designs. These designs pay homage to Rugby League, Australian Rules Football, and Rugby Union, all integrated into Rexona's new RIVALS sports competition initiative.

- February 2024: New Zealand's updated recycling standard excluded aerosol spray cans, along with their caps, lids, and bottle tops, from kerbside collections. The Palmerston North City Council highlighted health and safety concerns as the main rationale behind this decision.

Australia And New Zealand Aerosol Market Report Scope

An aerosol is a suspension of fine solid particles or liquid droplets in a gas, typically air. These microscopic, often invisible, particles are present throughout the atmosphere and originate from natural sources or human activity.

The Australia and New Zealand Aerosol market is segmented by material, application, and geography. By material, the market is segmented into steel, aluminum, and other materials. By application, the market is segmented into automotive, personal care, food products, herbicides, household products, insecticides, industrial and technical, medical, paint and coatings, and other applications. By Geography, the market is segmented into Australia and New Zealand. For each segment, market sizing and forecasts are provided on the basis of value (USD).

By Material

| Steel |

| Aluminium |

| Other Materials |

By Application

| Automotive |

| Personal Care |

| Food Products |

| Herbicide |

| Household Products |

| Insecticide |

| Industrial and Technical |

| Medical |

| Paint and Coatings |

| Other Applications |

By Geography

| Australia |

| New Zealand |

| By Material | Steel |

| Aluminium | |

| Other Materials | |

| By Application | Automotive |

| Personal Care | |

| Food Products | |

| Herbicide | |

| Household Products | |

| Insecticide | |

| Industrial and Technical | |

| Medical | |

| Paint and Coatings | |

| Other Applications | |

| By Geography | Australia |

| New Zealand |

Key Questions Answered in the Report

How fast is deodorant demand growing across Australia and New Zealand?

Personal care aerosols, mainly deodorants, are expanding at a 5.35% CAGR to 2031 as sports-themed launches and Gen-Z marketing lift unit volumes.

What propellant changes are expected after 2026?

Tightening HFC quotas push brands toward butane-propane blends, with pilot rollouts of ultra-low-GWP propellants and dry-powder inhaler formats underway.

Which can material is gaining share?

Aluminum cans are growing at 5.27% CAGR because retailers require higher recycled-content packaging, even though steel still leads total volume.

How do retailer sustainability targets affect aerosol suppliers?

Woolworths mandates at least 86% recyclability and 52% recycled content, so non-compliant SKUs risk losing promotional space or full delisting.

What is the impact of new asthma guidelines on inhaler demand?

The 2025 Australian and 2025 New Zealand guidelines switch patients to combination pMDIs, lifting aerosol inhaler volumes and ancillary spacer sales.

What is the current market size of Australia and New Zealand Aerosol Market?

The Australia and New Zealand Aerosol Market size is expected to increase from USD 1.33 billion in 2025 to USD 1.40 billion in 2026 and reach USD 1.79 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Page last updated on: