Market Overview

| Study Period | 2020 - 2031 |

|---|---|

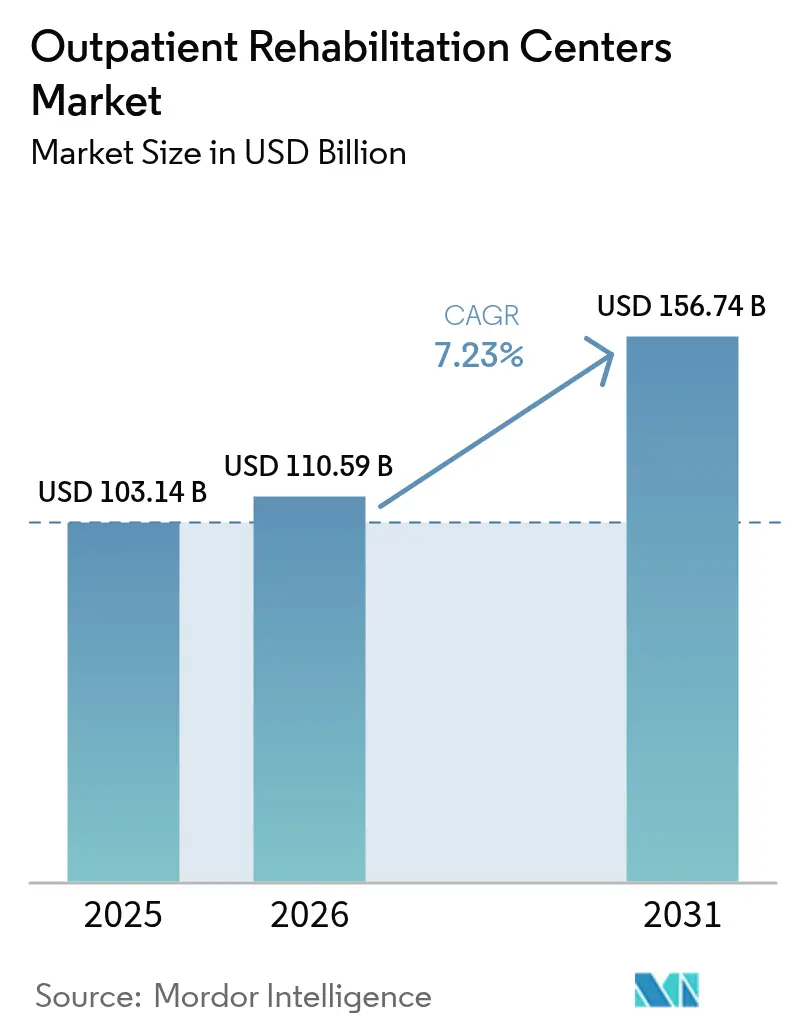

| Market Size (2026) | USD 110.59 Billion |

| Market Size (2031) | USD 156.74 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

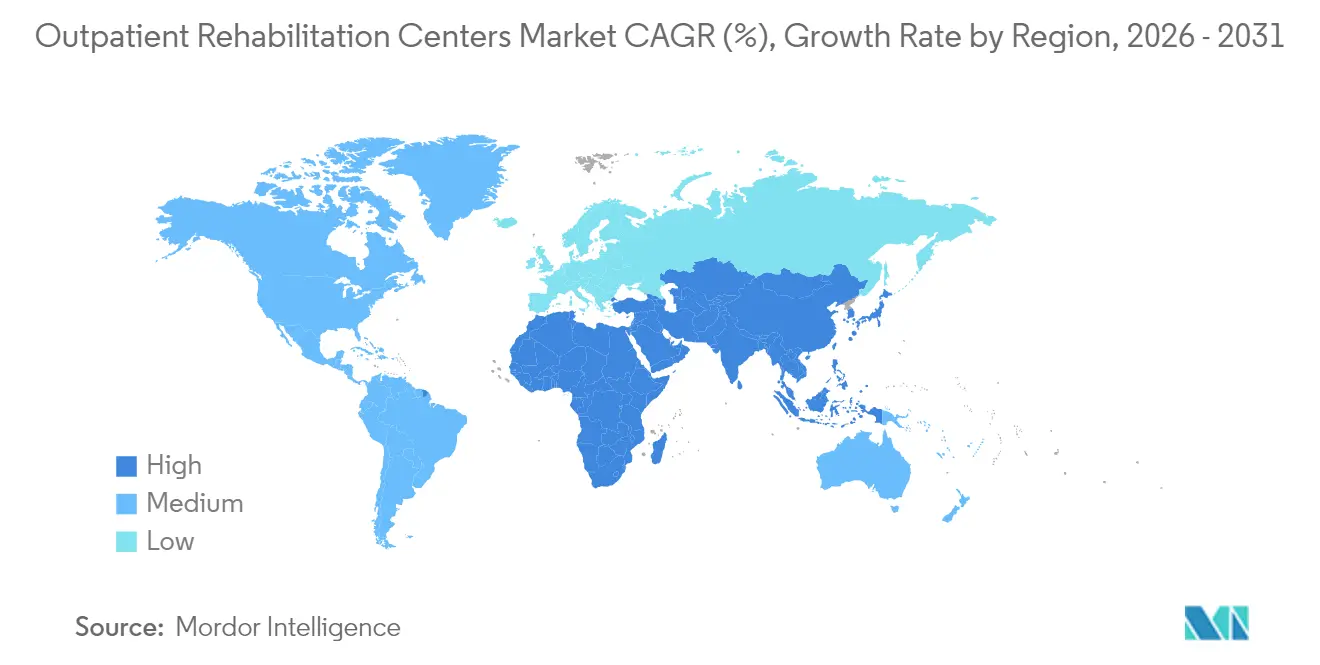

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outpatient Rehabilitation Centers Market Analysis by Mordor Intelligence

The outpatient rehabilitation centers market size is expected to grow from USD 103.14 billion in 2025 to USD 110.59 billion in 2026 and is forecast to reach USD 156.74 billion by 2031 at 7.23% CAGR over 2026-2031. This steady expansion reflects demographic aging, the surge in chronic diseases, and payer-led cost-containment that shifts volumes away from inpatient facilities. New Medicare Intensive Outpatient Program (IOP) billing codes introduced in 2024 have broadened reimbursement, while tele-rehab parity laws and employer-sponsored musculoskeletal (MSK) programs are funneling additional patient traffic into clinics. Technological adoption—from virtual reality (VR) therapy to AI-guided exercise prescriptions—continues to elevate clinical outcomes and widen provider reach. Consolidation remains an overarching theme as scale advantages help clinics absorb talent shortages and reimbursement pressure, yet the model is still largely fragmented and ripe for acquisition.

Key Report Takeaways

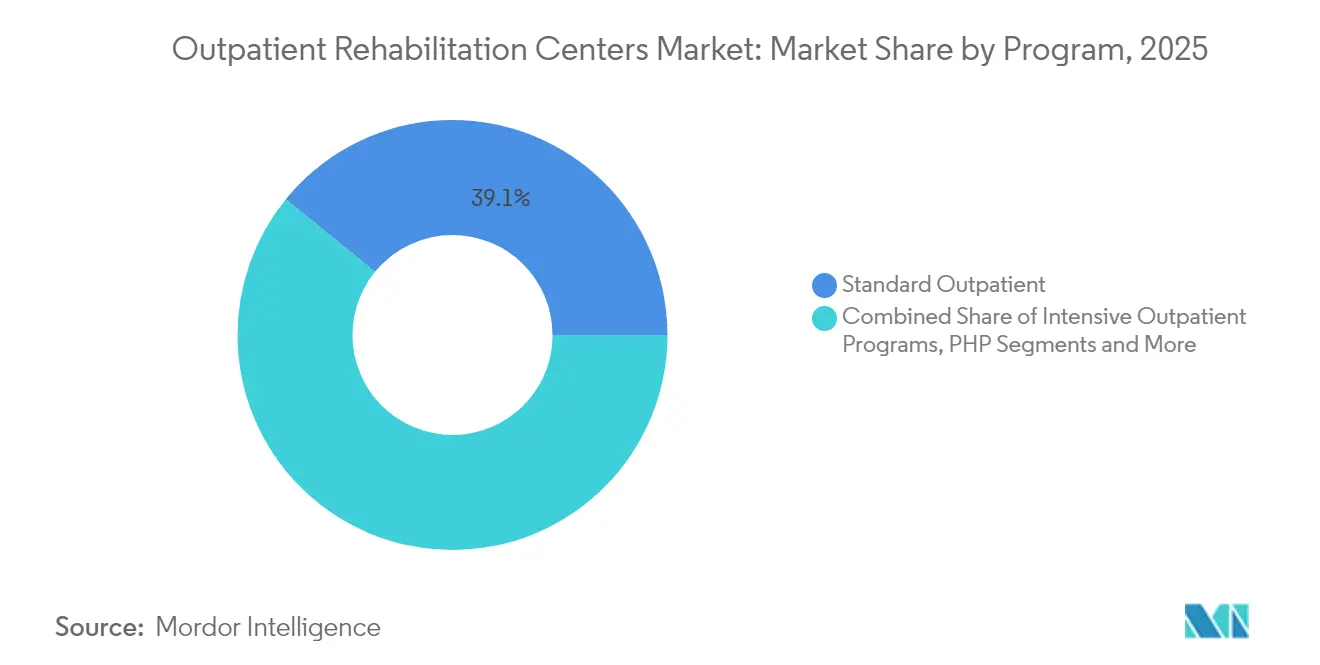

- By program, standard outpatient programs led with 39.12% of outpatient rehabilitation centers market share in 2025; hybrid tele-outpatient programs are poised for the fastest expansion at a 10.32% CAGR to 2031.

- By therapy, physical therapy held 42.31% of the outpatient rehabilitation centers market size in 2025, but VR-assisted therapy is forecast to accelerate at an 11.05% CAGR through 2031.

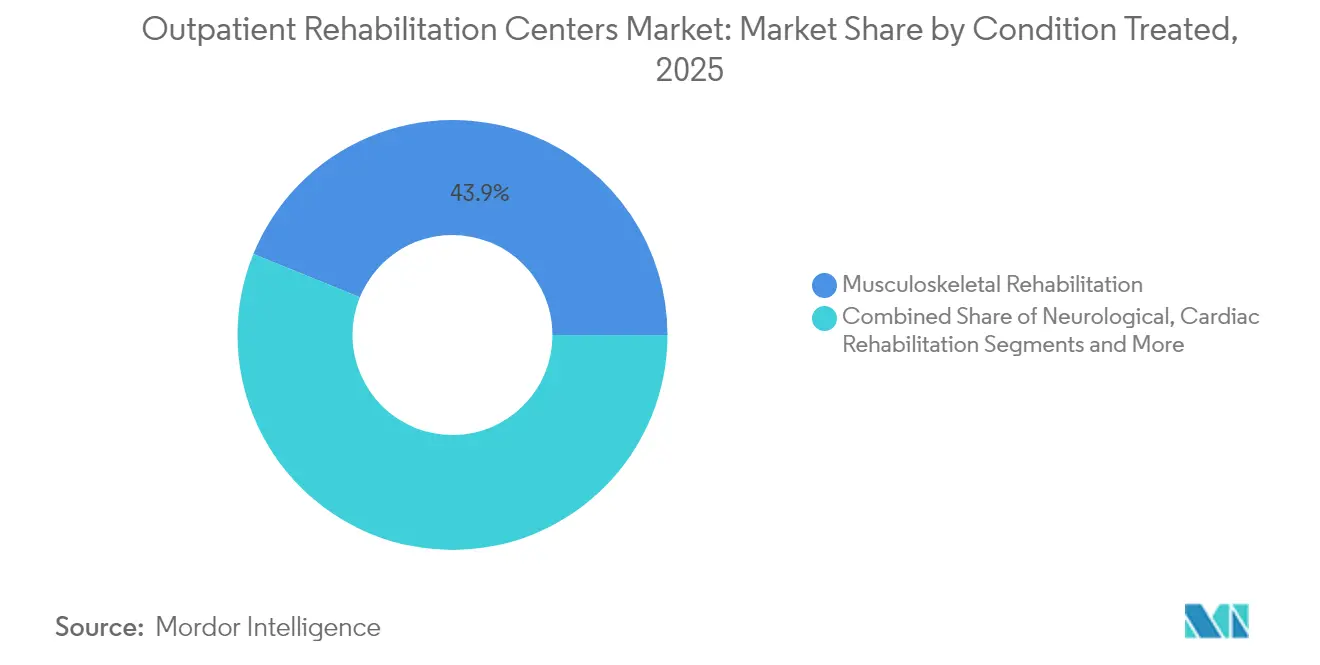

- By condition, musculoskeletal rehabilitation commanded 43.85% of outpatient rehabilitation centers market size in 2025, whereas cardiac rehabilitation will record the quickest growth at a 10.29% CAGR.

- By end user, adults represented 50.71% of 2025 volume; sports-injury patients form the most dynamic segment, expanding at a 9.11% CAGR to 2031.

- By geography, North America captured 44.05% of 2025 revenue, while Asia-Pacific is on track for the highest regional CAGR of 9.62% in the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outpatient Rehabilitation Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Ageing Population & Chronic Disease Burden | +1.8% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Cost-Shift From Inpatient To Lower-Cost Outpatient Settings | +1.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Inclusion Of Intensive Outpatient Program (IOP) Codes In Medicare (2024) | +0.9% | North America, specifically United States | Short term (≤ 2 years) |

| Tele-Rehab Parity Laws Boosting Rural Access | +0.7% | North America and Australia, rural regions | Medium term (2-4 years) |

| Employer-Sponsored MSK Programmes Driving Clinic Foot-Fall | +0.6% | North America and Europe, urban centers | Short term (≤ 2 years) |

| ACO / MSO Consolidation Accelerating Referral Volumes | +0.5% | North America, integrated health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapidly ageing population & chronic disease burden

Adults aged 65+ will exceed 20% of the U.S. population by 2030, intensifying demand for rehabilitation of arthritis, cardiovascular sequelae, and diabetes-related mobility issues. With 39% of adults already living with at least one chronic disease, payers and providers view outpatient programs as the most cost-effective long-term management setting. Clinics that bundle physical, occupational, and behavioral therapies are especially positioned to capture sustained, non-cyclical volumes.

Cost-shift from inpatient to lower-cost outpatient settings

Outpatient visits are projected to hit 5.82 billion annually by 2030, propelled by Medicare’s value-based purchasing and payer pushback against high hospital facility fees. States trimming Certificate-of-Need requirements have fueled a jump in ambulatory facility openings, widening choice for both surgeons and rehabilitation patients. Because outpatient rehabilitation costs 30-50% less than comparable inpatient episodes, commercial payers increasingly steer beneficiaries toward community clinics for post-acute recovery.

Inclusion of Intensive Outpatient Program codes in Medicare (2024)

Medicare’s new IOP codes allow hospitals, CAHs, and community mental health centers to bill at least nine hours of structured psychiatric care weekly, unlocking fresh revenue pools for rehabilitation operators embracing behavioral health.[1]Centers for Medicare & Medicaid Services, “MM13222 – New Condition Code 92: Billing Requirements for Intensive Outpatient Program Services,” cms.govInitial claims data show outpatient behavioral volumes rising in tandem, strengthening the business case for integrated physical-mental service lines.

Tele-rehab parity laws boosting rural access

Permanent telehealth parity in many U.S. states and Australia equalizes reimbursement for virtual and in-person sessions, eliminating geography as a payer hurdle. Rural Health Clinics secured rule changes that maintain flexibilities through December 2025, further easing adoption.[2]NARHC, “Rural Health Clinics Secure Major Regulatory Wins in Medicare Physician Fee Schedule Final Rule,” narhc.org By layering remote monitoring and VR coaching atop limited on-site therapy, providers can stretch scarce clinical staff across wider patient panels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Licensed Therapists & Clinicians | -1.2% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Downward Reimbursement Pressure From Private Payors | -0.8% | North America and Europe, private insurance markets | Medium term (2-4 years) |

| Rising Cyber-Security & HIPAA Compliance Costs For Tele-Rehab | -0.4% | Global, technology-dependent markets | Short term (≤ 2 years) |

| Community Zoning Restrictions On New Outpatient Sites | -0.3% | North America, urban and suburban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of licensed therapists & clinicians

A projected shortfall of 12,070 full-time physical therapists by 2037 threatens capacity, with current outpatient vacancy reaching 9.5% and rural supply at just 19% of need.[3]American Physical Therapy Association, “PTJ: New Workforce Forecast Projects PT Shortages Through 2037,” apta.org Salary inflation and retention bonuses squeeze margins for smaller independents and may slow new-site rollouts.

Downward reimbursement pressure from private payors

The 2025 Physician Fee Schedule lowers Medicare conversion factors 2.93%, signaling similar moves by commercial carriers. Prior-authorization protocols and shorter approved episode durations obligate clinics to prove outcomes quickly or absorb unreimbursed visits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Program: Hybrid Models Drive Innovation

Standard outpatient programs generated the largest share of 39.12% in 2025, underpinning the outpatient rehabilitation centers market through routine post-surgical and chronic-care visits. These clinics benefit from predictable volume streams and embedded referral pathways. Hybrid tele-outpatient programs, although nascent, are scaling at a 10.32% CAGR as patients welcome the convenience of alternating in-clinic assessments and at-home VR-guided sessions. Payers back these models when real-time data feed proves adherence and functional gains, curbing unnecessary in-person encounters and travel costs.

Hybrid formats combine traditional therapist oversight with AI-driven progress dashboards. Because reimbursement parity exists in many jurisdictions, providers can monetize digital-first follow-ups without revenue dilution. Intensive outpatient programs, newly reimbursable under Medicare, add a behavioral-health revenue layer, while partial-hospitalization and day-rehab schemes address complex neurologic and orthopedic cases needing multidisciplinary input. The upshot is a diversified service mix that cushions operators against payer or regulatory shocks.

By Therapy: VR Technology Transforms Treatment Paradigms

Physical therapy accounted for 42.31% of 2025 revenue, making it the anchor modality on which most clinics build broader service bundles. Its dominance stems from pervasive MSK and post-operative needs. VR-assisted therapy, expanding at an 11.05% CAGR, introduces immersive tasks that sharpen balance and neuro-motor control, shortening average recovery timelines. Occupational and speech therapy maintain steady demand for stroke and pediatric populations, whereas cognitive behavioral therapy and motivational interviewing open new revenue lanes in integrated substance-use and chronic-pain programs.

Therapists increasingly deploy exoskeletons and gamified VR labs to manage higher caseloads without sacrificing quality. AI-backed platforms personalize session intensity and adapt exercise scripts mid-stream, boosting adherence and outcomes. As outcome-based reimbursement tightens, clinics leveraging objective digital metrics gain favor with value-based payors.

By Condition Treated: Cardiac Rehabilitation Accelerates Growth

Musculoskeletal rehabilitation remained the largest condition category in 2025 at 43.85% because of prevalent workplace injuries and degenerative joint disease. Cardiac rehabilitation, though smaller, is outpacing all others at a 10.29% CAGR as guidelines embed rehab into secondary-prevention bundles following myocardial infarction and coronary bypass. Neuro-rehabilitation stands as a high-acuity segment requiring long episode lengths, while pulmonary and substance-use programs are expanding under integrated care protocols.

Remote patient monitoring devices now feed cardiopulmonary vitals directly into clinic dashboards, enabling therapists to titrate effort levels safely in home settings. VR-based neuro exercises demonstrate superior upper-limb gains in stroke survivors compared with conventional methods, unlocking payer support in outcome-driven contracts.

By End User: Sports Medicine Drives Premium Growth

Adults constituted 50.71% of 2025 visits and will remain the volume mainstay as chronic-care prevalence rises. Sports-injury patients, however, exhibit a 9.11% CAGR, drawn to high-tech gait labs and performance-optimization packages that carry premium price tags. Geriatric demand rises steadily as fall-prevention and osteoporosis programs extend functional independence, while pediatric rehabilitation requires developmental tailoring and family engagement.

Sports rehabilitation centers differentiate by integrating motion-capture analytics and strength-conditioning curricula, expanding revenue per patient and fueling word-of-mouth referrals among athletic communities. Workers’ compensation cases continue to supply reliable, insurer-funded caseloads focused on expedited return-to-duty metrics.

Geography Analysis

North America led the outpatient rehabilitation centers market with 44.05% revenue share in 2025, powered by broad insurance coverage, wage-adjusted reimbursement, and dense clinic networks. The United States embodies most spending, as Medicare and large commercial insurers reimburse diverse program types, including the new IOP behavioral codes. Canada supplements demand through universal coverage and rising chronic-disease prevalence, while Mexico’s growing medical tourism and employer MSK initiatives add cross-border volume.

Europe maintains mid-single-digit growth thanks to public-sector investment in community-based rehab and updated EU directives favoring home-based tele-rehab. Countries such as Germany are rolling out digital-health prescriptions reimbursed under statutory insurance, widening VR therapy acceptance. The United Kingdom’s NHS long-term plan invests in MSK hubs that coordinate surgeon, physio, and occupational therapy under value-based budgets, increasing outpatient throughput.

Asia-Pacific is the fastest-expanding region with a 9.62% CAGR, propelled by rapid population aging in China, South Korea, and Singapore, plus public–private partnerships that finance greenfield clinic builds. Governments champion AI adoption to offset therapist shortages, sparking demand for smart rehabilitation devices. Emerging markets such as India and Indonesia witness surging lifestyle disease incidence, spurring domestic chains to replicate Western outpatient models. Tele-rehab overcomes rural provider gaps and reduces capital required per patient served, accelerating geographic coverage.

South America and the Middle East & Africa present nascent yet promising landscapes. Brazil is streamlining private-insurance approvals for outpatient rehab as hospital occupancy rates climb, whereas Saudi Arabia’s Vision 2030 health agenda designates rehabilitation as a priority service. Infrastructure constraints and clinician scarcity continue to limit immediate scale, but bilateral training initiatives with U.S. and European partners are beginning to bolster capacity.

Competitive Landscape

The outpatient rehabilitation centers market remains fragmented, with the top ten operators controlling less than 20% of global revenue. Select Medical and Encompass Health expand by clustering multi-disciplinary centers near acute-care hospitals to capture bundled-payment discharges. ATI Physical Therapy focuses on employer MSK partnerships, while FOX Rehabilitation and Powerback Rehabilitation accelerate via acquisitions—FOX acquired Ageility in 2024 and Powerback bought Encore GC the same year.

Technology is now a primary differentiator. Net Health’s June 2025 acquisition of Limber Health adds remote-exercise tracking to its EHR suite, equipping small clinics with enterprise-grade data capture. DIH’s partnership with Nobis Rehabilitation deploys robotics and sensor-based gait training in inpatient-to-outpatient transitions, raising throughput without proportional headcount growth. Early adopters of VR platforms report double-digit increases in patient satisfaction scores and measurable reductions in average visits per episode, appealing to payers eyeing total-cost savings.

Value-based contracts continue to mature. Operators able to furnish real-time functional-outcome dashboards win share from independents reliant on fee-for-service models. However, capital intensity for technology rollouts and talent recruitment spurs ongoing consolidation; private-equity vehicles favor multi-state bolt-on strategies that build regional density and bargaining leverage with insurers and referring surgeons.

Outpatient Rehabilitation Centers Industry Leaders

Select Medical Holdings

AIM Health Group Inc.

LHC Group, Inc.

Trilogy Health Services, LLC.

Craig Hospital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Net Health acquired Limber Health, expanding its outpatient EHR and remote-care toolkit.

- March 2025: USPh purchased a three-clinic physical therapy practice to deepen its regional footprint.

- January 2025: DIH formed a strategic partnership with Nobis Rehabilitation Partners to broaden access to robotics-enabled therapy.

- July 2024: Blue Cross Blue Shield of Michigan launched a virtual muscle and joint program with Hinge Health, offering members 12 no-cost PT visits per year.

Global Outpatient Rehabilitation Centers Market Report Scope

As per the scope of the report, outpatient rehabilitation is an effective form of therapy for those with conditions that don't require intensive care. It has a lower cost and allows for a greater degree of freedom than inpatient therapy. Outpatient rehab is needed after many surgeries. As part of the recovery, the patient may start by getting care at a hospital. Depending on the nature or extent of the injury, the treatment might be given by physical therapists. The Outpatient Rehabilitation Centers Market is segmented by Program (Standard Outpatient Programs, Intensive Outpatient Programs, and Partial Hospitalization Programs), Therapy (Cognitive Behavioral Therapy, Contingency Management, Motivational Interviewing Treatment, The Matrix Model, and Family Therapy), End User (Pediatric Population, Adult Population, and Geriatric Population), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

By Program

| Standard Outpatient Programs |

| Intensive Outpatient Programs (IOP) |

| Partial Hospitalisation Programs (PHP) |

| Hybrid Tele-Outpatient Programs |

| Specialised Day Rehabilitation (Neuro, Cardiac, Ortho) |

By Therapy

| Physical Therapy |

| Occupational Therapy |

| Speech & Language Therapy |

| Cognitive Behavioural Therapy (CBT) |

| Contingency Management (CM) |

| Motivational Interviewing (MI) |

| Virtual-Reality-Assisted Therapy |

| Aquatic / Ocean Therapy |

By Condition Treated

| Musculoskeletal Rehabilitation |

| Neurological Rehabilitation |

| Cardiac Rehabilitation |

| Pulmonary Rehabilitation |

| Substance-Use-Disorder Rehabilitation |

| Others (Burn, Oncology, etc.) |

By End User

| Paediatric Population |

| Adult Population |

| Geriatric Population |

| Sports-Injury Patients |

| Workers’ Compensation Cases |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Program | Standard Outpatient Programs | |

| Intensive Outpatient Programs (IOP) | ||

| Partial Hospitalisation Programs (PHP) | ||

| Hybrid Tele-Outpatient Programs | ||

| Specialised Day Rehabilitation (Neuro, Cardiac, Ortho) | ||

| By Therapy | Physical Therapy | |

| Occupational Therapy | ||

| Speech & Language Therapy | ||

| Cognitive Behavioural Therapy (CBT) | ||

| Contingency Management (CM) | ||

| Motivational Interviewing (MI) | ||

| Virtual-Reality-Assisted Therapy | ||

| Aquatic / Ocean Therapy | ||

| By Condition Treated | Musculoskeletal Rehabilitation | |

| Neurological Rehabilitation | ||

| Cardiac Rehabilitation | ||

| Pulmonary Rehabilitation | ||

| Substance-Use-Disorder Rehabilitation | ||

| Others (Burn, Oncology, etc.) | ||

| By End User | Paediatric Population | |

| Adult Population | ||

| Geriatric Population | ||

| Sports-Injury Patients | ||

| Workers’ Compensation Cases | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the outpatient rehabilitation centers market?

The outpatient rehabilitation centers market stands at USD 110.59 billion in 2026.

How fast is the market expected to grow?

The market is forecast to expand at a 7.23% CAGR, reaching USD 156.74 billion by 2031.

Which program segment is growing the quickest?

Hybrid tele-outpatient programs are posting the highest growth, with a projected 10.32% CAGR through 2031.

Why is VR-assisted therapy gaining traction?

VR-assisted therapy delivers immersive, data-rich sessions that improve functional outcomes and patient engagement, fueling an 11.05% CAGR.

Which region offers the strongest growth opportunity?

Asia-Pacific is expected to grow the fastest at 9.62% CAGR thanks to healthcare modernization and supportive AI initiatives.

Page last updated on: