Cardiac Rehabilitation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

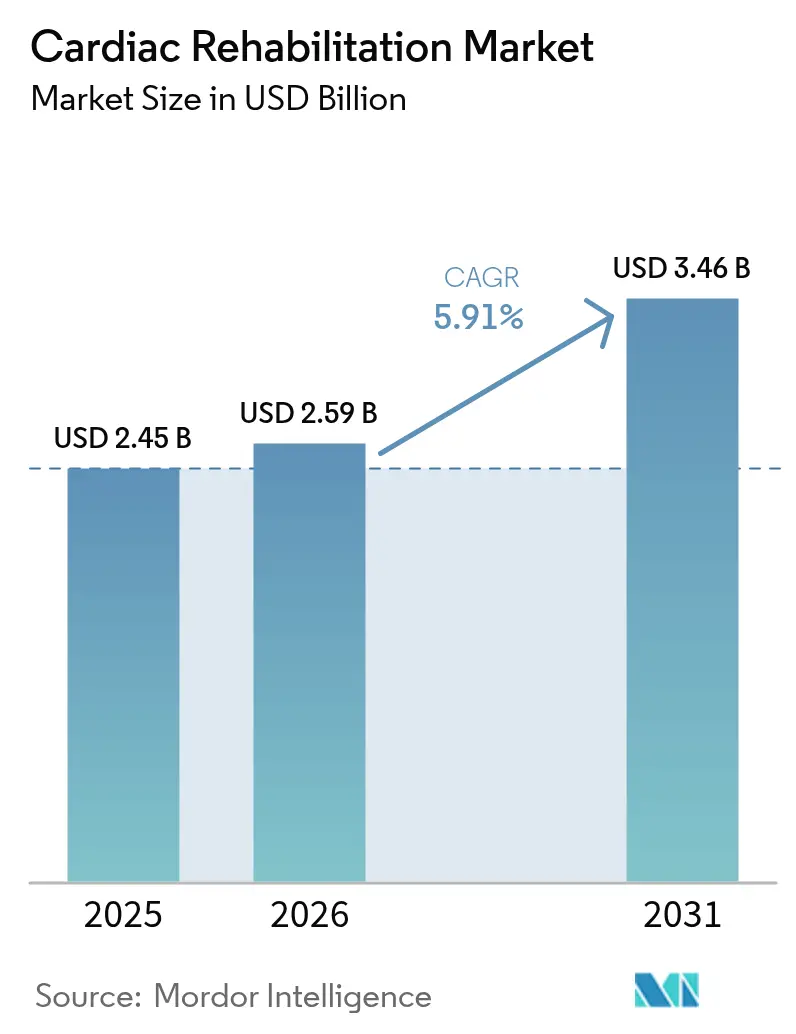

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

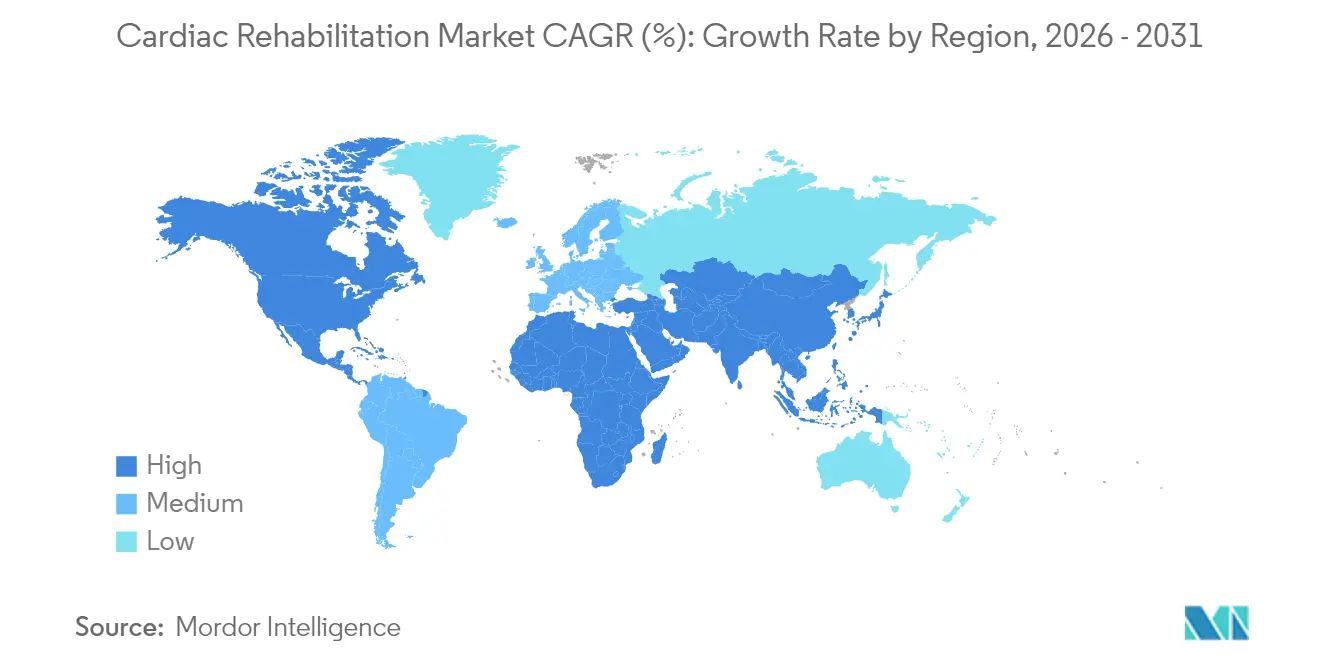

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

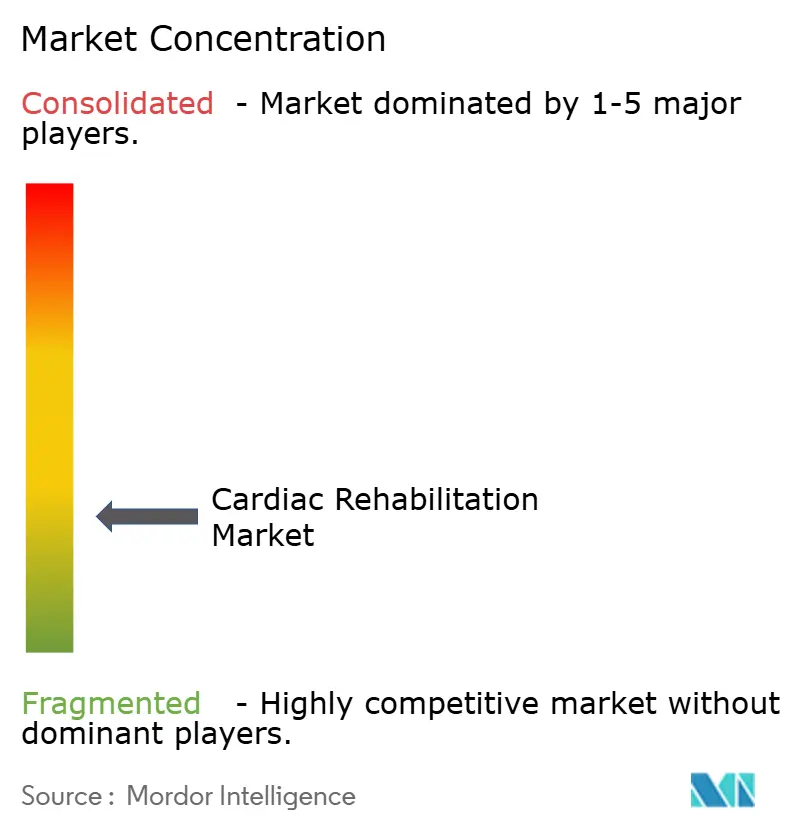

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Rehabilitation Market Analysis by Mordor Intelligence

cardiac rehabilitation market size in 2026 is estimated at USD 2.59 billion, growing from 2025 value of USD 2.45 billion with 2031 projections showing USD 3.46 billion, growing at 5.91% CAGR over 2026-2031. Rising adoption of AI-enabled feedback systems, virtual-reality exercise stations, and remote telemetry platforms is redefining care pathways and supporting consistent growth in the cardiac rehabilitation market. Connected treadmills and cycle-ergometers now feature cloud integrations that allow clinicians to adjust prescriptions in real time, while pneumatic strength machines are expanding participation among frail and elderly patients. Home-based programs are accelerating as reimbursers approve hybrid models, underscoring sustained momentum for the cardiac rehabilitation market across clinical and residential settings. Consolidation continues, with acquisitions such as ScottCare joining Marmon Holdings and partnerships like HeartBeam–AccurKardia strengthening product portfolios.

Key Report Takeaways

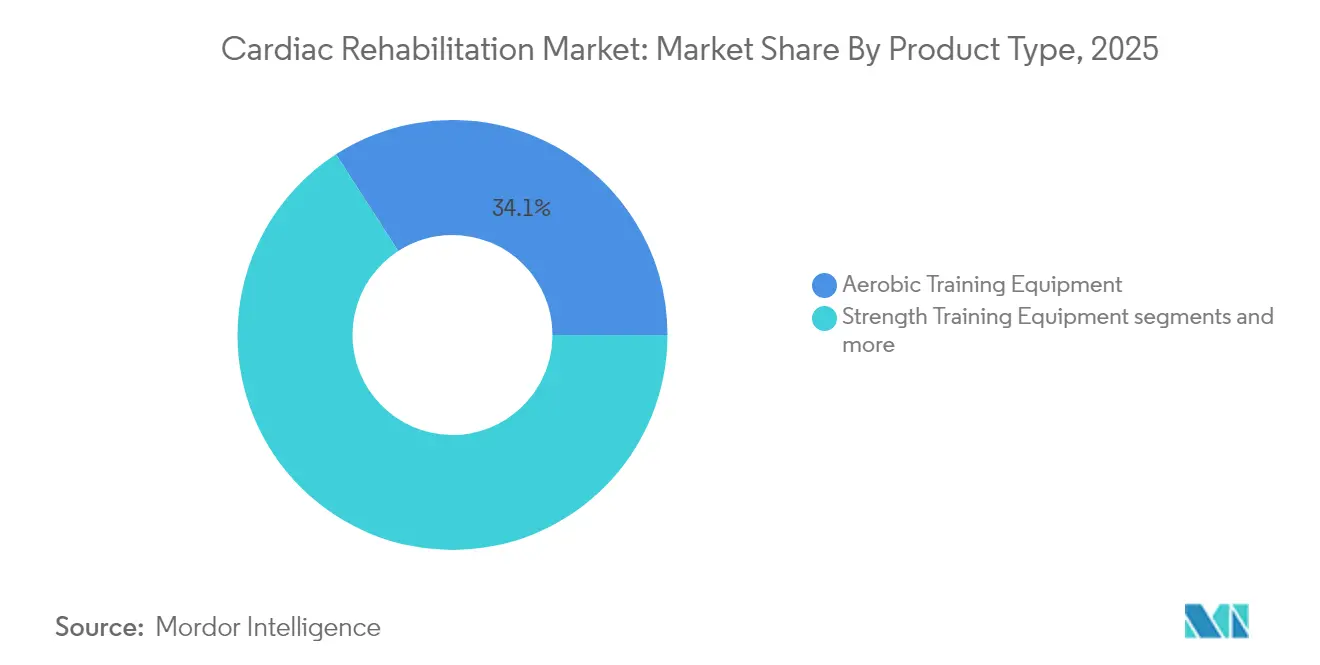

- By product type, aerobic training equipment led with 34.12% revenue share in2025, whereas emerging technologies are projected to expand at a6.15% CAGR to2031.

- By portability, fixed equipment held70.62% of the cardiac rehabilitation market share in2025, while portable solutions are advancing at a7.05% CAGR.

- By end user, hospitals captured47.25% share of the cardiac rehabilitation market size in2025, and home settings are forecast to grow at a7.34% CAGR through2031.

- By geography, North America accounted for39.05% revenue share in2025; Asia Pacific is the fastest-growing region at a6.58% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Rehabilitation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing installation of connected treadmills & cycle-ergometers in CR labs | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Integration of wearable sensors & remote telemetry into rehab devices | +1.5% | Global, accelerated in APAC markets | Short term (≤ 2 years) |

| Shift to low-impact pneumatic strength machines for frail patients | +0.8% | North America & EU core, expansion to APAC | Long term (≥ 4 years) |

| AI-enabled feedback loops boosting utilisation of home-use devices | +1.3% | Global, with premium adoption in developed markets | Medium term (2-4 years) |

| Virtual-reality rehab stations creating a new product niche | +0.7% | North America & EU initial, selective APAC rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing installation of connected treadmills& cycle-ergometers in CR labs

Real-time data capture has reshaped supervision as cloud-linked ergometers stream heart-rate, wattage, and cadence to clinician dashboards. Teams adjust workloads instantly, turning each session into a data-driven experiment that fits diverse comorbidity profiles. Automated uploads satisfy accreditation metrics, trimming paperwork and freeing staff for coaching. Gamified progress bars boost motivation, and facilities report 15% higher adherence than programs that use standalone machines. Together, these benefits position connected aerobic devices as the new standard for cardiac rehabilitation laboratories.

Integration of wearable sensors& remote telemetry into rehab devices

Continuous ECG, blood-pressure, and pulse-ox feeds now merge with equipment telemetry, giving clinicians second-by-second insight into physiologic response. Real-time analytics flag arrhythmias or unsafe pressures and can pause sessions automatically, improving safety for high-risk cohorts. Remote dashboards extend oversight to home programs, easing staffing shortages while sustaining clinical rigor. Facilities that embed telemetry report 23% lower dropout and faster attainment of goal workloads. The approach underpins scalable hybrids that blend clinic initiation with remote progression.

Shift to low-impact pneumatic strength machines for frail patients

Pneumatic resistance regulates load with compressed air, creating smooth curves that spare joints and surgical sites. This capability is vital for frail or elderly patients who face injury risk with free weights or stacks. Trials show comparable strength gains to conventional gear while cutting joint stress by 40%. Smaller footprints let facilities add more stations in tight spaces, raising throughput in urban centers. As reimbursement shifts toward functional outcomes, demand for low-impact platforms is set to accelerate

AI-enabled feedback loops boosting utilisation of home-use devices

Home-use bikes and steppers now ship with chips that ingest heart-rate, torque, and self-reported symptoms. Embedded AI adjusts resistance or cadence on the fly so patients stay within prescribed intensity zones. Alerts reach clinicians if biometrics drift outside safe ranges, enabling intervention without extra visits. Personalisation raises completion rates to 87% versus 54% for static protocols. Such results push payers toward permanent coverage for tech-enabled home rehabilitation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs for hospitals and centres | -1.80% | Global, acute in developing markets | Short term (≤ 2 years) |

| Space constraints limit deployment of large equipment | -0.90% | Urban markets globally, severe in APAC | Medium term (2-4 years) |

| Shortage of biomedical engineers for device upkeep | -1.10% | Global, critical in rural and emerging markets | Long term (≥ 4 years) |

| Lack of harmonised MDR/510(k) pathways for digital features | -0.70% | Global, regulatory fragmentation in EU-US-APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital & maintenance costs for hospitals and centres

Up-front prices for advanced treadmills, telemetry consoles, and exoskeletons can reach USD 50,000–200,000 per unit, straining tight capital budgets. Annual maintenance contracts add 8–12% of purchase cost and need on-site biomedical engineers who are scarce. Budget pressures lead 34% of hospitals to extend replacement cycles beyond manufacturer guidance, raising downtime and safety risks. Smaller community facilities fare worst because reimbursement barely covers operating cost, let alone depreciation. These realities slow refresh cycles and temper near-term demand despite clear clinical benefits.

Space constraints limit deployment of large equipment

A full cardiovascular gym needs roughly 2,500 sq ft, yet urban hospitals face escalating real-estate costs that force difficult allocation choices. Administrators often prioritise surgical suites over rehabilitation floor space, leaving programs to share crowded basements or outpatient annexes. The squeeze is acute in Asia-Pacific megacities where land premiums curb expansion of new units. Vendors now offer compact multi-function ergometers and fold-away strength stations, though higher unit prices slow uptake. Without creative space solutions, program capacity will remain capped even as patient referrals climb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innovation Anchored in Emerging Technologies

Aerobic training equipment retained 34.12% revenue in 2025, reflecting its foundational role in cardiac care. Treadmills and cycle-ergometers remain first-line interventions because extensive clinical trials prove gains in functional capacity and mortality reduction. Strength systems complement aerobic modalities, while upgraded telemetry modules link directly to electronic health records. The cardiac rehabilitation market continues to reward firms that integrate diagnostics with exercise hardware.

The emerging technologies subset posts the fastest 6.15% CAGR through 2031 as VR stations and robotic exoskeletons transition from pilot programs to commercial scale. CardioVR-ReTone exemplifies advanced exoskeleton design, combining 12 degrees of freedom with immersive scenery to sustain motivation. Gamification and motion capture redefine the user experience, helping vendors secure new reimbursements and attracting institutional buyers focused on patient engagement.

By Portability: Home-Based Solutions Gain Momentum

Fixed installations captured 70.62% revenue in 2025 thanks to full monitoring suites, crash carts, and integrated emergency protocols required for high-risk cohorts. Facilities capitalise on economies of scale and staff competencies, reinforcing the role of fixed units within the cardiac rehabilitation equipment market.

Portable systems register a 7.05% CAGR as technology miniaturisation and secure wireless channels bring clinical oversight to living rooms. Remote programs showed equivalent outcomes to on-site care at lower travel and scheduling burden. Firms now bundle connected cycle-ergometers with tablets and blood-pressure cuffs, helping providers meet participation goals during staffing shortages.

By End User: Expansion Beyond Hospital Walls

Hospitals held 47.25% of overall revenues in 2025 because phase II programs require telemetry, crash support, and immediate physician access. Integrated cardiology teams lead early adoption of AI dashboards and robotic trainers, reinforcing hospital demand for premium hardware in the cardiac rehabilitation equipment industry.

Home settings grow at a 7.34% CAGR to 2031, reflecting payer push for value-based care and patient preference for remote options. Virtual platforms cut readmissions from 43% to 15% among high-risk patients. Insurers continue to refine billing codes that encourage technology-enabled home models.

By Technology Integration: Digital Health Transforms Delivery

AI engines embedded within ergometers adjust resistance and pace at each heartbeat, ensuring workloads remain in therapeutic zones. Continuous data streams support early alerts and predictive analytics that lower adverse-event likelihood.

Telerehabilitation platforms address Japan’s low 3–7% participation rate by linking outpatient sessions to cloud dashboards, bypassing the need for on-site cardiologists. National societies endorse remote programs to widen access and align with healthy-aging policies.

Geography Analysis

North America contributed 39.05% revenue in 2025. Medicare reimbursement for virtual rehabilitation encourages hybrid models combining in-clinic baseline testing with home follow-up. Digital health start-ups such as Carda Health and Movn Health supply turnkey platforms, yet participation remains lower among women and Black seniors despite proven benefit.

Europe sustains dense infrastructure, with 90.9% of countries hosting programs and adherence touching 85%, although risk-factor modification lags expectations. EU initiatives standardise outcome reporting and encourage AI integration to personalise dosing.

Asia Pacific records the swiftest 6.58% CAGR. Japan's strict reimbursement codes limit utilisation to 3-7% of eligible patients. China has opened more than 500 centres, yet only 24% of hospitals operate active programs, constrained by affordability and distance. Regional consortia now champion telerehabilitation and low-cost portable kits to bridge service gaps.

Regulatory Landscape

In the United States, cardiac rehabilitation (CR) and intensive cardiac rehabilitation (ICR) program coverage and operational requirements are anchored in 42 CFR 410.49. This regulation defines conditions of coverage, patient eligibility, and supervision parameters that shape how facility-based and remote-supervised programs are structured. Medicare coverage limits also affect program design and equipment utilization, with standard CR generally capped at 36 sessions over 36 weeks (with a minimum duration requirement per session), while ICR coverage is limited to 72 one-hour sessions over a maximum of 18 weeks under CMS National Coverage Determination (NCD) 20.31.

Compliance and reimbursement governance remains a practical market gatekeeper. Medicare Administrative Contractors and the CMS Recovery Audit Program emphasize documentation and medical necessity for CR billing, which pushes providers and vendors toward tighter data capture, audit-ready workflows, and defensible patient selection. In June 2026, AACVPR issued provider guidance on interpreting 2026 Medicare regulatory changes affecting CR and pulmonary rehabilitation compliance, highlighting the continued importance of rule interpretation and coding discipline for sustainable hybrid delivery.

Value Chain Analysis

The cardiac rehabilitation value chain covers device OEMs for aerobic and strength equipment, telemetry/ECG monitoring, and blood pressure and metabolic monitoring, as well as software and remote telemetry platform providers and digital health developers that add coaching, dashboards, and analytics to equipment usage. These solutions are implemented by hospitals, outpatient rehabilitation centers, and specialty cardiac clinics delivering phase II services with higher-acuity monitoring. Home-setting programs, meanwhile, increasingly depend on connected peripherals, logistics support for device fulfillment, and secure data transmission.

Downstream value creation concentrates in program operations and reimbursement execution, where multidisciplinary staffing (exercise physiologists, nurses, and clinicians) pairs protocols with outcomes reporting and billing compliance. Bottlenecks persist around high equipment capex and ongoing maintenance, uneven geographic access (CR deserts), transportation barriers, and payer rules that determine whether virtual supervision and hybrid session constructs are financially viable. In January 2026, the CDCs Million Hearts program released the second edition of the Cardiac Rehabilitation Change Package, reinforcing a playbook for health systems to expand hybrid delivery and address access gaps through standardized workflows and referral-to-enrollment improvements.

Competitive Landscape

The cardiac rehabilitation market is moderately fragmented but trending toward consolidation as multinationals add rehabilitation assets to cardiovascular portfolios. Competitive advantage is moving toward software, where AI algorithms, cloud security, and analytics dashboards shape purchasing decisions.

HeartBeam integrated AccurKardia's ECG analytics to broaden its algorithm library and improve diagnostic precision. Anumana and InfoBionic.Ai link FDA-cleared ECG-AI with remote telemetry to shorten detection timelines for arrhythmias.

Digital health newcomers challenge incumbents. Recora secured USD 20 million to scale virtual programs, while ScottCare's move into Marmon Holdings injects equity for R&D and distribution. Vendors now target white-space segments such as paediatric and post-surgical applications with modular designs.

Cardiac Rehabilitation Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Omron Corporation

Core Health & Fitness, LLC

Technogym

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hybrid and virtual supervision models create a clear whitespace in markets constrained by access and staffing, particularly in CR deserts where travel burden and limited program density suppress participation. In the United States, the 2026 Medicare rule framework that permanently adds CR/ICR codes to the telehealth services list for physician office-based programs (with real-time, continuous audio-visual requirements) and enables virtual direct supervision expands addressable operating models for technology-enabled delivery. This is most relevant for vendors offering integrated telemetry, clinician dashboards, and patient coaching workflows.

Efforts to broaden who can prescribe or order rehabilitation services also point to an opportunity to reduce referral friction and accelerate enrollment, aligning with provider needs to improve throughput without proportional staff expansion. The introduction of H.R. 6894 and S. 717 (Quality Cardiac Rehabilitation Care Act of 2025) underscores ongoing legislative focus on access expansion, while national toolkits such as the Million Hearts Cardiac Rehabilitation Change Package (2026 edition) provide implementation scaffolding that health systems can use to standardize hybrid care pathways. For vendors, differentiation increasingly hinges on interoperable, audit-ready data capture, secure cloud connectivity, and multi-modal digital rehabilitation that combines wearables with supervised exercise prescriptions to meet payer and accreditation expectations.

Recent Industry Developments

- April 2026: OMRON Healthcare announced the rollout of Tricog CardioCheck (TCC) in India, integrating its ECG-enabled blood pressure monitors with an AI-enabled cardiac triage service deployed through health centers. The rollout expands upstream identification and monitoring that can feed referral pipelines into structured cardiac rehabilitation. It also strengthens OMRONs positioning in connected cardiovascular home monitoring ecosystems.

- March 2026: Royal Philips launched IntraSight Plus, an interventional guidance platform for percutaneous coronary interventions that is FDA 510(k) cleared and CE marked. While centered on cath lab workflows, the platform supports more integrated coronary care pathways. That integration can increase downstream demand for post-procedure rehabilitation programs that rely on connected monitoring and structured exercise progression.

- September 2024: Pritikin ICR acquired Chanl Health to expand hybrid outpatient rehabilitation services. The acquisition adds scale and operational capability in hybrid delivery. It reinforces competitive momentum toward programs that blend in-clinic evaluation with technology-enabled follow-up outside the facility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cardiac rehabilitation market is defined as the revenue generated from structured rehab programs and the commonly used supporting equipment and monitoring tools that help cardiac patients recover and reduce repeat events.

Scope exclusions: We exclude acute cardiology procedures, prescription drugs, and general fitness equipment that is not purchased or used as part of a cardiac rehab plan.

Segmentation Overview

- By Product Type (Value)

- Aerobic Training Equipment

- Treadmills

- Upright / Recumbent Bikes

- Arm-Ergometers & Rowers

- Strength Training Equipment

- Pneumatic Weight Machines

- Resistance Bands & Training Balls

- Monitoring & Feedback Devices

- ECG/Telemetry Systems

- Blood-Flow & Metabolic Monitors

- Emerging Technologies

- VR-based Rehab Stations

- Robotics & Exoskeletons

- Aerobic Training Equipment

- By Portability (Value)

- Fixed (Facility-based)

- Portable / Home-use

- By End-User (Value)

- Hospitals

- Rehabilitation Centres

- Specialty Cardiac Clinics

- Home Settings

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the baseline demand picture for cardiac rehab and to keep assumptions realistic before field checks. We reviewed public disease burden and outcomes data, along with rehabilitation and secondary prevention guidance, to estimate how many patients are clinically eligible and how care pathways typically flow.

Sources included non-paywalled references such as CDC cardiovascular statistics, WHO health datasets, OECD health indicators, CMS utilization and payment references, and American Heart Association scientific statements, along with hospital and clinic publications, peer-reviewed journals, and reputable press. We also used general company filings and investor presentations to understand product mix and reported trends, and a paid subscription for company financials and intelligence plus a patent database for technology direction checks. These examples are not exhaustive, and we also used many other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating adoption realities across equipment suppliers, rehab program operators, clinicians, and channel partners that support hospital and outpatient settings. We tested key assumptions like program participation, shift toward home-based and hybrid models, replacement cycles, and average selling prices for monitoring and training equipment, and we cross-checked whether these patterns differed across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 22% | Managers: 55% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build that uses cardiovascular prevalence and event volumes, then applies expected referral and participation rates in structured rehab programs. Once the treated cohort is estimated, spending is allocated across commonly used rehab equipment and monitoring tools using typical program set-up patterns and observed replacement behavior.

To keep the model grounded, we cross-check totals with selective bottom-up approximations, such as sampled ASP multiplied by estimated units in active centers, and channel checks on portable monitoring device shipments into rehab and home settings. Inputs that matter in this market include eligible patient volumes, Phase II and Phase III participation rates, average sessions per patient, adoption of remote monitoring for home programs, equipment replacement cycles, and regional reimbursement and coverage signals.

Forecasts are developed using scenario analysis, with base, conservative, and adoption-led cases built around participation growth, mix shift to hybrid delivery, and price movement by product category. Where bottom-up inputs are thin, we use center density proxies and coverage-adjusted adoption ratios, then validate those ratios again through follow-up expert calls.

Data Validation & Update Cycle

Outputs are validated through several checks so the final number stays consistent with real-world signals. We compare modeled spending with independent indicators such as center counts, reported utilization trends, and observed pricing ranges, and then investigate any large variances before sign-off.

A second analyst review is completed for assumption logic, arithmetic integrity, and year-over-year movement. Respondents are re-contacted when new policies, major product launches, or guideline changes could alter adoption. The report is refreshed annually, with interim updates for material events, and a final pre-delivery review is done to ensure the latest public data and market signals are reflected.

Mordor Intelligence's Cardiac Rehabilitation Market Size Versus Other Published Estimates

Published market values for cardiac rehabilitation can differ because each publisher draws the line differently on what counts as rehab spend, and because participation assumptions vary by region and by care setting. Timing also matters, since some estimates lock a base year early, and others incorporate newer adoption signals like hybrid programs and remote monitoring.

Some external figures expand the scope to include broad digital health platforms and wider cardiac care services. In Mordor Intelligence, the total is limited to structured cardiac rehab programs and the supporting equipment and monitoring devices that are directly used to deliver and track rehab, and adjacent cardiology treatment costs are kept out.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.59 B (2026) | |

| Global Consultancy A | USD 2.50 B (2024) | Uses an earlier base year and a broader product mix that explicitly emphasizes wearables and homecare buckets, which can pull in wider remote monitoring spend beyond structured rehab program delivery. |

| Regional Consultancy B | USD 1.79 B (2024) | Leans more toward program and service type definitions, with limited visibility on equipment and monitoring device revenue capture and less transparent alignment to center density and participation rates by region. |

The comparison shows that the spread is mainly driven by scope choices, base-year timing, and how participation and home-based adoption are translated into dollars. By tying demand to eligible patient pools, participation behavior, and practical equipment and monitoring usage, the final estimate stays traceable to clear drivers and can be repeated as those inputs change.

Key Questions Answered in the Report

What is the current value of the cardiac rehabilitation market?

The cardiac rehabilitation market size reached USD 2.59 billion in 2026 and is projected to grow steadily to USD 3.46 billion by 2031.

Which product segment holds the largest share?

Aerobic training equipment accounted for 34.12% of 2025 revenues, reflecting its continued central role in exercise-based therapy.

Why are portable devices gaining traction?

Portable systems support home-based programs that improve access, cut travel time, and achieve comparable clinical outcomes to facility care, driving a 7.05% CAGR through 2031.

Which region is expanding the fastest?

Asia Pacific leads growth with a 6.58% CAGR as telerehabilitation and AI tools help overcome low participation rates in traditional programs.

How is artificial intelligence used in cardiac rehabilitation?

In 2025, the North America accounts for the largest market share in Cardiac Rehabilitation Market.

Page last updated on: