Speech Therapy Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

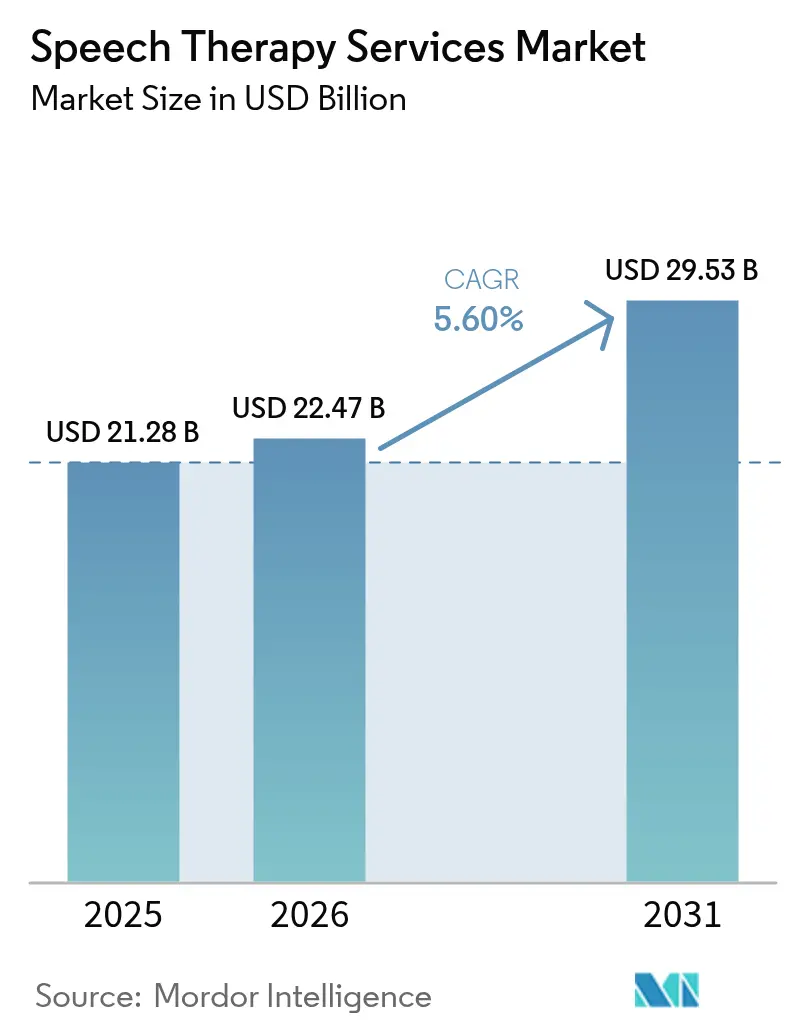

| Market Size (2026) | USD 22.47 Billion |

| Market Size (2031) | USD 29.53 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

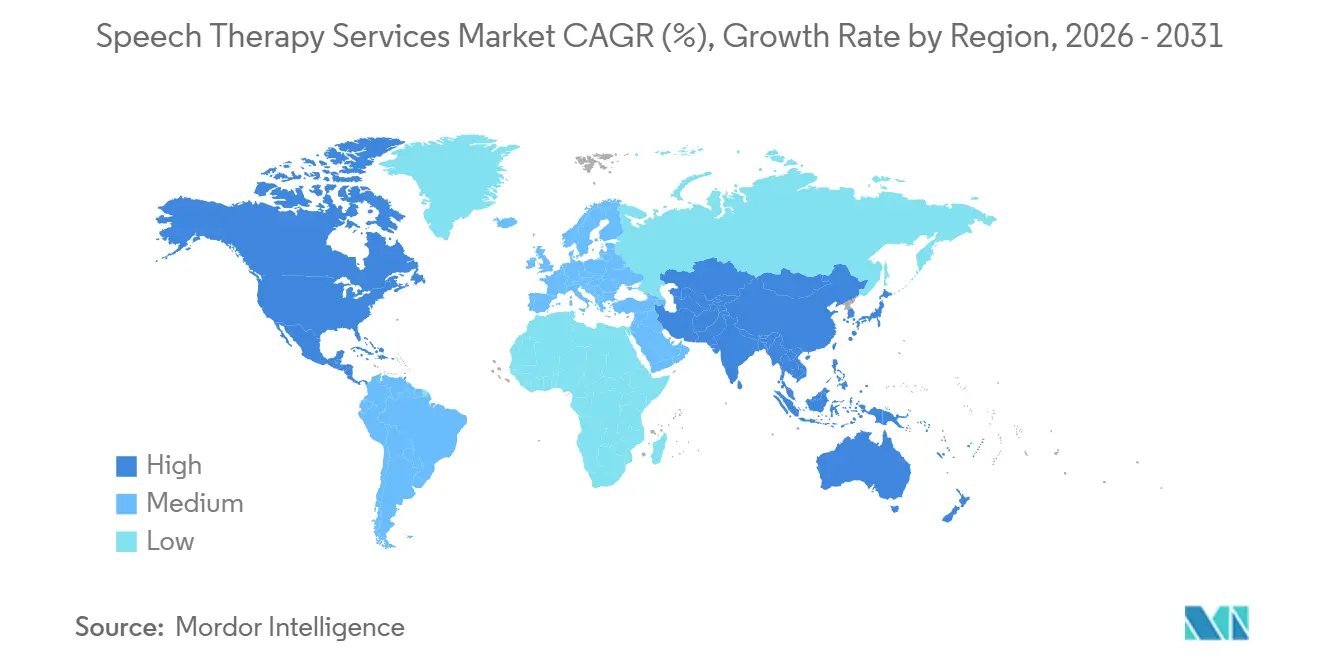

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Speech Therapy Services Market Analysis by Mordor Intelligence

The speech therapy services market size is expected to grow from USD 21.28 billion in 2025 to USD 22.47 billion in 2026 and is forecast to reach USD 29.53 billion by 2031 at 5.6% CAGR over 2026-2031. Pervasive screening programs, the rapid spread of virtual care, and AI-driven diagnostic innovation are generating resilient demand, while demographic shifts—especially a larger pediatric cohort diagnosed with autism spectrum disorder (ASD) and an expanding pool of post-stroke older adults—anchor the long-term growth trajectory of the speech therapy services market [1]Fangyuan Cao, "Speech and language biomarkers for Parkinson’s disease prediction, early diagnosis and progression," NPJ, nature.com. Providers are redesigning service models around value-based reimbursement, hybrid in-clinic/virtual pathways, and home-health therapy that emphasizes continuous monitoring. Competition remains diffuse, although regional consolidation is accelerating as larger chains buy independent clinics to capture scale, data, and technology advantages. Workforce shortages in speech-language pathology and minor reimbursement cuts in the United States create short-run cost pressure, yet digital tools that automate documentation and objective voice analytics partially offset labor gaps and support sustainable margins across the speech therapy services market.

Key Report Takeaways

- By age group, pediatric services led with 52.85% share of the speech therapy services market in 2025, whereas geriatric services are advancing at a 6.45% CAGR to 2031.

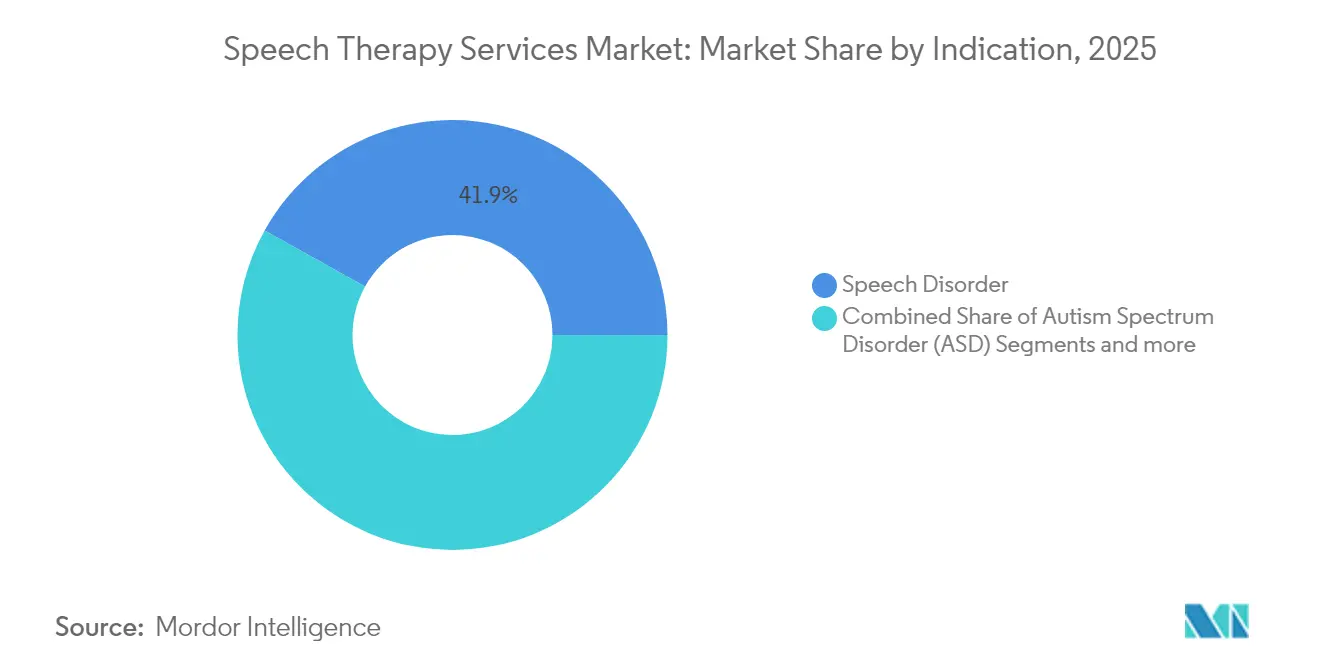

- By indication, speech disorders held 41.92% of the speech therapy services market share in 2025, while autism spectrum disorder interventions are expanding at a 6.41% CAGR through 2031.

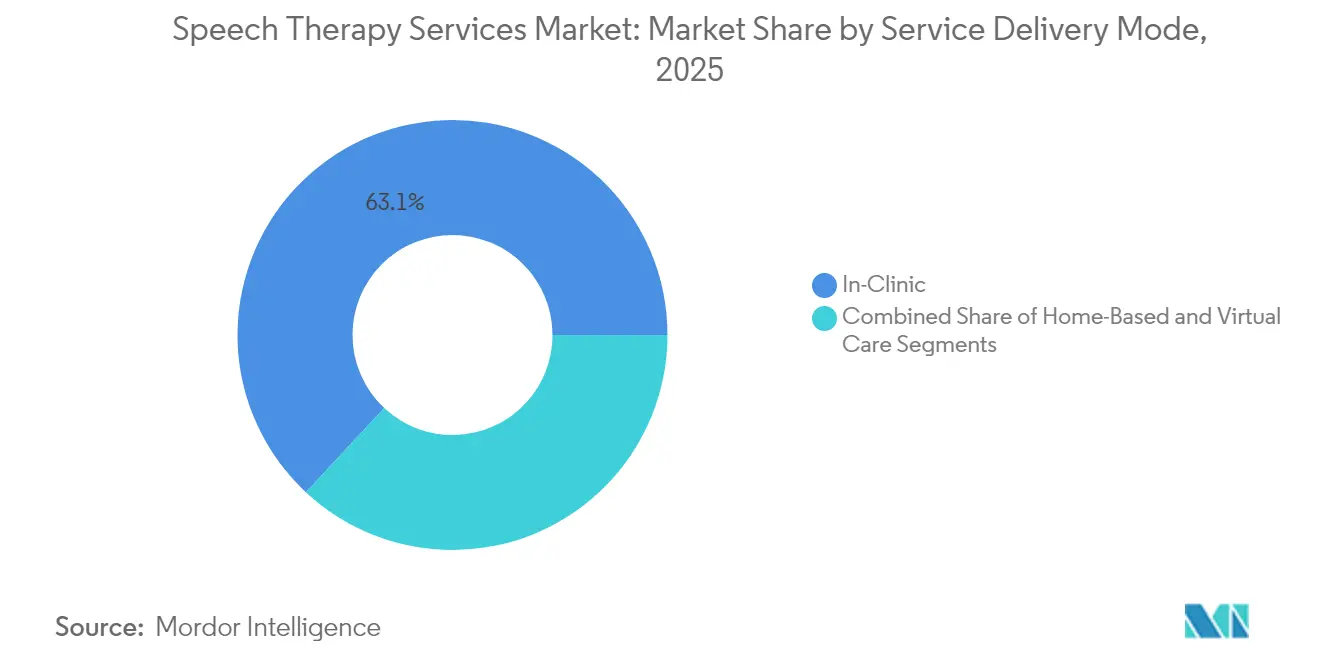

- By service delivery mode, in-clinic therapy captured 63.05% of the 2025 speech therapy services market size, whereas virtual care platforms are growing at a 6.5% CAGR to 2031.

- By end-user, hospitals and outpatient rehabilitation centers accounted for 39.42% of the speech therapy services market size in 2025, and home-health therapy is projected to rise at a 6.55% CAGR during the forecast period.

- By geography, North America commanded 41.98% of 2025 revenue, yet Asia-Pacific is posting the fastest 6.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Speech Therapy Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing screening for speech & hearing impairment in newborns | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rapid uptake of school-based tele-speech platforms | +0.8% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Growing geriatric population with post-stroke & neuro-degenerative dysphagia | +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| AI-enabled early voice analytics for Parkinson's & ASD detection | +0.4% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Growing awareness about speech therapy | +0.3% | Global, accelerating in emerging markets | Long term (≥ 4 years) |

| Value-based reimbursement pilots linking outcomes to payer bonuses | +0.2% | North America core, EU pilot programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Screening for Speech & Hearing Impairment in Newborns

Mandatory universal newborn hearing screening laws in 44 countries are unlocking earlier referral pipelines for pediatric speech therapy, ensuring that children receive intervention when neuroplasticity is at its peak [2]World Health Organization, “Newborn and Infant Hearing Screening,” who.int . Automated otoacoustic emission devices now incorporate AI voice-pattern modules that signal potential articulation delays inside the first six months of life. Longitudinal studies show that children enrolled in therapy before age 2 achieve 70-90% correction in speech sound disorders, far outpacing outcomes for those who start after preschool. Earlier detection also reduces downstream education spending, because timely therapy cuts the incidence of grade-retention and special-education placement. Providers therefore view neonatal screening as the most reliable top-of-funnel mechanism for steady, predictable utilization across the speech therapy services market. Government payers increasingly bundle newborn auditory screening with speech-language referral codes, ensuring reimbursement certainty that further propels provider participation.

Rapid Uptake of School-Based Tele-Speech Platforms

Sixty-four percent of U.S. school districts report unfilled speech-language pathology positions, a gap that tele-speech solutions are closing by streaming certified therapists directly into classrooms. Virtual platforms eliminate geographic hiring limits, letting rural districts comply with federal Individuals with Disabilities Education Act timelines even amid talent shortages. Since 2020, Medicaid and private payers have added new tele-speech billing codes, making school-based virtual sessions financially sustainable. Cloud-hosted therapy rooms also create high-quality data logs that track articulation gains, improving Individualized Education Program compliance and fostering outcome-based reimbursement pilots. The scalability of tele-speech allows providers to schedule back-to-back sessions across time zones, lifting clinician productivity by 20-25%—a critical efficiency gain in the speech therapy services market. Simultaneously, students become comfortable with video-mediated interactions, a skill transferable to future telehealth encounters across other disciplines.

Growing Geriatric Population with Post-Stroke & Neuro-Degenerative Dysphagia

A stroke occurs every 40 seconds in the United States, and nearly half of survivors require dysphagia rehabilitation to curb aspiration pneumonia risk. Nursing-home audits reveal swallowing-disorder prevalence as high as 75% among residents with advanced dementia. Because dysphagia extends hospital stays by up to seven days, pay-for-performance models are rewarding providers that deploy early speech therapy to accelerate discharge [3]Centers for Disease Control and Prevention, “Stroke Facts 2025,” cdc.gov . Videofluoroscopic swallow studies and flexible endoscopic evaluations now guide precision-based therapy, while surface electromyography and transcranial magnetic stimulation tools offer novel neuromuscular re-education pathways. These advances make swallowing therapy one of the highest-value interventions for geriatric care payers, reinforcing robust volume across the speech therapy services market. As life expectancy rises, multi-morbidity grows, anchoring a decade-long tailwind for dysphagia-oriented speech therapists.

AI-Enabled Early Voice Analytics for Parkinson’s & ASD Detection

Machine-learning models that analyze micro-tremors in vowel articulation achieve up to 99% diagnostic accuracy for early Parkinson’s disease screening, years before motor symptoms emerge. Similar acoustic-signature systems distinguish ASD-related prosody patterns, allowing pediatricians to route toddlers to therapy sooner, when cognitive-linguistic plasticity is highest. SaaS voice-biomarker engines operate through smartphones, widening reach in low-resource regions that lack neurologists or developmental pediatricians. Providers using these AI tools report 15-20% faster case identification, directly enlarging the speech therapy services market funnel. Moreover, conversational voice cloning technology restores an individual’s authentic vocal timbre during aphasia treatment, boosting patient engagement and psychosocial well-being. Payers appreciate the technology’s low cost and strong predictive value, trends that entrench AI analytics as a mainstream diagnostic adjunct by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low public awareness in emerging markets | -0.7% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Chronic shortage & high burnout of certified SLP workforce | -0.5% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Inconsistency in service quality | -0.3% | Global, pronounced in fragmented markets | Medium term (2-4 years) |

| Insurer session-caps & pre-auth hurdles for long-term therapy | -0.4% | North America & EU core markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Public Awareness in Emerging Markets

In many lower-middle-income economies, parents attribute delayed speech to cultural or spiritual factors rather than neurodevelopmental conditions, postponing intervention and shrinking therapeutic windows. Urban private hospitals offer high-quality services, yet rural districts seldom employ certified speech-language pathologists, forcing families to travel long distances for care. Governments are gradually integrating communication-screening modules into national child-wellness checklists, but resource constraints slow roll-out. Foreign aid agencies have begun sponsoring speech therapy diploma programs, though graduate output remains below minimum workforce density thresholds recommended by the World Health Organization. Until awareness, professional supply, and insurance coverage converge, the speech therapy services market in emerging regions will underperform its demographic potential.

Chronic Shortage & High Burnout of Certified SLP Workforce

The U.S. Bureau of Labor Statistics projects 13,700 annual openings for speech-language pathologists between 2025 and 2035, yet university programs confer only 9,400 master’s degrees per year, creating a widening gap. Heavy caseloads, administrative paperwork, and stagnating wages accelerate burnout, driving attrition rates that exceed 9% in public-school settings. While tele-practice platforms redistribute talent, virtual service still requires licensed clinicians, so technology cannot fully neutralize shortages. Some states now allow assistant-level practitioners under remote supervision, but scope-of-practice limitations restrain productivity gains. In Europe, cross-border credentialing differences hinder labor mobility, aggravating regional inequities. Unless governments expand graduate-program seats and simplify licensure reciprocity, supply constraints will temper growth across the speech therapy services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: ASD Drives Therapeutic Innovation

The autism spectrum disorder sub-segment is registering a 6.41% CAGR, the fastest within the speech therapy services market, propelled by earlier diagnosis protocols and near-universal U.S. insurance mandates that bundle speech therapy into Applied Behavior Analysis plans. Speech disorders, however, continued to contribute the largest 41.92% share of the speech therapy services market size in 2025, reaffirming their centrality to day-to-day clinical volume.

Digital therapeutics supplement traditional articulation drills by gamifying turn-taking and prosody training, broadening home practice adherence. Augmentative and alternative communication (AAC) apps further extend functional communication for minimally verbal individuals, expanding billable intervention hours. Interdisciplinary teams combining behavior analysts and speech-language pathologists yield holistic outcomes, strengthening clinical value propositions. With smartphone penetration exceeding 70% in most OECD markets, mobile-delivered ASD speech modules scale efficiently, making this indication a cornerstone of future growth in the speech therapy services market.

By Age Group: Geriatric Surge Reshapes Service Models

Pediatric clients dominate usage at 52.85% in 2025, yet the geriatric cohort is expanding at 6.45% CAGR, reshaping staffing mixes and clinical protocols. Speech therapists now receive dysphagia-specific credentialing to handle complex swallowing cases tied to stroke, Parkinson’s disease, and frailty.

Because older adults often present with multiple comorbidities, speech therapy sessions are increasingly coordinated with dietitians and occupational therapists to ensure consistent care plans. Home-health agencies embed portable endoscopic devices that facilitate bedside swallowing assessments, reducing hospital readmissions—a key metric under value-based purchasing. Reimbursement agencies reward post-acute providers that demonstrate reduced aspiration-pneumonia incidence, encouraging more facilities to expand clinician rosters. This systemic incentive cycle feeds sustained volume expansion for geriatric speech services, thereby widening the speech therapy services market size attributable to senior care.

By Service Delivery Mode: Virtual Care Accelerates Access

In-clinic therapy retained 63.05% revenue share in 2025; however, virtual sessions are progressing at a 6.5% CAGR, making them the fastest-growing delivery channel in the speech therapy services market. Post-pandemic regulatory waivers allow Medicare tele-speech billing through December 2025, and bipartisan bills aim to convert those flexibilities into permanent statutes.

Families appreciate reduced drive times and schedule flexibility, and clinicians report 15% lower no-show rates in virtual settings. AI-powered transcription automates SOAP notes, adding 2–3 available patient slots per day per therapist. Hybrid models that alternate in-person and virtual modalities provide comprehensive assessment without compromising convenience. As 5G coverage expands, low-latency video will further improve acoustic fidelity, essential for diagnosing subtle phonological errors. These dynamics cement tele-speech as a long-term growth lever within the broader speech therapy services market.

By End-User: Home-Health Leads Growth Transformation

Hospitals and outpatient rehabilitation centers accounted for 39.42% share of the speech therapy services market in 2025, yet home-health therapy is projected to climb at a 6.55% CAGR over the study horizon. Value-based purchasing programs reimburse agencies based on functional-communication gains and 30-day readmission rates, aligning incentives toward intensive home-based therapy after discharge.

Portable biofeedback devices now document articulation metrics in real time, letting therapists remotely adjust programs between visits and satisfy outcome-tracking mandates. Family caregivers, trained via micro-learning video libraries, extend practice hours beyond scheduled sessions, accelerating progress. Pediatric home-health particularly benefits children with mobility-limiting conditions such as cerebral palsy, while geriatric home therapy accommodates clients who struggle with clinic travel due to transportation or energy constraints. These operational and patient-centric advantages ensure that home-health remains the highest-growth end-user slice of the speech therapy services market.

Geography Analysis

North America preserved its leadership with 41.98% of global revenue in 2025, buoyed by comprehensive insurance frameworks, state mandates for school-based services, and an entrenched culture of early intervention. The region also records one of the highest virtual-care uptakes, supported by reliable broadband penetration and favorable payer policies that underpin continual expansion of the speech therapy services market. Providers leverage robust electronic medical-record ecosystems that furnish outcome data essential for pay-for-performance contracts, consolidating North America’s competitive advantage.

Europe forms a mature, quality-standardized arena where universal healthcare systems cover speech therapy as a core rehabilitation service. Rigorous professional certification under the European Speech and Language Therapy Association guarantees consistent care quality, stabilizing reimbursement trust. Despite slower macroeconomic growth, targeted investments in geriatric swallowing programs and refugee-language integration services help maintain steady volumes. Cross-border tele-speech initiatives further optimize resource allocation by routing patients to surplus therapist capacity across member states, reinforcing operational efficiency within the regional speech therapy services market.

Asia-Pacific is accelerating at a 6.62% CAGR and is positioned to become the principal incremental revenue engine by 2031. China’s 14th Five-Year Plan prioritizes rehabilitation medicine, catalyzing public-hospital spending on speech laboratories and equipment. India’s Ayushman Bharat scheme adds secondary and tertiary-care entitlements that indirectly reimburse speech therapy, extending access to lower-income groups. Japan faces rapid population aging, fostering demand for post-stroke dysphagia services, while Australia’s National Disability Insurance Scheme continues to allocate flexible funding for ASD interventions. Tele-practice essentially leapfrogs infrastructure gaps, knitting together multilingual clinician networks that span the region and fueling heightened competition inside the speech therapy services market.

Competitive Landscape

The speech therapy services market remains fragmented; the top five U.S. providers control less than 15% of national revenue, granting ample room for roll-ups and multi-state platform formation. The Ensign Group’s 2024–2025 acquisition of 15 post-acute facilities, raising its footprint to 343 operations, underscores the sector’s consolidation momentum. Chain operators benefit from payer negotiations, centralized marketing, and shared technology stacks that smaller clinics cannot afford, nudging independent practices toward affiliation or sale.

Technology is emerging as a principal differentiator. Expressable’s USD 26 million Series B funding round is earmarked for AI-infused progress-tracking dashboards and multilingual therapy modules, reflecting investor confidence in virtual-first business models. Competitors are rushing to embed voice-biomarker analytics and automated documentation software to win contracts under outcome-linked reimbursement. Those unable to assemble capital for tech upgrades risk margin compression as payers favor data-rich providers.

Workforce dynamics compound competitive pressure. Larger groups negotiate tuition-repayment deals with graduate programs and operate internal residency tracks, while smaller clinics struggle to fill vacancies. International recruitment programs in the United Kingdom and Canada source talent from the Philippines and South Africa, but regulatory credentialing delays impede rapid onboarding. Therefore, scalability, technology adoption, and robust hiring pipelines collectively shape long-run market positioning in the speech therapy services market.

Speech Therapy Services Industry Leaders

-

SPEECH THERAPY SOLUTIONS, INC.

-

John McGivney Children's Centre

-

Speechpathway.net

-

Speech Plus

-

Speech Therapy Services London Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UnitedHealthcare Community & State launched an enhanced virtual speech-language pathology program through Expressable, adding interpretation in 250+ languages and improving rural access.

- January 2025: The Ensign Group expanded into Alabama and Tennessee, bringing its facility count to 343 and widening its speech therapy footprint across the Southeast.

- May 2024: Expressable secured USD 26 million in Series B funding led by HarbourVest Partners to scale its virtual therapy platform and hire additional clinicians

Global Speech Therapy Services Market Report Scope

As per the scope of the report, speech therapy is an intervention service that focuses on improving a patient's speech and abilities to understand and express language, including nonverbal language.

The speech therapy services market is projected to record a CAGR of 5.9% during the forecast period. The speech therapy services market is segmented by indication (speech disorder, language disorder, autism spectrum disorder, and other indications), age group (geriatric, adult, and pediatric), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Speech Disorder |

| Language Disorder |

| Autism Spectrum Disorder (ASD) |

| Other Indications |

| Pediatric |

| Adult |

| Geriatric |

| In-Clinic |

| Home-Based |

| Virtual Care |

| Hospitals and Out-patient Rehab Centers |

| Schools and Early-intervention Programs |

| Long-term Care Facilities |

| Home-Health |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Speech Disorder | |

| Language Disorder | ||

| Autism Spectrum Disorder (ASD) | ||

| Other Indications | ||

| By Age Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Service Delivery Mode | In-Clinic | |

| Home-Based | ||

| Virtual Care | ||

| By End-User | Hospitals and Out-patient Rehab Centers | |

| Schools and Early-intervention Programs | ||

| Long-term Care Facilities | ||

| Home-Health | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the speech therapy services market?

The speech therapy services market size reached USD 22.47 billion in 2026 and is projected to climb to USD 29.53 billion by 2031 at a 5.6% CAGR.

Which segment is expanding the fastest?

Autism spectrum disorder interventions are growing at a 6.41% CAGR, the highest among all indications.

How quickly is virtual speech therapy growing?

Virtual care platforms are advancing at a 6.5% CAGR, outpacing traditional in-clinic growth.

Which region shows the strongest future growth momentum?

Asia-Pacific is forecast to lead regional gains with a 6.62% CAGR through 2031.

What is the biggest operational challenge facing providers?

A chronic shortage of certified speech-language pathologists, compounded by high burnout rates, continues to restrain capacity.

How are value-based reimbursement models affecting the market?

Outcome-linked bonuses are encouraging providers to document measurable communication gains, raising demand for digital progress-tracking tools.

Page last updated on: