Cool Roof Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

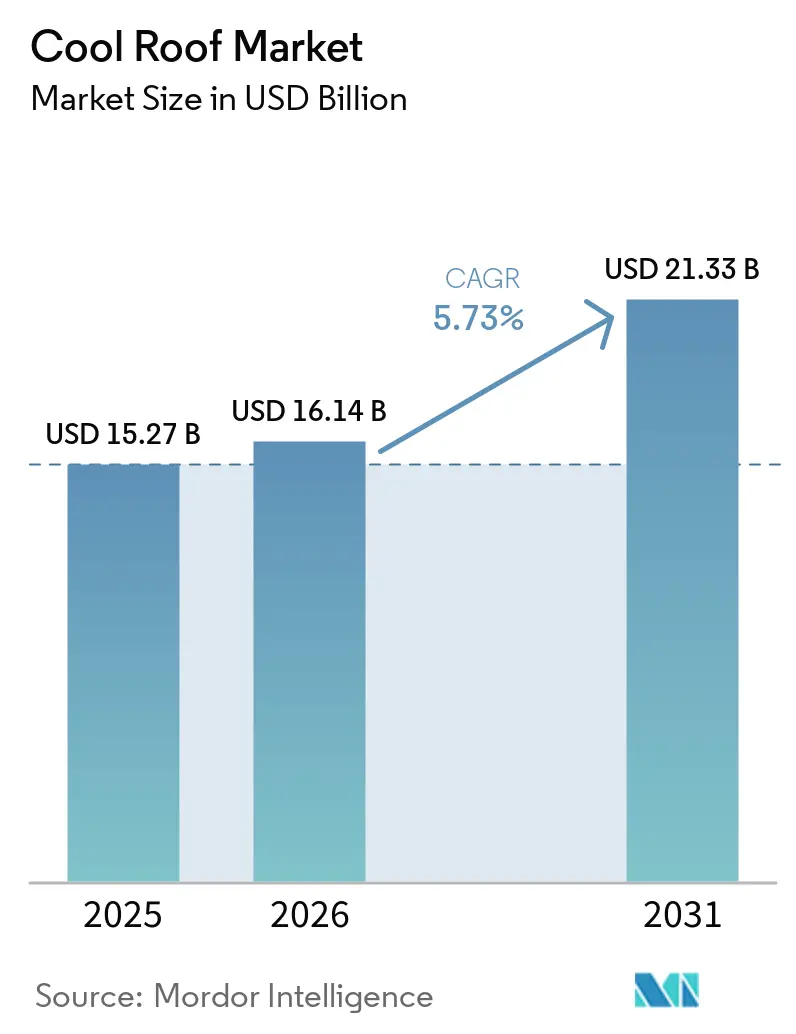

| Market Size (2026) | USD 16.14 Billion |

| Market Size (2031) | USD 21.33 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

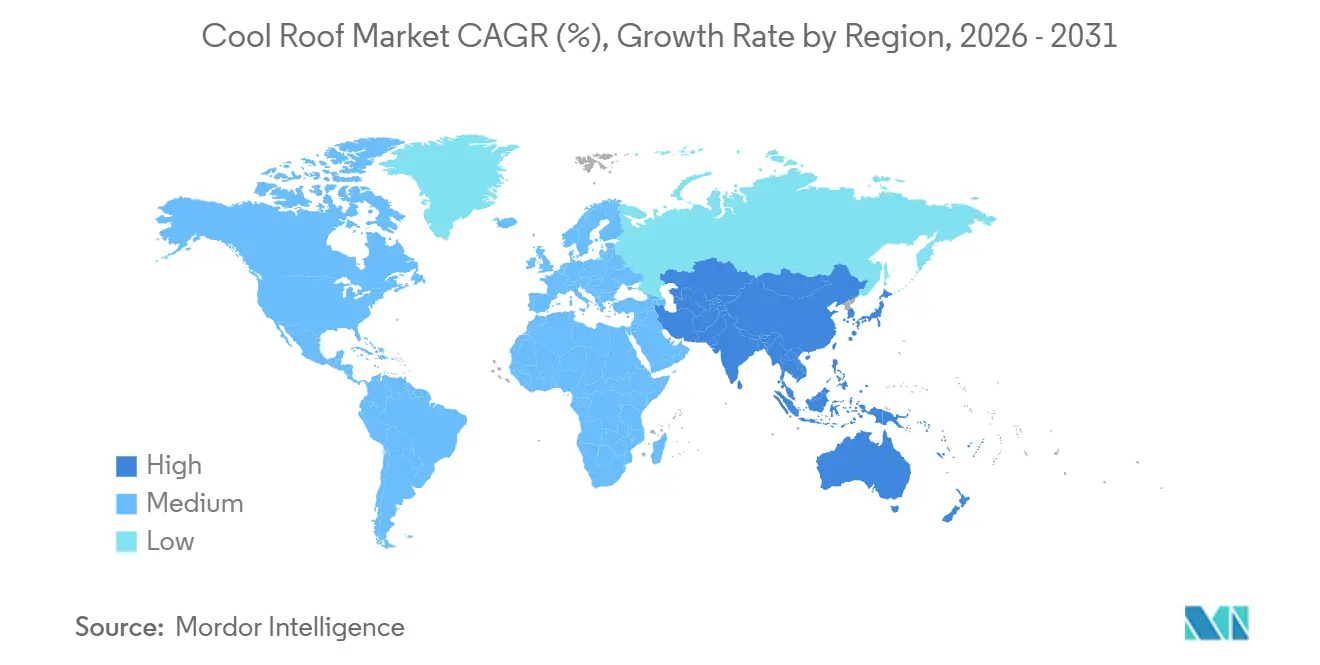

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cool Roof Market Analysis by Mordor Intelligence

The Cool Roof Market size was valued at USD 15.27 billion in 2025 and is estimated to grow from USD 16.14 billion in 2026 to reach USD 21.33 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Accelerating code requirements, increasing electricity prices in hot climates, and growing urban heat-island programs are reducing payback periods and elevating baseline standards for high-SRI roof assemblies. Municipal mandates, such as Atlanta’s 2025 ordinance and California’s Title 24 2025 Energy Code, have shifted reflective surfaces from optional credits to mandatory compliance. In Europe, zero-emission building targets provide a 26-year retrofit timeline that prioritizes coatings over complete roof replacements. Manufacturers are addressing these changes with innovations like dirt-resistant chemistries, closed-loop membrane recycling, and hybrid solutions that combine reflectivity with distributed energy generation. The competitive landscape remains moderately fragmented but is becoming increasingly technology-focused, as established players acquire metal roofing and solar capabilities, while new entrants develop nano-ceramic and self-healing coatings.

Key Report Takeaways

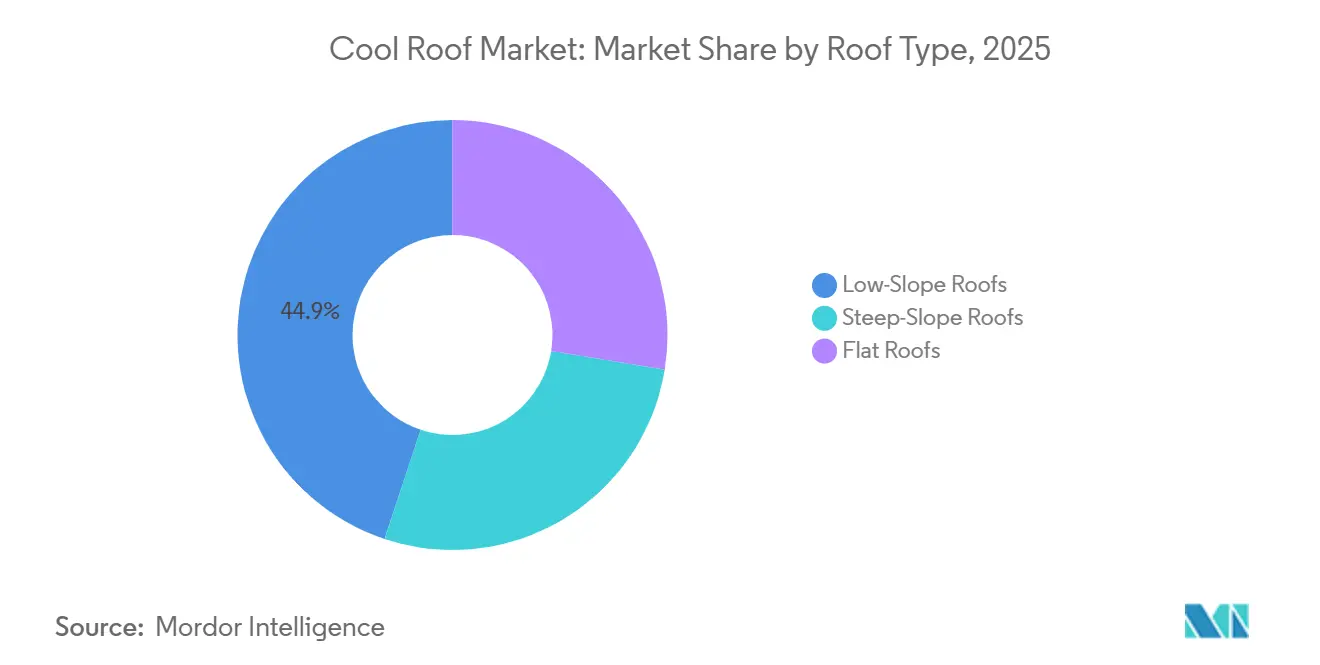

- By roof type, low-slope roofs led with 44.87% of the cool roof market share in 2025, while flat roofs are projected to expand at a 6.28% CAGR through 2031.

- By material type, cool roof coatings accounted for 30.02% of the cool roof market share in 2025, while single-ply membranes are expected to advance at a 6.42% CAGR through 2031.

- By coating chemistry, acrylic held 40.18% of the cool roof market share in 2025, while silicone is projected to expand at a 6.72% CAGR through 2031.

- By build phase, new construction represented 53.44% of the cool roof market share in 2025; retrofit/reroofing is set to grow at a 7.05% CAGR through 2031.

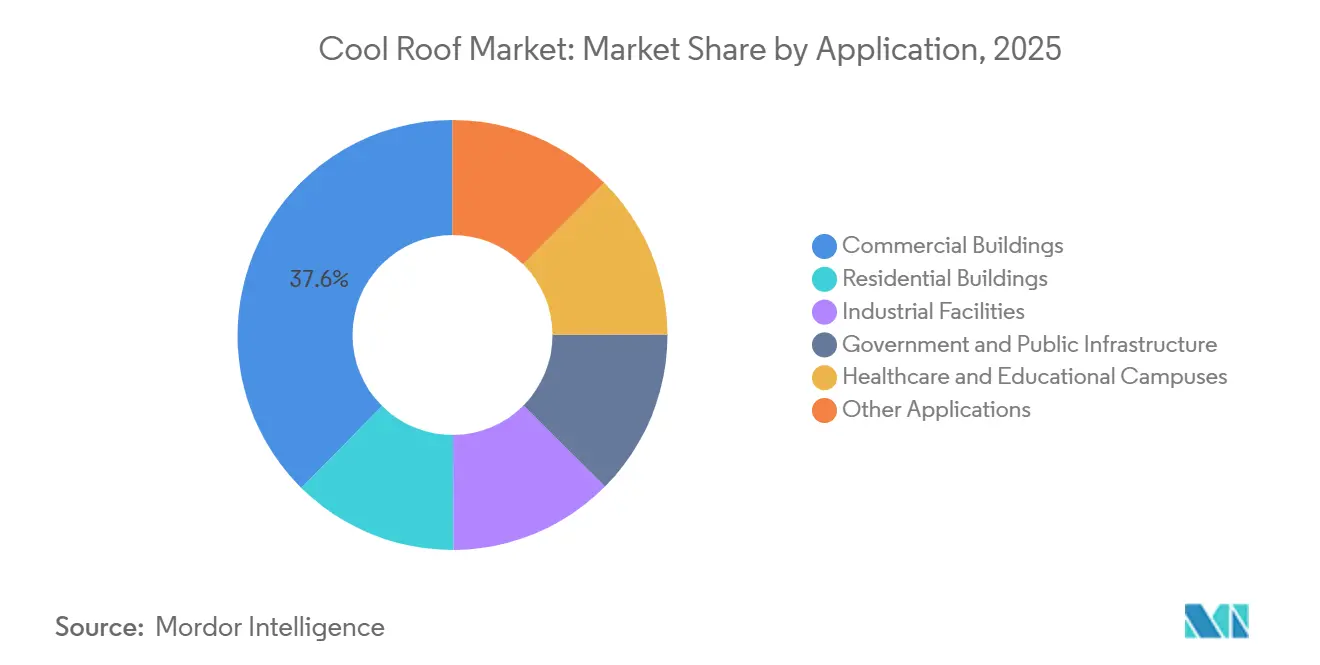

- By application, commercial buildings captured 37.59% of the cool roof market share in 2025, whereas other applications are forecast to post the fastest 6.69% CAGR through 2031.

- By geography, North America dominated with a 35.50% of the cool roof market share in 2025, while Asia-Pacific is on track for the fastest 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cool Roof Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency Regulations and Zero-carbon Mandates | +1.8% | Global, with early adoption in EU, California, China | Medium term (2-4 years) |

| Urban Heat-Island Mitigation Programs | +1.2% | North America and Asia-Pacific urban cores | Short term (≤ 2 years) |

| Rising Electricity Tariffs in Hot Climates | +1.1% | Middle-East, India, Australia, US Southwest | Short term (≤ 2 years) |

| Green-Building Certification Incentives | +0.9% | Global, concentrated in LEED/BREEAM markets | Medium term (2-4 years) |

| Data-Centre Cooling Retrofits for Heat Reduction | +0.7% | North America, Europe, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations and Zero-Carbon Mandates

Jurisdictions are incorporating minimum SRI thresholds directly into building codes, removing trade-off options that previously allowed developers to use additional insulation instead of reflective roofs[1]California Energy Commission, “2025 Building Energy Efficiency Standards,” energy.ca.gov. Europe’s directive for zero-emission new buildings by 2030 requires architects to integrate cool roofs early in the design process, while China’s GB 55015-2021 performance standards effectively mandate high-albedo roofing to achieve its approximately 30% energy-reduction target. India’s Eco-Niwas Samhita 2024 introduces numeric caps on roof U-values and requires an initial reflectance of 0.6 for shallow slopes, signaling a strong regulatory push for the cool roof market. In the United States, LEED v5 increases SRI requirements to 82 (initial) and 64 (aged) for low-slope assemblies, driving manufacturers to reformulate coatings to withstand pollution-related degradation. These regulatory changes are expediting specification decisions, reducing payback periods, and fostering material innovation and supply chain scaling.

Urban Heat-Island Mitigation Programs

Cities are increasingly funding cool roofs as public infrastructure to reduce peak energy demand and lower ambient summer temperatures. For example, Atlanta’s 2025 ordinance applies to commercial buildings over 10,000 ft² and projects USD 310 million in cumulative energy savings by 2035. Hyderabad’s program aims to cover 300 million m² by 2028, achieving indoor temperature reductions of up to 4.5 °C and significant cooling energy savings. Other cities, such as Boston, Montreal, and various locations in California, offer grants to subsidize cool roof adoption for low-income buildings. These initiatives shift demand from private retrofits to public procurement, stabilizing supplier volumes and expanding the market footprint for cool roofs.

Rising Electricity Tariffs in Hot Climates

Rising electricity prices in some of the world’s hottest regions are shortening the payback period for reflective roofs from seven years to less than three. In 2024, average U.S. residential electricity tariffs increased to USD 0.162/kWh, while India’s tariffs reached INR 7.5/kWh (USD 0.09) and Gulf commercial tariffs rose to USD 0.103/kWh. A Saudi study quantified annual energy savings of 110–182 kWh/m² from cool roofs, translating to USD 5.30–15.50/m² in tariff-indexed benefits. As utilities phase out subsidies and implement tiered pricing, facility managers are accelerating cool roof adoption to mitigate future rate increases.

Green-Building Certification Incentives

Green building certification programs are raising SRI thresholds, making cool roof compliance a requirement rather than an optional credit. Standards such as LEED v5, BREEAM 2024, Singapore’s Green Mark, and the UAE’s Estidama now mandate minimum SRI values that most dark surfaces cannot meet. Developers pursuing certification are specifying reflective coatings during the design phase, ensuring sustained demand for cool roofs. This trend is also driving suppliers to validate aged performance under stricter testing protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Cost vs Conventional Asphalt Roofs | -0.9% | Global, acute in price-sensitive residential segments | Short term (≤ 2 years) |

| Reflectivity Loss from Airborne Soot and Pollution | -0.6% | Asia-Pacific urban cores, Middle-East industrial zones | Medium term (2-4 years) |

| Performance Degradation in Humid/Cloudy Zones | -0.4% | Southeast Asia, coastal Europe, US Gulf Coast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost vs Conventional Asphalt Roofs

Reflective coatings cost between USD 0.75–2.50/ft², and TPO membranes range from USD 3.50–6.50/ft², compared to USD 1.00–3.00/ft² for basic asphalt shingles. This 50–150% premium deters cost-sensitive builders. In temperate regions with lower cooling demands, payback periods can exceed five years, limiting cool roofs to discretionary upgrades. Tear-off disposal adds an additional USD 1–2/ft², although retrofit coatings that avoid removal can reduce payback to under five years. While PACE financing spreads costs through property taxes, adoption remains concentrated in California and a few other states. Until incentives bridge this cost gap, price remains a significant barrier to wider market penetration.

Reflectivity Loss from Airborne Soot and Pollution

Pollution significantly impacts the performance of cool roofs. A New York City study found that nearly 25% of monitored cool roofs fell below LEED’s aged SRI threshold within six years, with half of the degradation occurring in the first two years[2]NYC Department of Buildings, “Cool Roof Performance Study 2020,” nyc.gov. In Milan and Rome, reflectance dropped by 30% after one year, increasing peak surface temperatures by 14 °C. Every 0.10 reduction in reflectance raises roof temperatures by approximately 5 °C, increasing HVAC loads. While smooth PVC and TPO membranes retain albedo longer than porous coatings, they still experience a 10–15% reflectance loss in polluted areas. Accelerated aging protocols developed by Berkeley Lab offer faster screening for new chemistries, but ASTM adoption remains slow. Innovations such as dirt-resistant silicones and self-healing polymers are helping to mitigate these issues, but maintenance requirements continue to add to life-cycle costs, limiting adoption in heavily polluted urban areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Roof Type: Low-Slope Roofs Lead Market

Low-slope roofs accounted for 44.87% of 2025 revenue, emphasizing their importance in the cool roof market share for warehouses, malls, and institutional buildings. These roofs utilize large contiguous areas to enhance cooling efficiency and support ballasted solar arrays without membrane penetrations. CRRC’s stricter three-climate aged-rating protocol, adopted in 2025, now prioritizes membranes with longer-lasting reflectance, increasing demand for premium PVC and TPO options that sustain cool roof market size gains. Steep-slope installations have slower growth as reflective asphalt shingles carry a 30–50% cost premium, and homeowners often prioritize aesthetics over energy savings. However, GAF’s solar shingle launch suggests a bundled value proposition that could increase residential adoption if costs decrease further.

Secondary growth is driven by logistics operators retrofitting built-up roofs with TPO membranes, contributing to a 6.28% CAGR for flat roofs through 2031. Integrated 30-year warranties and ENERGY STAR certifications enhance financial appeal, enabling asset managers to qualify for green bonds. Roofers also utilize closed-loop take-back programs to reduce landfill fees and promote environmental credentials, further differentiating cool roofs from conventional membranes.

By Material Type: Cool Roof Coatings Dominate, While Single-ply Membranes Accelerate

Cool roof coatings retained 30.02% revenue in 2025 due to their ability to overlay existing substrates, avoiding tear-off costs and expanding the cool roof market size across cost-sensitive retrofits. Single-ply membranes, however, are the fastest-growing segment, with a 6.42% CAGR through 2031, as builders of new logistics and data hubs prefer their 20-year warranties and weld-sealed seams. Acrylic elastomers remain cost-effective but are prone to dirt accumulation, while silicones and polyurethane-acrylic hybrids are increasingly specified for their superior aged reflectance. Asphalt shingles show modest growth, while metal roofs gain traction in hurricane-prone regions for their uplift resilience. Emerging nano-ceramic top-coats offer anti-soiling benefits but remain niche until standardized testing validates their long-term performance.

By Coating Chemistry: Acrylic Leads, Silicone Gains Momentum

Acrylic coatings captured 40.18% of 2025 revenue due to their low initial cost. However, silicone coatings are growing at the highest 6.72% CAGR through 2031, driven by their dirt-repellent properties and ability to maintain reflectance. Polyurethane coatings are preferred for high-traffic areas, while hybrid coatings combine the cost advantages of acrylic with the durability of silicone, contributing to notable market value growth. Accelerated-aging validation has shortened development cycles, enabling manufacturers to quickly update premium product lines to meet stricter LEED aged-SRI requirements.

By Build Phase: New Construction Leads, Retrofits Close the Gap

New construction contributed 53.44% of 2025 demand, as architects can specify reflective roofs during the design phase, avoiding logistical challenges. Retrofits, however, are growing at a 7.05% CAGR through 2031, driven by urban building-performance standards with near-term deadlines. Contractors use low-odor coatings to minimize tenant disruptions during operating hours. Tear-off recycling programs reduce waste disposal costs and help property owners earn green-building credits, further supporting the growth of retrofits in the cool roof market.

By Application: Commercial Buildings Dominate, Other Applications Rising

Commercial buildings accounted for 37.59% of the revenue share in 2025, as strip malls and offices focus on reducing energy operating costs to enhance property valuations. Other applications are growing at the fastest 6.69% CAGR through 2031, as passive cooling reduces the need for capital-intensive mechanical upgrades. Residential adoption remains concentrated in U.S. Sunbelt states, where utility rebates and PACE financing drive demand. However, overall residential growth remains modest due to the high cost of steep-slope reflective shingles.

Geography Analysis

North America led 2025 demand with 35.50% share, driven by California’s stringent building codes, Atlanta’s city mandates, and widespread LEED adoption. Federal tax incentives and state grants offset upfront costs, sustaining the leading cool roof market size momentum. Canada and Mexico exhibit slower growth due to fewer cooling-degree days, though urban heat-island studies in Toronto and Monterrey are encouraging municipal pilot programs.

Asia-Pacific exhibits the fastest 6.88% CAGR through 2031. India’s regional acceleration is supported by Telangana’s policy targeting 300 km² of installations by 2028 and Eco-Niwas caps on roof U-values, steering both public and private tenders toward reflective options. China’s GB 55015-2021 energy code establishes cool roofs as the standard compliance path for new dwellings, while Japan’s CASBEE assessments promote adoption in high-occupancy commercial towers.

Europe grows steadily on the back of the recast Energy Performance of Buildings Directive. Germany and France have translated EU mandates into national codes that incorporate SRI minimums, while Nordic countries remain cautious due to winter heat-loss concerns. Southern Europe is seeing increased adoption to mitigate extreme summer temperatures, though high pollution levels in cities like Milan and Madrid drive demand for dirt-resistant silicone coatings.

The Middle East and Africa expand from a smaller base. Saudi Arabia’s post-subsidy tariff reforms create strong economic incentives, while the UAE’s Estidama certification mandates reflective roofing for major projects in Abu Dhabi and Dubai. South Africa’s growth is modest, limited by lower cooling needs outside Gauteng, but supported by green-building initiatives in Johannesburg and Cape Town. Brazil anchors South America’s uptake following the 2024 publication of NBR 17162, which aligns testing standards with ASTM and boosts local production capacity.

Competitive Landscape

The cool roof market is moderately concentrated, with differentiation driven by advancements in chemistry and vertical integration. Sika began construction in 2026 on a USD 90 million membrane plant in Texas, featuring a closed-loop recycling line that reduces material costs by 10–15% and aligns with U.S. landfill-diversion goals. Carlisle’s USD 300 million acquisition of Drexel Metals in 2024 shifts its focus toward 50-year metal roofing with inherent reflectivity, complementing its single-ply product line. GAF allocated USD 500 million for a Tennessee facility to produce solar-reflective shingles that meet both ENERGY STAR and LEED v5 standards.

Incumbents are investing in accelerated-aging labs to comply with CRRC-1 Manual 2025 revisions, reducing product development timelines and certifying longer-lasting reflectance. Emerging players, such as nano-ceramic formulators, are introducing anti-soiling coatings that reduce cleaning frequency by half. Self-healing polyacrylate films, utilizing trithiocarbonate chemistry, are in early commercialization stages and demonstrate 90% reflectance retention after simulated three-year exposure, appealing to polluted urban markets. Market share shifts will depend on the ability to deliver proven aged performance and integrate recycling or solar capabilities into comprehensive roof solutions.

Cool Roof Industry Leaders

Sika AG

Owens Corning

Carlisle Companies Inc.

CertainTeed, LLC

GAF Materials LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Employees from three Korean airlines, including Air Busan, Jin Air, and Air Seoul, collaborated on a "Cool Roof" volunteer project in Nambumin-dong, Seo-gu, Busan. The initiative aimed to mitigate urban heat and reduce indoor temperatures for energy-vulnerable households in preparation for the summer heat wave.

- December 2025: In India, the Tamil Nadu government announced plans to expand the Cool Roof Initiative to 297 green schools. As part of this initiative, classrooms in a government school in Ambattur have been coated with heat-reflective white paint.

Global Cool Roof Market Report Scope

A cool roof is engineered to reflect a higher amount of sunlight and absorb less solar heat compared to traditional roofs. It achieves this through high solar reflectance and thermal emittance, maintaining temperatures up to 50°F (28°C) cooler. Cool roofs help lower indoor temperatures, reduce energy consumption for air conditioning, and alleviate the effects of urban heat islands.

The Cool Roof Market is segmented into roof type, material type, coating chemistry, build phase, application, and geography. By roof type, the market is segmented into low-slope roofs, steep-slope roofs, and flat roofs. By material type, the market is segmented into cool roof coatings, single-ply membranes (TPO, PVC, EPDM), asphalt shingles, metal roofs, tiles and slates, built-up roofs (BUR), modified bitumen, and other material types (green roofs, wood shingles). By coating chemistry, the market is segmented into acrylic, elastomeric, silicone, polyurethane, and other coating chemistries (aluminum, ceramic, nano). By build phase, the market is segmented into new construction and retrofit/reroofing. By application, the market is segmented into commercial buildings, residential buildings, industrial facilities, government and public infrastructure, healthcare and educational campuses, and other applications. The report also covers the market size and forecasts for the cool roof in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Low-Slope Roofs |

| Steep-Slope Roofs |

| Flat Roofs |

| Cool Roof Coatings |

| Single-Ply Membranes (TPO, PVC, EPDM) |

| Asphalt Shingles |

| Metal Roofs |

| Tiles and Slates |

| Built-Up Roofs (BUR) |

| Modified Bitumen |

| Other Material Types (Green Roofs, Wood Shingles) |

| Acrylic |

| Elastomeric |

| Silicone |

| Polyurethane |

| Other Coating Chemistries (Aluminum, Ceramic, Nano) |

| New Construction |

| Retrofit/Reroofing |

| Commercial Buildings |

| Residential Buildings |

| Industrial Facilities |

| Government and Public Infrastructure |

| Healthcare and Educational Campuses |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Roof Type | Low-Slope Roofs | |

| Steep-Slope Roofs | ||

| Flat Roofs | ||

| By Material Type | Cool Roof Coatings | |

| Single-Ply Membranes (TPO, PVC, EPDM) | ||

| Asphalt Shingles | ||

| Metal Roofs | ||

| Tiles and Slates | ||

| Built-Up Roofs (BUR) | ||

| Modified Bitumen | ||

| Other Material Types (Green Roofs, Wood Shingles) | ||

| By Coating Chemistry | Acrylic | |

| Elastomeric | ||

| Silicone | ||

| Polyurethane | ||

| Other Coating Chemistries (Aluminum, Ceramic, Nano) | ||

| By Build Phase | New Construction | |

| Retrofit/Reroofing | ||

| By Application | Commercial Buildings | |

| Residential Buildings | ||

| Industrial Facilities | ||

| Government and Public Infrastructure | ||

| Healthcare and Educational Campuses | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the cool roof market?

The cool roof market size stands at USD 16.14 billion in 2026 and is forecast to reach USD 21.33 billion by 2031, expanding at a 5.73% CAGR from 2026.

Which roof type leads adoption in 2025?

Low-slope roofs held 44.87% of 2025 revenue because commercial buildings favor their large contiguous surfaces for maximum cooling benefit.

Why is silicone coating chemistry gaining share?

Silicone coatings retain solar reflectance longer than acrylics, resisting dirt in polluted or humid climates, and are projected to grow at a 6.72% through 2031.

Which region will grow fastest through 2031?

Asia-Pacific is on track for a 6.88% CAGR through 2031, led by India’s Telangana policy and China’s mandatory high-SRI codes.

Page last updated on: