Geogrids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 1.93 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geogrids Market Analysis by Mordor Intelligence

The Geogrids Market size was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 1.93 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). Increasing adoption of performance-based pavement design, alignment of public spending with whole-life cost principles, and carbon-reduction mandates are cementing demand for geogrids across infrastructure programs. Agencies now emphasize extending pavement life rather than replacing entire road sections, which raises the value of engineered soil reinforcement solutions that deliver verifiable lifecycle savings. Demand also benefits from stricter disclosure rules on embodied emissions that favor lightweight geosynthetics over thicker unreinforced aggregate layers. Meanwhile, digital twin modeling is improving specification accuracy and shortening approval cycles, fostering a more data-driven purchasing culture. Together, these forces are moving the geogrids market beyond early adoption and into a period of steady, efficiency-oriented growth.

Key Report Takeaways

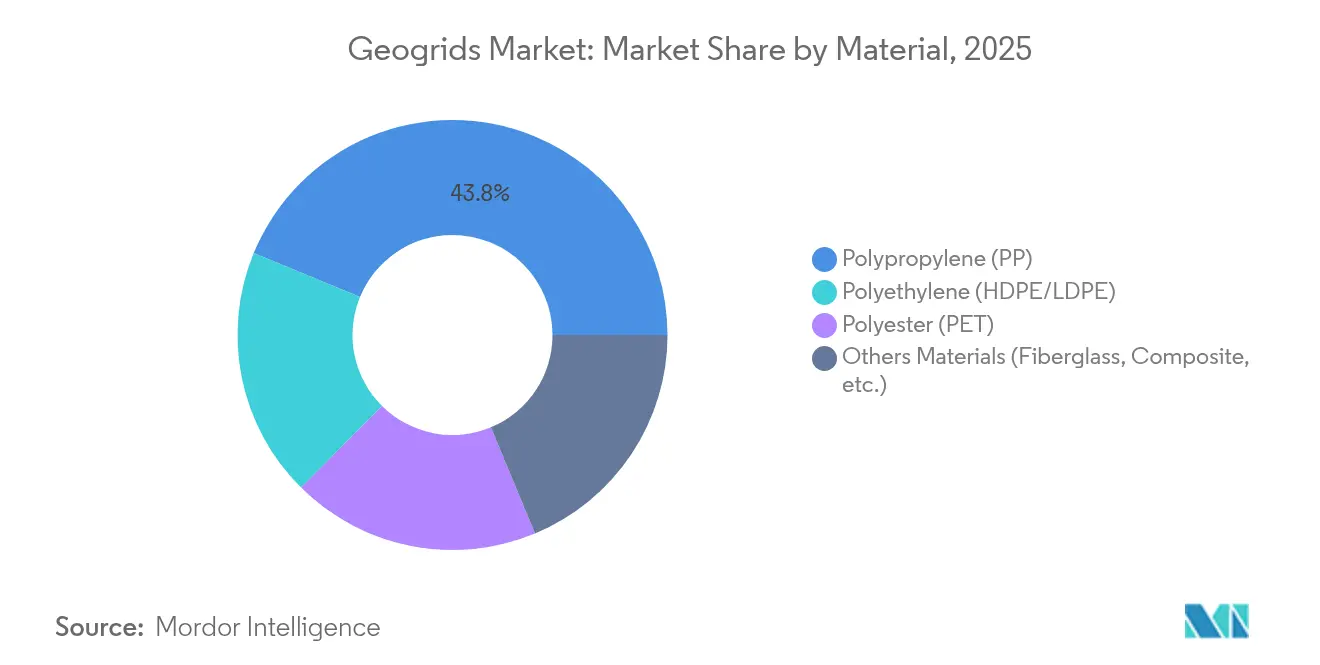

- By material, polypropylene led with 43.78% of the geogrids market share in 2025, while polyester registered the fastest expansion at a 5.32% CAGR through 2031.

- By structural types, biaxial products accounted for 45.21% of 2025 revenues; triaxial designs are forecast to grow at a 5.05% CAGR, the swiftest among structural types.

- By manufacturing method, extrusion remained the dominant manufacturing method with 40.79% share in 2025, whereas knitted/woven output is projected to post a 4.67% CAGR to 2031.

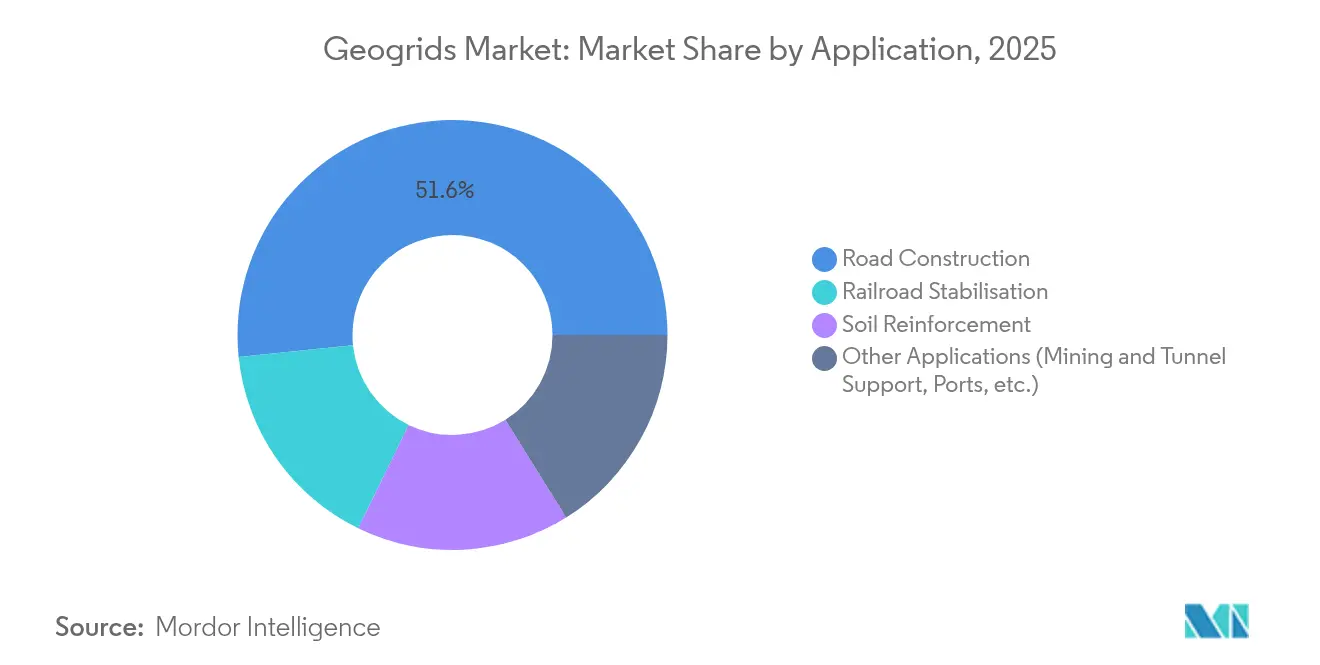

- By application, road construction absorbed 51.63% of the 2025 demand; other applications are projected to expand at a 4.94% CAGR, the highest among all applications.

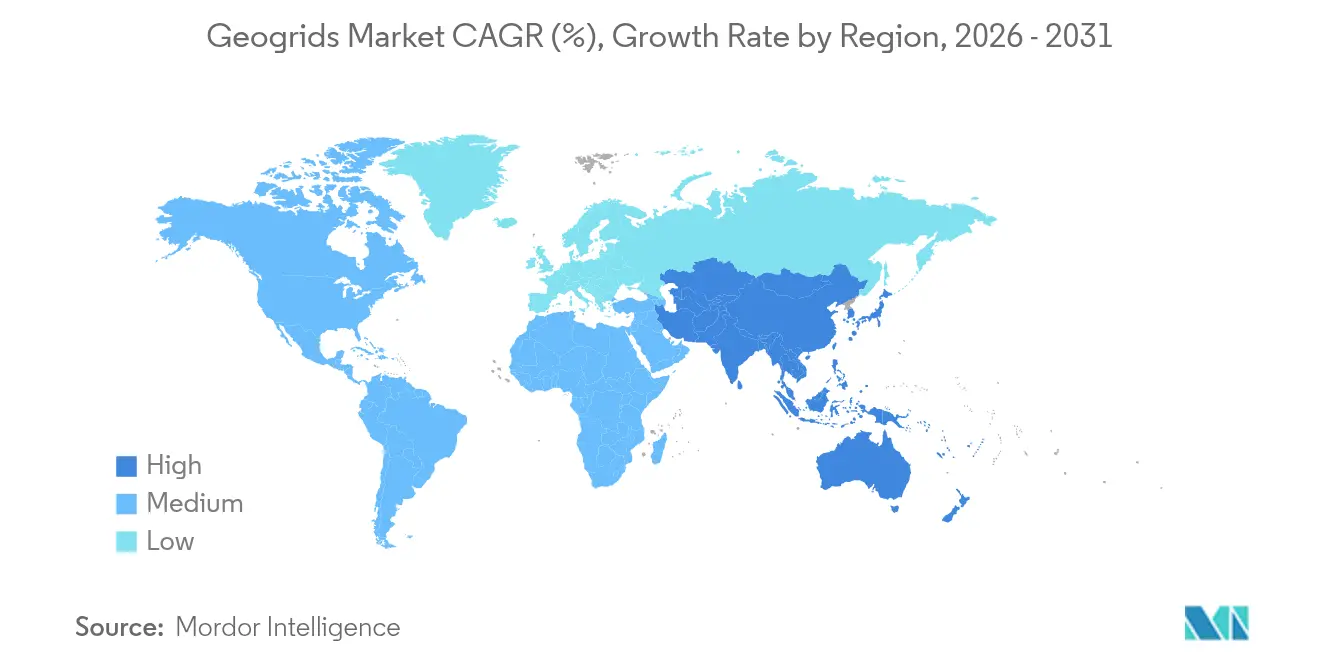

- By geography, North America held 39.01% of 2025 revenues, yet Asia-Pacific is poised for the fastest regional growth at a 4.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geogrids Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pavement life-cycle extension targets | +1.2% | North America and Europe | Medium term (2-4 years) |

| Carbon-reduction mandates | +0.8% | EU and North America | Long term (≥ 4 years) |

| Expressway build-out in developing markets | +1.1% | Asia-Pacific; spill-over to MEA and Latin America | Medium term (2-4 years) |

| Mining haul-road reinforcement | +0.6% | Resource-rich regions worldwide | Short term (≤ 2 years) |

| Digital twin-based design optimisation | +0.4% | North America and Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Pavement Life-Cycle Extension Targets

Transport agencies are shifting from thickness-based empirical design toward mechanistic-empirical approaches that quantify the incremental benefit of geogrid inclusion over a 40- to 100-year life. Layer Coefficient Ratio calculations prove that thinner reinforced pavements can deliver identical fatigue performance, directly supporting budget-constrained jurisdictions[1]Federal Highway Administration, “Design and Construction Guidelines for Geosynthetic Reinforced Soil Structures,” fhwa.dot.gov. United States state departments have begun embedding geogrids in standard specifications for weak-subgrade corridors, a practice mirrored in several EU member states. This behavioural change elevates lifecycle cost over first cost, heightening interest in products with robust field performance data. The resulting demand uptick is most visible in rehabilitation contracts, where agencies seek rapid construction and minimal lane closure times. Consequently, the geogrids market registers increased pull-through from pavement preservation budgets and stimulus allocations earmarked for deferred maintenance.

Carbon-Reduction Mandates Favouring Lightweight Geo-Solutions

Several jurisdictions now score bids partly on total embodied carbon, prompting contractors to quantify emissions from aggregate haulage and asphalt production. Independent studies show geogrid-reinforced base layers can shrink material haulage volumes by 28 to 45%, translating into 58 to 85 tCO₂e/km savings on two-lane highways. With material production accounting for more than 95% of road-building emissions, this benefit carries decisive weight. Early movers in France and the Nordics have created procurement templates that treat carbon reduction as a non-price criterion, a model now spreading to US state DOTs. Suppliers able to substantiate carbon savings with third-party verified data gain preferred status on low-carbon pilot programs. Over the long term, lifecycle inventory disclosure is expected to become mandatory on publicly funded transportation projects, embedding geogrids deeper into mainstream design.

Rapid Expansion of Expressway Networks in Developing Economies

China, India, and Indonesia are commissioning multilane corridors across variable subgrade profiles, often crossing soft clays, expansive soils, or frost-susceptible ground. On the Harbin–Yichun high-speed corridor, triaxial geogrids stabilise sub-freezing soils while minimising excavation volumes. India’s Bharatmala initiative specifies geogrid reinforcement on black cotton soil stretches to mitigate differential settlement and cracking. Latin American public-private partnerships similarly rely on geogrids to control rutting in heavy truck lanes traversing tropical soils. Collectively, these projects add more than 12,000 km of reinforced pavement annually, underpinning above-average demand growth for the geogrids market in developing regions.

Mining Haul-Road Reinforcement Demand

Open-pit mines face escalating tyre and suspension costs as equipment payloads surpass 360 tons. Case studies show that triaxial grids can cut dozer-maintenance hours by 52% while extending haul-road resurfacing intervals from three weeks to six months. Furthermore, geogrids enable the use of locally sourced inferior aggregates, trimming imported crushed-rock procurement. As mining stakeholders embed Scope 3 emission considerations, material-efficient road designs resonate with sustainability commitments, fuelling short-term demand across resource-rich geographies.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polypropylene and HDPE price volatility | -0.7% | Global, pronounced in price-sensitive regions | Short term (≤ 2 years) |

| Fragmented certification standards | -0.5% | Worldwide, hurdles for cross-border projects | Medium term (2-4 years) |

| Limited installer skill sets | -0.3% | Asia-Pacific, MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Polypropylene and HDPE

Spikes in polypropylene spot values compress margins for manufacturers locked into fixed-price public contracts. To buffer risk, producers hedge feedstock exposure and diversify toward polyester, yet substitution remains partial because polypropylene dominates high-volume roads. Price uncertainty also complicates project budgeting, leading some agencies to postpone geogrid tenders or seek escalation clauses. Over the near term, volatility is likely to deter adoption in cost-sensitive rural road programs, trimming incremental demand in emerging economies despite strong structural drivers for the geogrids market.

Fragmented Certification Standards Across Regions

A lack of globally harmonised test methods forces suppliers to duplicate certification across ASTM, ISO, and country-specific regimes[2]ASTM International, “Committee D35 on Geosynthetics,” astm.org . Each additional protocol adds laboratory fees, inventory complexity, and time-to-market delays, disadvantages that fall hardest on small and medium enterprises. Multilateral attempts to converge standards move slowly, so manufacturers allocate engineering budgets to matrix regional test variations instead of product innovation. Disparate rules also impair project tendering, as owners struggle to compare technical equivalence, occasionally defaulting to familiar incumbent brands. This regulatory friction moderates international expansion, dampening the compound growth of the geogrids market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polypropylene Dominance Amid Polyester Innovation

The geogrids market registered a polypropylene contribution of 43.78% in 2025, translating into the single-largest slice of global revenues. In absolute terms, the polypropylene segment commanded a larger share of the geogrids market size than any other material because its tensile efficiency, chemical inertness, and price competitiveness meet most highway specifications without additional resin modifiers.

Yet the same data show polyester advancing at a 5.32% CAGR, the sharpest trajectory among materials, as engineers prioritise creep resistance for long-term load-bearing structures. Polyester’s lower susceptibility to oxidative degradation under sustained stress makes it the preferred choice for high embankments and reinforced steep slopes that must resist constant gravitational pull over decades. Design consultancies increasingly prescribe polyester for structures exceeding 10 m in height, a specification niche widening as urban sprawl pushes transport corridors onto marginal terrain.

By Structural Type: Triaxial Gains Ground on Biaxial Leadership

Biaxial designs delivered 45.21% of global revenue in 2025, thereby anchoring the structural hierarchy of the geogrids market. Their dominance stems from multi-decade design guidance, abundant field data, and manufacturing economies of scale that drive down unit costs. Engineers deploying standard flexible pavement rehabilitation often default to biaxial because guidance documents contain traffic-equivalent thickness factors calibrated for its stiffness profile.

Nevertheless, triaxial units are expanding at a 5.05% CAGR and are increasingly specified for heavy-loading conditions where omnidirectional traffic patterns create high shear at aggregate interfaces. Independent laboratory tests reveal that triaxial grids can reduce permanent deformation 30–40% more effectively than biaxial under cyclic wheel loads, owing to their radial rib distribution that mobilises interlock in every direction.

By Manufacturing Method: Knitted/Woven Techniques Challenge Extrusion

Extrusion supplied 40.79% of global volume in 2025 and continues to dominate mass-market supply on account of high-throughput lines that confer cost advantages for commodity grades. The method provides tight aperture control, facilitating quality-assurance protocols compliant with ASTM D6637 tensile testing. However, knitted and woven production is posting a 4.67% CAGR, outpacing extrusion as pavement engineers prioritise aggregate interlock and junction flexibility.

Knitted PET grids exhibit superior junction efficiency because yarns are mechanically interlaced rather than heat-bonded, yielding higher pull-out resistance when laid over rough subgrades. Comparative trials conducted on Louisiana DOT’s full-scale test section showed that knitted grids lowered rutting by 18 mm versus 11 mm for extruded equivalents over identical base thickness, an outcome attributed to the higher conformability of woven structures.

By Application: Mining and Tunnel Support Diversify Beyond Roads

Road construction represented 51.63% of the 2025 geogrids market size as agencies embedded grids into standard pavement-rehab playbooks. Layered flexible pavement designs integrating geogrids typically achieve 20–35% reductions in aggregate thickness, savings that multiply across multi-kilometre projects. Yet the application portfolio is broadening; demand for haul-road stabilisation, tunnel-face support, and rail ballast confinement is projected to grow 4.94% annually through 2031, outpacing highways. The shift is particularly notable in copper, gold, and lithium mines where geogrids underpin high-speed haul traffic as pits deepen.

Railways are another emerging outlet as operators look to control ballast settlement under higher axle loads from double-stack freight. Tests at the Transportation Technology Center in Pueblo, Colorado, found that geogrid-stiffened ballast layers halve maintenance tamping cycles without compromising track geometry. Collectively, these non-road segments provide countercyclical revenue streams that soften the impact of highway funding cycles, reinforcing the structural resilience of the geogrids market.

Geography Analysis

North America delivered 39.01% of 2025 revenues, underpinned by USD 350 billion of federal highway funding authorised by the Infrastructure Investment and Jobs Act. State DOT specifications routinely cite AASHTO R50 procedures for geogrid qualification, effectively institutionalising demand. Pavement preservation philosophies in California, Texas, and New York have moved from thickness-addition toward mechanical stabilisation, translating into higher unit uptake even as lane-kilometre growth slows.

Asia-Pacific ranks as the fastest-growing territory with a 4.74% CAGR through 2031, buoyed by expressway and rail megaprojects across China, India, Indonesia, and Vietnam. Chinese provinces allocate grids for frost-susceptible embankments on high-speed routes such as the Harbin–Yichun corridor, while India’s National Highways Authority mandates tensile-grade PET geogrids on expansive-clay subgrades within the Bharatmala Pariyojana. Abundant infrastructure pipelines and soil-condition challenges synergize to keep the Asia-Pacific geogrids market on a higher-than-global trajectory.

Europe is driven by the rehabilitation of legacy networks and stringent carbon-reduction rules that favour material-efficient reinforcement. France’s Directorate-General for Infrastructure specifies geogrids in full-depth pavement recycling, while the UK Infrastructure Strategy aligns product selection with net-zero goals.

Beyond the triad, South America leans on public-private concession models, and Gulf Cooperation Council states fund new-build corridors across desert terrain, both contexts where geogrids counteract weak subgrade stiffness and sand-induced rutting, broadening the global footprint of the geogrids market.

Competitive Landscape

The geogrids industry maintains moderate fragmentation. Commercial Metals Company (CMC) heightened consolidation momentum by purchasing Tensar for USD 550 million, securing polymer extrusion capacity alongside engineering service teams. Technological differentiation stands out as a primary competitive lever. Digital twin compatibility is gaining strategic weight; suppliers offering parameterised product libraries that integrate with finite-element platforms like MIDAS and Plaxis shorten consultant design cycles, thereby embedding their grids into tender packages. On the sustainability front, players are experimenting with mass-balance certified recycled polypropylene and bio-based resin blends to pre-empt tightening EU carbon disclosure rules. Early pilots show that recycled-content grids can achieve 90% of virgin-polymer tensile strength, positioning eco-grades as credible substitutes once durability testing matures.

Geogrids Industry Leaders

Commercial Metals Company

HUESKER International

Maccaferri Spa

Naue GmbH & Co. KG

Solmax

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: Commercial Metals Company announced it had acquired a geosynthetics manufacturing facility from BOSTD-America to expand production for Tensar geogrid lines.

- March 2023: Singhal Industries expanded its geogrid portfolio into the United States, the United Kingdom, and Gulf countries following successful domestic rollouts.

Global Geogrids Market Report Scope

The geogrids market report include:

| Polypropylene (PP) |

| Polyethylene (HDPE/LDPE) |

| Polyester (PET) |

| Others Materials (Fiberglass, Composite, etc.) |

| Uniaxial |

| Biaxial |

| Triaxial |

| Extrusion |

| Knitted/Woven |

| Bonded/Welded |

| Road Construction |

| Soil Reinforcement |

| Railroad Stabilisation |

| Other Applications (Mining and Tunnel Support, Ports, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polypropylene (PP) | |

| Polyethylene (HDPE/LDPE) | ||

| Polyester (PET) | ||

| Others Materials (Fiberglass, Composite, etc.) | ||

| By Structural Type | Uniaxial | |

| Biaxial | ||

| Triaxial | ||

| By Manufacturing Method | Extrusion | |

| Knitted/Woven | ||

| Bonded/Welded | ||

| By Application | Road Construction | |

| Soil Reinforcement | ||

| Railroad Stabilisation | ||

| Other Applications (Mining and Tunnel Support, Ports, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the geogrids market?

The geogrids market size reached USD 1.58 billion in 2026 and is projected to grow to USD 1.93 billion by 2031.

Which material segment leads the geogrids market?

Polypropylene leads, accounting for 43.78% of 2025 revenue, although polyester is expanding the fastest.

Why are triaxial geogrids gaining popularity?

Triaxial designs distribute loads omnidirectionally, lowering rutting and settlement, and hence are growing at a 5.05% CAGR.

Which region is forecast to post the highest growth?

Asia-Pacific is expected to grow at a 4.74% CAGR through 2031, propelled by large-scale highway and rail projects.

How do geogrids contribute to carbon reduction in road construction?

Reinforced pavements require thinner aggregate layers, cutting embodied emissions by up to 85 tCO₂e per kilometre.

Page last updated on: