Asparagus Market Size and Share

Asparagus Market Analysis by Mordor Intelligence

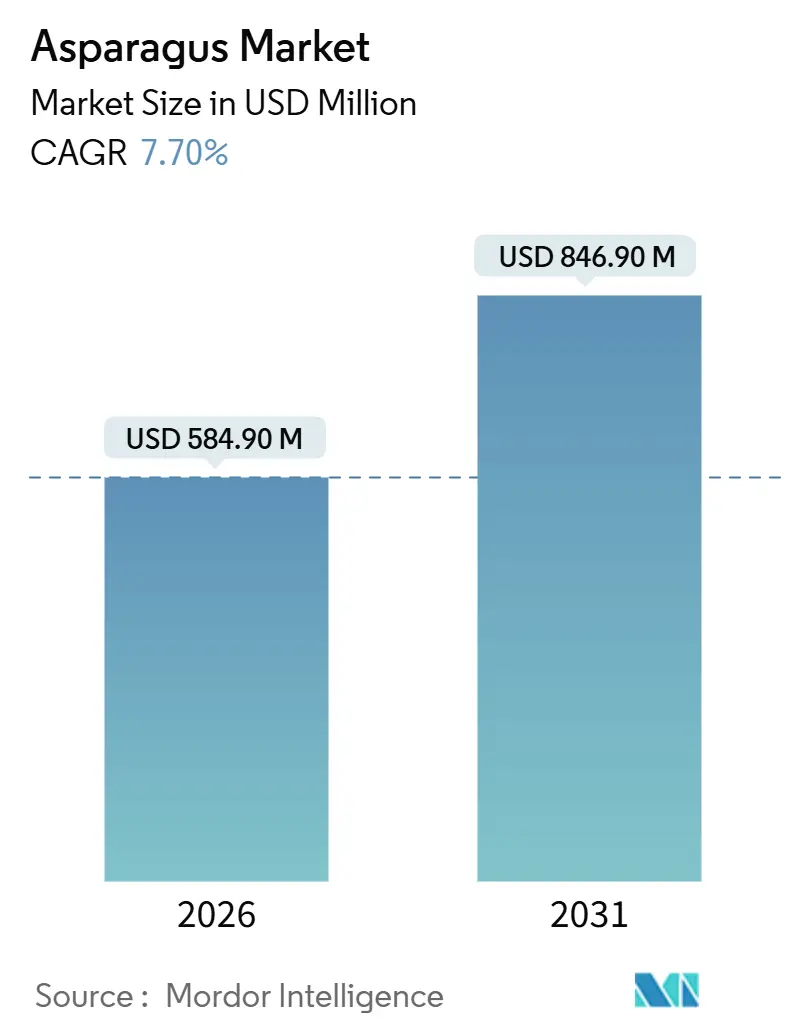

The asparagus market size reached USD 584.9 million in 2026 and is projected to increase to USD 846.9 million by 2031, representing a 7.7% CAGR between 2026 and 2031. Steady growth relies on health-driven diets, expanded cold chain coverage that ensures year-round supply, and precision practices that increase yields while reducing input costs. The Asia-Pacific region led consumption value with a 38% share in 2025, driven by rising incomes in China and persistent demand for premium vegetables in Japan and Australia. Organic acreage is outpacing conventional fields as retailers dedicate more shelf space to pesticide-free produce, while biotech research into heat- and disease-tolerant cultivars promises longer stand life. Conversely, acute labor shortages, volatile freight tariffs, and Fusarium outbreaks continue to inflate operating expenses, keeping margins tight for exporters and growers.

Key Report Takeaways

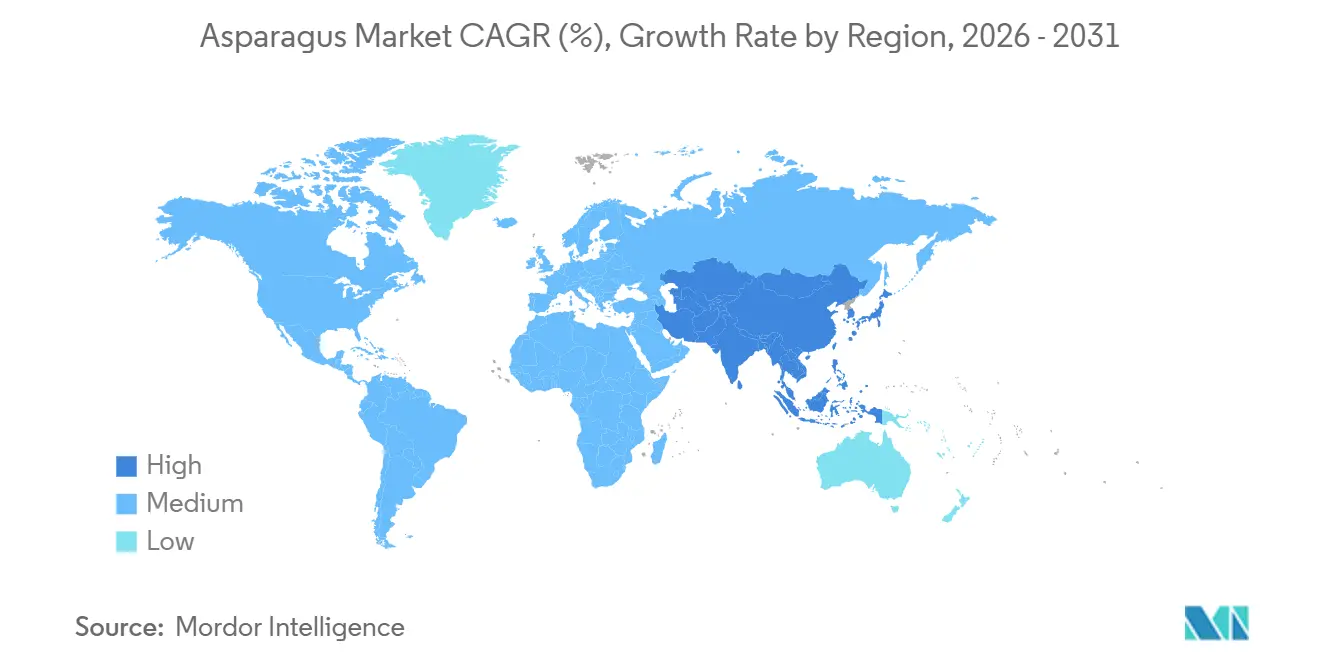

- By geography, the Asia-Pacific region captured 38% of the 2025 value, while the Middle East is forecast to expand at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Asparagus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-centric diets boost demand for nutrient-dense fresh vegetables | +0.8% | Global, strongest uptake in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization of organic asparagus in high-income markets | +0.7% | North America and Europe, emerging in Japan and Australia | Medium term (2-4 years) |

| Year-round availability via counter-season exports and cold chain expansion | +0.6% | Global, notably Peru to North America and Europe, Mexico to United States | Short term (≤2 years) |

| Precision drip-fertigation and plasticulture lift farm yields | +0.5% | Peru, Mexico, California, Spain, China, Australia | Long term (≥4 years) |

| Carbon-credit revenue streams for perennial plantings | +0.4% | Europe, pilot efforts in North America and South America | Long term (≥4 years) |

| Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR)-enabled breeding of heat and rust-tolerant cultivars | +0.3% | United States, Netherlands, Peru, rollout in all production hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Health-Centric Diets Boost Demand for Nutrient-Dense Fresh Vegetables

Asparagus delivers 2.9 grams of fiber, 70 micrograms of folate, and 2.9 milligrams of vitamin E per 100-gram serving, positioning it as a nutrient-dense choice for consumers prioritizing cardiovascular health, prenatal nutrition, and digestive wellness[1]Source: USDA FoodData Central, “Asparagus Nutritional Profile,” fdc.nal.usda.gov. A 2024 consumer survey conducted by the Produce Marketing Association found that 36.7% of United States households purchased fresh asparagus during the year, up from 26% in 2023, with higher-income cohorts exhibiting purchase rates exceeding 50%. This income gradient highlights asparagus's role as a premium vegetable that benefits disproportionately from wage growth and increases in discretionary spending in developed markets. United States per capita availability declined from 2.0 pounds in 2022 to 1.5 pounds in 2023, yet this contraction reflects supply-side constraints rather than demand erosion, as terminal market prices remained firm despite lighter offerings.

Premiumization of Organic Asparagus in High-Income Markets

Organic asparagus commanded retail price premiums ranging from 7 to 36% across North American and European markets in 2025, with the spread narrowing as conventional prices rose more rapidly during the 2022-2024 inflationary cycle. Organic sales grew 7.4% annually over the past three years, while conventional volumes contracted by 2.9%, signaling a structural shift in consumer preference toward pesticide-free produce. Retailer mandates for organic SKUs have expanded shelf space, yet Peruvian organic exports to the United States remain blocked by methyl bromide fumigation requirements that strip organic certification. The Instituto Peruano del Espárrago y Hortalizas is collaborating with the National Service of Agri-Food Health and Quality (SENASA) to pilot modified-atmosphere treatments that could satisfy phytosanitary protocols without the need for fumigation, potentially unlocking USD 50 million in annual organic export value.

Year-Round Availability via Counter-Season Exports and Cold Chain Expansion

According to the ITC Trade Map, Peru and Mexico are significant exporters of asparagus, with Peru exporting USD 406,708 thousand in 2024 and Mexico exporting USD 328,300 thousand. These exports enable Northern Hemisphere retailers to maintain year-round SKUs. In July 2025, Maersk inaugurated a 17,500-square-meter cold storage hub in Olmos, Peru. This facility is designed to reduce post-harvest losses by 10% through rapid pre-cooling and controlled-atmosphere storage. It has a capacity to handle 15,000 pallets and is integrated with Peru's new Port of Chancay, which began operations in the fourth quarter of 2024. The port reduces transit time to Shanghai from 35 days to 25 days. Given asparagus's high respiration rate and a shelf life of 7 to 10 days at 32 to 35°F, uninterrupted cold chains are essential, making infrastructure investments critical for preserving margins.

Precision Drip-Fertigation and Plasticulture Lift Farm Yields

Drip irrigation systems reduce water consumption by 30 to 50% compared to flood irrigation, while fertigation improves nitrogen use efficiency by 20 to 30%, lowering input costs and reducing environmental runoff. Peruvian growers in the Ica and La Libertad regions were projected to adopt drip systems on approximately 70% of their asparagus acreage by 2024, supported by government subsidies under the Programa de Riego Tecnificado, which co-funds 50% of the installation costs. The United States Department of Agriculture's Environmental Quality Incentives Program awarded up to USD 450,000 in grants for irrigation system upgrades in New Mexico in 2024, reflecting the federal prioritization of water conservation in arid production zones. Yield improvements from precision agriculture range from 10 to 15% over conventional practices, yet adoption remains constrained by upfront capital requirements and limited technical assistance in smallholder regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute harvest-season labor shortages drive up unit costs | -0.9% | United States, Mexico, Peru, Spain | Short term (≤2 years) |

| Volatile air-freight and refrigerated trucking tariffs squeeze margins | -0.7% | Global, notably Peru and Mexico to U.S. and Europe | Short term (≤2 years) |

| Soil-borne Fusarium and crown-rot outbreaks reduce stand life | -0.4% | Peru, California, Spain, Australia, China | Medium term (2-4 years) |

| Rising pesticide-residue audit failures due to retailer Maximum Residue Limit (MRL) tightening | -0.3% | Peru and Mexico exports to European Union and United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Harvest-Season Labor Shortages Drive Up Unit Costs

United States H-2A temporary agricultural visa certifications reached 378,000 in 2024, up from 310,000 in 2022, yet grower demand exceeded supply by an estimated 15% during peak asparagus harvest windows in California and Washington [2]Source: US Department of Labor, “H-2A Temporary Agricultural Program,” dol.gov. Adverse effect wage rates for H-2A workers rose 5 to 8% annually from 2022 to 2024, while California's statewide minimum wage increased to USD 16 per hour in 2024, compressing margins for labor-intensive crops like asparagus that require daily hand-picking over 8 to 12-week seasons. Mechanical harvesting remains commercially unviable for fresh-market asparagus due to the fragility of the spears and quality degradation, leaving growers dependent on manual labor. Mexico's asparagus sector competes with higher-paying berry and avocado operations for seasonal workers, thereby exacerbating shortages in the production zones of Sonora and Guanajuato.

Volatile Air-Freight and Refrigerated Trucking Tariffs Squeeze Margins

Refrigerated trucking costs in the United States rose 15 to 20% between 2022 and 2024, driven by diesel price volatility and a 10% shortfall in qualified commercial drivers. Air freight rates from Lima to Miami, the primary corridor for Peruvian asparagus, fluctuated between USD 2.50 and USD 4.20 per kilogram in 2024, as Red Sea shipping disruptions diverted cargo to air routes and tightened capacity. Drought conditions in the Panama Canal in 2023 and 2024 reduced daily vessel transits from 36 to 24, resulting in surcharges of USD 500 to USD 1,200 per container for refrigerated shipments and extending transit times by 5 to 7 days. Asparagus's 7 to 10-day shelf life limits ocean freight viability, forcing exporters to absorb air freight premiums that can represent 25 to 35% of landed cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

The Asia-Pacific region captured 38% of the 2025 value, driven by rising disposable incomes in China, sustained premium vegetable demand in Japan, and the expansion of cold chain infrastructure in Australia, which enables year-round availability. China's asparagus imports increased by 15% annually from 2022 to 2024, primarily sourced from Peru and Mexico, as urbanization and Western dietary trends elevated consumption in tier-1 and tier-2 cities[3]Source: China Customs, “Asparagus Import Statistics,” customs.gov.cn. Japan remains the region's highest per capita consumer, at approximately 0.8 kilograms annually, with retail prices averaging USD 8 to USD 12 per kilogram, reflecting tight supply and consumer preference for thick-spear premium grades.

The Middle East is forecast to expand at a 6.8% CAGR through 2031, the fastest pace globally, as food security policies prioritize diversified fresh-produce imports and cold chain networks expand in the United Arab Emirates and Saudi Arabia. According to the UAE Federal Competitiveness and Statistics Centre, asparagus imports to the United Arab Emirates reached 4,200 metric tons in 2024, sourced from Peru, Mexico, and Spain. Re-exports to neighboring Gulf Cooperation Council markets accounted for 30% of inbound volumes. Saudi Arabia's Vision 2030 agricultural diversification initiatives include subsidies for controlled-environment vegetable production, yet asparagus's perennial nature and water requirements limit domestic cultivation potential, sustaining import dependence.

North America constituted a significant market, with per capita availability of asparagus in the United States declining from 2.0 pounds in 2022 to 1.5 pounds in 2023. This decrease was primarily due to a 10.8% reduction in Peruvian export volumes by week 46 of 2024 and Mexico's reallocation of acreage toward higher-value crops. In Europe, Germany, Spain, and the United Kingdom represented the largest markets. These mature markets exhibited limited elasticity, while traditional practices, such as white asparagus consumption, experienced a generational decline. In South America, Peru and Argentina dominated the region, with domestic markets absorbing production surpluses during export off-seasons.

Competitive Landscape

The fresh asparagus market comprises various players, including producers, importers, and exporters, who collectively supply asparagus. Peruvian companies such as DanPer, Agrokasa, Camposol, and Sociedad Agricola Viru maintain origin-based cold storage facilities and proprietary genetics, ensuring a consistent supply during production gaps in the Northern Hemisphere. Camposol began utilizing Peru’s Port of Chancay in late 2024, reducing shipping times to China by ten days and signaling a strategic focus on the Asian market. Altar Produce, managing 29,000 acres in Mexico, announced in May 2025 its diversification into Brussels sprouts and broccoli to mitigate labor-related risks.

Technology adoption has emerged as a significant differentiator in the market. Leading growers have invested in drip fertigation systems, reducing water usage by up to 50% and aligning with retailer sustainability requirements. Smaller operations face challenges in affording such upgrades. Compliance with standards like GlobalGAP and BRC adds USD 0.05–0.10 per pound to the landed cost, benefiting vertically integrated firms that can distribute these expenses across larger volumes. Opportunities exist in CRISPR-developed cultivars resistant to Fusarium and in modified-atmosphere treatments that eliminate the need for fumigation, potentially unlocking a USD 50 million organic market opportunity for Peru.

European market consolidation continued with Maf Roda Group's acquisition of German processor Strauss in April 2025, aimed at scaling value-added product formats. Camposol’s biotechnology division supplied one million proprietary fruit plants in 2024, indicating potential future developments in asparagus genetics. Moderate entry barriers persist, including stringent residue limits, high freight costs, and reliance on seasonal labor, which disadvantages smaller exporters. However, market fragmentation below the top-tier players provides opportunities for niche participants.

Recent Industry Developments

- March 2025: Maf Roda Group acquired Strauss, a German asparagus processing company, expanding its European footprint and vertical integration into value-added products. The transaction value was not disclosed the move signals consolidation in the European asparagus supply chain as processors seek to offset rising labor and compliance costs.

- September 2024: Pacific Produce, a subsidiary of Grupo Hame, confirmed plans to double asparagus output in Peru, with 250 hectares under crop and a USD 24 million water project to support sustainable expansion.

- July 2024: Camposol released its 2023 Sustainability Report detailing environmental and social metrics across asparagus farms and outlining future ESG targets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the asparagus market as the value generated from sales of fresh, frozen, and canned spears obtained from Asparagus officinalis that reach food retail, food-service, and bulk export channels worldwide. The scope tracks value in USD as well as volume in metric tons and follows the crop from field gate to first commercial sale.

Scope Exclusion: Specialty derivatives such as extracts, soups, or nutraceutical concentrates fall outside this boundary.

Segmentation Overview

- By Geography

- North America

- United States

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Canada

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Mexico

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Germany

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- United Kingdom

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Spain

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Netherlands

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- France

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Italy

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Germany

- Asia-Pacific

- China

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Japan

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Australia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- China

- South America

- Peru

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Argentina

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Peru

- Middle East

- United Arab Emirates

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- Saudi Arabia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- United Arab Emirates

- Africa

- South Africa

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistic and Infrastructure

- Seasonality Analysis

- South Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed growers in Peru, Mexico, Germany, and China, pack-house managers in Spain and the U.S., plus import buyers at European wholesale markets. These dialogues clarified farm-gate pricing spreads, organic acreage intentions, and likely yield gains, helping us refine model variables and stress-test early desk findings.

Desk Research

We began by mining public data troves such as FAO FAOSTAT, UN Comtrade trade sheets, and Eurostat crop panels, which quantify production, trade flows, and average unit prices. Complementary insights were drawn from USDA GAIN reports, Peruvian SENASA shipment data, and the International Asparagus Association newsletters that clarify planting acreage and yield shifts. Company 10-Ks, customs filings, and reputable press articles then anchored recent price swing narratives. Select facts were validated through D&B Hoovers and Dow Jones Factiva. This listing is illustrative; many additional reference points informed the evidence base.

The next pass involved harmonizing country-level time series, converting all values to constant 2024 USD using IMF average exchange rates, and flagging anomalies for analyst review.

Market-Sizing & Forecasting

A top-down construct starts with FAO production and UN Comtrade net-trade balances to recreate apparent consumption, which is then multiplied by weighted average selling prices that our team derived from customs invoices and retailer scans. Supplier roll-ups and sampled ASP × volume checks act as bottom-up guardrails, and gaps such as informal cross-border flows are closed through coefficient adjustments sourced from expert calls. Key drivers in the model include harvested area, yield per hectare, import dependence ratios, per-capita intake trends, organic share, and retail price inflation. A multivariate regression with lagged weather indices and disposable-income growth produces the five-year forecast; scenario bands reflect policy or climate shocks flagged by interviewees.

Data Validation & Update Cycle

Outputs undergo cross-tab checks against historical volatility bands, peer-value spreads, and fresh news triggers. Two analysts and a senior reviewer sign off before release; reports refresh annually, with interim patches when tariff or disease events materially alter baselines.

Why Mordor's Asparagus Market Baseline Earns Confidence

Published figures often differ because publishers pick varying product mixes, price anchors, and update cadences. We acknowledge those gaps up front and show how careful scope choices and yearly refreshes keep our estimate balanced for decision makers.

Key gap drivers are usually the inclusion of downstream processed goods, older currency bases, or single-country price proxies, whereas Mordor Intelligence restricts coverage to primary formats, rebases values each cycle, and validates multi-region prices before modeling.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.01 B | Mordor Intelligence | - |

| USD 31.29 B | Global Consultancy A | Narrow price sample; excludes food-service volumes |

| USD 36.61 B | Industry Publisher B | Adds value-added sauces; older 2024 FX rates |

These comparisons show that, while external numbers swing by several billion dollars, our disciplined variable selection and yearly data sweep offer a transparent, reproducible baseline clients can rely on.

Key Questions Answered in the Report

How large is the fresh asparagus market in 2026?

The fresh asparagus market size reached USD 584.9 million in 2026 and is forecast to grow at a 7.70% CAGR toward 2031.

Which region consumed the most asparagus in 2025?

Asia-Pacific led with 38% of global consumption value, supported by rising Chinese imports and steady demand in Japan.

Why is organic asparagus growing faster than the conventional supply?

Retailer shelf mandates and consumer willingness to pay 7 to 36% premiums are pushing organic acreage to a projected 9.1% CAGR through 2031.

What is the impact of the 2025 United States tariff on Peruvian asparagus?

The 10% tariff took effect in April 2025 and is anticipated to raise United States retail prices 3-5% while redirecting some Peruvian volume to Europe and Asia.

Page last updated on: