Rapeseed Market Size and Share

Rapeseed Market Analysis by Mordor Intelligence

The rapeseed market size is expected to grow from USD 44.7 billion in 2025 to USD 46.61 billion in 2026 and is forecast to reach USD 57.53 billion by 2031 at 4.28% CAGR over 2026-2031. The market growth is primarily attributed to strengthening bio-fuel mandates across Europe and North America, increased incorporation in sustainable aviation fuel production, and the commodity's dual functionality as an oil and protein source. The implementation of Europe's Renewable Energy Directive III has intensified the demand for vegetable-oil feedstock. The United States' renewable diesel capacity, which exceeds 850,000 barrels of oil-equivalent per day in 2024, is projected to expand to 1.3 million barrels by 2035, subsequently impacting global supply dynamics. Market development is further supported by China's advancement in high-yield varieties and India's expansion of crushing capacity, particularly for protein meal production. Supply constraints stemming from climate variability in primary production regions continue to maintain robust price levels. The market structure is transforming strategic vertical integration initiatives by major agribusinesses and the incorporation of regenerative agriculture practices.

Key Report Takeaways

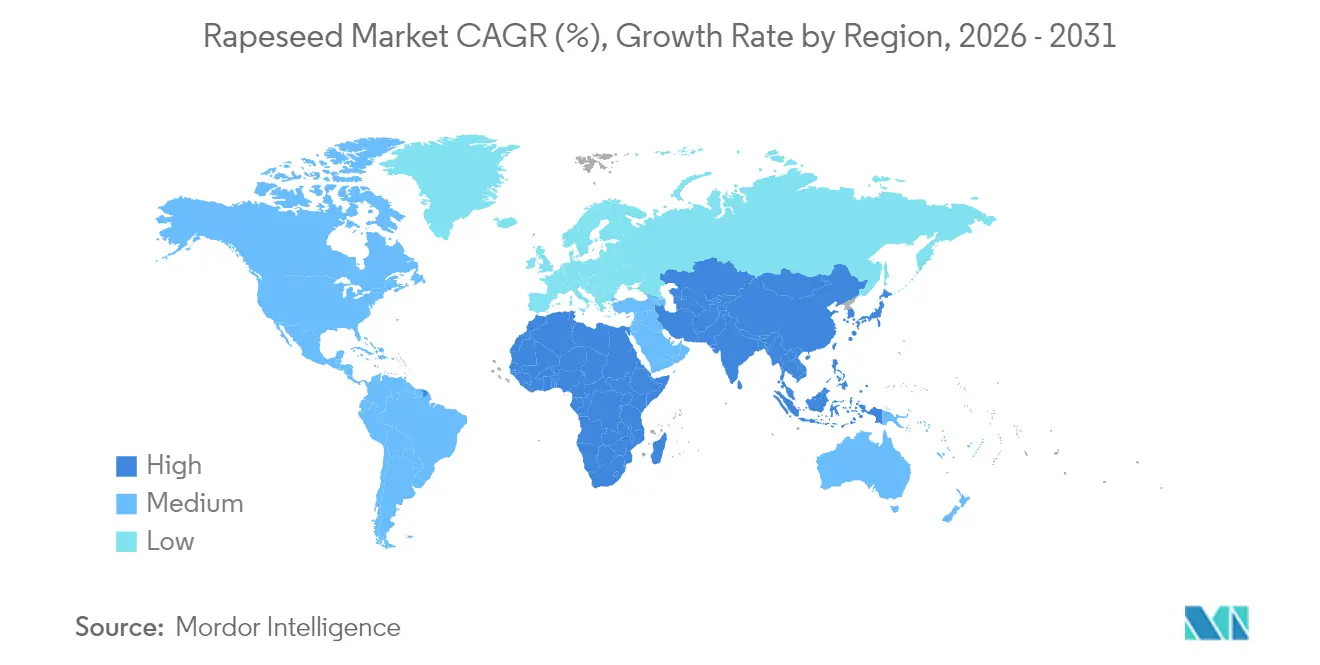

- By geography, Europe accounted for 34.85% of the rapeseed market share in 2025, and Asia-Pacific is registering the fastest growth at a 4.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapeseed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of bio-fuel mandates | +1.2% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Rising demand for plant-based protein meal | +0.8% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Favorable price spread versus other oilseed crops | +0.6% | Global, particularly Canada and Australia | Short term (≤ 2 years) |

| High-yield/lower erucic cultivar innovations | +0.5% | Global, early adoption in China and Europe | Long term (≥ 4 years) |

| Rapeseed oil as feedstock for sustainable aviation fuel | +0.4% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Carbon-credit revenue from regenerative rotations | +0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Bio-fuel Mandates

Bio-fuel policy acceleration is driving significant demand in the rapeseed market. Europe's Renewable Energy Directive III mandates a 14.5% greenhouse-gas intensity reduction in transport fuels by 2030, compelling refiners to increase their low-carbon feedstock procurement. In the United States, renewable diesel projects are expanding capacity to 1.3 million barrels of oil-equivalent per day by 2035, resulting in record rapeseed oil imports. The implementation of Indonesia's B35 mandate and Brazil's B15 target further increases the global vegetable-oil deficit, supporting rapeseed prices. European hydrotreated vegetable-oil demand is projected to increase by more than 400,000 metric tons in 2025, with rapeseed oil accounting for nearly half of this volume. The imposition of anti-dumping duties on Chinese biodiesel reinforces rapeseed's importance in meeting renewable-fuel requirements.

Rising Demand for Plant-Based Protein Meal

Rapeseed meal consumption is increasing across livestock, aquaculture, and human-nutrition sectors as an alternative protein source to soybean. The EU-27 consumed 13.75 million metric tons and China 12.54 million metric tons in 2024, demonstrating the growing global adoption of rapeseed[1]U.S. Department of Agriculture, “Oilseeds: World Markets and Trade,” usda.gov. Danish research developments in glucosinolate removal have created a human-grade protein concentrate suitable for food ingredients. Research indicates that rapeseed protein's amino-acid profiles match soybean quality and provide superior benefits for non-ruminant animals. Through fermentation processes, antinutritional factors have been reduced, enabling 25% fishmeal replacement in salmon feed and reducing aquaculture production costs. The pharmaceutical industry's extraction of bioactive peptides from rapeseed meal has created additional revenue opportunities and strengthened market growth.

Favorable Price Spread Versus Other Oilseed Crops

Rapeseed traded at USD 576.4 (EUR 500) per metric ton ex-farm in 2024, representing 2.5 times the value of soft-wheat prices, which incentivized agricultural expansion despite agronomic considerations. The crop's dual-purpose economic structure through oil and meal production provides income diversification against single-use crop volatility. Winter rapeseed integration during fallow periods in cereal rotations generates supplementary revenue without impacting prime-season crop allocation, particularly beneficial in regions experiencing climate stress. United States rapeseed plantings surpassed 1 million hectares in 2024, driven by renewable-fuel premium support above historical price benchmarks. The European production deficit, combined with Ukrainian logistical constraints, maintains favorable market fundamentals, sustaining rapeseed price levels.

Rapeseed Oil as Feedstock for Sustainable Aviation Fuel

U.S. renewable-diesel facilities are projected to increase their sustainable aviation fuel (SAF) production capacity to 834.4 million gallons by 2026, representing a twelve-fold increase from 2023 levels.[2] University of Illinois, “Sustainable Aviation Fuel Feedstocks,” illinois.edu The hydro-processed esters and fatty acids (HEFA) pathway continues to be the primary production method, with rapeseed oil reducing life-cycle carbon intensity by 40-80% compared to conventional jet fuel. The European Union's mandatory SAF blending requirements of 2% by 2025 and 6% by 2030, combined with U.S. tax incentives, have established a premium market that encourages long-term feedstock supply agreements. Research indicates that rapeseed-based SAF demonstrates a global warming potential that is at least 1.05 times lower than conventional jet fuel when compared on an energy-equivalent basis. The integration of SAF and renewable-diesel production facilities enables manufacturers to adjust their output according to market conditions, increasing operational flexibility and strengthening the demand for rapeseed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-driven pest and disease volatility | -0.7% | Global, acute in Europe and Canada | Short term (≤ 2 years) |

| Acreage competition from other oilseed crops | -0.5% | Global, strongest in North America and Asia | Medium term (2-4 years) |

| Sustainability caps on biodiesel | -0.4% | Europe and North America | Medium term (2-4 years) |

| GMO-threshold trade-policy uncertainty | -0.3% | Global trade flows, Europe-centric | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Pest and Disease Volatility

An increase of one degree Celsius in winter temperatures reduces UK rapeseed yields by 113 kg per hectare, resulting in USD 21.61 million (GBP 16 million) in annual losses for producers. Higher winter temperatures enable multiple generations of aphids, increasing virus transmission risk and pesticide expenditure, thereby reducing profit margins. Research demonstrates that the combination of elevated CO₂, heat, and ozone reduces omega-3 content by 45% and decreases oil yields by 58% in controlled trials, indicating potential quality deterioration under future climate conditions. The northward migration of pathogens, evidenced by clubroot detection beyond traditional boundaries in Scandinavia, necessitates enhanced biosecurity measures. While producers implement biological controls, resistant varieties, and precision monitoring to maintain yields, these measures increase operational complexity and costs, limiting rapeseed market expansion.

Acreage Competition from Other Oilseed Crops

The United States' soybean production, with 84.36 million harvested acres, significantly exceeds rapeseed cultivation and maintains profitability through established crushing facilities and export infrastructure. Palm oil maintains a competitive cost advantage in tropical regions, limiting rapeseed market penetration in price-sensitive segments, despite ongoing sustainability concerns. Brazil's soybean exports of 3.74 billion bushels in 2023 demonstrate the economies of scale that influence growers' crop selection. Agricultural models indicate North Dakota farmers transition to soybean cultivation when crush margins surpass rapeseed by USD 45 per metric ton. The combination of switching costs and operational learning requirements impedes rapeseed adoption in new regions, constraining market expansion opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Europe maintains a 34.85% share of the global rapeseed market in 2025 despite increasing import requirements due to weather-affected yields. France demonstrates acreage recovery, and Germany reports incremental area expansion, while reduced seed counts persist due to insufficient vernalization periods. The United Kingdom recorded a 12% decrease in output year-on-year due to flea beetle infestations, while demand remains consistent for biodiesel and culinary oil production. Ukraine increased export volumes to Europe despite logistical constraints, with Australia providing a supplementary supply, demonstrating Europe's strategic diversification of import sources. The region's hydrotreated vegetable oil production requirements will increase by 400,000 metric tons in 2025, sustaining crusher utilization and market stability.

Asia-Pacific holds the fastest growth rate at 4.68% CAGR through 2031 due to policy support and agronomic improvements. China's implementation of high-yield hybrids across 7 million hectares could increase domestic self-sufficiency by 14.5 percentage points, reducing edible oil import expenses. India's expanding poultry sector, growing at 9% annually, drives increased meal consumption. Australia strengthens its position through record rapeseed plantings and new crushing facilities near Perth, serving both domestic bio-fuel needs and export markets. Japan focuses on specialty oil production, including non-GMO food-service varieties, while South Korea imports rapeseed meal for aquaculture feed, creating diverse regional market opportunities.

North America benefits from supportive policies and agricultural advantages. The United States reached 1 million hectares of rapeseed cultivation in 2024, with North Dakota contributing 830,000 hectares, supported by improved crop insurance and favorable pricing. Canadian processors crushed 5.93 million metric tons in 2024, producing 2.49 million metric tons of oil and 3.47 million metric tons of meal for export to Mexico, Japan, and the United States. New processing facilities in Kansas and Saskatchewan will add 1.5 million metric tons of crushing capacity, strengthening regional supply. South America maintains a limited market presence, with Argentina's production restricted by soybean prevalence, though Brazil's southern regions show potential through winter-rapeseed trials.

Recent Industry Developments

- September 2024: Burcon NutraScience Corporation introduced Puratein, a rapeseed protein isolate that functions as an egg substitute in baked goods.

- June 2024: Bayer introduced the DEKALB rapeseed hybrid, DK401TL, to Western Canadian farmers. This hybrid is Bayer's highest-yielding rapeseed variety, outperforming competitor hybrids.

- April 2024: Cargill and CBH Group unveiled plans for a large-scale rapeseed-crushing plant near Perth to feed BP’s planned bio-fuel hub.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the rapeseed market as the total farm-gate value of rapeseed (canola) seed harvested worldwide and the first-stage value generated when that seed is crushed into oil and protein meal. The model tracks volume and price movements through growers, primary elevators, and crushers before the oil or meal is blended, refined, or retailed.

Scope exclusions: Consumer-packaged refined oils, downstream biodiesel retail sales, and farm-saved or brown-bag seed are not counted.

Segmentation Overview

- By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- North America

- United States

- Canada

- Mexico

- Europe

- Russia

- Germany

- United Kingdom

- Italy

- Spain

- France

- Poland

- Ukraine

- Asia-Pacific

- China

- India

- Japan

- Australia

- South America

- Brazil

- Argentina

- Middle East

- United Arab Emirates

- Turkey

- Iran

- Africa

- South Africa

- Egypt

- North America

Detailed Research Methodology and Data Validation

Primary Research

To verify numbers and fill data gaps, we interview growers in Saskatchewan, crushers in the Rhine corridor, biodiesel refiners in the U.S. Gulf Coast, and feed formulators across Jiangsu and Haryana. These conversations test yield assumptions, crush margins, and mandate compliance, then feed back into our working model.

Desk Research

Mordor analysts begin with authoritative agriculture datasets such as FAOSTAT, USDA-FAS PS&D, Eurostat, and International Grains Council trade sheets, which outline harvested acreage, yields, and cross-border flows. Trade association briefs from the Canadian Canola Council and the European Oilseed Alliance help us align subsidy, mandate, and sustainability policies with supply signals, while patent and crusher-capacity insights are pulled from Questel and D&B Hoovers. News and price series from Dow Jones Factiva, government gazettes, and selected peer-reviewed agronomy journals round out trend detection. The sources named here illustrate our desk research foundation and are not exhaustive.

Market-Sizing & Forecasting

A top-down and bottom-up framework is applied. First, national production, import, and ending-stock series are reconstructed to derive apparent consumption; crush rates convert seed to oil and meal value pools. Selective bottom-up checks, capacity roll-ups of 30 representative crushing plants and sampled ex-mill average selling prices, calibrate totals. Key variables include planted hectares, five-year yield trend, crush utilization, renewable diesel blending mandates, and export parity prices. A multivariate regression, supported by scenario analysis on weather anomaly and policy indices, projects the 2025-2030 trajectory. Data sparsity in smaller origins is bridged through regional averages that are stress-tested in expert calls.

Data Validation & Update Cycle

Outputs pass three filters: automated variance flags against long-run averages, peer review by a senior commodities analyst, and a final reconciliation with fresh customs filings before sign-off. The report is refreshed every twelve months, with interim revisions when major policy or crop updates emerge.

Why Mordor's Rapeseed Baseline Earns Decision-Maker Trust

Published estimates often diverge because firms choose different supply chain touchpoints, price levels, and refresh cadences.

Key gap drivers include narrower "oil-only" scopes, conservative acreage growth assumptions, or reliance on static average selling prices that ignore mandate-driven volatility. Mordor reports the integrated seed-to-meal value, updates acreage with each planting intention survey, and inflates prices using contemporaneous currency conversions, which together ground our 2025 baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.70 B (2025) | Mordor Intelligence | - |

| USD 27.60 B (2025) | Global Consultancy A | Tracks refined oil revenue only, excludes seed value and meal co-product |

| USD 15.00 B (2025) | Industry Database B | Uses traded seed volumes at CIF prices, omits domestic consumption and crush-margin uplift |

| USD 48.10 B (2025) | Regional Consultancy C | Applies retail bottle prices and blends historical CAGR without policy break points |

The comparison shows that once scope, price level, and update rhythm are aligned, Mordor's balanced model provides the most transparent and repeatable baseline for planners who cannot afford hidden assumptions.

Key Questions Answered in the Report

What is the size of the rapeseed market in 2026?

The rapeseed market is valued at USD 46.61 billion in 2026 and is projected to reach USD 57.53 billion by 2031 at a 4.28% CAGR.

Which region holds the largest share of the rapeseed market?

Europe leads with 34.85% of global rapeseed market share, driven by strong bio-diesel demand and established crushing infrastructure.

Which forces are most responsible for rising rapeseed demand?

Tightening bio-fuel mandates, expanding sustainable-aviation-fuel capacity, and strong appetite for plant-based protein meal are the key demand drivers.

How do renewable-fuel policies shape rapeseed consumption?

Renewable diesel and SAF incentives are adding hundreds of thousands of metric tons of annual vegetable-oil demand, making energy use the fastest-growing outlet for rapeseed oil.

What climate-related challenges could hinder rapeseed supply?

Warmer winters, shifting pest life-cycles, and more frequent disease outbreaks can trim yields and raise production costs, introducing volatility to global supply.

Page last updated on: