Asia Pacific Small Cell Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

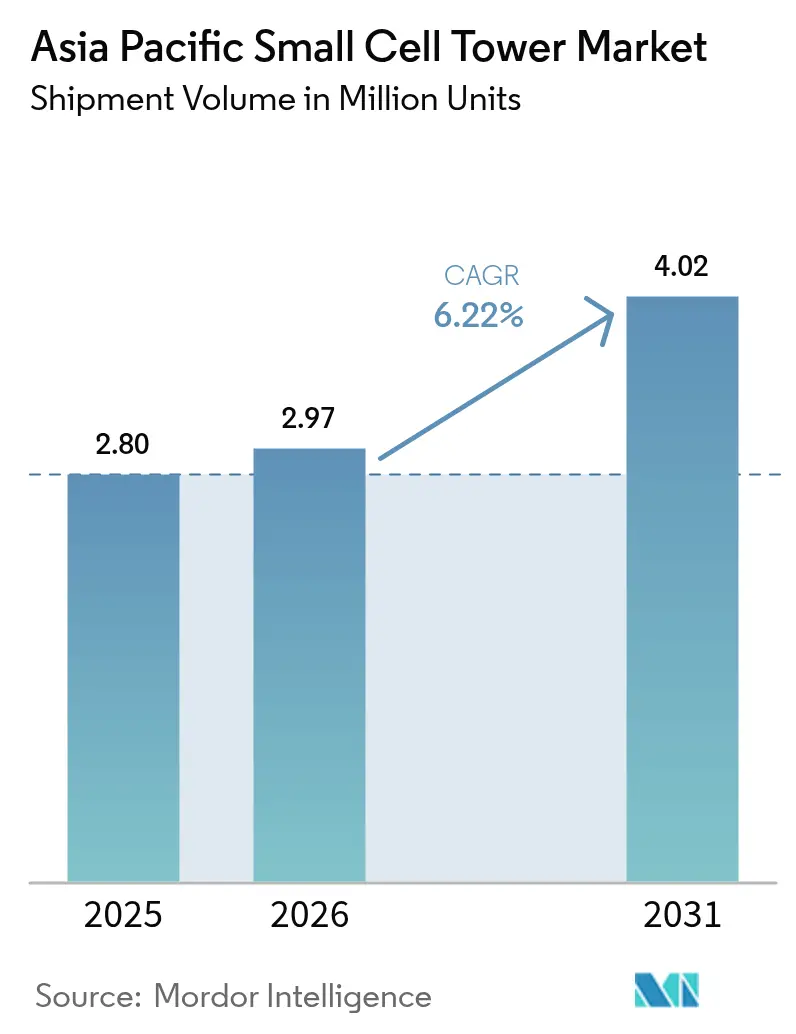

| Base Year Market Size (2025) | 2.80 Million units |

| Market Volume (2026) | 2.97 Million units |

| Market Volume (2031) | 4.02 Million units |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Small Cell Tower Market Analysis by Mordor Intelligence

The Asia Pacific small cell tower market size is expected to grow from 2.80 million units in 2025 to 2.97 million units in 2026 and is forecast to reach 4.02 million units by 2031 at 6.22% CAGR over 2026-2031. Rising data traffic density, accelerated 5G timelines, and state-led spectrum reforms have placed network densification at the center of operator strategy, driving continuous demand for compact radio sites. The need to relieve macro-layer congestion in business districts, transit hubs, and entertainment venues is encouraging large-scale outdoor rollouts, while emerging private 5G campus networks are strengthening indoor demand. Equipment vendors are responding with integrated 4G/5G radios, automated site-optimization software, and Open RAN-ready architectures that curb the total cost of ownership. Competitive intensity is increasing as neutral-host specialists and software-centric challengers court operators with capex-light deployment models. The combination of policy momentum, enterprise digitization, and technology modularity signals a multi-year expansion phase for the Asia Pacific small cell tower market.

Key Report Takeaways

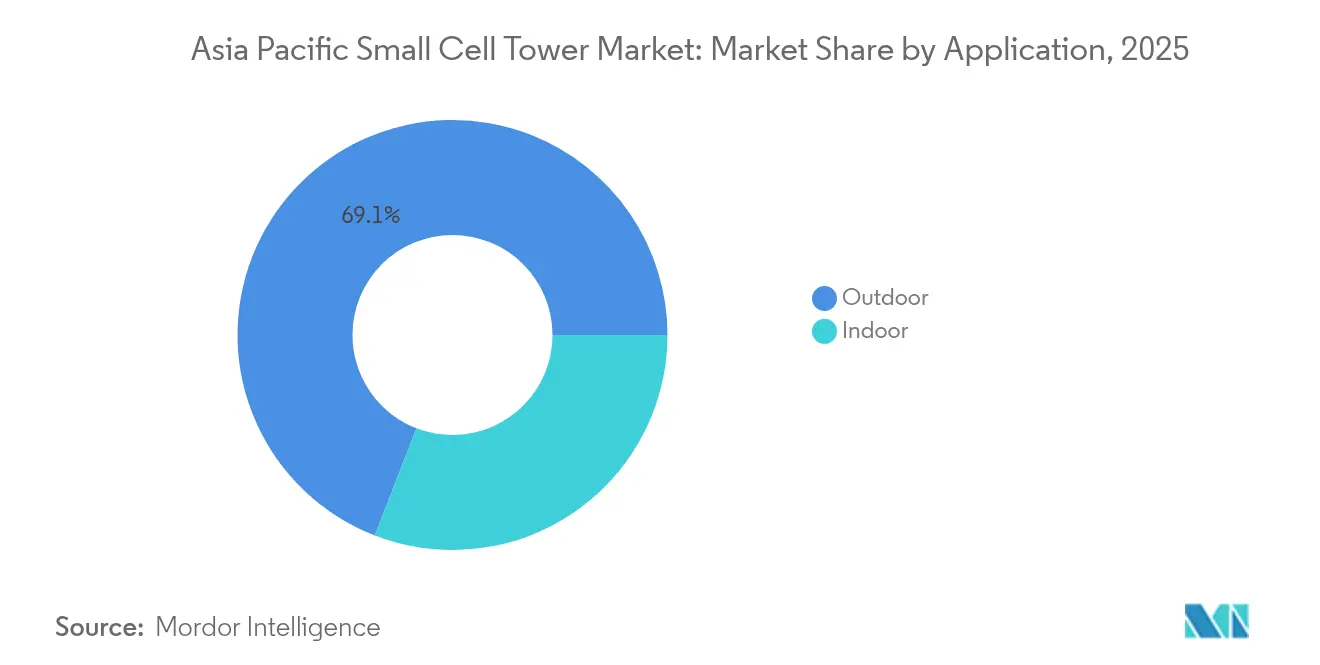

- By application, outdoor installations led with 69.12% of the Asia Pacific small cell tower market share in 2025; indoor deployments are projected to advance at a 7.32% CAGR through 2031.

- By network technology, 4G/LTE accounted for 50.32% of the Asia Pacific small cell tower market size in 2025, while 5G implementations are forecast to expand at an 7.98% CAGR through 2031.

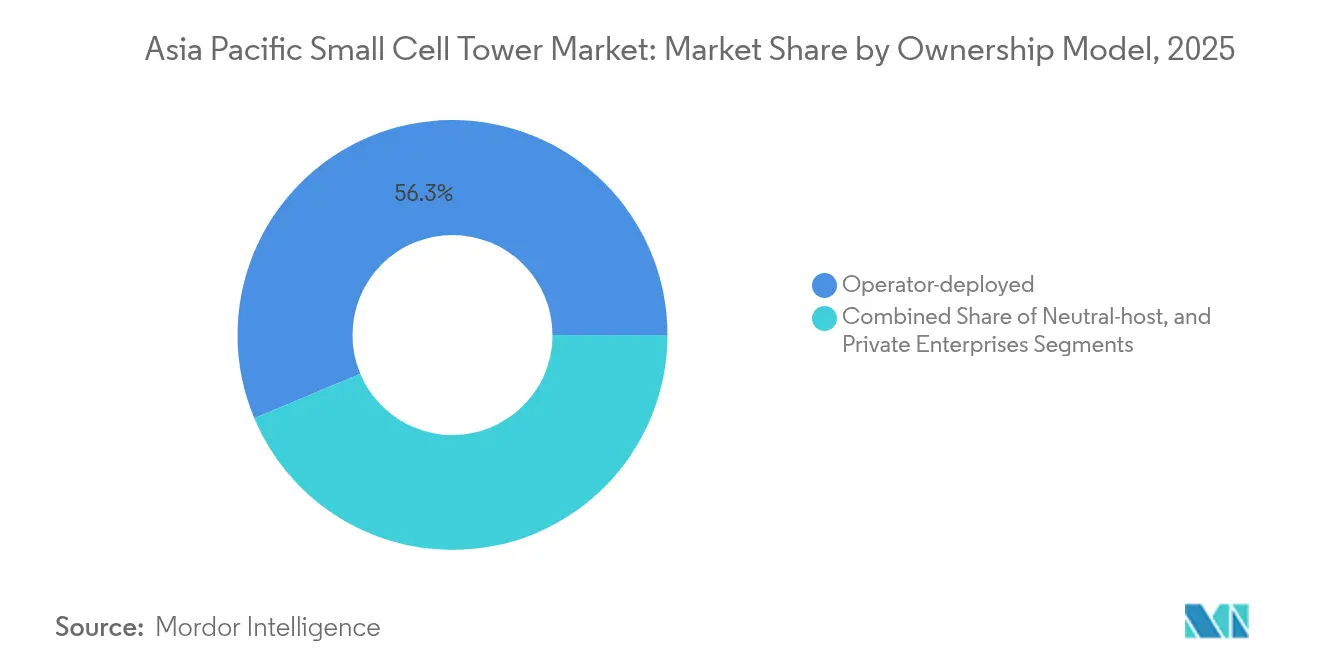

- By ownership model, operator-deployed sites held a 56.32% share of the Asia Pacific small cell tower market in 2025; private enterprise rollouts are set to grow at an 7.74% CAGR to 2031.

- By deployment location, urban nodes captured a 66.35% share of the Asia Pacific small cell tower market in 2025, whereas rural implementations are projected to grow at a 7.55% CAGR over the forecast horizon.

- By country, China accounted for a 39.76% share of the Asia Pacific small cell tower market in 2025, and India is projected to have the fastest growth at an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Small Cell Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid surge in mobile data traffic and densification requirements | +2.1% | China, India | Medium term (2-4 years) |

| Accelerated 5G rollout timelines across Asia Pacific | +1.8% | Asia Pacific core, emerging markets | Short term (≤ 2 years) |

| Government initiatives and supportive spectrum policies | +1.3% | Japan, Korea, Singapore | Long term (≥ 4 years) |

| Emergence of private 5G networks in manufacturing corridors | +0.9% | Southeast Asia, China | Medium term (2-4 years) |

| AI-powered self-optimizing networks lowering OPEX | +0.6% | Japan, Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Surge in Mobile Data Traffic and Densification Requirements

Mobile video streaming, cloud gaming, and workplace collaboration tools have triggered year-over-year traffic spikes of 40–60% in key metropolitan areas, exceeding the capacity of macro sites beyond their engineered limits.[1]Ericsson Mobility Report Team, “Mobile Data Traffic Outlook June 2024,” Ericsson, ericsson.com Operators now view dense grids of small cells as the most cost-efficient lever to add spectral reuse in real estate-constrained neighborhoods. Street-level poles, bus shelters, and building facades host these radios, minimizing landlord negotiations while shortening installation cycles. The densification imperative extends to airports, malls, and entertainment venues, where per-user throughput demands remain highest during peak hours. Vendors able to supply compact, multi-band radios that integrate 4G anchor carriers with 5G NR are securing preferred-supplier status. As a result, the Asia Pacific small cell tower market continues to mature from pilot deployments toward mass-scale grid planning.

Accelerated 5G Rollout Timelines Across Asia Pacific

Competitive announcements have condensed national 5G roadmaps by as much as 18 months, forcing operators to compress site-acquisition, civil works, and integration activities.[2]Ministry of Science and ICT, “Accelerated 5G Deployment Guidelines,” MSIT, msit.go.kr Governments in China and South Korea have linked infrastructure development to broader economic growth targets, releasing funds and public properties for accelerated deployment. Because small cells cover limited radii, they enable rapid 5G coverage overlays without waiting for new macro towers. Multi-technology radios that switch between NSA and SA modes help operators satisfy near-term coverage promises while laying groundwork for standalone cores. Integrated antennas, digital front-haul, and zero-touch provisioning tools are shortening time-to-revenue, underpinning robust demand for the Asia Pacific small cell tower market.

Government Initiatives and Spectrum Policies Supporting Small Cell Deployments

Regulators have reduced administrative friction by standardizing permit templates, increasing EIRP thresholds, and authorizing shared infrastructure frameworks. Japan’s Ministry of Internal Affairs and Communications reduced the license-processing window from three months to under four weeks, immediately increasing operator build rates. Singapore mandates neutral-host systems in high-footfall buildings, creating a guaranteed addressable base for shared small cell assets. Preferential spectrum blocks for industrial 5G in Korea and China further expand opportunities for private network suppliers. Policy clarity reduces business-case risk, enabling vendors and tower companies to invest capital in high-volume manufacturing and prefabricated site kits.

Emergence of Private 5G Networks in Manufacturing Corridors

Automotive, electronics, and logistics enterprises are funding dedicated 5G networks to automate production lines, track assets, and enable autonomous vehicles. Unlike operator deployments, these projects prioritize indoor coverage, deterministic latency, and high uplink capacity. Small cells act as the local-access layer, backhauled to on-premise 5G cores that safeguard intellectual property. Vendors offering pre-integrated radio-core packages and simplified spectrum-licensing support are winning contracts across Vietnam’s electronics clusters and Malaysia’s automotive parks. The private-network pivot diversifies the Asia Pacific small cell tower industry’s revenue streams beyond carrier capex cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex site acquisition and permitting hurdles | −1.4% | India, Indonesia | Medium term (2-4 years) |

| High upfront capital expenditure | −1.1% | Emerging Asia Pacific | Short term (≤ 2 years) |

| Interference management in shared spectrum | −0.8% | Dense metros | Long term (≥ 4 years) |

| Semiconductor supply-chain disruptions | −0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Site Acquisition and Permitting Hurdles

Municipal zoning disparities prolong approval cycles and inflate leasing charges, especially across tier-1 Indian cities where building owners demand premium rents.[3]Surajeet Das Gupta, “Site-Acquisition Hurdles Slow 5G Rollout,” Economic Times, economictimes.indiatimes.com Some jurisdictions require separate no-objection certificates from fire, aviation, and heritage departments, which can extend project timelines. The absence of standardized fee structures complicates network planning, as per-site cost variability challenges return-on-investment calculations. Operators often negotiate rooftop access on an ad-hoc basis, delaying grid densification and capping near-term shipment volumes for the Asia Pacific small cell tower market.

High Upfront Capital Expenditure for Dense Deployments

Site hardware, fiber backhaul, power provisioning, and installation labor lift per-node capex to USD 15,000–40,000. Operators in low-ARPU territories struggle to absorb such outlays while simultaneously bidding for mid-band spectrum. Financing constraints, therefore, skew deployments toward cash-rich incumbents, limiting competitive parity and stalling overall grid-density gains. Multilateral funding initiatives and equipment-leasing models are emerging, yet economic pressures remain a brake on volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Indoor Deployments Broaden Coverage Horizons

Indoor sites captured 30.88% of shipments in 2025, equivalent to approximately 0.86 million units of the Asia Pacific small cell tower market size, and are projected to track a 7.32% CAGR to 2031. Enterprises view robust indoor 5G as non-negotiable for customer engagement tools, cashier-less checkouts, and immersive retail displays. Consequently, shopping malls, airports, and stadiums allocate capital expenditure budgets exclusively for small cell layers rather than Wi-Fi upgrades. Neutral-host operators bundle these systems into long-term service agreements, easing budget approval while ensuring multi-carrier access.

Outdoor deployments continue to anchor the Asia Pacific small cell tower market, accounting for 69.12% of the 2025 volumes. Operators use pole-mount and wall-mount radios in alleyways and transit corridors to alleviate macro-sector congestion during peak commuting hours. Integrated street-furniture designs blend radios, power modules, and backhaul links into aesthetically pleasing housings, thereby satisfying municipal ordinances. Although outdoor grids remain the dominant revenue stream, the rising momentum in indoor grids underscores the market’s dual-track growth narrative.

By Network Technology: 5G Adds Momentum as 4G Persists

4G/LTE radios comprised 50.32% of 2025 shipments, equivalent to 1.41 million units in the Asia Pacific small cell tower market size, reflecting operators’ preference for maximizing existing spectrum allocations. Yet 5G radios are expanding at an 7.98% CAGR as carriers introduce mid-band and mmWave layers that support multi-gigabit peak throughput. Combo radios that deliver dual-standard coverage preserve site rent outlays and accelerate user migration.

Multi-technology platform adoption also addresses the realities of device mix. In late 2025, 5G smartphone penetration sits below 45% in many Southeast Asian markets, compelling operators to retain 4G anchor links for voice services and IoT endpoints. Gradual sunset plans for 3G free additional spectrum, enabling carriers to refarm bandwidth for 5G NR, thus reinforcing demand for software-upgradable radios.

By Ownership Model: Enterprise Capital Unlocks New Revenue Pools

Operator-owned assets generated 56.32% of 2025 shipments but face share dilution as enterprises finance private grids. Manufacturing plants, logistics depots, and office campuses are turning to on-premise networks to satisfy deterministic service-level agreements. This category is expected to grow at an 7.74% CAGR, adding approximately 372,000 units by 2031.

Neutral-host providers enter as intermediary landlords, leasing spectrum slices and fiber backhaul to multiple operators within a shared radio network. This model aligns with public policy goals in Singapore and Australia, where governments aim to avoid redundant street furniture clutter. By alleviating capex burdens, neutral hosts speed nodal density, indirectly boosting shipment volumes for the Asia Pacific small cell tower market.

By Deployment Location: Rural Expansion Adds Incremental Volume

Urban municipalities accounted for 66.35% of 2025 shipments, driven by dense population clusters and persistent mobile video usage. However, rural rollouts are forecast to grow at a 7.55% CAGR as universal-service programs release subsidies for digital inclusion. Governments in India and Indonesia allocate grants covering up to 30% of the costs for radio, power, and trenching, thereby de-risking operator participation.

Suburban belts form an intermediate growth layer. New housing developments in Thailand and Vietnam bundle fiber backhaul and smart-city services, prompting carriers to deploy small cells alongside smart-lighting poles. As suburban economies mature, per-capita data consumption climbs, unlocking fresh densification budgets and sustaining shipment momentum.

Geography Analysis

China shipped approximately 1.11 million units in 2025, accounting for a 39.76% share of the Asia Pacific small cell tower market. China’s leadership arises from a synchronized ecosystem of equipment suppliers, tower companies, and municipal authorities. Central funding lowers borrowing costs, while urban planning bodies allocate standardized pole designs, accelerating the average deployment interval to under 45 days. Large-scale procurement contracts unlock volume discounts, enabling nationwide coverage sweeps that surpass those of regional competitors. Industrial parks in Shenzhen and Chongqing host dedicated private 5G networks, each featuring hundreds of indoor small cells that support machine-vision quality control and AGV fleets.

India, although trailing in absolute volume, is projected to have an 8.43% CAGR through 2031, driven by Jio’s 50,000-site rural order book and Airtel’s enterprise-centric expansion. India’s momentum builds on competitive rivalry and an expanded spectrum roadmap. Airtel’s deal with Ericsson for 10,000 urban small cells emphasizes enterprise service differentiation through assured indoor performance. Jio’s USD 500 million rural program combines commercial incentives with universal-service obligations, ensuring revenue visibility and alignment with social impact. State-level right-of-way harmonization further trims lead times.

Japan and South Korea serve as technological bellwethers. KT’s USD 300 million mmWave contract with Samsung uses pole-mounted 28 GHz radios to support autonomous-vehicle corridors in Seoul’s CBD. NTT DOCOMO’s AI-driven optimization trial with Nokia demonstrates contiguous self-healing clusters, reducing call-drop rates by 30% during festivals. These pioneering deployments shape global standards and vendor roadmaps, enhancing the reputational value of successful suppliers.

Southeast Asian nations, led by Thailand and Vietnam, adopt neutral-host models to sidestep capex limitations. Regulatory clarity on cost-sharing and pole aesthetics encourages tower companies to aggregate demand across carriers. Baicells’ Open RAN certification in Thailand opens a low-cost equipment avenue for emerging ISPs, democratizing access to the Asia Pacific small cell tower market.

Competitive Landscape

Supplier dynamics reveal a mid-tier concentration wherein the top five vendors control roughly 62% of shipments, leaving meaningful whitespace for software-defined entrants. Huawei leverages vertically integrated silicon and optics to deliver cost-efficient turnkey packages. Ericsson and Nokia differentiate themselves through multi-standard radios and cloud-native RAN software, attracting operators who are pursuing vendor diversity. Samsung’s silicon control positions it favorably for mmWave grids.

Parallel Wireless and Baicells leverage Open RAN interfaces to separate hardware and software, reducing bill-of-materials costs in price-sensitive markets. Patent race intensity escalates as firms register antenna array innovations that mitigate interference in densely populated urban areas.[4]IEEE Spectrum, “Antenna Design and Interference Mitigation,” IEEE, ieee.org Neutral-host tower firms partner with equipment vendors on revenue-share deals, bundling installation, fiber backhaul, and AI analytics into end-to-end managed services.

The Asia Pacific small cell tower market, therefore, balances scale economics with rapid technological evolution. Vendors that fuse R&D heft, channel depth, and agile software roadmaps are best positioned to capture incremental volume and margin upside.

Asia Pacific Small Cell Tower Industry Leaders

Huawei Technologies Co., Ltd.

Telefonaktiebolaget LM Ericsson

Nokia Corporation

ZTE Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ericsson announced a strategic partnership with China Mobile to deploy AI-powered small cell networks across 20 major Chinese cities, representing a USD 400 million investment in autonomous network optimization technology. The deployment will feature self-healing capabilities and predictive maintenance systems.

- September 2025: Samsung completed the world's first commercial 6G-ready small cell trial in Seoul, demonstrating terahertz frequency capabilities and ultra-low latency applications for autonomous vehicle networks. The trial achieved data speeds exceeding 1 terabits per second (Tbps) in controlled environments.

- August 2025: Nokia secured a USD 250 million contract with Bharti Airtel to deploy Open RAN small cells across India's tier-2 cities, focusing on interoperable solutions that support multiple vendor ecosystems and reduce operator lock-in risks.

- July 2025: Huawei has launched its next-generation small cell platform, featuring integrated AI processing capabilities that enable real-time network optimization and reduce energy consumption by 40% compared to previous-generation equipment.

- June 2025: Reliance Jio announced the completion of its rural small cell expansion program, deploying 75,000 units across underserved areas and achieving 95% population coverage in targeted regions through government partnership initiatives.

- May 2025: NTT DOCOMO and Fujitsu established a joint venture for small cell manufacturing in Japan, targeting export markets across Southeast Asia and focusing on disaster-resilient network solutions for typhoon-prone regions.

Asia Pacific Small Cell Tower Market Report Scope

Small cell towers are low-power, short-range wireless transmission devices that may cover a small geographic region or be used indoors and outdoor. Small cell towers play an important role in efficiently offering high-speed mobile internet and other low-latency applications in 5G deployments.

The Asia-Pacific Small Cell Tower Market is Segmented Application (Outdoor and Indoor) and Country (China, South Korea, Japan, India, Philippines, Rest of Asia Pacific).The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Outdoor |

| Indoor |

| 3G |

| 4G/LTE |

| 5G |

| Operator-deployed |

| Neutral-host |

| Private enterprises |

| Urban |

| Suburban |

| Rural |

| China |

| South Korea |

| Japan |

| India |

| South-East Asia |

| Rest of Asia Pacific |

| By Application | Outdoor |

| Indoor | |

| By Network Technology | 3G |

| 4G/LTE | |

| 5G | |

| By Ownership Model | Operator-deployed |

| Neutral-host | |

| Private enterprises | |

| By Deployment Location | Urban |

| Suburban | |

| Rural | |

| By Country | China |

| South Korea | |

| Japan | |

| India | |

| South-East Asia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What shipment volume is forecast for Asia Pacific small cell towers by 2031?

The region is projected to reach 4.02 million units by 2031, expanding from 2.97 million units in 2026.

Which application category is growing fastest for small cells in Asia Pacific?

Indoor deployments, especially in malls and airports, are advancing at a 7.32% CAGR through 2031.

How large is China’s share of Asia Pacific small cell tower demand?

China commanded 39.76% of 2025 shipments, underpinned by state-backed infrastructure programs.

Why are private 5G networks important to small cell suppliers?

Manufacturing and logistics enterprises are financing their own grids, pushing an 7.74% CAGR for private deployments to 2031.

What is the main hurdle slowing urban small cell rollouts?

Lengthy site-acquisition and permitting processes can extend deployment timelines by up to 12 months in major cities.

Which new technology feature is cutting operating costs for dense small cell networks?

AI-powered self-optimizing software reduces manual retuning visits and can lower OPEX by 30%.

Page last updated on: