China Optoelectronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.34 Billion |

| Market Size (2026) | USD 7.63 Billion |

| Market Size (2031) | USD 9.27 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

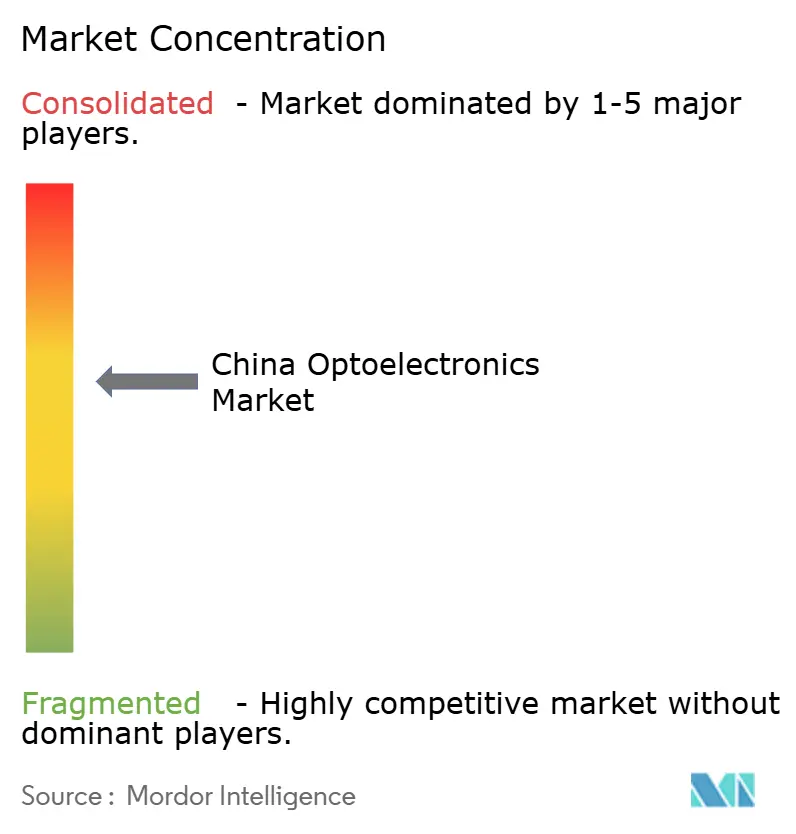

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Optoelectronics Market Analysis by Mordor Intelligence

The China optoelectronics market size is expected to grow from USD 7.34 billion in 2025 to USD 7.63 billion in 2026 and is forecast to reach USD 9.27 billion by 2031 at 3.96% CAGR over 2026-2031. The measured growth pace signals a maturing competitive landscape as state-backed initiatives shift capital from volume-driven LED lighting toward compound semiconductors, laser diodes, and advanced packaging. Policy-mandated localization requirements, combined with a widening 5G and data-center build-out, continue to redirect demand from commodity illumination to higher-margin optical communication and sensing solutions. Upstream, gallium nitride and silicon carbide wafer capabilities gain priority funding, while downstream players pursue vertical integration to mitigate U.S. export-control risks. Consolidation accelerates among domestic champions that leverage government incentives, but capital intensity and talent shortages keep entry barriers high for smaller firms.

Key Report Takeaways

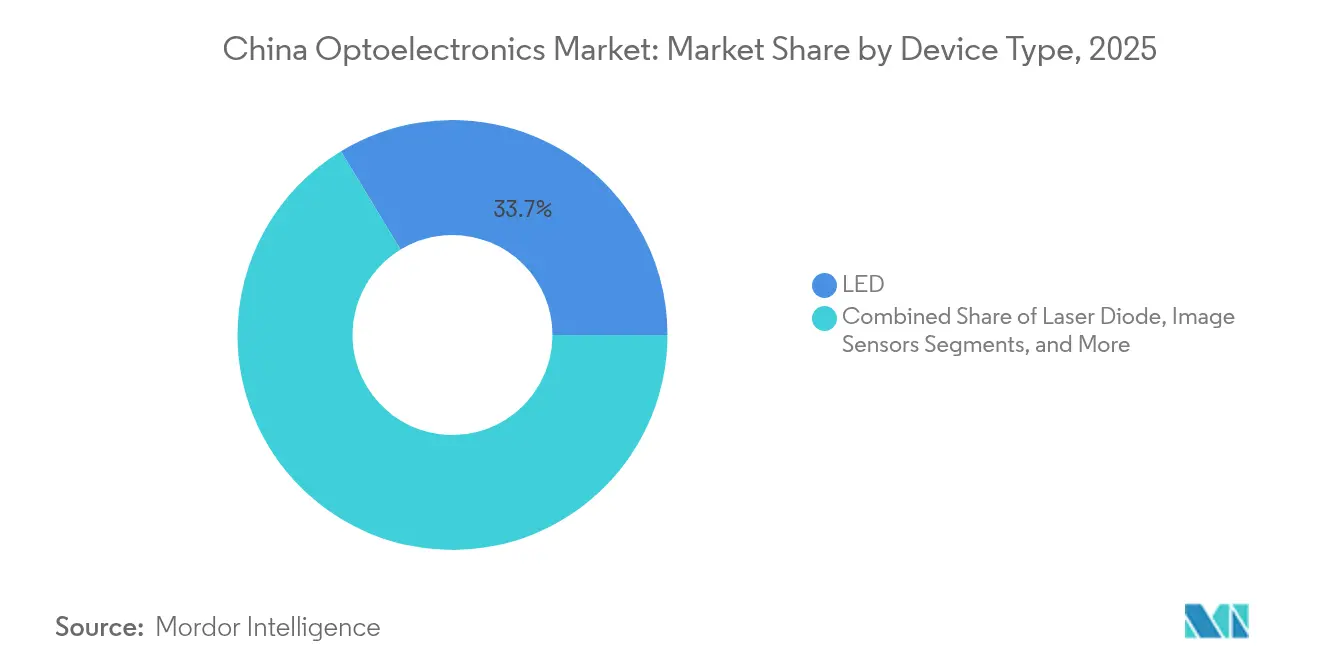

- By device type, LED components led with a 33.68% revenue share in 2025, whereas laser diodes are forecast to post the fastest growth at a 4.86% CAGR to 2031.

- By material, gallium nitride dominated with a 41.75% China optoelectronics market share in 2025, while silicon carbide is on course for a 4.45% CAGR through 2031.

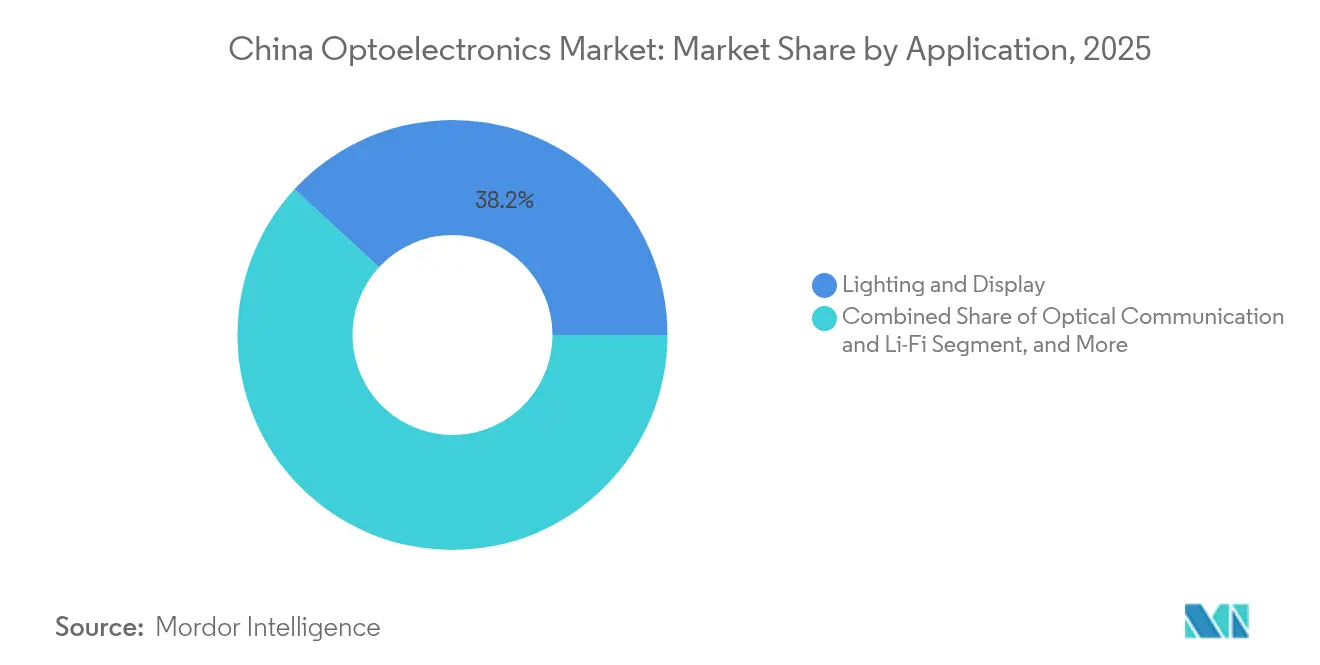

- By application, lighting and displays retained a 38.15% share in 2025; however, optical communication and Li-Fi are projected to expand at a 5.14% CAGR through 2031.

- By end user, consumer electronics accounted for 42.64% of the China optoelectronics market size in 2025, whereas automotive applications carried the strongest 5.72% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Optoelectronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push for domestic semiconductor supply chains | +0.8% | National, centered in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Rapid LED mini- and micro-LED commercialization | +1.2% | Guangdong and Jiangsu | Short term (≤ 2 years) |

| 5G- and data-center-driven optical-transceiver demand | +0.9% | Tier-1 cities and industrial clusters | Medium term (2-4 years) |

| Electric-vehicle LiDAR integration | +0.7% | Early adoption in Beijing, Shanghai, Shenzhen | Long term (≥ 4 years) |

| Carbon-neutral policies accelerating photovoltaic adoption | +0.6% | Western provinces | Long term (≥ 4 years) |

| Emerging quantum-dot image-sensor start-ups | +0.3% | Beijing, Shanghai, Shenzhen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for Domestic Semiconductor Supply Chains

The third phase of the National Integrated Circuit Industry Investment Fund injected more than USD 40 billion in 2024, with a clear mandate to scale compound-semiconductor capacity critical for optoelectronic devices. Subsidized fab projects lower effective capital costs, lock in bank financing, and guarantee procurement channels through local-content rules. Collectively, these measures tilt purchasing toward domestic LED, laser diode, and sensor vendors, creating a baseline floor for the China optoelectronics market even during cyclical slowdowns. The policy also shortens technology-learning curves by financing joint pilot lines with university partners. Over the medium term, the localization agenda should close process-technology gaps in metal-organic chemical vapor deposition and ion implantation.

Rapid LED Mini and Micro-LED Commercialization

BOE Technology transitioned from pilot to volume mini-LED backlighting for premium smartphones and tablets in 2024, validating mass-transfer processes that reduce die-bonding cycle times by 35%.[1]BOE Technology Group Co., Ltd. Company News, “BOE Technology Mini-LED Production Capacity,” BOE Technology Group Co., Ltd. www.boe.com Unit-cost compression widens the addressable tier-two handset and TV segments, accelerating revenue capture for domestic substrate, driver-IC, and packaging firms. Color gamut and lifetime advantages over OLED win OEM design slots, while trade policy dynamics render overseas supply less competitive on landed cost. Rapid-qualifier programs at Shenzhen-based contract assemblers enable six-month design-win cycles, compared with nine months or more for foreign rivals. As a result, the China optoelectronics market benefits from higher average selling prices and lower churn risk versus commoditized LED lighting.

5G- and Data-Center-Driven Optical Transceiver Demand

China surpassed 3.6 million installed 5G macro sites by end-2024, each requiring multiple 25G-plus optical modules for fronthaul and backhaul links. Hyperscale cloud providers simultaneously ramp 400G and 800G optics to feed AI training clusters. Local transceiver makers, supported by procurement preferences, translate proximity into faster design iterations and reduced field-failure rates. Supply-chain localization also mitigates geopolitical risk for cloud operators hosting critical workloads. Demand visibility extends into the medium term as deployment roadmaps move toward 6G testbeds, reinforcing a multi-year revenue stream for optical-component vendors within the China optoelectronics market.

Electric Vehicle LiDAR Integration

BYD, NIO, and other domestic OEMs introduced solid-state LiDAR on mid-tier models in 2024, advancing the sensor from luxury niche to mass option packages. Cost decline stems from in-house laser diode and photodetector fabrication, coupled with ASIC-level signal-processing integration. Transition toward 1550 nm architectures raises demand for indium phosphide wafers, catalyzing new epitaxy investments. Over the long term, wider LiDAR adoption is expected to double automotive laser-diode unit volumes, diversifying revenue away from saturated handset 3D-sensing applications and driving incremental growth for the China optoelectronics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US-China tech export controls | -0.9% | Advanced fabs nationwide | Short term (≤ 2 years) |

| Talent shortage in compound-semiconductor processing | -0.4% | Beijing, Shanghai, Shenzhen, Wuhan | Medium term (2-4 years) |

| High CAPEX for 8-inch GaN and SiC fabrication | -0.5% | Leading semiconductor hubs | Medium term (2-4 years) |

| Price erosion in LED backlighting | -0.3% | Guangdong and Jiangsu | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

US-China Tech Export Controls

The October 2024 revision of U.S. regulations curtailed shipments of advanced gallium-nitride and silicon-carbide equipment, lengthening tool-procurement lead times to more than 18 months. Domestic fabs either run older-node reactors or accelerate in-house tool designs, both scenarios depressing initial yields and raising cost per wafer. Multinational suppliers postpone local service-center expansion, further delaying ramp schedules. Consequently, near-term wafer output lags demand from EV and 5G segments, trimming the China optoelectronics market CAGR during the first two forecast years.

High CAPEX for 8-inch GaN and SiC Fabrication

A single 8-inch GaN line surpasses USD 500 million in base investment, while SiC fabs can breach USD 700 million after substrate prep and high-temperature furnaces. Financing such outlays stresses even well-capitalized firms when coupled with protracted payback cycles. Smaller entrants default to 6-inch retrofits, which suffer from inferior die economies, leaving the supply-base highly concentrated. Without fresh equity or state subsidies, wafer shortages could persist, limiting downstream module scale and tempering the China optoelectronics market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Laser Diodes Drive Premium Applications

Laser diodes are expected to contribute a 4.86% CAGR through 2031, outperforming the broader China optoelectronics market despite LEDs retaining a 33.68% revenue lead in 2025. Rising LiDAR attach rates and data-center optics create resilient demand buffers that cushion cyclical swings in handset VCSEL volumes. The price elasticity of LEDs erodes margins, prompting vendors to migrate capacity to coherent-light products where ASPs exceed USD 20 per unit. Industrial laser arrays for metal cutting and additive manufacturing further widen addressable revenue pools, while optocouplers maintain utility in power-conversion isolation despite slower growth.

In parallel, photovoltaic cells wrestle with overcapacity-led price compression yet still benefit from grid-parity projects under carbon-neutral mandates. Image-sensor volumes climb on dual- and triple-camera smartphone designs, but value capture shifts toward stacked-pixel architectures that embed logic under photodiodes. Collectively, these shifts raise the blended ASP across device categories, helping the China optoelectronics market offset slower unit expansion.

By Device Material: Silicon Carbide Gains Traction

Silicon carbide posted the fastest 4.45% CAGR, nibbling at gallium nitride’s 41.75% revenue dominance in 2025. EV traction inverters and 5G base-station PA modules value SiC’s superior thermal conductivity, enabling higher power density and reduced cooling overhead. Tianjin Zhonghuan’s 200 mm SiC substrate breakthrough cut defect density by 40%, narrowing the cost delta with GaN and supporting wider adoption. GaN retains an edge in fast-switching chargers and RF front-ends, while indium phosphide rises for 1550 nm automotive LiDAR lasers. The shift toward compound semiconductors magnifies equipment-qualification hurdles but unlocks premium pricing that smooths gross-margin volatility across the China optoelectronics market.

Traditional silicon and gallium arsenide remain relevant in mid-power LED lamps and handset P-As but face secular share drift to higher-performance alternatives. Process-yield improvements and localized substrate supply are strategic for sustaining competitive cost structures as the China optoelectronics industry advances.

By Application: Optical Communication Accelerates

Optical communication and Li-Fi registered a 5.14% CAGR, eclipsing lighting’s 38.15% share benchmark in 2025. AI server clusters demand 800G links at rack-scale, driving multi-mode VCSEL and single-mode EML proliferation. Telecom operators fast-track fiber-deep 5G backhaul, deploying coherent transceivers that rely on narrow-line-width lasers and modulators. The convergence of datacom and telecom architectures amplifies unit demand and intensifies design-win competition within the China optoelectronics market.

Sensing and imaging expand through factory automation and autonomous mobility, but price erosion in LED backlight panels compresses legacy revenues. Defense and security verticals remain protected niches, insulated from pricing cycles by stringent qualification protocols yet capped by export-license controls that limit volume scale.

By End-User Industry: Automotive Transformation Accelerates

Automotive applications are set to deliver the highest 5.72% CAGR, challenging consumer electronics’ 42.64% 2025 share lead. Battery-electric platforms incorporate matrix LED headlights, ambient-lighting strips, and multi-sensor ADAS suites, each embedding photonics content multiple times that of internal-combustion predecessors. Domestic Tier-1 suppliers partner directly with LED and laser fabs to co-develop automotive-grade packages, locking in multi-year volume contracts. As government subsidy tapering shifts value perception to safety and connectivity, optoelectronic-content growth cushions any EV sales plateau, reinforcing the China optoelectronics market trajectory.

Telecom and cloud data-center operators sustain double-digit demand for high-speed optics, while healthcare upgrades to high-resolution endoscopes and diagnostic scanners. Industrial automation adds machine-vision nodes, and aerospace implements fiber-optic gyros, contributing incremental diversity to the China optoelectronics industry revenue mix.

Geography Analysis

Regional clusters drove roughly 74.68% of China optoelectronics market value in 2025, with the Yangtze River Delta leading due to Shanghai’s R&D and Jiangsu’s packaging scale. Vertical-integration models flourish here; BOE Technology and Sanan Optoelectronics co-locate substrate, epi, and module lines to streamline logistics and tap a deep engineering talent base. The Pearl River Delta follows, with Shenzhen anchoring consumer electronics-oriented supply chains and benefiting from Hong Kong’s trade and finance ecosystem.

Beijing’s Zhongguancun Science Park houses quantum-dot and silicon-photonic start-ups that spin out of Tsinghua and Peking Universities, leveraging proximity to venture funding and state labs. Wuhan’s “Optics Valley” specializes in laser-tech clusters, capitalizing on Huazhong University’s photonics faculty and attracting more than 300 enterprises by 2024. These inland hubs diversify geographic risk and alleviate coastal wage inflation, aligning with central government regional development mandates. Second-tier cities such as Xi’an, Chengdu, and Hefei offer tax holidays and lower land rates that entice capacity-expansion projects, including BOE’s 2025 micro-LED fab announcement in Hefei. The dispersion strategy aims to foster complementary skill pools and ensure redundancy against localized supply-chain shocks, collectively sustaining the nationwide China optoelectronics market growth engine.

Competitive Landscape

Top-10 suppliers controlled roughly 45% of 2024 revenue, signaling moderate concentration within the China optoelectronics market. Market leaders adopt end-to-end integration, spanning substrate fabrication to final module assembly, to secure scale benefits and lower bill-of-materials volatility. BOE Technology’s acquisition of U.S. micro-LED innovator Rohinni granted it proprietary mass-transfer IP, fast-tracking next-gen display roadmaps. Sanan Optoelectronics expanded its playbook by acquiring a German compound-semiconductor equipment manufacturer in 2025 to mitigate export-control exposure.

Patent-application volumes in compound-semiconductor processing climbed 35% year-on-year in 2024, underscoring a race for defensible technology positions. Emerging challengers specialize in high-value niches such as quantum-dot sensors and SiC MOSFETs, leveraging agility to out-innovate incumbents in narrow domains. Strategic alliances with foreign automotive Tier-1 Suppliers, highlighted by HC Semitek’s 2024 partnership with Continental and its 2025 supply deal with Tesla, validate its quality credentials and open export pathways.

Financing dynamics favor firms able to secure central-government seed funds or local-government land grants, yet continued CAPEX escalation may accelerate future mergers as smaller players seek economies of scale. The net effect sustains a mid-level concentration that balances innovation diversity with adequate scale economies, keeping the China optoelectronics industry competitively vigorous.

China Optoelectronics Industry Leaders

BOE Technology Group Co., Ltd.

Shenzhen China Star Optoelectronics Technology Co., Ltd.

Sanan Optoelectronics Co., Ltd.

HC Semitek Corporation

Leyard Optoelectronic Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BOE Technology committed USD 2.1 billion to build China’s first mass-production micro-LED fab in Hefei, targeting smartphone and automotive displays.

- September 2025: Sanan Optoelectronics acquired a German compound semiconductor equipment firm for USD 450 million, gaining access to advanced GaN reactor designs that were previously subject to U.S. export controls.

- August 2025: China’s Ministry of Industry and Information Technology has launched the National Optoelectronics Innovation Center, backed by USD 800 million in initial funding, to accelerate research in quantum-dot, silicon-photonics, and laser technologies.

- July 2025: HC Semitek won a USD 320 million LED-component contract with Tesla’s Gigafactory Shanghai for interior and exterior automotive lighting.

China Optoelectronics Market Report Scope

Optoelectronics is the field of technology concerned with electronic device applications for sourcing, detecting, and controlling light. It encompasses the design, manufacture, and study of electronic hardware devices that, as a result, convert electricity into photon signals for various purposes, such as medical equipment, telecommunications, and general science.

The China optoelectronics market is segmented by component type (photo voltaic (PV) cells, optocouplers, image sensors, light emitting diodes (LED), laser diode (LD), infrared components (IR), and component types) and end-user (aerospace & defense, automotive, consumer electronics, information technology, healthcare, residential and commercial, industrial, and other end-user industries). The report offers market forecasts and size in value (USD) for all the above segments.

| LED |

| Laser Diode |

| Image Sensors |

| Optocouplers |

| Photovoltaic Cells |

| Other Device Types |

| Gallium Nitride (GaN) |

| Gallium Arsenide (GaAs) |

| Silicon Carbide (SiC) |

| Indium Phosphide (InP) |

| Silicon and Other Device Materials |

| Lighting and Display |

| Optical Communication and Li-Fi |

| Sensing and Imaging |

| Power Conversion and Photovoltaics |

| Other Applications |

| Consumer Electronics |

| Automotive |

| Information Technology and Telecom |

| Healthcare and Life-Sciences |

| Aerospace and Defense |

| Industrial Automation |

| Other End-user Industries |

| By Device Type | LED |

| Laser Diode | |

| Image Sensors | |

| Optocouplers | |

| Photovoltaic Cells | |

| Other Device Types | |

| By Device Material | Gallium Nitride (GaN) |

| Gallium Arsenide (GaAs) | |

| Silicon Carbide (SiC) | |

| Indium Phosphide (InP) | |

| Silicon and Other Device Materials | |

| By Application | Lighting and Display |

| Optical Communication and Li-Fi | |

| Sensing and Imaging | |

| Power Conversion and Photovoltaics | |

| Other Applications | |

| By End-user Industry | Consumer Electronics |

| Automotive | |

| Information Technology and Telecom | |

| Healthcare and Life-Sciences | |

| Aerospace and Defense | |

| Industrial Automation | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the China optoelectronics market?

The China optoelectronics market size stood at USD 7.63 billion in 2026.

How fast will China’s optoelectronics sector grow through 2031?

Aggregate revenue is projected to rise at a 3.96% CAGR, reaching USD 9.27 billion by 2031.

Which device category is expanding the quickest?

Laser diodes lead growth with a 4.86% CAGR, buoyed by LiDAR and optical-network deployments.

What material shows the strongest demand momentum?

Silicon carbide exhibits the highest 4.45% CAGR thanks to electric-vehicle power electronics and 5G amplifiers.

Which end-use segment offers the largest growth opportunity?

Automotive applications are forecast to advance at a 5.72% CAGR as EV and autonomous-driving adoption scales.

How do export controls affect domestic optoelectronics suppliers?

Restricted access to advanced GaN and SiC equipment raises near-term costs and lengthens fab-ramp timelines.

Page last updated on: