Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

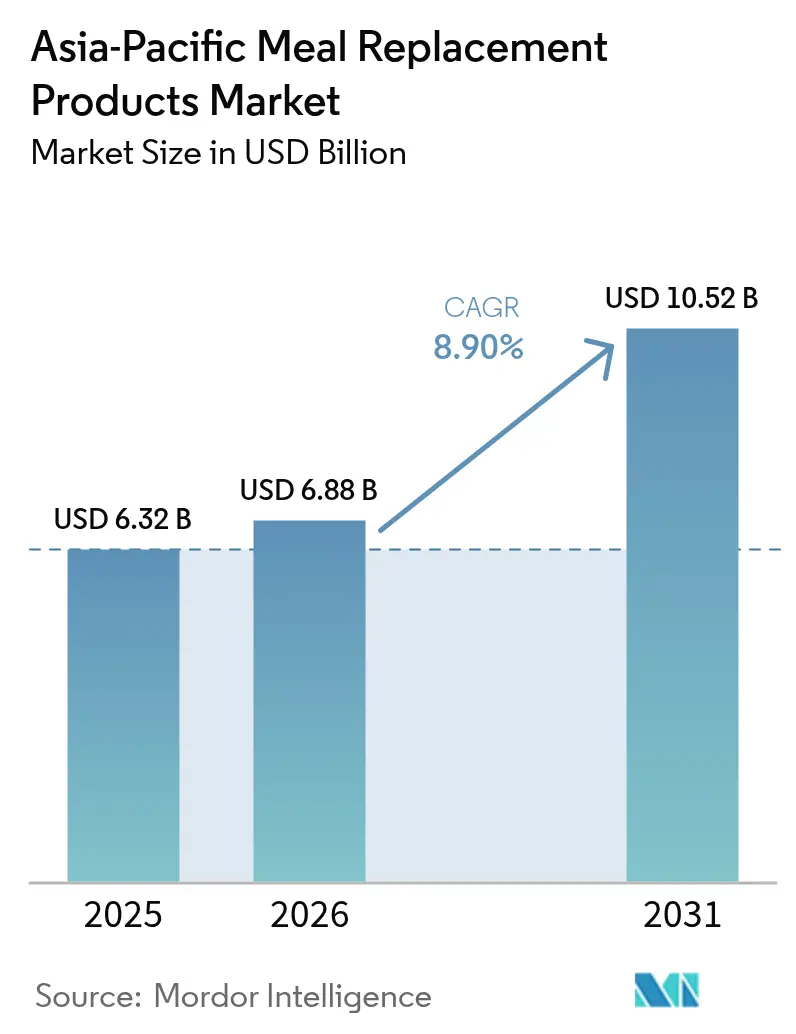

| Base Year Market Size (2025) | USD 6.32 Billion |

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 10.52 Billion |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Meal Replacement Products Market Analysis by Mordor Intelligence

The Asia-Pacific meal replacement products market size was valued at USD 6.32 billion in 2025 and estimated to grow from USD 6.88 billion in 2026 to reach USD 10.52 billion by 2031, at a CAGR of 8.90% during the forecast period (2026-2031). This growth trajectory reflects the region's accelerating health consciousness, urbanization pressures, and evolving dietary preferences that favor convenient nutrition solutions over traditional meal patterns. China's National Fitness Plan targeting 38.5% of the population exercising regularly by 2025 exemplifies the policy-driven wellness momentum propelling demand across major economies[1]Source: State Council of the People’s Republic of China, “National Fitness Program (2021-2025),” gov.cn.

Key Report Takeaways

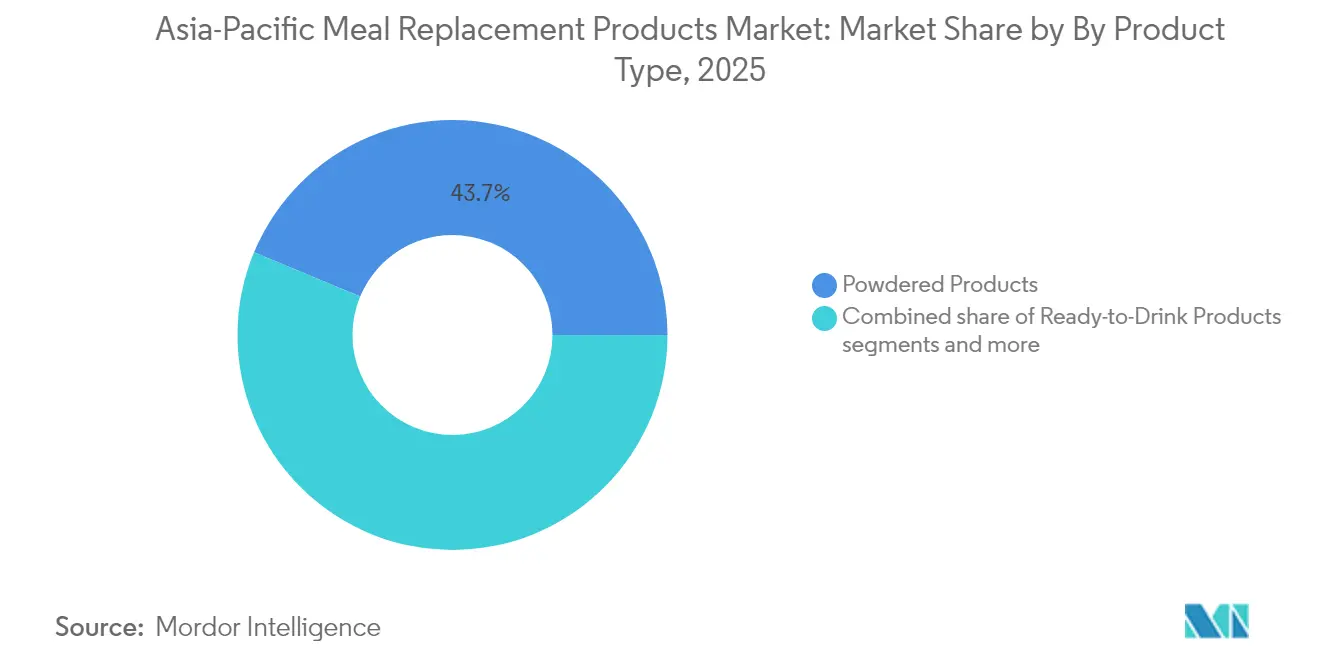

- By product type, powdered formulas held a 43.72% share of the Asia-Pacific meal replacement products market share in 2025, while ready-to-drink (RTD) offerings are projected to post a 10.43% CAGR to 2031.

- By packaging format, bottles/jars captured 44.31% revenue in 2025; pouches are set to expand at a 9.87% CAGR through the forecast period.

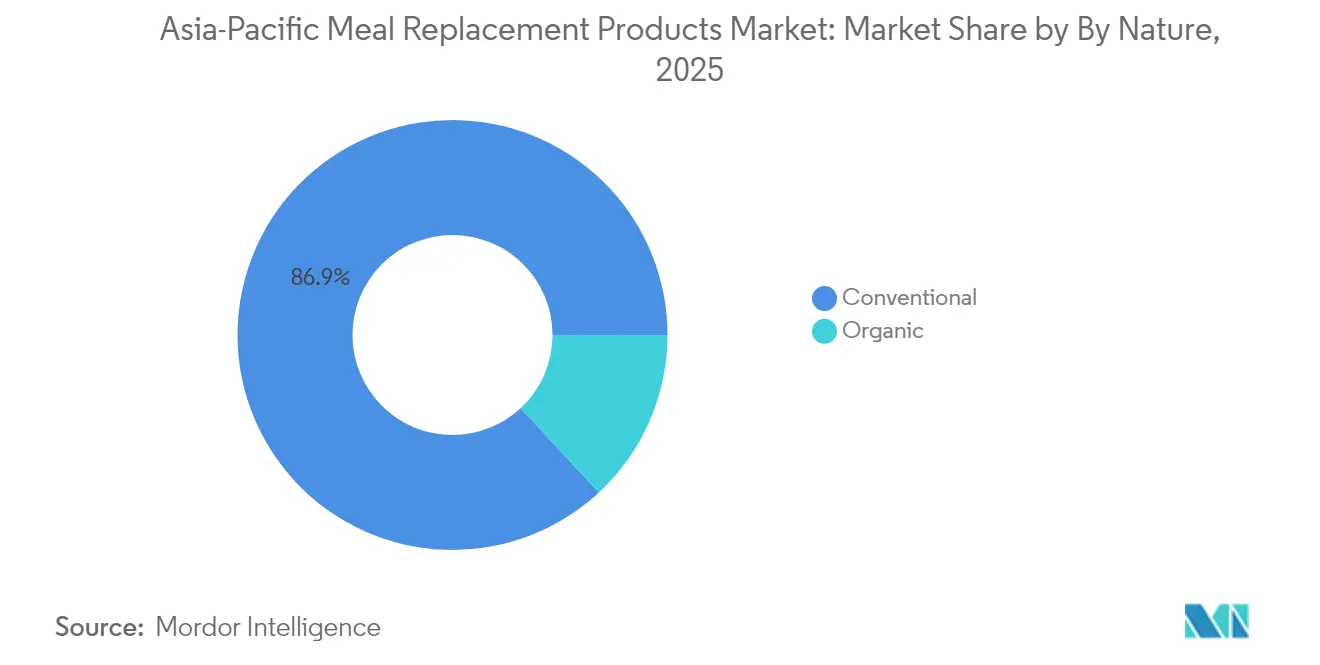

- By nature, conventional formulations controlled 86.92% of the 2025 base, but organic lines are on track for an 10.89% CAGR between 2026 and 2031.

- By distribution channel, supermarkets/hypermarkets contributed 34.78% of 2025 sales; online retail is expected to register the fastest 11.12% CAGR.

- By geography, China dominated with a 37.92% 2025 share, whereas India is forecast to lead in growth at 10.11% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Meal Replacement Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, portion-controlled nutrition | +1.8% | Global, strongest in urban China, Japan, Singapore | Medium term (2-4 years) |

| Growing obesity and fitness focus fuels weight-management usage | +1.5% | China, India, Australia, with spillover to Thailand, Malaysia | Long term (≥ 4 years) |

| Premiumization and innovation in protein-fortified RTD beverages | +1.2% | Japan, South Korea, Singapore, urban China | Short term (≤ 2 years) |

| Corporate wellness schemes and gym chain growth boost adoption | +0.9% | Japan, Australia, Singapore, expanding to China, India | Medium term (2-4 years) |

| Rising consumer demand for functional ingredients | +0.7% | Asia-Pacific core markets, early adoption in premium segments | Medium term (2-4 years) |

| Rising preference for plant-based and protein-rich meal replacements | +0.6% | Australia, Singapore, Japan, emerging in India, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient, Portion-Controlled Nutrition

Urbanization pressures and extended working hours across Asia-Pacific create structural demand for time-efficient nutrition solutions that maintain dietary quality without preparation complexity. There is an increase in meal replacement sales, reflecting the healthcare sector's recognition of controlled nutrition benefits for patient management and staff wellness programs. The trend extends beyond individual consumers to institutional adoption, where corporate cafeterias and healthcare facilities integrate portion-controlled options to address rising diabetes and obesity rates. Regulatory frameworks in Indonesia and Thailand implemented new labeling requirements for sugar, salt, and fat content in 2024, creating transparency that favors nutritionally balanced meal replacements over traditional processed foods.

Growing Obesity and Fitness Focus Fuels Weight-Management Usage

Asia-Pacific's obesity epidemic drives systematic healthcare responses that position meal replacements as clinical intervention tools rather than lifestyle products. Whorld Health Organization (WHO) data indicates obesity rates exceeding 31% in the Southeast Asia region, with government initiatives promoting structured weight management programs that incorporate controlled-calorie nutrition solutions[2]Source: World Health Organization, “Obesity and overweight,” who.int. Additionally, corporate wellness schemes gain momentum as employers recognize productivity benefits from employee health improvements, with Australian and Japanese companies leading the adoption of workplace nutrition programs that include meal replacement subsidies. The fitness industry's expansion creates complementary demand channels, where gym chains partner with nutrition brands to offer post-workout recovery solutions and weight management support programs.

Premiumization and Innovation in Protein-Fortified RTD Beverages

Premium positioning strategies succeed across developed Asia-Pacific markets as consumers demonstrate willingness to pay higher prices for enhanced nutritional profiles and functional benefits. Abbott's January 2025 launch of Protality Nutrition Shake exemplifies this trend, featuring 30 grams of high-quality protein, 25 vitamins and minerals, and positioned at USD 13.69 for a four-pack, targeting adults seeking weight loss while preserving muscle mass. Japanese consumers prioritize protein content in balanced nutrition foods, with consumers specifically seeking protein-focused formulations, supporting premium RTD product development that emphasizes bioavailability and amino acid profiles. Technology integration enables personalized nutrition approaches, where brands leverage mobile applications and diagnostic tools to justify premium pricing through customized formulations.

Corporate Wellness Schemes and Gym Chain Growth Boost Adoption

Institutional demand channels create stable revenue streams that reduce market volatility and enable long-term planning for meal replacement manufacturers. Corporate wellness program adoption accelerates across Asia-Pacific as employers recognize healthcare cost reduction benefits and productivity improvements from employee nutrition support. Gym chain proliferation creates dedicated distribution channels where meal replacement products integrate with fitness services, offering post-workout nutrition and weight management programs that drive consistent consumption patterns. Japanese companies increasingly include health investment support, with younger demographics willing to invest in health-focused products, creating favorable conditions for corporate procurement programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of meal replacement products compared to traditional meals | -1.4% | Price-sensitive markets: India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Regulatory hurdles and varying standards across countries | -0.8% | Cross-border operations, particularly China, India, Indonesia | Medium term (2-4 years) |

| Challenges in taste and flavor acceptance | -0.6% | Traditional food culture markets: China, Japan, Thailand, Indonesia | Medium term (2-4 years) |

| Competition from traditional healthy snacks and fresh food options | -0.5% | Markets with strong street food culture: Thailand, Singapore, Malaysia, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Meal Replacement Products Compared to Traditional Meals

Price sensitivity across emerging Asia-Pacific markets creates adoption barriers that limit mass-market penetration despite growing health awareness and urbanization trends. Consumers in Asia-Pacific increasingly hunt for cheaper alternatives and promotions, with value-seeking behavior intensifying across price-sensitive markets, including India, Indonesia, Philippines, and Vietnam. Traditional meal options remain significantly more affordable, with local street food and home-cooked meals costing fractions of branded meal replacement products, particularly in markets where labor costs keep food service prices low. Currency fluctuations and import dependencies exacerbate cost challenges, as many premium ingredients and specialized processing equipment require foreign exchange, making local pricing vulnerable to macroeconomic volatility.

Regulatory Hurdles and Varying Standards Across Countries

Fragmented regulatory frameworks across Asia-Pacific create compliance complexity that increases market entry costs and delays product launches, particularly affecting smaller manufacturers lacking regulatory expertise. China's SAMR guidance on Foods for Special Medical Purposes registration processes, updated in January 2025, exemplifies evolving standards that require continuous compliance monitoring and documentation. Indonesia implemented new labeling regulations for sugar, salt, and fat content in October 2024, followed by health supplement labeling requirements in June 2024, creating additional compliance layers for meal replacement products. ASEAN harmonization efforts progress slowly, with individual countries maintaining distinct approval processes, ingredient restrictions, and health claim requirements that necessitate market-specific formulations and documentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTD Innovation Drives Category Evolution

Powdered products held the largest segment share at 43.72% in 2025, while ready-to-drink products are anticipated to grow at a CAGR of 10.43% through 2031, reflecting a shift in consumer preferences toward immediate consumption and convenience. Abbott's strategic product launches exemplify this trend, with Protality Nutrition Shake targeting weight management through ready-to-consume formats and Ensure Gold Plant-Based addressing lactose intolerance concerns in the Philippines market. The nutritional bars segment benefits from portability advantages and snack-replacement positioning, while the soups category gains traction in markets with established liquid meal traditions, particularly in China and Japan, where hot consumption preferences align with cultural dietary patterns.

Powdered products retain dominance through cost advantages and extended shelf life benefits that appeal to price-conscious consumers and institutional buyers seeking bulk procurement options. The format enables customization through mixing ratios and flavor additions, supporting personalized nutrition approaches that resonate with health-conscious demographics. Other product types explore niche applications in sports nutrition and medical nutrition segments, where specialized delivery mechanisms address specific consumer needs beyond general meal replacement.

By Packaging Format: Sustainability Meets Convenience

Traditional bottles and jars hold a dominant market share of 44.31% in 2025, while the pouches segment is projected to grow at a CAGR of 9.87%, driven by manufacturers' focus on sustainability and portability benefits. Flexible packaging innovations reduce material usage and transportation costs while enabling portion control and freshness preservation that appeals to single-serving consumption patterns. Tetra packs and cartons maintain steady growth through established supply chains and consumer familiarity, particularly in markets where ambient storage capabilities matter for distribution efficiency.

Environmental consciousness drives packaging evolution, with companies achieving B Corp certification and emphasizing sustainable packaging transitions as a core business strategy. Consumer willingness to pay premiums for sustainable packaging creates opportunities for innovative formats that combine environmental benefits with functional advantages. Regulatory frameworks increasingly emphasize packaging waste reduction, with Singapore's Zero Waste Master Plan and 30-by-30 food security goal creating policy support for circular economy approaches in food packaging.

By Nature: Organic Premium Positioning Gains Momentum

Conventional products held an 86.92% market share in 2025, while the organic segment is expected to grow at a CAGR of 10.89%. This growth reflects the success of premium positioning strategies targeting health-conscious consumers who are willing to pay higher prices for perceived quality benefits. Certification requirements create entry barriers that limit competitive intensity while establishing consumer trust through third-party validation of ingredient sourcing and processing methods. Supply chain complexity for organic ingredients necessitates long-term supplier relationships and inventory management that favor established players with procurement capabilities.

Conventional products benefit from cost advantages and wider ingredient availability that enable mass-market positioning and institutional sales channels. The segment's stability provides a cash flow foundation for manufacturers to invest in organic product development and market education initiatives. Cross-contamination prevention requirements in organic production create operational challenges that smaller manufacturers struggle to address, consolidating market share among larger players with dedicated facility capabilities.

By Distribution Channel: Digital Transformation Accelerates

Traditional supermarkets/hypermarkets held a 34.78% market share in 2025. Online retail channels are expected to grow at a CAGR of 11.12%, driven by the growth of e-commerce platforms that facilitate direct-to-consumer relationships and subscription models. Southeast Asian e-commerce growth, led by Indonesia and Vietnam, showing the highest intent to increase online usage, creates favorable conditions for meal replacement brands seeking market entry through digital channels. Social commerce integration through TikTok Shop and livestreaming formats drives discovery and conversion, particularly for health-related products where influencer tutorial content resonates with younger demographics.

Convenience stores and specialty stores maintain relevance through immediate availability and product trial opportunities that complement online purchasing behavior. The channel mix evolution requires omnichannel strategies that balance digital efficiency with physical touchpoints for consumer education and brand building. Moreover, localized e-commerce strategies combined with marketplace presence and retail partnerships can drive rapid market penetration .

Geography Analysis

China commands 37.92% market share in 2025 through established consumer awareness, extensive distribution infrastructure, and regulatory frameworks that support meal replacement product development. The market benefits from urbanization trends, rising disposable incomes, and government health initiatives that promote structured nutrition approaches for obesity prevention and fitness enhancement.

India emerges as the fastest-growing geography at 10.11% CAGR through 2031, driven by an expanding middle class, increasing health consciousness, and corporate wellness program adoption across major cities. The market's growth potential attracts international players seeking to establish a presence before competitive intensity increases. Japan maintains mature market characteristics with sophisticated consumer preferences for functional ingredients and premium positioning, while Australia benefits from an established sports nutrition culture and regulatory clarity that supports product innovation. Indonesia, South Korea, Thailand, and Singapore represent emerging opportunities with distinct consumer preferences and regulatory environments that require localized approaches. The Rest of Asia-Pacific segment includes smaller markets with growth potential as distribution networks expand and consumer awareness increases through regional brand expansion strategies.

Competitive Landscape

The Asia-Pacific meal replacement products market shows moderate fragmentation. This market structure creates a competitive environment where established multinational corporations compete with regional brands for market share. Local companies focus on specific consumer segments by offering products tailored to regional tastes and preferences. The market's competitive dynamics are characterized by localized product development, distribution strategies, and marketing approaches to effectively serve diverse consumer needs across different Asia-Pacific regions.

White-space opportunities emerge in sustainable protein sources and functional ingredient integration, where companies like Ajinomoto leverage microbial protein technology through Solein partnerships to create premium positioning in Singapore's novel food approval framework. Manufacturing capacity expansion signals long-term commitment, with Sirio Pharma investing USD 40 million in Thailand's first Asian facility outside China, targeting Southeast Asian nutraceutical market growth through localized production capabilities.

Emerging companies are focusing on sustainability practices, such as eco-friendly packaging and reduced carbon emissions in their production processes. They are also establishing direct-to-consumer sales channels through e-commerce platforms and dedicated online stores. Meanwhile, established companies are strengthening their market positions by acquiring smaller competitors, expanding their product portfolios, and increasing their distribution networks.

Asia-Pacific Meal Replacement Products Industry Leaders

Glanbia PLC

Nestlé SA

Amway Corp.

Abbott Laboratories

Herbalife Nutrition

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qingdao-based infant formula company Synutra entered the weight management market with the introduction of its meal replacement series, branded as Xianfeng.

- May 2025: Zantus Lifesciences LLP, an Indian nutraceutical start-up, launched low-carb meal replacement powders for pre-diabetic consumers. The company's meal replacement powder, Reducarb, aims to reduce daily carbohydrate intake from 70% to 55%.

- May 2025: Indian nutraceutical start-up Zantus Lifesciences LLP introduced low-carbohydrate meal replacement powders targeted at pre-diabetics. The product, Reducarb, is formulated as a low-carb meal replacement powder. It features whey protein isolate and soy protein as its primary ingredients and is available in two variants tailored to the distinct nutritional requirements of men and women.

Asia-Pacific Meal Replacement Products Market Report Scope

Meal replacement products are formulated to provide the nutrition of a full meal. Most meal replacement supplements contain 200-400 calories, have high fiber content, are low in carbohydrates, and are enriched with the goodness of vitamins and minerals.

The Asia-Pacific meal replacement products market is segmented by product type, distribution channel, and geography. By product type, the market studied is segmented into ready-to-drink products, nutritional bars, powdered supplements, and other product types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, specialty stores, and other distribution channels. The report analyzes the market for meal replacement products in established and emerging countries of Asia-Pacific, including China, Japan, India, Australia, and the Rest of Asia-Pacific.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Powdered Products |

| Ready-to-Drink Products |

| Nutritional Bars |

| Soups |

| Other Product Types |

By Packaging Format

| Bottles/Jars |

| Pouches |

| Tetra Packs and Cartons |

| Others |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Channels |

By Country

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Powdered Products |

| Ready-to-Drink Products | |

| Nutritional Bars | |

| Soups | |

| Other Product Types | |

| By Packaging Format | Bottles/Jars |

| Pouches | |

| Tetra Packs and Cartons | |

| Others | |

| By Nature | Conventional |

| Organic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Channels | |

| By Country | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific meal replacement products market?

It is USD 6.88 billion in 2026 and is forecast to reach USD 10.52 billion by 2031

Which product type is expanding fastest?

Ready-to-drink formats are set to post a 10.43% CAGR through 2031, making them the quickest-growing category.

Which country leads sales?

China held 37.92% of 2025 regional sales, giving it clear leadership.

Why are pouches gaining popularity?

They cut packaging weight, improve portability, and align with regional waste-reduction policies.

Page last updated on: