Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

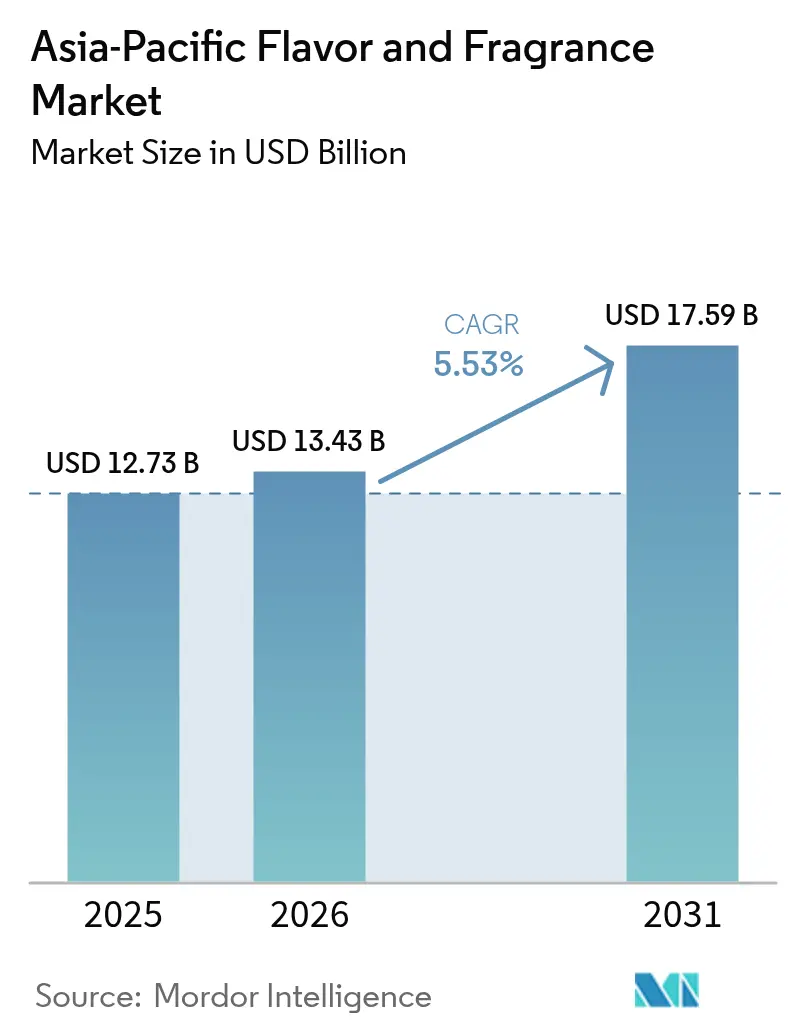

| Base Year Market Size (2025) | USD 12.73 Billion |

| Market Size (2026) | USD 13.43 Billion |

| Market Size (2031) | USD 17.59 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Flavor And Fragrance Market Analysis by Mordor Intelligence

The Asia-Pacific flavors and fragrances market size demonstrated robust performance by reaching USD 12.73 billion in 2025. The Asia-Pacific flavors and fragrances market was valued at USD 12.73 billion in 2025 and estimated to grow from USD 13.43 billion in 2026 to reach USD 17.59 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). The region has established itself as an indispensable hub for both consumption patterns and technological innovation in sensory ingredients, primarily influenced by the substantial increase in consumer purchasing power and their evolving preferences towards high-quality, premium food products with enhanced functional benefits. The biotechnology landscape in the region is undergoing significant transformation in production methodologies, with notable institutions such as the Tokyo University of Science spearheading innovations through the development of sophisticated bioengineered enzymes. These enzymes have revolutionized the industry by enabling the efficient conversion of agricultural waste materials into valuable vanillin through streamlined single-step processes.

Key Report Takeaways

- By product type, flavors led with 57.35% of Asia-Pacific flavors and fragrances market share in 2025 and are projected to grow at a 6.74% CAGR through 2031.

- By source, synthetic inputs accounted for 69.45% share of the Asia-Pacific flavors and fragrances market size in 2025, while natural sources are forecast to advance at a 6.62% CAGR between 2026-2031.

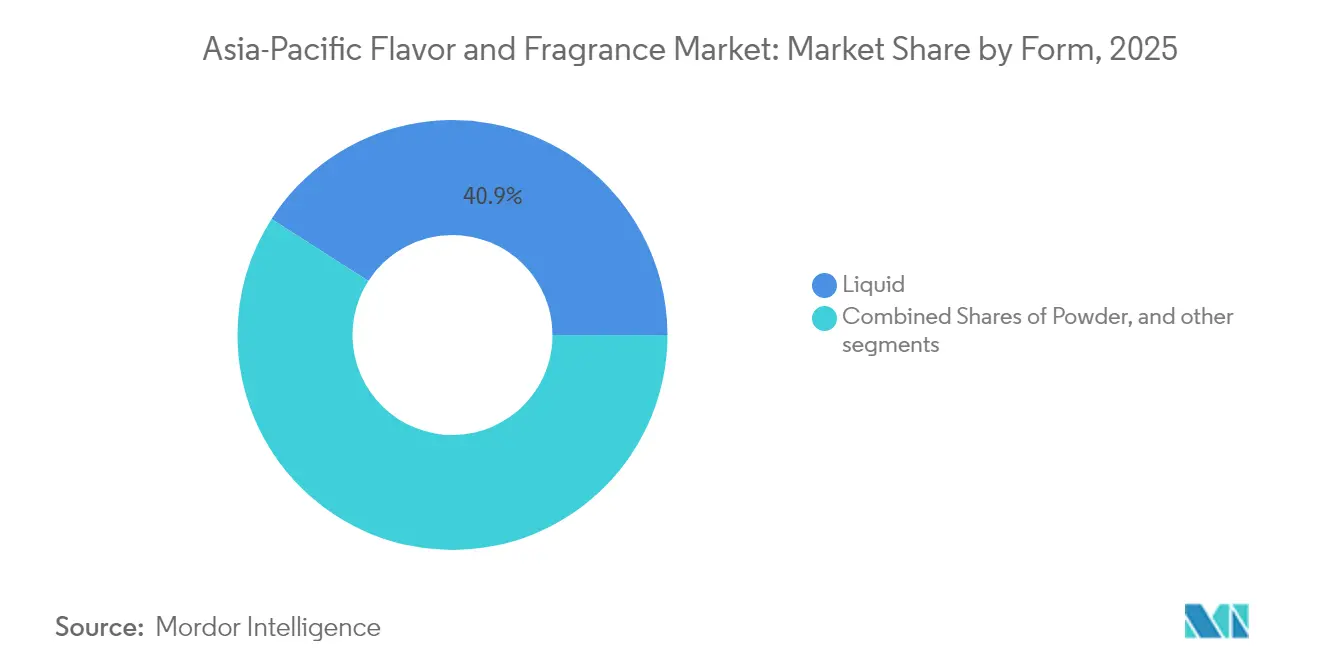

- By form, liquid formats captured 40.92% share of the Asia-Pacific flavors and fragrances market size in 2025 and powders are poised for a 6.35% CAGR to 2031.

- By application, beverages commanded 35.88% share of the Asia-Pacific flavors and fragrances market size in 2025 and will expand at a 6.49% CAGR through 2031.

- By geography, China dominated with 42.10% share of the Asia-Pacific flavors and fragrances market size in 2025 and is expected to register a 6.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Flavor And Fragrance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of processed and convenience foods industry | +1.2% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Growing preference for functional flavors with health benefits | +0.9% | Japan, South Korea, Australia with spillover to emerging markets | Long term (≥ 4 years) |

| Innovations in flavor and fragrance formulations using biotechnology | +0.8% | Japan, China, Singapore innovation hubs | Long term (≥ 4 years) |

| Rising interest in traditional and regional flavors | +0.7% | APAC regional, strongest in Southeast Asia | Medium term (2-4 years) |

| Demand for sustainable and eco-friendly flavors and fragrances | +0.6% | Global with leadership in Japan, Australia, South Korea | Long term (≥ 4 years) |

| Development of multi-sensory flavors and fragrances combining taste and aroma | +0.6% | Urban centers across major APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Processed and Convenience Foods Industry

The demand for packaged meals with extended shelf life that replicate home-cooked flavors continues to grow among urban households, driven by their need for convenience and time-saving solutions. Southeast Asian consumers demonstrate strong daily consumption patterns for cookies, with a significant portion expressing willingness to pay premium prices for innovative flavor experiences. The expansion of digital grocery platforms and on-demand delivery services enhances product accessibility across markets, while the increasing participation of women in the workforce generates consistent market demand. Major food companies in China, Indonesia, and India are establishing strategic partnerships with specialized flavor houses to accelerate product reformulation processes that cater to local taste preferences. This substantial increase in order volume allows contract manufacturers to optimize their investments in spray-drying and liquid blending equipment, fostering economies of scale that promote broader flavor application across processed food categories.

Growing Preference for Functional Flavors with Health Benefits

Growing consumer awareness of the relationship between diet and wellness has driven significant demand for beverages containing botanicals, amino acids, and probiotic cultures that provide immunity and energy benefits. The global functional beverage market continues to experience substantial growth, with the Asia-Pacific region emerging as the primary growth driver. Japan's Foods with Health Claims regulatory framework serves as a comprehensive model for transparent efficacy labeling, influencing regulations across the region and establishing a standardized approval process. Manufacturers are incorporating umami compounds to improve satiety and mouthfeel while reducing sodium content, supporting weight management and low-sugar product lines. The premium positioning of these beverages enables higher pricing to offset the increased costs of bioactive ingredient extraction and stabilization, fostering a continuous cycle of margin growth and research investment.

Innovations in Flavor and Fragrance Formulations Using Biotechnology

Biotechnology applications in flavor production continue to advance through innovative enzyme engineering methods, creating sustainable production pathways that effectively address both cost challenges and environmental concerns in the industry. The Tokyo University of Science's breakthrough in developing bioengineered enzymes has established a new method for vanillin production from agricultural waste materials, marking a significant shift toward circular economy principles in flavor manufacturing processes[1]Source: Phys.org, “Bioengineered enzyme creates natural vanillin,” phys.org. Newcastle University's development of biocatalyst technology for solvent-free flavor ester production showcases strong potential for industrial implementation, delivering enhanced catalytic performance and repeated usability in production environments. These technological advancements align with current regulatory frameworks that favor natural ingredients while reducing industry reliance on fluctuating agricultural commodity markets, providing substantial advantages to businesses that implement biotechnology-enabled flavor production systems.

Rising Interest in Traditional and Regional Flavors

Regional flavor preferences continue to shape consumer behavior as people increasingly seek authentic taste experiences that connect them to cultural heritage and local ingredient traditions. Research examining East Asian culinary traditions reveals that fundamental elements such as rice, soy products, and umami-rich fermented foods form the backbone of these cuisines, transcending national boundaries while preserving distinct local characteristics. This evolution presents significant opportunities for flavor companies to develop comprehensive region-specific portfolios that authentically capture traditional taste profiles in modern applications, especially as food manufacturers work to distinguish their products in competitive markets. The ongoing shift toward traditional flavors harmonizes with clean-label preferences, as consumers increasingly make strong associations between regional ingredients and authenticity, which in turn drives substantial demand for locally-sourced flavor compounds and traditional processing methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory frameworks and approval processes | -0.8% | China, Japan, South Korea with regional spillover | Short term (≤ 2 years) |

| Limited shelf life and storage challenges for natural flavor and fragrance products | -0.6% | Tropical APAC regions, supply chain dependent markets | Medium term (2-4 years) |

| Variability in quality and potency of natural raw ingredients | -0.5% | Indonesia, India, Thailand agricultural regions | Medium term (2-4 years) |

| Fluctuations in global commodity prices impacting ingredient costs | -0.7% | Global with acute impact on import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Frameworks and Approval Processes

The diverse and intricate regulatory framework across Asia-Pacific jurisdictions poses substantial compliance challenges for businesses aiming to enter these markets or innovate their products. China's implementation of GB 2760-2024, taking effect in February 2025, introduces more stringent regulations on food additive definitions and usage limitations, compelling manufacturers to undertake comprehensive product reformulations [2]Source: U.S. Department of Agriculture, “China: Usage Standard for Food Additives Finalized,” fas.usda.gov. Similarly, Japan's regulatory decision to prohibit the use of 3,6-dimethyl-5,6,7,7a-tetrahydro-2(4H)-benzofuranone from January 2025 illustrates the dynamic nature of safety assessment protocols, requiring businesses to maintain vigilant monitoring systems [3]Source: The Japan Food Chemical Research Foundation, “Deletion of 3,6-dimethyl-5,6,7,7a-tetrahydro-2(4H)-benzofuranone from the List of Essence of 18 kinds,” ffcr.or.jp . The fragmented nature of regulations across these markets necessitates companies to develop and maintain distinct product development approaches for each jurisdiction. This regulatory complexity significantly increases development costs and extends time-to-market periods, creating particular challenges for smaller enterprises that often lack specialized regulatory expertise and financial resources.

Limited Shelf Life and Storage Challenges for Natural Flavor and Fragrance Products

Natural flavor compounds encounter significant stability limitations that affect supply chain operations and inventory management across Asia-Pacific's diverse climate conditions. Research demonstrates that natural flavorings experience substantial degradation in their intensity during storage periods, while synthetic alternatives maintain higher stability under identical conditions. The tropical environments prevalent in Southeast Asia accelerate this degradation process, necessitating specialized packaging solutions and robust cold chain infrastructure that increase distribution costs. Consumer preferences for natural ingredients create a fundamental challenge between market demand and technical feasibility, limiting product development opportunities and market penetration potential of natural flavor solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavors Drive Market Leadership

Flavors dominate the market with a substantial 57.35% share in 2025, demonstrating their fundamental role in shaping food and beverage applications. The segment's robust growth trajectory, marked by a CAGR of 6.74% through 2031, underscores the increasing demand for innovative flavor solutions across diverse consumer segments. The industry's evolution has led to a significant shift toward multi-sensory experiences, where taste and aroma elements merge to create unique product offerings that bridge traditional category boundaries.

This transformation is exemplified by strategic initiatives such as Givaudan's establishment of L'Appartement 125, a Fine Fragrance Creative Centre in Shanghai, in October 2024. The facility serves as a collaborative hub for partnerships with local brands, enabling the integration of cultural nuances into fragrance development. Through these strategic investments, flavor and fragrance companies are well-positioned to capitalize on opportunities across multiple segments while addressing the sophisticated consumer preferences for products that deliver comprehensive sensory experiences.

By Source: Synthetic Dominance Faces Natural Challenge

Synthetic sources dominate the market with a 69.45% share in 2025, primarily due to their significant cost advantages and highly reliable supply chains. These characteristics make synthetic sources particularly attractive for large-scale food and beverage manufacturers who require consistent, high-volume ingredient supplies for their production processes.

Natural sources are experiencing rapid growth at a 6.62% CAGR through 2031, as consumers increasingly seek clean-label products and regulatory bodies implement supportive frameworks for natural ingredients. This market evolution demonstrates a clear shift toward premium positioning, where natural ingredients command higher prices despite their increased production costs and supply chain complexities. Nature-identical compounds serve as an intermediate solution in this landscape, offering manufacturers a practical way to balance evolving consumer preferences with operational efficiency requirements.

By Form: Liquid Leadership Challenged by Powder Innovation

Liquid forms maintain a dominant position with a 40.92% market share in 2025, primarily because manufacturers find them highly adaptable for beverage applications. These forms integrate seamlessly into existing manufacturing processes, making them a preferred choice for production facilities. The liquid segment's strong market position is further reinforced by well-established infrastructure and deep formulation expertise, which creates substantial barriers for new market entrants.

Powder forms demonstrate remarkable growth potential, recording a 6.35% CAGR through 2031. This growth is fueled by their extensive applications in convenience foods and their ability to remain stable for longer periods, particularly beneficial in tropical climate regions where storage conditions can be challenging. The market also encompasses other innovative forms, including encapsulated products and specialized delivery systems, where companies invest in developing proprietary technologies to distinguish themselves from competitors and capture specific market segments.

By Application: Beverage Supremacy Reflects Health Trends

The beverage applications segment commands a substantial 35.88% market share in 2025 and is expected to maintain robust growth at a 6.49% CAGR through 2031. This segment's market leadership underscores its role as a primary innovation center for functional and premium products in the industry. The strong market position is fundamentally supported by consumer behavior, particularly in Southeast Asia, where customers consistently demonstrate a willingness to invest in products offering unique and distinctive flavor experiences.

Traditional application segments, including dairy, bakery, and confectionery, continue to hold significant market positions through their high-volume consumption patterns. The savory snacks category has found success through innovative flavor development, particularly in bold and spicy profiles that resonate with changing consumer preferences. In the specialized meat applications segment, manufacturers focus on achieving authentic taste replication while incorporating advanced preservation technologies. The expanding functional beverage market is driving innovation toward health-beneficial flavor compounds, with umami-rich formulations experiencing increased adoption among consumers who seek satisfying taste alternatives to animal-based ingredients.

Geography Analysis

China dominates the Asia-Pacific flavors and fragrances market with a substantial 42.10% market share in 2025. This market leadership position is built on the country's robust manufacturing infrastructure and expanding consumer base. The market's strength is underpinned by continued urbanization trends, steady increases in disposable incomes, and evolving consumer preferences that increasingly favor premium and functional products.

China is also exhibiting the most rapid growth in the region, with a projected CAGR of 6.58% through 2031. This growth trajectory is supported by the expanding middle class, increased consumer spending power, and the ongoing transformation of consumer preferences. The market's expansion is further reinforced by the rising demand for processed foods, beverages, and personal care products that require flavor and fragrance components.

Southeast Asian markets, including Indonesia, Thailand, and Singapore, are experiencing notable growth driven by economic development and shifting dietary patterns toward processed and convenience foods. Australia represents a mature market segment characterized by sophisticated regulatory frameworks and established consumer preferences for natural and organic ingredients. Major industry players are responding to these market dynamics, as demonstrated by Givaudan's CHF 50 million investment in an Indonesian facility and IFF's expansion of their Shanghai center in October 2024. These strategic regional investments enable companies to build local capabilities and strengthen customer relationships essential for long-term market success.

Competitive Landscape

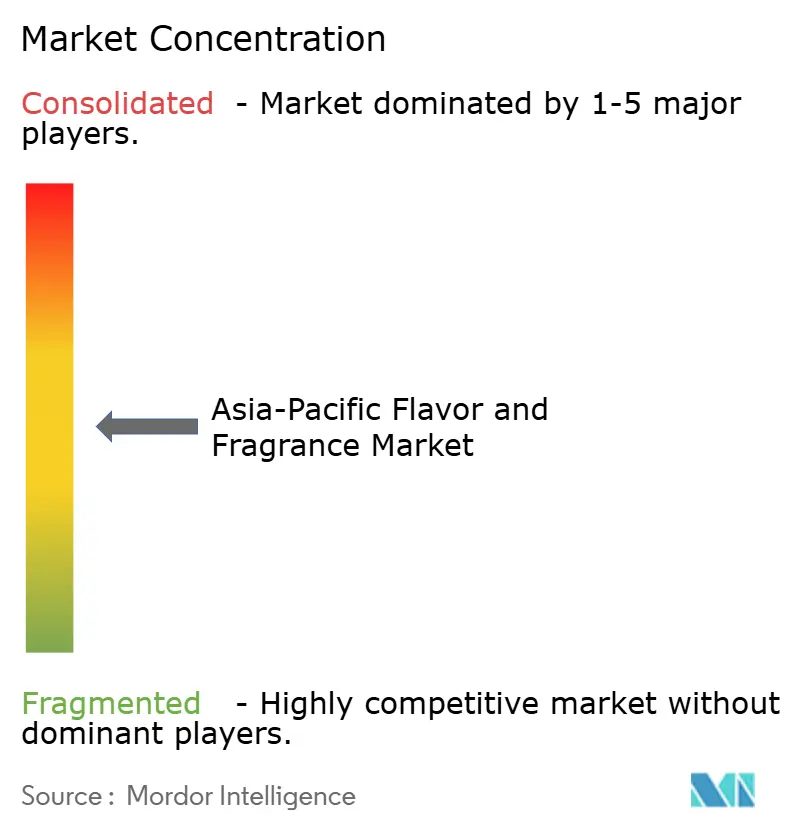

The Asia-Pacific flavors and fragrances market structure enables both established multinational corporations and emerging regional players to thrive, characterized by moderate concentration and significant fragmentation. The market's competitive landscape is dominated by global industry leaders, with Givaudan achieving CHF 7.4 billion in 2024 sales and recording 8.8% growth in Asia-Pacific, while dsm-firmenich generated EUR 12.31 billion in combined revenues. These companies have established their market presence through strategic investments in local innovation centers and production facilities, ensuring deep understanding of regional preferences and compliance with regulatory requirements.

Biotechnology-enabled production methods and sustainable ingredient sourcing represent the fastest-growing segments within the market. This growth is evidenced by increased patent filings for Lamiaceae bioactives, particularly from Korea, China, and the U.S., as manufacturers respond to rising consumer demand for natural preventive health solutions. The development of bioengineered enzymes for flavor compound synthesis has transformed production methods, offering both cost efficiency and environmental benefits.

Other market segments show development through technological advancement and innovation. Companies implementing artificial intelligence in flavor development gain competitive advantages through improved consumer preference prediction and product optimization capabilities. Additionally, businesses investing in multi-sensory product development create unique value propositions that support premium pricing strategies, further diversifying their market offerings and revenue streams.

Asia-Pacific Flavor And Fragrance Industry Leaders

Givaudan

DSM-Firmenich

International Flavors & Fragrances Inc.

Symrise AG

Archer Daniels Midland Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Symrise and Shan Foods have inaugurated a state-of-the-art production facility in Pakistan, enhancing local manufacturing to deliver innovative taste and health food solutions. This partnership supports market growth with faster speed to market, local sourcing, and expansion into Middle Eastern markets.

- July 2024: IFF is expanding its Shanghai facility to support the development of flavour and functional ingredient solutions tailored to the Chinese portfolio. The 16,000 m² site will enhance end-to-end innovation capabilities in taste, biotech, and perfumery, targeting the rapidly growing Asian market demand.

- May 2024: S H Kelkar and Company shifted fragrance production to its Mulund site, converting the flavor facility for fragrance manufacturing to maintain capacity. The entire flavor manufacturing is consolidated at Vashivali, and customer servicing resumed from April 30, 2024, with backlog expected to normalize shortly.

Asia-Pacific Flavor And Fragrance Market Report Scope

The Asia-Pacific flavor and fragrance market is segmented by type into synthetic and natural. By Application, the market is segmented into food, beverage, beauty and personal care, perfumes, and others. By country, the market is segmented into China, India, Japan, Australia, and the Rest of Asia-Pacific.

By Product Type

| Flavors |

| Fragrance |

By Source

| Natural |

| Synthetic |

| Nature Identical |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy |

| Bakery |

| Confectionary |

| Savory Snacks |

| Meat |

| Beverage |

| Others |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Flavors |

| Fragrance | |

| By Source | Natural |

| Synthetic | |

| Nature Identical | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Dairy |

| Bakery | |

| Confectionary | |

| Savory Snacks | |

| Meat | |

| Beverage | |

| Others | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific flavors and fragrances market in 2026?

It is valued at USD 13.43 billion and is projected to hit USD 17.59 billion by 2031 on a 5.53% CAGR path.

Which product type currently dominates demand?

Flavors lead with 57.35% share in 2025 and will remain the fastest-growing segment through 2031.

Why is China so important for suppliers?

China holds 42.10% regional share and posts a 6.58% CAGR, driven by processed-food output and premium beauty consumption.

Which application shows the fastest expansion?

Beverages, supported by functional and premium drink launches, command 35.88% share and a 6.49% CAGR to 2031.

How are regulations affecting market entry?

Stricter additive and labeling rules across China, Japan, and South Korea raise compliance costs and favor firms with strong regulatory teams.

Page last updated on: