Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

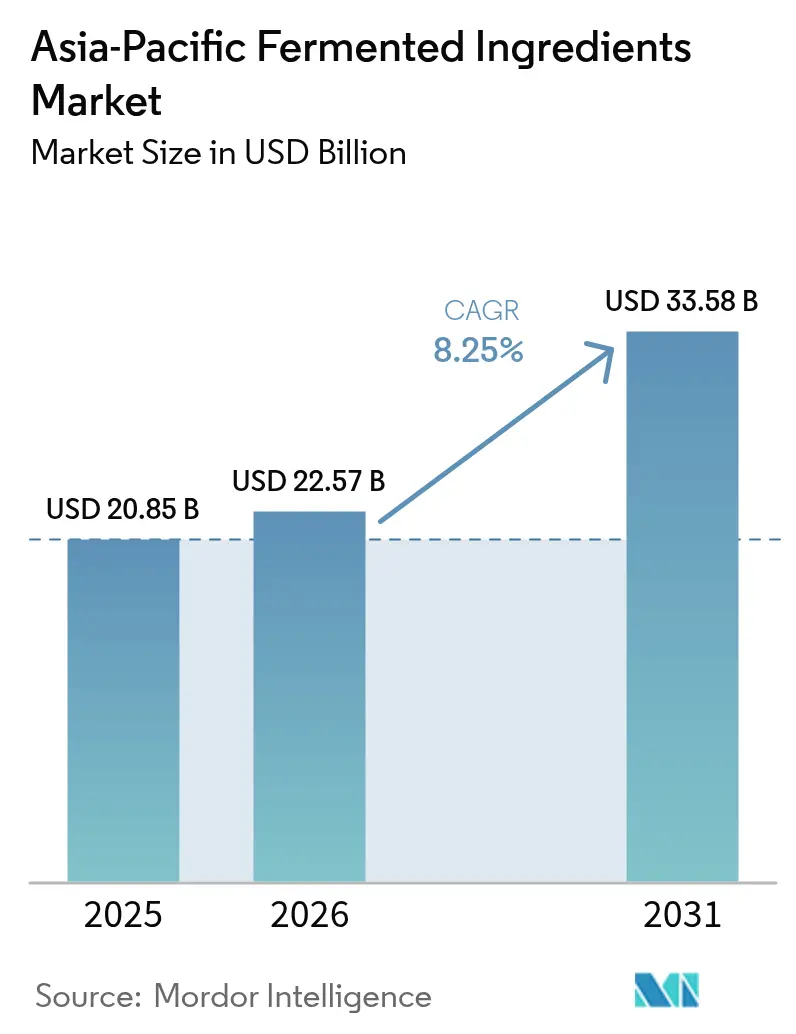

| Base Year Market Size (2025) | USD 20.85 Billion |

| Market Size (2026) | USD 22.57 Billion |

| Market Size (2031) | USD 33.58 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

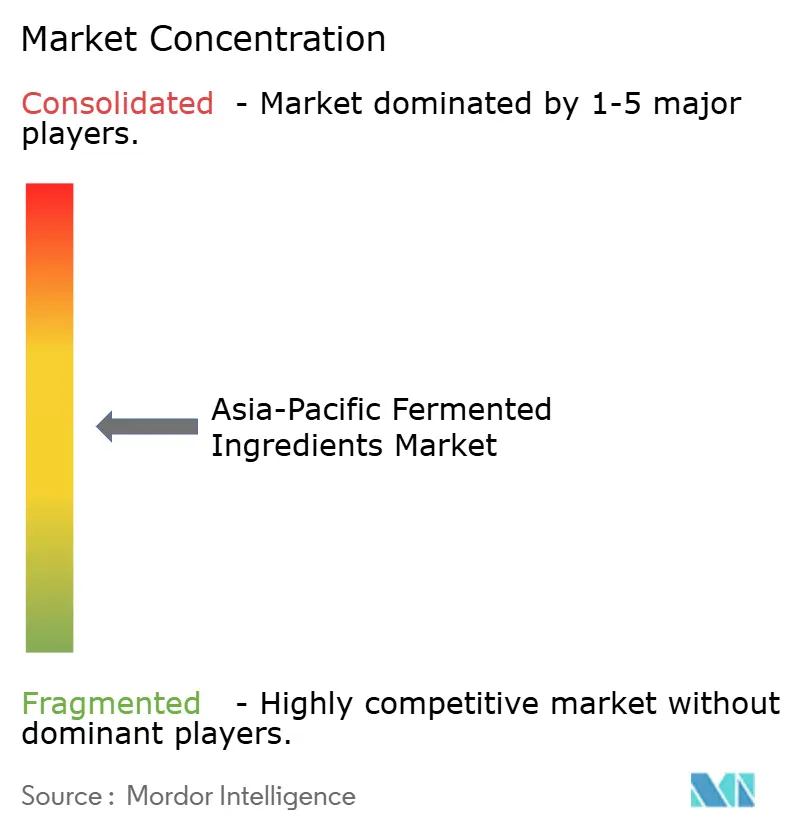

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fermented Ingredients Market Analysis by Mordor Intelligence

The Asia-Pacific fermented ingredients market size is expected to grow from USD 20.85 billion in 2025 to USD 22.57 billion in 2026 and is forecast to reach USD 33.58 billion by 2031 at 8.25% CAGR over 2026-2031. Cost-efficient amino acid production in coastal China, rising probiotic awareness among urban consumers in India and China, and expanding enzyme adoption by beverage makers collectively sustain this momentum. Manufacturers are retrofitting their plants with continuous bioreactors to reduce energy consumption, while governments in China, India, and the ASEAN bloc are actively subsidizing fermentation parks to attract investment. Regional feedstock advantages, such as corn steep liquor in China, sugarcane molasses in India, and cassava bagasse in Thailand, shield producers from commodity-price volatility and support their long-term pricing power. At the same time, premium niches such as post-biotics and fermented plant proteins enable innovators to capture double-digit margins, thereby balancing the sector’s reliance on volume-driven amino acids.

Key Report Takeaways

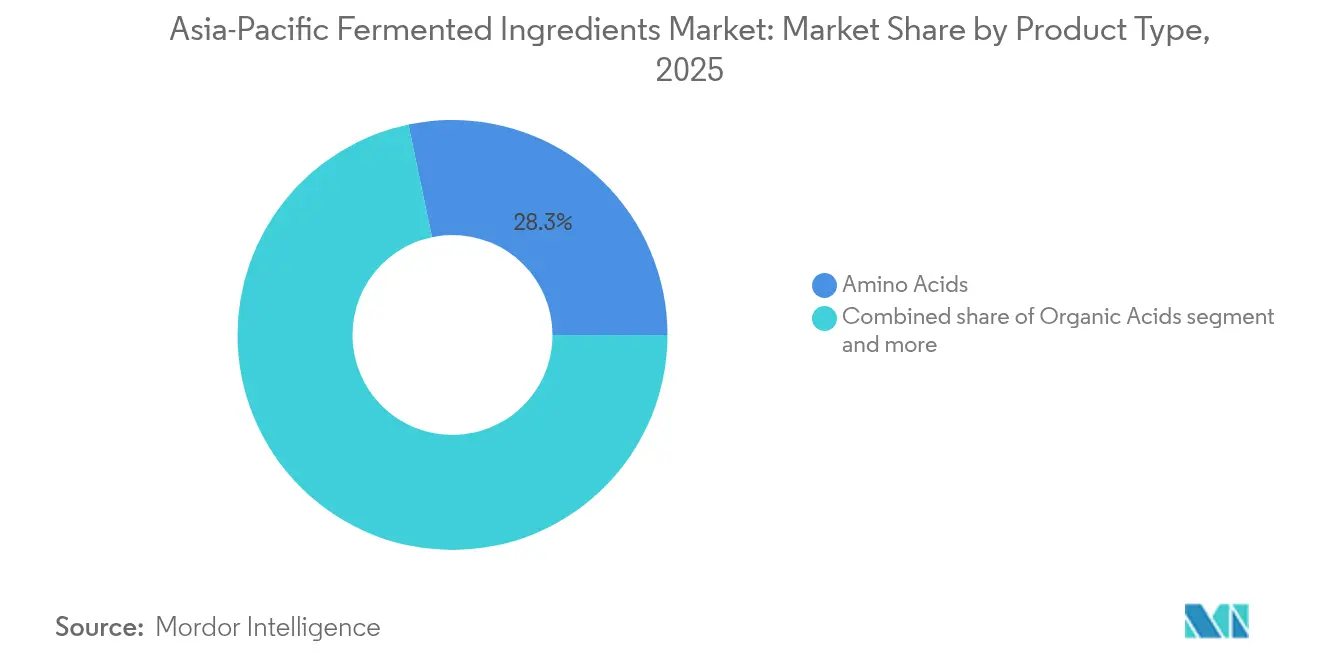

- By product type, amino acids led with a 28.29% share of the Asia-Pacific fermented ingredients market in 2025, whereas probiotics and post-biotics are expanding at a 9.05% CAGR through 2031.

- By form, dry ingredients captured 58.21% of the Asia-Pacific fermented ingredients market share in 2025; liquid formats are expected to record the fastest CAGR of 8.62% to 2031.

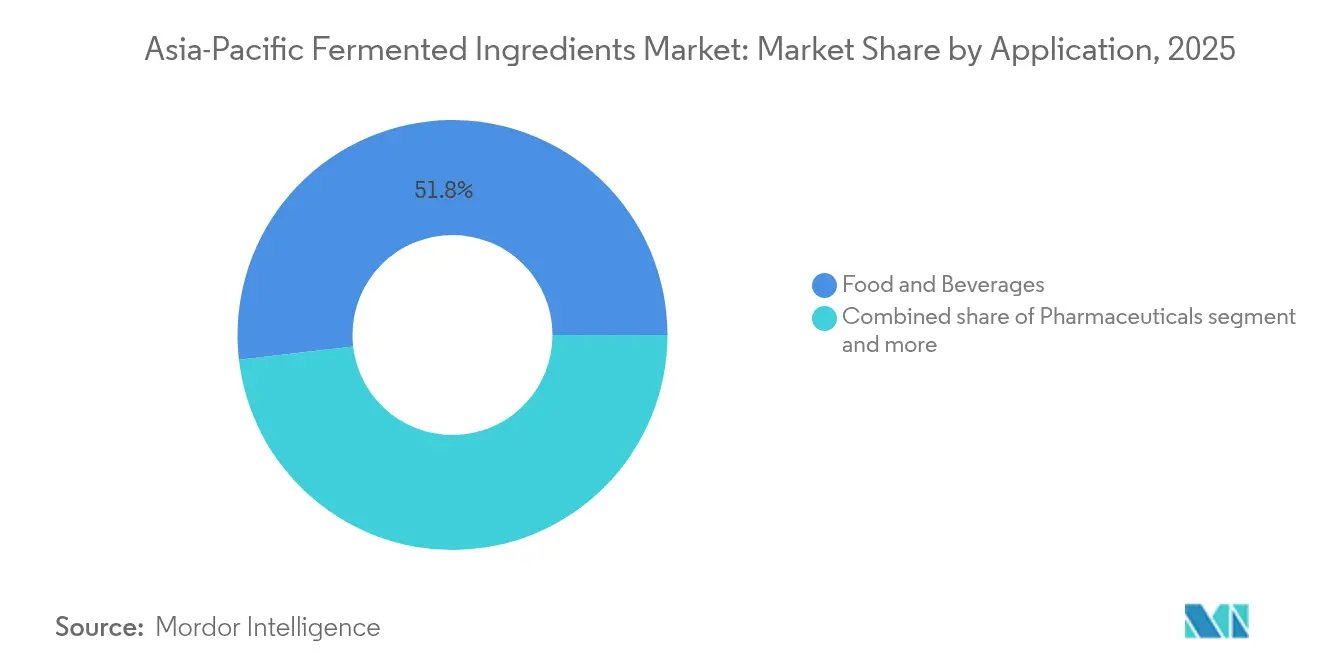

- By application, food and beverages accounted for 51.84% of the Asia-Pacific fermented ingredients market size in 2025, while pharmaceuticals grew at a 10.05% CAGR over the forecast horizon.

- By geography, China held 48.12% of the Asia-Pacific fermented ingredients market in 2025; India is the fastest-growing country at a 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Fermented Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in fermentation technology and ingredient innovation | +1.8% | Japan, South Korea, China biotech hubs | Medium term (2-4 years) |

| China and India gut-health boom fuels probiotics demand | +1.5% | Tier-1 and tier-2 Chinese cities, urban India | Short term (≤ 2 years) |

| Regenerative-ag feedstocks unlock low-cost carbon inputs | +0.9% | China rice provinces, Indian sugarcane belt, Thai cassava areas | Long term (≥ 4 years) |

| Growing demand for clean-label, natural, less-processed ingredients | +1.3% | Japan, Australia, South Korea, China | Medium term (2-4 years) |

| ASEAN halal-certified facilities drive export-grade amino acids | +0.7% | Malaysia, Indonesia | Medium term (2-4 years) |

| Popularity of fermented drinks and functional beverages | +1.1% | China, Japan, South Korea, India, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advances in Fermentation Technology and Ingredient Innovation

Continuous bioreactors, AI-driven strain selection, and inline sensors are compressing cycle times and pushing yields higher across the fermentation industry. Ajinomoto reports a 12% reduction in L-glutamate fermentation time, boosting asset utilization and lowering unit costs, while Japan’s Ministry of Economy, Trade, and Industry has allocated JPY 15 billion in 2024 to accelerate next-generation bioreactor development[1]Source: Ministry of Economy, Trade and Industry, “Biotechnology Roadmap 2024,” METI.GO.JP. Chinese leaders Fufeng and Meihua are upgrading legacy lines with real-time pH and dissolved-oxygen control systems, cutting energy consumption per ton by up to 18%. These technology advances not only shrink greenhouse-gas footprints but also free capacity for higher-value specialty ingredients. Downstream, emerging metabolic pathways now enable commercial production of rare vitamins, aroma molecules, and functional actives, expanding revenue opportunities in pharmaceutical and cosmetic applications.

China and India Gut-Health Boom Fuels Probiotics Demand

Post-pandemic wellness habits continue to drive demand for probiotic supplements, with India’s imports and domestic output projected to reach USD 1.8 billion in 2024, amid booming e-commerce and rising disposable incomes, according to the Press Information Bureau. China’s probiotic ingredient sales jumped 22% in 2024, with tier-1 cities contributing 60% of volumes[2]Source: China National Food Industry Association, “Probiotic Market Analysis 2024,” CNFIA.CN. Regulators are tightening quality controls: China’s National Health Commission introduced strain-specific CFU thresholds in early 2024, while India’s FSSAI followed with draft norms requiring third-party verification. These higher standards concentrate market power among suppliers with clinically validated strains and reliable cold-chain capabilities, lifting average selling prices and intensifying consolidation. Urban, health-conscious consumers remain the core growth engine, driving the segment’s robust 9.33% CAGR and reinforcing the shift of probiotics from a niche supplement to a mainstream preventive health product.

Regenerative-Ag Feedstocks Unlock Low-Cost Carbon Inputs

Rice husk hydrolysate can substitute up to 40% of glucose in amino acid fermentation, reducing raw material costs by approximately 15% without compromising yield, according to a 2024 Journal of Cleaner Production study. Thailand now channels more than 2 million tons of cassava bagasse into fermenters under circular-economy incentives, while sugar mills in Maharashtra secure multi-year molasses contracts that stabilize input costs amid commodity volatility[3]Source: Thai Ministry of Agriculture, “Circular Economy Initiatives,” MOAC.GO.TH. These agricultural residues also shrink Scope 3 emissions. DuPont reported a 25% regional reduction after transitioning to by-product feedstocks. Broadening the feedstock base, therefore, enhances both cost resilience and sustainability credentials across Asia-Pacific’s fermentation industry.

Growing Demand for Clean-Label, Natural, and Less-Processed Ingredients

As of 2024, 68% of Asia-Pacific consumers were willing to pay a premium for naturally fermented products, up from 54% in 2022, according to a Cargill survey. Japan’s revised Food Labeling Act mandated disclosure of production methods, prompting manufacturers to switch to fermentation-derived acids and flavors. Corbion experienced a 30% increase in lactic acid orders from regional beverage brands in 2024, underscoring the impact of label transparency on purchasing decisions. In Australia, retailers pledged to phase out synthetic preservatives by 2026, further expanding the addressable market. This clean-label momentum underpinned steady premiumization across food, beverage, and personal-care categories in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs due to specialized fermentation processes | -0.8% | Japan, Australia, smaller ASEAN markets | Short term (≤ 2 years) |

| Stringent regulatory requirements for food safety and labeling | -0.5% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Short shelf life of certain fermented products requires cold chain logistics | -0.6% | India, Southeast Asia | Short term (≤ 2 years) |

| Risk of microbial contamination and quality-control challenges | -0.4% | APAC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Requirements for Food Safety and Labeling

China’s National Medical Products Administration required multi-year toxicology data for novel fermentation-derived compounds, potentially delaying product launches by up to two years. India’s FSSAI mandated third-party probiotic CFU testing, adding USD 5,000-10,000 to annual SKU costs. Japan has enforced batch-wise certificates of analysis for pharmaceutical-grade amino acids, which has strained smaller exporters, according to the Ministry of Health, Labor and Welfare. This regulatory heterogeneity increased compliance budgets and favored incumbents with dedicated regulatory teams.

Short Shelf Life of Certain Fermented Products Requires Cold Chain Logistics

An International Institute of Refrigeration survey found that up to 40% of probiotic shipments in India exceeded 8 °C during last-mile delivery, reducing product viability and prompting returns[4]Source: International Institute of Refrigeration, “Cold Chain Study Asia-Pacific 2024,” IIFIIR.ORG. Tropical humidity in Indonesia and the Philippines further increased cold-chain costs, adding roughly 15-20% to landed prices. Manufacturers invested in freeze-drying and microencapsulation to extend shelf stability, but these processes added USD 2-4 per kilogram, pushing prices beyond the reach of value-oriented brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amino Acids Anchor Volume, Probiotics Lead Growth

Amino acids accounted for 28.29% of the Asia-Pacific fermented ingredients market in 2025, driven by strong demand for feed-grade lysine and threonine from China’s livestock sector. Food-grade glutamate production in Shandong and Jiangsu remained essential for regional savory formulations. Probiotics and post-biotics are projected to grow at a 9.05% CAGR through 2031, as heat-stable strains allow bakery and snack manufacturers to make gut-health claims without refrigeration. Organic acids, led by citric and lactic acids, continue to support beverage acidulation and meat preservation, while polylactic acid is gaining traction in sustainable packaging. Fermented vitamins, such as B12, enable pharmaceutical companies to meet purity targets with a reduced environmental impact.

Market demand is shifting from commodity bulk products toward specialty, high-margin offerings. Chr. Hansen’s heat-tolerant Bifidobacterium facilitates probiotic bread launches in Japan, while DSM-Firmenich and BASF operate riboflavin fermenters in coastal China to leverage integrated corn-processing hubs. NatureWorks expanded its Thai PLA facility by 25,000 tons in 2024 to meet the sustainability pledges of its brand owners. Enzymes for detergents and starch processing are growing steadily in the mid-teens, as bio-based alternatives replace petrochemical catalysts, while antibiotics, although a mature segment, maintain stable volumes through semi-synthetic upgrades for hospital formularies.

By Form: Dry Dominates Logistics, Liquid Gains in Ready-to-Use Applications

Dry formats accounted for 58.21% of the Asia-Pacific fermented ingredients market in 2025, driven by longer shelf life and lower freight costs. Powdered amino acids and spray-dried probiotics integrate seamlessly into feed and bakery production lines, particularly in India, where cold-chain gaps remain a challenge. Liquid fermentates, however, are projected to grow at an 8.62% CAGR through 2031, as beverage and pharmaceutical processors value the dosing convenience and sterility of ready-to-use enzyme blends. Angel Yeast’s liquid yeast extract for plant-based meat exemplifies this trend, avoiding flavor losses associated with spray-drying.

Regional infrastructure also shapes form preference. Japan’s dense refrigerated logistics support the rapid distribution of liquid enzymes to breweries, while Vietnam’s aquaculture sector adopts Evonik’s semi-liquid amino-acid paste, combining stability with ease of mixing. Regulatory purity standards further influence choices; China’s updated GB codes are easier to meet with crystalline powders than viscous concentrates. Hybrid pastes and granules are emerging as compromise formats, reflecting converging needs for handling efficiency and storage stability.

By Application: Food and Beverages Lead, Pharmaceuticals Surge

Food and beverages accounted for 51.84% of the Asia-Pacific fermented ingredients market in 2025, covering dairy cultures, bakery improvers, beverage acidulants, and meat preservatives. Pharmaceuticals registered the fastest growth, with a 10.05% CAGR, as biosynthetic vitamins, infusion-grade amino acids, and antibiotic intermediates increasingly replaced traditional chemical routes. India’s USD 2 billion Production-Linked Incentive scheme lowered capital expenditure barriers, spurring the construction of new fermentation-based bulk drug plants, according to the Press Information Bureau, Government of India.

Within the food sector, probiotic yogurt and kefir dominated the Chinese dairy aisles, while enzymes enhanced the softness and shelf life of bread across Japanese chains. Citric acid remained prevalent in carbonated soft drinks, while lactic acid gained share in functional beverages marketed for gut health. Feed-grade amino acids benefited from China’s hog herd recovery, boosting lysine tonnage by approximately 8% in 2024, according to the U.S. Foreign Agricultural Service. Personal-care formulators increasingly adopted fermented hyaluronic acid and amino-acid surfactants, leveraging the growth of K-beauty exports. Industrial applications, from bio-polymers to pulp-bleaching enzymes, grew steadily as circular-economy mandates in Japan and South Korea encouraged the use of renewable inputs.

Geography Analysis

China accounted for 48.12% of the Asia-Pacific fermented ingredients market revenue in 2025, driven by the development of integrated fermentation parks in Shandong, Jiangsu, and Hebei. Large-scale corn processing provides low-cost substrates, while the 14th Five-Year Biotechnology Plan allocated CNY 50 billion to synthetic-biology research and development, according to the National Development and Reform Commission. Oversupply in commodity amino acids has compressed margins, encouraging producers to shift toward specialty post-biotics, fermented plant proteins, and precision-fermented aromas. Environmental regulations are tightening, with 2024 wastewater standards prompting smaller plants to merge or exit, while retrofits with continuous bioreactors help offset rising compliance costs.

India, growing at a 9.42% CAGR, is expanding fermentation capacity for pharmaceutical-grade amino acids and probiotic supplements. The Production-Linked Incentive scheme covers up to 20% of capital expenditure, attracting USD 800 million in committed investments by mid-2024, according to the Press Information Bureau. E-commerce platforms are democratizing access to supplements, although cold-chain gaps in tier-2 cities continue to drive demand for shelf-stable dry powders. Sugarcane molasses contracts in Maharashtra stabilize inputs, while state governments in Rajasthan and Maharashtra support commercialization of fermented beverages such as kanji and sol kadhi.

Japan and South Korea supply advanced bioreactors, inline sensors, and engineered enzymes, exporting both technology and high-purity ingredients. Japan’s fermentation equipment exports rose 18% in 2024, according to JETRO. Domestic demand emphasizes clean-label and functional products, with convenience stores stocking probiotic drinks and cosmetics brands adopting fermented hyaluronic acid.

Australia occupies a premium segment, with dairy and beverage companies paying double-digit premiums for non-GMO, traceable inputs. The rest of Asia-Pacific, including Thailand, Vietnam, Malaysia, and Indonesia, leverages cost advantages and halal certifications to target Middle Eastern buyers, with Thailand’s cassava feedstock boosting organic-acid exports and Malaysia and Indonesia earning halal premiums for amino acids despite longer audit cycles.

Competitive Landscape

The Asia-Pacific fermented ingredients market remains moderately concentrated. The top five suppliers, Ajinomoto, Angel Yeast, Fufeng, Cargill, and Kyowa Hakko, command meaningful volume but leave space for regional specialists and biotech startups. Ajinomoto’s 2024 purchase of a Thai cassava mill secures feedstock and lowers upstream risk, while Angel Yeast invests in proprietary strains tailored for plant-based meat. Chinese firms compete fiercely on scale in feed-grade lysine, but specialty categories, such as post-biotics, reward expertise in regulation and formulation support.

Patent trends highlight divergent priorities: Chinese entities filed 52% of regional fermentation patents in 2024, primarily focusing on strain optimization, whereas Japanese and South Korean filers emphasized enzyme engineering, according to the World Intellectual Property Organization (WIPO). Continuous fermentation and AI process control are standard in Japan, yet scarce in emerging ASEAN plants. Sustainability differentiates suppliers to multinationals under net-zero mandates; DuPont increased its use of agricultural residue to 35% of its Asia-Pacific feedstock in 2024. Meanwhile, Perfect Day licenses precision-fermented whey technology to Asian partners, signaling cross-border collaboration in alternative proteins.

Regional consolidation may accelerate as smaller facilities struggle with ISO 22000 compliance and wastewater upgrades. CJ CheilJedang’s 60% stake in a Vietnamese enzyme plant exemplifies opportunistic acquisition aimed at supply-chain synergies. Fufeng’s USD 200 million xanthan-gum project in Inner Mongolia bundles wastewater recycling to meet stricter discharge norms. Innovation centers, such as DuPont’s Singapore hub, channel R&D into fermented dairy analogs and flavor enhancers, illustrating how incumbents seek differentiated growth lanes beyond bulk amino acids.

Asia-Pacific Fermented Ingredients Industry Leaders

Ajinomoto Co., Inc.

Angel Yeast Co., Ltd.

Fufeng Group Ltd.

Cargill, Inc.

Kyowa Hakko Bio Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ajinomoto Co., Inc. announced a USD 150 million expansion of its amino acid fermentation facility in Jiangsu, China, which will add 30,000 tons of annual capacity for feed-grade lysine and threonine. The expansion incorporates continuous fermentation technology and renewable energy integration, targeting a 20% reduction in carbon intensity per ton of product. The facility is expected to commence operations in Q4 2026 and will serve growing demand from China's recovering livestock sector.

- February 2025: Chr. Hansen Holding A/S launched a next-generation probiotic strain, Bifidobacterium lactis HN019 Plus, specifically formulated for the Asia-Pacific market. The strain demonstrates enhanced survivability in tropical climates and maintains viability for 24 months at ambient temperature, addressing cold-chain challenges in India and Southeast Asia. Initial customer trials in India and Thailand showed 85% retention of CFU counts after 18 months of storage at 25°C.

- January 2025: CJ CheilJedang Corporation completed the acquisition of a 60% stake in a Vietnamese enzyme production facility for USD 45 million, expanding its footprint in Southeast Asia. The facility produces industrial enzymes for textile and pulp-and-paper applications and will be integrated into CJ's regional supply chain to serve customers in Thailand, Indonesia, and the Philippines.

- December 2024: Novozymes A/S partnered with India's Biocon Limited to co-develop fermentation-derived enzymes for pharmaceutical applications, with a focus on biosynthetic routes for active pharmaceutical ingredients. The partnership includes a USD 25 million joint investment in a pilot fermentation facility in Bangalore, expected to be operational by mid-2026.

Asia-Pacific Fermented Ingredients Market Report Scope

The Asia-Pacifc fermented ingredients market is segmented by type, form, application, and geography. On the basis of type, the market is segmented into amino acids, organic acids, polymers, vitamins, industrial enzymes, and antibiotics. On the basis of form, the market is segmented into dry and liquid. On the basis of application, the market is segmented into food and beverages, feed, pharmaceutical, industrial use, and other applications. Additionally, the study provides an analysis of the fermented ingredients market in the emerging and established markets across the Asia-Pacific.

By Product Type

| Amino Acids |

| Organic Acids |

| Polymers |

| Vitamins |

| Industrial Enzymes |

| Antibiotics |

| Probiotics & Post-biotics |

| Others |

By Form

| Dry |

| Liquid |

By Application

| Food and Beverages | Dairy |

| Bakery and Confectionery | |

| Beverages | |

| Meat and Fish Products | |

| Others | |

| Animal Feed | |

| Pharmaceutical | |

| Personal Care and Cosmetics | |

| Industrial Use (Bio-polymer, Bio-fuel, Paper) |

By Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Amino Acids | |

| Organic Acids | ||

| Polymers | ||

| Vitamins | ||

| Industrial Enzymes | ||

| Antibiotics | ||

| Probiotics & Post-biotics | ||

| Others | ||

| By Form | Dry | |

| Liquid | ||

| By Application | Food and Beverages | Dairy |

| Bakery and Confectionery | ||

| Beverages | ||

| Meat and Fish Products | ||

| Others | ||

| Animal Feed | ||

| Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Industrial Use (Bio-polymer, Bio-fuel, Paper) | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific fermented ingredients market?

The Asia-Pacific fermented ingredients market size is USD 22.57 billion in 2026.

How fast is demand for probiotics growing in the region?

Probiotics and post-biotics are advancing at a robust 9.05% CAGR through 2031, outpacing every other product segment.

Which application consumes the most fermented ingredients today?

Food and beverages lead, absorbing 51.84% of regional revenue in 2025 thanks to dairy cultures, bakery enzymes, and beverage acidulants.

Why is India the fastest-rising geography for fermented ingredients?

Government incentives for fermentation-based bulk drugs and growing urban probiotic consumption drive India’s 9.42% CAGR.

What key technology trend is reshaping production economics?

Continuous fermentation paired with AI-driven strain optimization is cutting batch times, boosting yields, and lowering carbon intensity.

Page last updated on: