Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

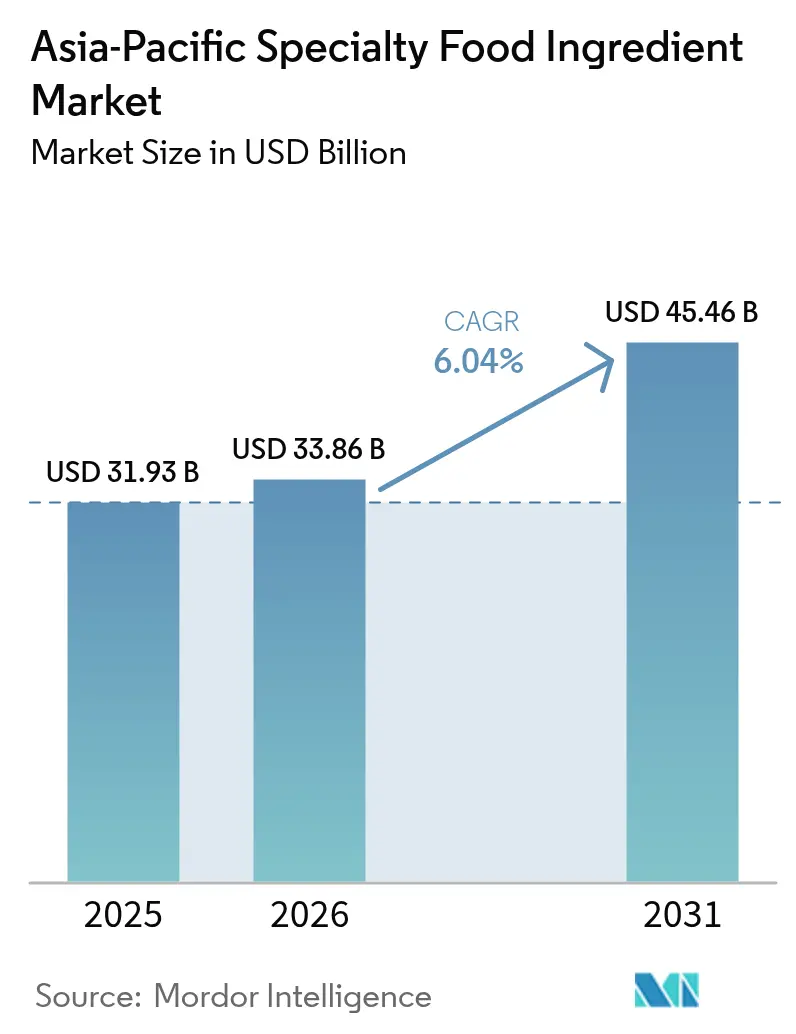

| Base Year Market Size (2025) | USD 31.93 Billion |

| Market Size (2026) | USD 33.86 Billion |

| Market Size (2031) | USD 45.46 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Specialty Food Ingredient Market Analysis by Mordor Intelligence

The Asia-Pacific specialty food ingredients market size is expected to grow from USD 31.93 billion in 2025 to USD 33.86 billion in 2026 and is forecast to reach USD 45.46 billion by 2031 at 6.04% CAGR over 2026-2031. The market growth is driven by increasing urbanization, rising household incomes, and middle-class expansion, which fuel demand for functional, plant-based, and clean-label products incorporating specialized flavors, texturants, proteins, and lipid systems. Manufacturers are enhancing their product portfolios through precision fermentation, enzyme technology, and alternative protein platforms to meet consumer demands for nutrition and sustainability. The regulatory environment is evolving, with developments such as Singapore's novel food pathway and Japan's function-claim system reducing the time required to commercialize innovative ingredients. While commodity price fluctuations highlight the importance of local sourcing and supply chain resilience, the market maintains moderate fragmentation. Multinational companies benefit from integrated value chains, while regional companies capture market share in specific segments through fermentation-derived and bio-based ingredients.

Key Report Takeaways

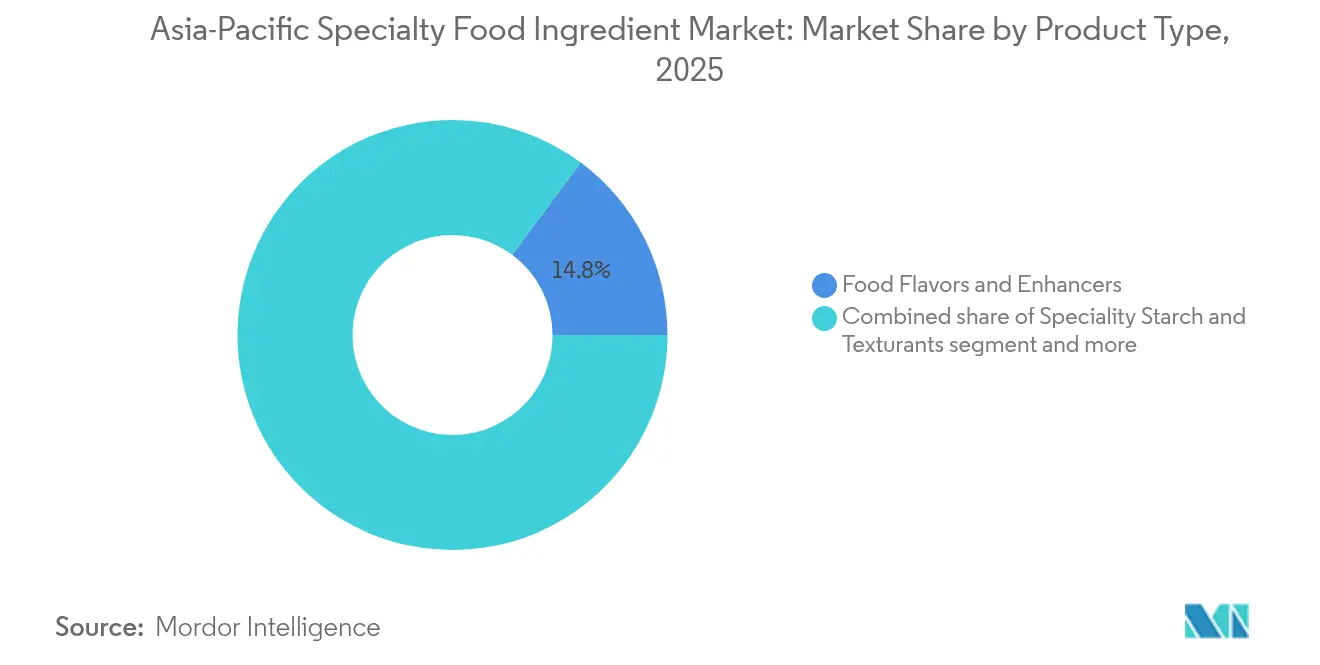

- By product type, food flavors and enhancers held 14.82% of the Asia-Pacific specialty food ingredients market share in 2025. Specialty Fats and Oils are poised for the fastest expansion, advancing at a 7.09% CAGR through 2031.

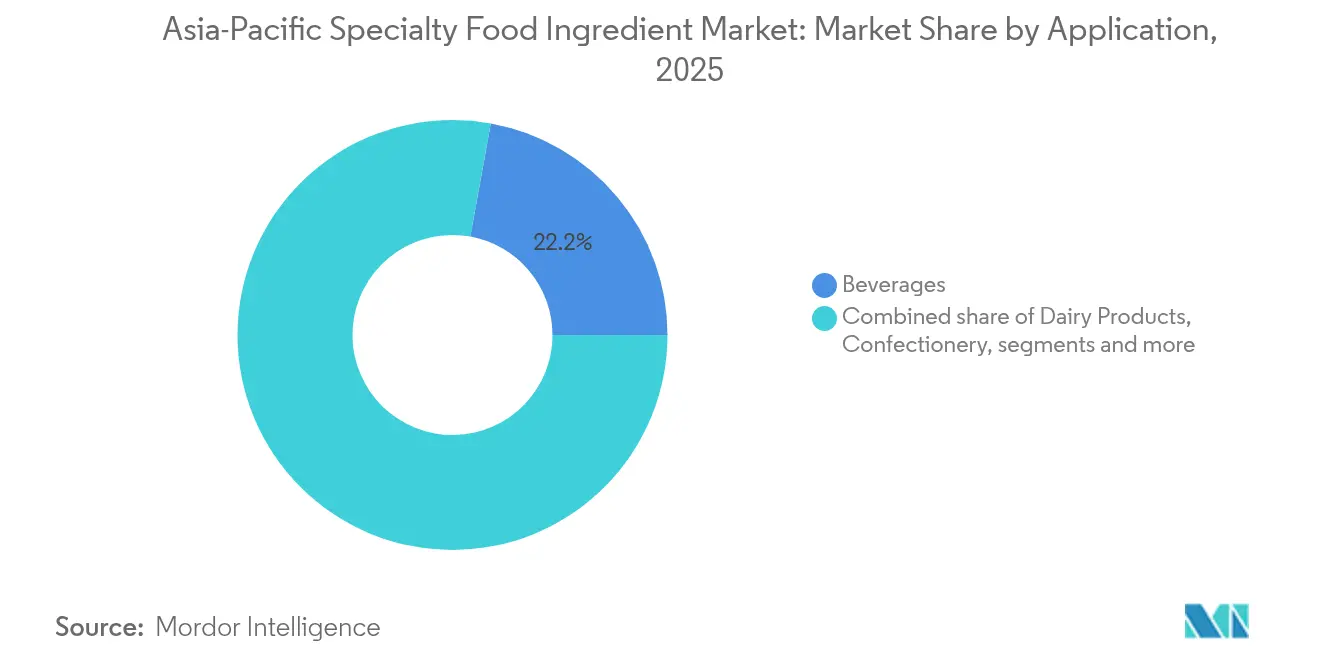

- By application, beverages led with 22.15% revenue share in 2025, while plant-based food and beverage applications are set to grow at a 7.12% CAGR to 2031.

- By geography, China commanded 40.05% of the Asia-Pacific specialty food ingredients market size in 2025, whereas India exhibits the highest projected CAGR of 7.06% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Specialty Food Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased health and wellness awareness among consumers | +1.2% | Global, strongest in urban China, India, Japan | Medium term (2-4 years) |

| Surge in demand for functional foods and beverages | +1.5% | Asia-Pacific core, spillover to Southeast Asia | Long term (≥ 4 years) |

| Rising trend of plant-based diets and veganism | +0.9% | Urban centers across China, India, Australia, Singapore | Medium term (2-4 years) |

| Popularity of natural, clean-label, and organic products | +1.1% | Japan, Australia, urban China, South Korea | Long term (≥ 4 years) |

| Expanding premium snacking and confectionery segment | +0.8% | China, India, Southeast Asia emerging markets | Short term (≤ 2 years) |

| Adoption of convenience and ready-to-eat/packaged foods | +1.0% | Urban Asia-Pacific, strongest in China, India, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Health and Wellness Awareness Among Consumers

Rising health consciousness among consumers is driving changes in ingredient demand across Asia-Pacific markets, with functional ingredients gaining wider adoption in food applications. The Japanese functional foods market demonstrates this trend, particularly in women's health and cognitive supplements, where ingredients targeting brain function and hormonal balance maintain premium pricing despite economic challenges. Japan's regulatory framework for functional claims enables manufacturers to differentiate products through evidence-based ingredient benefits, creating competitive advantages for specialty ingredient suppliers. Singapore's expansion of Nutri-Grade labeling to sauces and seasonings by 2027 increases demand for sugar and sodium reduction solutions, making enzyme-based technologies and natural flavor enhancers essential for product formulation. These regulatory changes shift ingredient selection priorities from cost to functionality, favoring suppliers with strong research capabilities and regulatory knowledge.

Surge in Demand for Functional Foods and Beverages

The functional foods market is transforming as manufacturers integrate bioactive compounds that deliver quantifiable health benefits beyond basic nutrition. In February 2025, Vivici obtained EUR 32.5 million in Series A funding to expand its production of animal-free lactoferrin and beta-lactoglobulin proteins for sports nutrition through precision fermentation. This advancement allows ingredient suppliers to improve margins by producing specialized fermentation-derived proteins that offer both environmental and functional advantages. MOA Foodtech's EUR 14.8 million European Innovation Council funding highlights the importance of AI-enhanced fermentation in expediting functional ingredient development from agricultural byproducts [1]Source: Good Food Institute, “Fermentation-Derived Proteins,” gfi.org. The regulatory frameworks in Singapore and Japan favor functional ingredients with established safety records, benefiting companies that prioritize regulatory documentation and clinical studies. The functional beverages market in India is expanding, driven by health-conscious consumers seeking drinks with natural ingredients, gut-health benefits, and energy-enhancing properties, incorporating Ayurvedic components and practical wellness solutions [2]Source: Trade Promotion Council of India, “Sip into the future: The rise of functional beverages,” indusfood.co.in.

Rising Trend of Plant-Based Diets and Veganism

The plant-based food industry has witnessed significant expansion in ingredient innovation, moving beyond traditional protein substitutes to meet consumer demands. Manufacturers now require specialized texturants, flavor masking solutions, and functional lipids to recreate the sensory experience of animal-based products. Companies like Ajinomoto, with its ACTIVA transglutaminase technology, help manufacturers achieve authentic meat-like textures, while BENEO has strengthened its portfolio of functional ingredients for dairy alternatives. The integration of precision fermentation with plant-based ingredients has resulted in hybrid solutions where microbial proteins enhance both nutrition and taste. Singapore's investment of USD 39 million in the Bezos Centre for Sustainable Protein demonstrates the region's commitment to advancing plant-based ingredient development, with shared infrastructure reducing costs and accelerating market entry. In India, the plant-based food market continues to grow, supported by traditional spiritual values of non-violence and ethical eating, alongside increasing awareness of health benefits and environmental impact. This growth is further strengthened by technological advancements, government support, and rising consumer demand across domestic and international markets [3]Source: India Brand Equity Foundation, "The Rising plant Based Sector in India," ibef.org.

Popularity of Natural, Clean-Label, and Organic Products

Consumer demand for clean-label products is influencing ingredient sourcing strategies, particularly in developed Asia-Pacific markets where consumers closely examine product labels. This trend aligns with Western market expectations for ingredient transparency. Layn Natural Ingredients' development of bio-based preservation solutions demonstrates the industry's response to extending product shelf life while maintaining clean-label requirements. Natural preservation methods command premium prices, benefiting suppliers who invest in natural extraction technologies and organic certifications. The regulatory environment in Asia-Pacific supports this transition, with Japan's functional claims system and Singapore's novel food approval process enabling market entry for natural functional ingredients. These regulations favor ingredient suppliers that maintain comprehensive traceability systems and sustainable sourcing practices, as manufacturers seek partners to support their clean-label initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sourcing and raw material supply chain disruptions | -0.7% | Global, acute in Southeast Asia import-dependent markets | Short term (≤ 2 years) |

| Lack of consumer awareness about new or novel ingredients | -0.5% | Rural Asia-Pacific, emerging markets in Indonesia, Thailand | Medium term (2-4 years) |

| Limited shelf life and instability of some specialty ingredients | -0.4% | Tropical climates across Southeast Asia | Long term (≥ 4 years) |

| Food safety and quality assurance complexities | -0.6% | China, India regulatory compliance markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sourcing and Raw Material Supply Chain Disruptions

Supply chain vulnerabilities expose ingredient manufacturers to cost volatility and availability constraints, particularly in import-dependent Southeast Asian markets. The 70% increase in cocoa prices in 2024 illustrates how climate-related commodity disruptions affect specialty ingredient supply chains, compelling manufacturers to modify formulations or accept reduced margins. Rice production fluctuations in key Asia-Pacific markets create supply constraints for starch-based ingredients, while extreme weather events disrupt raw material flows from traditional sourcing regions. Companies that diversify their supply chains and adopt alternative sourcing technologies gain advantages, as precision fermentation and cellular agriculture offer ways to reduce dependence on climate-sensitive agricultural inputs. The industry's move toward localized ingredient production, demonstrated by significant investments in regional manufacturing facilities, indicates a shift from incremental improvements to fundamental supply chain restructuring.

Food Safety and Quality Assurance Complexities

Food safety standards across Asia-Pacific markets are becoming more stringent, increasing regulatory compliance costs and creating entry barriers for smaller ingredient suppliers. Established companies with robust quality systems maintain an advantage. Updates to China's GB standards and Korea's MFDS regulations require significant investments in testing infrastructure, documentation systems, and regulatory expertise, which strain mid-tier suppliers' resources. Managing diverse regulatory frameworks across Asia-Pacific markets reduces operational efficiency, especially for ingredients that need country-specific approvals or formula adjustments. HACCP certification and traceability requirements increase operational costs and extend product development timelines. These regulatory requirements benefit compliant suppliers, as brand manufacturers prefer ingredient partners with proven regulatory compliance and comprehensive quality assurance systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Ingredients Drive Premium Growth

Food flavors and enhancers maintain a significant presence in the market with a 14.82% share in 2025, demonstrating their fundamental importance in differentiating food products across various applications. The Specialty Fats and Oils segment has emerged as the market's growth leader, advancing at a 7.09% CAGR through 2031. This notable growth trajectory reflects the industry's increasing focus on functional lipids that enable plant-based formulations and clean-label products. A prime example of this innovation is NoPalm Ingredients' introduction of REVÓLEO™, their fermentation-based alternative to traditional ingredients like palm oil, shea butter, and cocoa butter, scheduled for launch in April 2025.

The functional food ingredients segment, which encompasses essential components such as vitamins, minerals, amino acids, omega-3 ingredients, and probiotic cultures, continues to benefit from increasing consumer health consciousness and favorable regulatory frameworks supporting functional claims throughout key Asia-Pacific markets. Within this category, the protein ingredients subsegment demonstrates particularly robust growth, with plant-based proteins gaining substantial market acceptance through technological improvements in taste masking and texture enhancement. The market is also witnessing emerging opportunities in alternative protein sources, including animal, insect, and microbial proteins. This diversification is exemplified by significant industry developments, such as Nutrition Technologies' USD 100 million MOU with Sumitomo for insect protein development and Pawsible Foods' securing a USD 25,000 grant for their innovative fermentation-derived mycoprotein production.

By Application: Plant-Based Innovation Reshapes Traditional Categories

The beverage sector commands the largest market share at 22.15% in 2025, with plant-based food and beverage applications showing remarkable growth at 7.12% CAGR. This reflects the ongoing transformation in how consumers choose their food and what ingredients they prefer. Traditional beverage companies now focus on adding functional ingredients for health benefits, while companies producing plant-based alternatives need specific proteins, texturants, and flavor enhancers to match the taste and feel of conventional products.

The dairy products industry is evolving through new fermentation technologies that create animal-free dairy proteins, as seen in dsm-firmenich's recent approval for human milk oligosaccharides in China's infant nutrition market. Bakery and confectionery businesses are turning to specialty starches, texturants, and natural colorants to meet clean-label demands while maintaining product quality. The meat, poultry, and seafood industry uses enzyme technologies to improve texture and shelf life, while prepared food manufacturers balance food safety requirements with clean-label preservation methods.

Geography Analysis

The Asia-Pacific specialty food ingredients market demonstrates moderate fragmentation, creating significant opportunities for established multinational companies to strengthen their market presence. Market leaders are leveraging integrated value chains that combine advanced research and development (R&D) capabilities, large-scale manufacturing, and regulatory expertise. These companies are well-positioned to serve diverse customer segments across multiple geographies. The adoption of cutting-edge technologies, such as precision fermentation, enzyme innovations, and AI-driven formulation platforms, has become a critical differentiator. These advancements enable the development of next-generation ingredients that cater to evolving consumer demands for functionality, sustainability, and clean-label products, solidifying the leadership position of these players.

The fastest-growing segment in the market is driven by emerging disruptors and innovative technologies. Companies focusing on precision fermentation-derived ingredients and plant molecular farming are gaining traction by addressing niche market needs. For example, Kinish is advancing plant molecular farming for dairy proteins, while INTAKE is scaling yeast-based precision fermentation platforms to support global expansion. These players are capitalizing on white-space opportunities, such as sustainable packaging solutions and localized sourcing platforms, which not only address supply chain vulnerabilities but also align with the increasing demand for clean-label and environmentally friendly products. Their specialized focus and agility allow them to rapidly adapt to market trends and consumer preferences.

Other market dynamics include strategic consolidation through acquisitions and partnerships, as seen in dsm-firmenich's increased stake in Andre Pectin to 90.5% and its decision to divest lower-margin animal nutrition activities to focus on higher-value specialty segments. Additionally, ISO certification requirements and HACCP compliance frameworks create competitive advantages for established players, acting as barriers for new entrants who may lack comprehensive quality assurance systems. These regulatory and quality standards ensure product safety and consistency, further reinforcing the position of established companies in the market. Meanwhile, opportunities in sustainable and localized solutions continue to attract attention, providing room for growth across various segments of the specialty food ingredients market.

Competitive Landscape

The Asia-Pacific specialty food ingredients market shows a balanced mix of companies, where both global corporations and regional specialists compete to gain market share. Companies that lead the market succeed by managing the entire process - from developing new ingredients to manufacturing them on a large scale while following regulations. What sets companies apart is how well they use technology, especially in areas like precision fermentation, enzyme development, and using artificial intelligence to create better ingredients. These capabilities help companies produce ingredients that consumers want - ones that work well, are sustainable, and have simple, clean labels.

The market is seeing more companies join forces through acquisitions and partnerships. For example, DSM-Firmenich recently increased its ownership of Andre Pectin to 90.5% and plans to separate its animal nutrition business to focus on more profitable specialty products. Companies have opportunities to grow by developing ingredients through precision fermentation, creating sustainable packaging, and setting up local supply networks that ensure reliable delivery while meeting clean-label demands.

New companies are making their mark in specific areas - like Kinish, which uses plant technology to make dairy proteins, and INTAKE, which is expanding globally with its yeast-based fermentation methods. However, industry requirements like ISO certification and HACCP compliance give established companies an advantage, as these standards can be difficult for new companies to meet without proper quality control systems in place.

Asia-Pacific Specialty Food Ingredient Industry Leaders

-

Cargill, Inc.

-

Kerry Group plc

-

Tate & Lyle plc

-

ADM

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSM-Firmenich increased its equity stake in Yantai DSM Andre Pectin Company Limited from 75% to 90.5% by acquiring an additional 15.5% of shares, strengthening its position in the specialty food ingredient market through enhanced control of pectin production capabilities

- March 2025: Angel Yeast launched AngeoPro, a revolutionary yeast-derived protein ingredient featuring high protein content, complete amino acid profile, and neutral taste, positioning it as a sustainable alternative for food and beverage formulations across Asia-Pacific markets

- February 2025: Vivici secured EUR 32.5 million in Series A funding led by APG and Invest-NL, with participation from dsm-firmenich and Fonterra, to expand precision fermentation dairy protein production and launch lactoferrin ingredients for international markets including planned Asia-Pacific expansion

Asia-Pacific Specialty Food Ingredient Market Report Scope

The Asia-Pacific specialty food ingredient market is segmented by type into sweeteners & starch, flavors & colorants, acidulants, emulsifiers, enzymes, proteins, specialty oils & fats, and others; and by application into beverages, bakery & confectionery, dairy products, meat products, and other applications. Also, the study provides an analysis of the specialty food ingredient market in the emerging and established markets across the Asia Pacific countries, including China, Japan, India, Australia, and Rest of Asia-Pacific.

By Product Type

| Functional Food Ingredient | Vitamins | |

| Minerals | ||

| Amino Acids | ||

| Omega-3 Ingredients | ||

| Probiotic Cultures | ||

| Other Functional Food Ingredients | ||

| Speciality Starch and Texturants | ||

| Sweetener (Sugar Substitutes) | Sucralose | |

| Xylitol | ||

| Stevia | ||

| Aspartame | ||

| Saccharin | ||

| Other Sugar Substitutes | ||

| Food Flavors and Enhancers | ||

| Acidulants | ||

| Preservatives | ||

| Emulsifiers | ||

| Colorants | ||

| Enzymes | ||

| Proteins | Plant Protein Ingredients | Soy Protein |

| Wheat Protein | ||

| Rice Protein | ||

| Pea Protein | ||

| Other Plant Protein | ||

| Animal, Insect and Microbial Protein Ingredients | ||

| Speciality Fats and Oils | ||

| Food Hydrocolloids and Polysaccharides | ||

| Anti-Caking Agents | ||

| Yeast | ||

| Food-Grade Glycerin | ||

By Application

| Bakery Products |

| Beverages |

| Meat, Poultry, and Seafood |

| Dairy Products |

| Confectionery |

| Fats and Oils |

| Dressings/Condiments/Sauces/Marinade |

| Pasta, Soup and Noodles |

| Plant-based Food and Beverage |

| Other Applications |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Functional Food Ingredient | Vitamins | |

| Minerals | |||

| Amino Acids | |||

| Omega-3 Ingredients | |||

| Probiotic Cultures | |||

| Other Functional Food Ingredients | |||

| Speciality Starch and Texturants | |||

| Sweetener (Sugar Substitutes) | Sucralose | ||

| Xylitol | |||

| Stevia | |||

| Aspartame | |||

| Saccharin | |||

| Other Sugar Substitutes | |||

| Food Flavors and Enhancers | |||

| Acidulants | |||

| Preservatives | |||

| Emulsifiers | |||

| Colorants | |||

| Enzymes | |||

| Proteins | Plant Protein Ingredients | Soy Protein | |

| Wheat Protein | |||

| Rice Protein | |||

| Pea Protein | |||

| Other Plant Protein | |||

| Animal, Insect and Microbial Protein Ingredients | |||

| Speciality Fats and Oils | |||

| Food Hydrocolloids and Polysaccharides | |||

| Anti-Caking Agents | |||

| Yeast | |||

| Food-Grade Glycerin | |||

| By Application | Bakery Products | ||

| Beverages | |||

| Meat, Poultry, and Seafood | |||

| Dairy Products | |||

| Confectionery | |||

| Fats and Oils | |||

| Dressings/Condiments/Sauces/Marinade | |||

| Pasta, Soup and Noodles | |||

| Plant-based Food and Beverage | |||

| Other Applications | |||

| By Geography | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific specialty food ingredients market?

The market stands at USD 33.86 billion in 2026.

What CAGR is forecast for Asia-Pacific specialty food ingredients through 2031?

The market is projected to grow at 6.04% between 2026 and 2031.

Which product segment is expanding the fastest in Asia-Pacific?

Specialty Fats and Oils lead growth with a 7.09% CAGR through 2031.

Which application is seeing the highest growth?

Plant-based Food and Beverage applications are forecast to rise at 7.12% CAGR to 2031.

Page last updated on: