Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

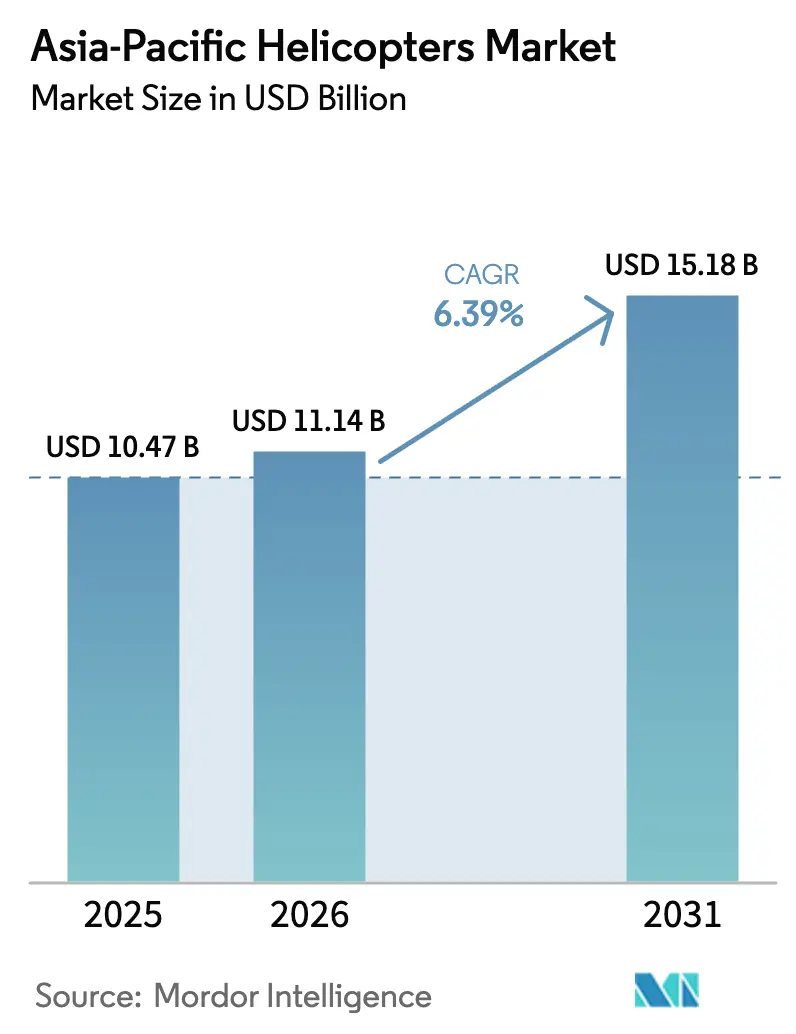

| Base Year Market Size (2025) | USD 10.47 Billion |

| Market Size (2026) | USD 11.14 Billion |

| Market Size (2031) | USD 15.18 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

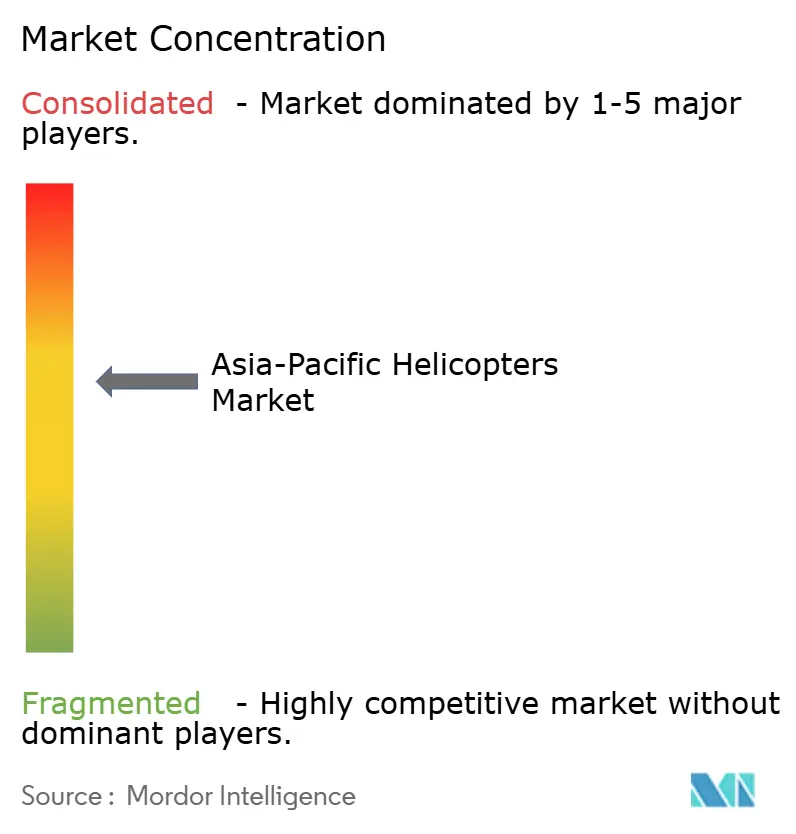

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Helicopters Market Analysis by Mordor Intelligence

The Asia-Pacific helicopters market size is expected to grow from USD 10.47 billion in 2025 to USD 11.14 billion in 2026 and is forecasted to reach USD 15.18 billion by 2031 at a 6.39% CAGR over 2026-2031. Fleet managers are shifting from age-based replacement toward mission-specific modernization as offshore wind operations, emergency medical services (EMS), and multi-role defense missions demand contemporary avionics and improved hot-and-high performance. China’s accelerated Z-20 induction, indigenous program momentum in India and Japan, and public-private air-ambulance models across Southeast Asia are driving new-build deliveries, despite a persistent pilot shortage that has held regional training capacity 22% below demand in 2025. Currency swings of up to 15% a year have historically weighed on import-reliant operators, yet localized production in India and South Korea is reducing exposure while supporting supply-chain sovereignty. Parallel technology spill-overs from eVTOL research, including composite blades and active vibration control, are already lifting turbine efficiency and cabin comfort, positioning the Asia-Pacific helicopters market for steady upgrade cycles.

Key Report Takeaways

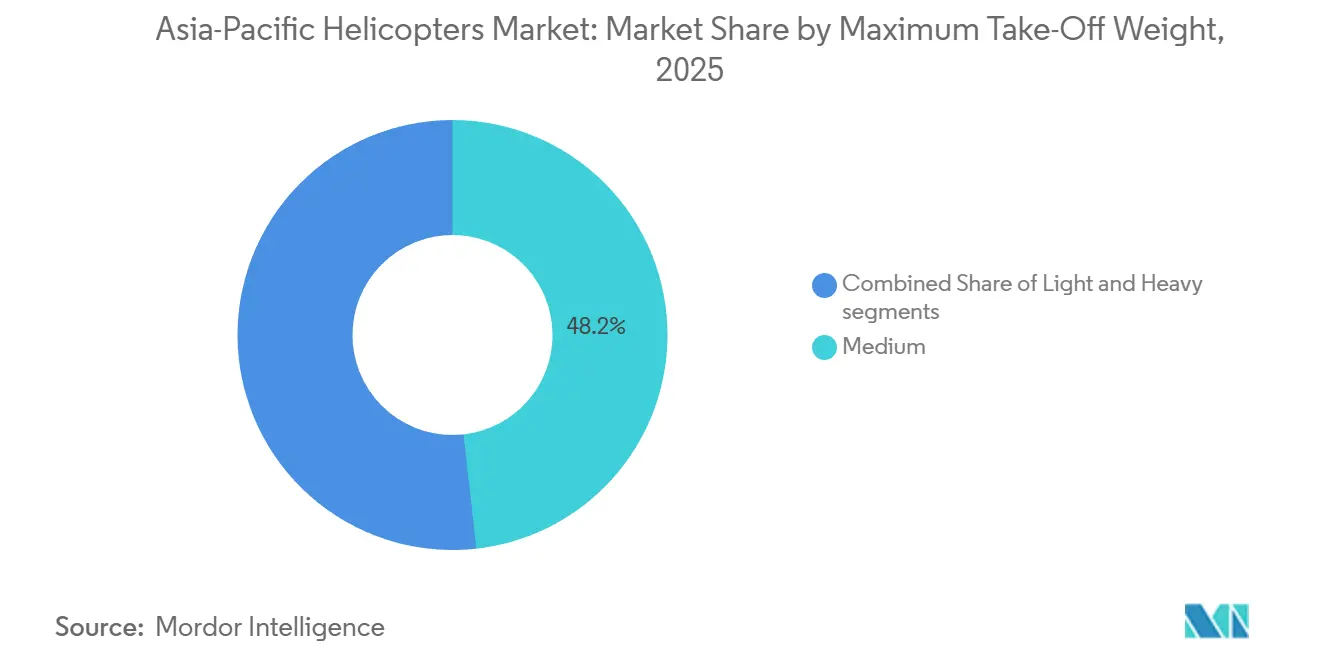

- By maximum take-off weight, medium platforms accounted for 48.23% of the Asia-Pacific helicopters market in 2025, while light platforms are forecast to grow at an 8.82% CAGR through 2031.

- By application, military missions accounted for 58.89% of the Asia-Pacific helicopters market in 2025, whereas civil and commercial demand is projected to grow at a 7.94% CAGR through 2031.

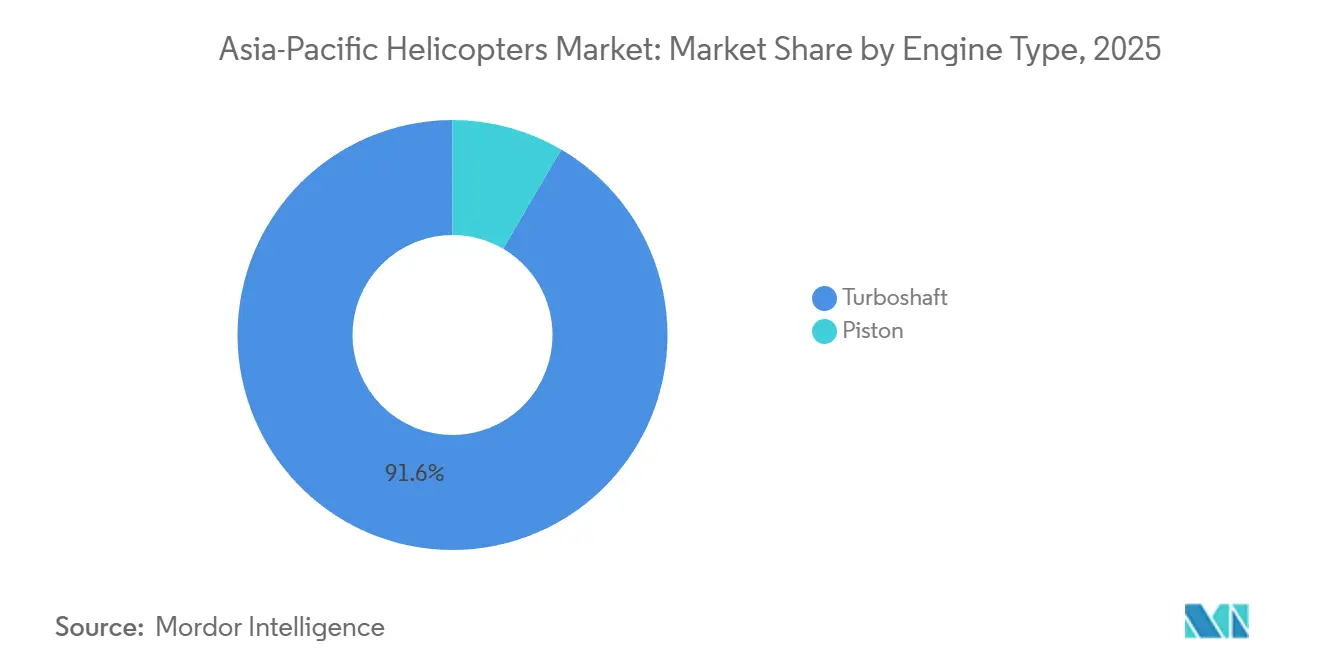

- By engine type, turboshaft engines dominated with a 91.56% share in 2025, even as piston-powered fleets are forecast to grow at a 7.57% CAGR through 2031.

- By end-use, combat accounted for 32.47% of demand in 2025, and emergency medical services (EMS) are projected to grow at an 8.11% CAGR through 2031.

- By geography, China led the Asia-Pacific helicopters market, accounting for a 31.17% share in 2025. India is projected to grow at a 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Helicopters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Next-generation eVTOL-inspired rotor technology spill-over | +0.8% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Rapid fleet modernization for offshore wind O&M in Asia-Pacific | +1.2% | Taiwan, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Asian med-evac public-private partnerships (PPPs) expansion | +0.9% | India, Thailand, Japan, South Korea | Medium term (2-4 years) |

| Rising localized defense procurement programs in India and Japan | +1.4% | India, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Recovery of tourism-linked heli-charter operations post-COVID | +0.6% | Thailand, Indonesia, Australia, China | Short term (≤ 2 years) |

| Military shift toward multi-role medium-lift platforms | +1.0% | China, India, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Next-Generation EVTOL-inspired Rotor Tech

Variable-pitch composite blades, first prototyped for eVTOL demonstrators, have reduced vibration and noise in legacy turbine models by up to 40%, thereby extending mission reach in noise-sensitive urban airspace.[1]Japan Society for Aeronautical and Space Sciences, “Variable-Pitch Rotor Blade Performance Benefits,” jsass.or.jp Sikorsky fitted active vibration control derived from Raider X research to production S-76D aircraft, lowering cabin noise to 78 decibels and winning new offshore contracts in Singapore during 2025. Tokyo’s 85-decibel daytime limit incentivizes rapid adoption across Japanese operators. Korea Aerospace Industries is integrating tilt-rotor composite blade expertise into its Light Armed Helicopter, aiming for a 15% weight reduction that enhances high-altitude performance. As these upgrades migrate into serial production, the Asia-Pacific helicopters market gains operational flexibility without waiting for full-scale eVTOL certification.

Fleet Modernization For Offshore Wind O&M

Taiwan expects to have 20.7 GW of offshore wind by 2035, requiring roughly 45 dedicated rotorcraft to ferry technicians 30-80 km offshore. Ørsted contracted Bristow in 2024 for continuous Sikorsky S-92 support at the Greater Changhua fields. Japan has designated six promotion zones and plans to establish helicopter bases in Akita and Chiba to maintain a 3 GW capacity. South Korea’s floating wind sites near Ulsan require heavy-class helicopters capable of hovering in 25-knot winds. Australia cleared the Gippsland zone in 2025, creating future demand for 8-10 aircraft by 2029.

Asian Med-Evac PPP Expansion

Hybrid funding now underpins a fast-growing regional air-ambulance network. Hong Kong’s Government Flying Service cut island-to-hospital transfer times by 35 minutes after adding two AW139s in 2024. Bangkok Dusit Medical Services operates eight helicopters under a revenue-sharing model, which caps patient charges at THB 150,000 (approximately USD 5,000), while the government rebates one-third of the costs. India’s 2025 pilot scheme covers half of Uttarakhand and Himachal Pradesh air-ambulance expenses and triggered the deployment of four Bell 407GXi units. South Korea’s Doctor Helicopter program reached 12 hubs in 2025 and posted a 92% survival rate for patients lifted within one hour. Japan’s 57-base network reduced per-flight costs to JPY 800,000 (approximately USD 5,060.78) from JPY 1.2 million (approximately USD 7,591.17) over five years.

Localized Defense Procurement

Indigenous platforms are displacing imports while effectively managing currency risk. Hindustan Aeronautics delivered 16 Light Utility Helicopters in 2024 and holds a USD 950 million backlog for 156 more through 2028, slashing import content to 42%. Japan awarded Subaru and Bell Textron USD 720 million to co-develop the UH-2, with 65% of the components to be local, in 2025. Mitsubishi Heavy Industries will supply eight SH-60K units to the Maritime Self-Defense Force, extending domestic production through 2027. South Korea budgeted KRW 890 billion (USD 0.61 billion) for 40 Light Armed Helicopters, including 20 export variants for Southeast Asia. Australia’s plan to add 29 helicopters by 2030 prioritizes regional sustainment and US system interoperability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent pilot shortage in emerging ASEAN markets | -0.7% | Indonesia, Thailand, Malaysia, Philippines | Medium term (2-4 years) |

| Currency-driven capex volatility for import-heavy operators | -0.5% | India, Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Urban air mobility (UAM) regulatory uncertainty crowding investment | -0.4% | Singapore, Japan, South Korea, Australia | Medium term (2-4 years) |

| Escalating ESG pressure against fossil-fuel rotorcraft | -0.3% | Australia, Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Pilot Shortage

Indonesia, Thailand, and Malaysia jointly require approximately 450 additional helicopter pilots by 2028, yet the training output lags significantly. Singapore’s regulator estimated a regional training deficit of 22% in 2025.[2]Civil Aviation Authority of Singapore, “Regional Pilot Training Gap,” caas.gov.sg Indonesia licensed only 87 new pilots in 2024, compared to a demand for 150, which delayed the delivery of 12 aircraft. Malaysian flight schools graduated 34 pilots in 2024, despite instructor shortages persisting. Two new Thai academies approved in 2025 will not reach capacity until 2027. The Philippines still relies on foreign schools, adding USD 80,000 per trainee to operator costs.

Currency-Driven CAPEX Volatility

Dollar-denominated helicopters expose emerging-market buyers to exchange rate fluctuations that can add 10-20% to capital costs within a year. The INR depreciated by 6.2% in 2024, resulting in a USD 1.2 million increase in the effective price of a USD 20 million medium rotorcraft. The rupiah lost 8.1% in the same period, forcing three Indonesian firms to defer Bell 407GXi deliveries. THB fluctuations led to a 12% increase in Thai lease payments in 2025. Vietnam trimmed an H145 order to two units as dong depreciation inflated its budget by 8%. Only 28% of Asian operators used hedging tools in 2024, significantly lower than the 67% uptake in Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Maximum Take-Off Weight: Light Platforms Gain on Training and Corporate Demand

The light-class segment accounted for 8,820 units within the Asia-Pacific helicopters market size in 2025 and is set to grow at an 8.82% CAGR, the fastest among weight classes. Flight academies and corporations prefer the Robinson R44, R66, and Bell 505 models, which cost USD 350 per flight hour, one-third the burn of a medium turbine. Robinson delivered 142 piston helicopters to the Asia-Pacific region in 2024, 60% of which were destined for training academies in China, India, and Australia, where demand remains capacity-constrained.[3]Robinson Helicopter Company, “Asia-Pacific Deliveries 2024,” robinsonheli.com Bell 505 adoption surged across Indonesian and Philippine charter firms, its USD 1.4 million price undercutting an Airbus H125 by 18%.

Medium-sized helicopters still commanded 48.23% of the 2025 Asia-Pacific helicopters market share, thanks to defense and offshore energy missions that require greater payload and range. Leonardo AW139 and Sikorsky S-76 remained the mainstay with 89 combined deliveries in 2024. Heavy-class usage remains niche, centered on CHC’s 14 S-92s, which serve long-range oil platforms in Australia and Malaysia. Regulatory easing also favors light helicopters. Japan reduced the single-engine experience threshold for commercial pilots to 1,200 hours in 2025, accelerating throughput for flight schools and further stimulating demand for light helicopters.

By Application: Civil and Commercial Segments Accelerate on Tourism and Corporate Transport

Military missions accounted for 58.89% of the Asia-Pacific helicopters market size in 2025, as China, India, and Japan advanced their modernization programs. Civil and commercial activities, however, are forecast to climb at a 7.94% CAGR through 2031 as tourism rebounds and corporates prioritize time-critical shuttle links. Thai charter operators added 11 helicopters in 2024 and reported 140% revenue growth on resort transfers.

Corporate usage is spreading to India’s tier-2 industrial corridors, where road congestion undermines schedules. Nine H125 and Bell 407GXi aircraft entered service on Pune-Ahmedabad and Coimbatore routes in 2024. Offshore wind services lifted commercial demand in Taiwan, where eight dedicated helicopters began operations and maintenance (O&M) duties in 2025. Scenic operators in Hokkaido and Okinawa reached 95% load factors in peak 2025 seasons after adding five H125s. This broadening use case pipeline underpins a durable demand floor beyond defense budgets in the Asia-Pacific helicopters market.

By Engine Type: Piston Gains Traction in Training While Turboshaft Dominates Mission-Critical Roles

Turboshaft powerplants held a 91.56% share of the Asia-Pacific helicopters market in 2025, driven by military, offshore, and medevac missions that require high power margins and single-engine-inoperative performance. Piston models, though, will advance at a 7.57% CAGR to 2031. A Robinson R44 burns 15 gallons of Avgas per hour, compared to 35 gallons of Jet A-1 for a Bell 407, resulting in a typical school saving USD 120,000 per year on 500 flight hours.

China’s relaxed private-pilot rules spurred 38 piston purchases in 2024. Turboshaft engines remain irreplaceable for overwater missions; S-92 and AW139 aircraft, powered by the PT6 and CT7 families, guarantee the performance envelope operators need. Military fleets in India and South Korea rely on Safran Ardiden engines, which deliver up to 1,400 shp for mountain operations at altitudes of 15,000 feet. Urban noise caps still favor turbine craft because piston models struggle to meet sub-85 decibel limits in Tokyo’s downtown corridors.

By End-Use Sector: Emergency Medical Services Expands Fastest as Air-Ambulance Networks Scale

In 2025, the combat segment captured 32.47% of the market share, fueled by surging demand for military helicopters and an uptick in procurement contracts. Factors such as escalating defense budgets, geopolitical tensions, and political instability in neighboring Asia-Pacific nations are propelling the demand for military helicopters. Emergency medical services (EMS) are expected to expand at an 8.11% CAGR through 2031, as governments recognize the survival benefits of one-hour trauma evacuation. Japan’s 57-base Doctor Helicopter network has raised trauma survival to 92%, outperforming ground transport by 14 points.

Bangkok Hospital’s eight-aircraft fleet now covers eastern provinces, cutting average transfer times by 45 minutes. India subsidizes half the operating cost of air ambulances in two Himalayan states, spurring the deployment of nine helicopters in 2025. Law enforcement applications grew modestly after Indonesia’s National Police bought four Bell 412 helicopters for border surveillance in 2024. Search and rescue demand rose in Australia, where the maritime authority contracted six AW139 helicopters to replace life-expired S-76 units.

Geography Analysis

China commanded 31.17% of the Asia-Pacific helicopters market in 2025, supported by the PLA’s 47-unit Z-20 intake and AC352 civil certification, which opened the domestic corporate and offshore segments.[4]Aviation Industry Corporation of China, “AC352 Certification Press Release,” avic.com General aviation added 68 rotorcraft in 2024 as simplified licensing rules encouraged private ownership. AVIC exported four AC313A helicopters to Cambodia in 2025 for disaster relief, signaling early overseas traction.

India remains the fastest-growing country with a 7.22% CAGR outlook to 2031. Hindustan Aeronautics’ Light Utility Helicopter (LUH) backlog of 156 units anchors production, while the government’s 50% air ambulance subsidy seeded nine private helicopters in hill states during 2025. Urban executives in Pune and Ahmedabad chartered H125 flights that bypass road congestion, broadening civil uptake.

Japan mixes defense and civil power. Eight SH-60K orders in 2024 sustain domestic jobs and strengthen anti-submarine coverage. The Doctor Helicopter network’s 57 bases underpin the growth of med-evac services. Offshore wind promotion zones in Akita and Chiba will need 10-12 medium helicopters by 2028. South Korea’s Surion and Light Armed Helicopter programs drive local output while exports to Peru validate price competitiveness. Australia added 18 rotorcraft in 2024, with applications spanning maritime defense, offshore wind, and tourism missions. The country awarded Babcock a contract for six AW139 rescue helicopters.

Regulatory Landscape

Rotorcraft certification and operating rules across Asia-Pacific continue to tighten around formal airworthiness baselines and more prescriptive operational standards. In China, the Civil Aviation Administration of China (CAAC) brought the Airworthiness Regulations for Normal Category Rotorcraft (2025 Order No. 8) into force on January 1, 2026 for rotorcraft up to 3,180 kg and up to nine seats. In February 2026, CAAC opened industry consultation on special conditions for the AC332, including a 30-minute All Engines Operating power status. Australia maintains a dedicated rotorcraft air transport regime through the Civil Aviation Safety Authority (CASA) framework, with the Part 133 Manual of Standards compiled and in force as of March 14, 2026, covering items such as NVIS operations and fuel requirements.

Regulators are also aligning helicopter oversight with broader aviation system changes, particularly around unmanned aircraft integration that affects shared airspace, operator permitting, and infrastructure planning at heliports and airports. The Civil Aviation Authority of Singapore (CAAS) published the Air Navigation (101, Unmanned Aircraft Operations) (Amendment No. 3) Regulations 2025 on December 26, 2025, effective December 29, 2025, while CAAC updated its type-certification management procedures in May 2026 (AP-21-AA-2026-11R2) to formally include civil unmanned aircraft and remote control stations. Thailand and Pacific island markets have also been updating helicopter operations requirements and international helicopter operations standards through their national authorities, supporting more standardized compliance expectations for commercial and public-service operators.

Value Chain Analysis

The value chain in the Asia-Pacific helicopters market runs from global subsystem suppliers (notably engines, avionics, and dynamic components) through OEM final assembly, completions, delivery, and long-tail MRO and spares distribution. Operators are placing more weight on assured parts availability and through-life support alongside the aircraft sale. Supply constraints in propulsion and maintenance capacity remain a key friction point, with industry commentary highlighting engine shortages and maintenance backlogs across Asia, and constraints on specific engine lines affecting availability for popular training helicopters.

OEMs are responding by deepening regional industrialization and support footprints to shorten lead times and reduce import dependence. Airbus expanded Indian aerostructure sourcing through fuselage manufacturing awards to Mahindra Aerostructures (H130 in April 2025 and H125 in August 2025) and confirmed Vemagal, Karnataka, as the location for an H125 final assembly line with Tata Advanced Systems (October 2025). On the services side, Airbus inaugurated a regional logistics hub in Singapore in February 2026 to support parts distribution across 21 Asia-Pacific countries, reinforcing the aftermarket layer of the chain and improving spares responsiveness for civil, public-safety, and offshore operators.

Competitive Landscape

Airbus Helicopters (Airbus SE), Leonardo S.p.A., Textron Inc., The Boeing Company, and Lockheed Martin Corporation collectively held approximately 58% of the civil and military segments within the Asia-Pacific helicopters market in 2025; however, their dominance is eroding as local champions emerge. Hindustan Aeronautics won a USD 950 million LUH contract in 2024 at price points 25% lower than those of its imported rivals. Korea Aerospace Industries exported eight Surion helicopters to Peru in 2024 at an 18% discount to comparable Leonardo offers while bundling training and MRO support. AVIC’s AC352 certification positions the maker to satisfy China’s corporate shuttle and offshore requirements, where domestic content rules favor local supply.

Technology differentiation is shifting toward predictive maintenance and low-noise flight. Airbus integrated health-monitoring analytics on H145 and H160 fleets in Australia during 2025, cutting unscheduled downtime by 22% and winning new offshore contracts.[5]Airbus Helicopters, “Predictive Maintenance Suite for H145,” airbus.com Lockheed Martin bundled 10-year support packages with S-92 deliveries to Australian and Malaysian operators, boosting customer retention and raising switching costs. Patent filings underscore the arms race: Airbus lodged seven rotor-blade designs in 2024-2025, focusing on noise reduction, while Leonardo filed five modules for rapid mission reconfiguration.

Cost leadership remains Robinson’s forte. It shipped 142 R44 and R66 units to the Asia-Pacific region in 2024 at prices 35% below those of turbine alternatives, dominating the piston training niche. Smaller US players, such as Enstrom and MD Helicopters, delivered fewer than 20 units combined, as dealers prioritized higher-margin European and mainstream US brands. Across the competitive spectrum, the Asia-Pacific helicopters market continues to reward OEMs that combine regional assembly, through-life support, and financing flexibility.

Asia-Pacific Helicopters Industry Leaders

Leonardo S.p.A.

Lockheed Martin Corporation

The Boeing Company

Textron Inc.

Airbus Helicopters (Airbus SE)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is visible where governments are funding rotorcraft-enabled public services and connectivity, and where operators want bundled aircraft plus sustainment to manage training and supply constraints identified in the region. India provides an anchor example through the modified UDAN connectivity push, including a 10-year plan with a reported outlay of INR 28,840 crore for regional connectivity infrastructure that includes 200 modern helipads. This creates a clearer pathway for helicopter deployment beyond major metro corridors. In March 2026, the Indian Union Cabinet approved a procurement initiative under modified UDAN allocating INR 400 crore for two HAL Dhruv helicopters for Pawan Hans, alongside fixed-wing acquisitions, reinforcing demand for locally supported platforms in difficult terrain and public-service missions.

Defense indigenization and sovereign sustainment are the other major opportunity axis, with programs expanding the addressable scope for local manufacturing, final assembly, and deep MRO. HAL has publicly outlined a long-horizon production strategy for about 1,000 military helicopters in the 3-15 tonne class supported by facility expansion, including the Tumakuru helicopter factory. Australia is also executing its Multi Role Helicopter Rapid Replacement Project for 40 UH-60M Black Hawks, with a parallel emphasis on through-life support. Taken together with persistent pilot and technician capacity gaps in the region, these initiatives support demand for OEMs and service providers that offer integrated packages combining aircraft, training, spares logistics, and availability-based maintenance rather than standalone deliveries.

Recent Industry Developments

- April 2026: Vietnam Helicopter Corporation ordered three Airbus H225 helicopters to expand offshore energy operations. The order adds heavy twin capacity suited to longer-range overwater missions and strengthens Airbus presence in Southeast Asia's offshore segment. It also signals operator preference for platforms with established support ecosystems as availability and spares responsiveness become more critical.

- February 2026: Leonardo signed an MoU with Adani Defence and Aerospace to build an India-focused helicopter manufacturing ecosystem, targeting AW169M and AW109 TrekkerM variants. The agreement supports indigenization requirements and positions Leonardo for local assembly, supply-chain localization, and deeper sustainment participation in India. It also increases competitive pressure on other OEMs to pair bids with manufacturing and MRO commitments in-country.

- August 2025: Lockheed Martin delivered five more S-70i Black Hawk helicopters to the Philippine Air Force. The delivery advances fleet modernization and strengthens the installed base that drives follow-on training, spares, and sustainment demand across the Philippines. It also reinforces the role of repeat batches in keeping regional delivery pipelines active amid broader aerospace supply constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as the total value of helicopter procurement in Asia-Pacific, covering military, civil, and commercial demand for new rotorcraft across key operating missions.

Scope exclusions: We exclude routine aftermarket revenues such as MRO, spare parts, upgrades, leasing, and pre-owned helicopter transactions unless they are explicitly bundled within a new aircraft procurement contract.

Segmentation Overview

- By Maximum Take-off Weight

- Light

- Medium

- Heavy

- By Application

- Military

- Civil and Commercial

- By Engine Type

- Piston Engine

- Turboshaft Engine

- By End-Use Sector

- Combat

- Offshore Energy

- Emergency Medical Services (EMS)

- Law Enforcement and Public Safety

- Tourism and VIP Charter

- Search and Rescue (SAR)

- Utility and Aerial Work

- Intelligence, Surveillance, and Reconnaissance (ISR)

- By Geography

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the country demand map, and compile a stable set of reference indicators that can be checked year after year. We relied on public sources such as ICAO for aviation context, IATA for operator and traffic signals, World Bank and IMF for macro indicators, SIPRI for defense spending trends, and national civil aviation regulators and transport ministries for fleet and operational cues.

To convert those signals into a workable value model, we also reviewed OEM and operator public materials such as annual reports, investor presentations, and press releases about orders and deliveries. In specific cases, we used import and export statistics, patent databases, and global contracts and tenders databases to clarify procurement timing and to sanity-check what is publicly announced versus what is being delivered. The sources listed above are illustrative and not exhaustive, and we used additional references during data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought in the region and why, since published disclosures can be uneven across countries and missions. We spoke with a mix of fleet operators, procurement stakeholders, maintenance ecosystem participants, and subject experts across APAC, then used these inputs to adjust adoption assumptions by mission need and weight class.

The most useful inputs were typical order cycle length, shifts in the mix between light, medium, and heavy platforms, and the pricing logic seen in recent contracts, including what is counted within the delivered aircraft package.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 28% | |

| Smaller Players: 19% | Managers: 60% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procurement value is reconstructed from a country demand pool, linked to fleet expansion and replacement needs across military, civil, and commercial missions. Once the country totals are formed, they are stress-tested using selective bottom-up approximations such as sampled announced orders and deliveries, typical unit pricing bands by weight class, and channel checks on timing, and then adjusted when gaps appear.

Key inputs for this market include helicopter fleet age and replacement intensity, defense and public safety procurement budgets, offshore energy activity (including logistics needs), EMS and SAR modernization programs, and the share of turboshaft versus piston helicopters used in each mission set. Forecasts are produced using scenario analysis, where base demand is tied to these drivers and then varied for procurement delays, contract slippage, and currency timing that can change reported value in a given year. When a bottom-up check is incomplete for a country, we fill the gap using comparable-country benchmarks, then re-validate the implied units and pricing with experts before finalizing the value.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as announced order backlogs, delivery cadence patterns, defense budget direction, and civil fleet growth cues, so totals stay aligned with actual demand conditions. Variances are investigated at the country and mission level, and outliers are revisited by rechecking source assumptions and, when needed, re-contacting interviewees to confirm what changed.

Before sign-off, the full model goes through a multi-step analyst review focusing on math checks, consistent scope application, and year-on-year reasonableness. Reports are refreshed annually, with interim updates triggered by material events such as large tender awards, major program cancellations, or sharp currency movements. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Helicopters Market Size Compared Against Other Published Estimates

It is common to see different market values for helicopters in Asia-Pacific because the boundary can shift based on what is counted as revenue and which year is treated as the base. Estimates can also change when pricing is handled differently, for example, using list prices versus contract-realistic prices, or mixing delivery value with service and retrofit spending.

By tracking procurement-linked demand indicators and then refreshing country-level order and delivery timing checks, Mordor Intelligence keeps the count focused on new helicopter procurement value in Asia-Pacific, which leads to a different number than studies that combine aftermarket, leasing, or pre-owned activity into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.47 B (2025) | |

| Regional Consultancy A | USD 15.60 B (2024) | This estimate includes aftermarket items such as MRO, upgrades, and spares, and it may also include leasing, which lifts the total beyond new aircraft procurement. |

| Trade Journal B | USD 56.87 B (2033) | This figure is a long-horizon forecast with a broad scope that can mix new, pre-owned, and multiple applications, so the value is not directly comparable to a single-year procurement-only market size. |

The table shows that the biggest spread comes from scope and timing rather than a simple math difference. When the count is limited to new helicopter procurement in a defined region and then cross-checked with order cadence and realistic pricing bands, the result stays traceable to clear variables and can be replicated in future updates.

Key Questions Answered in the Report

What is the current value of the Asia-Pacific helicopters market?

The Asia-Pacific helicopters market is valued at USD 11.14 billion in 2026 and is projected to reach USD 15.18 billion by 2031, registering a 6.39% CAGR.

Which country is growing fastest for helicopter procurement in Asia-Pacific?

India is expected to post a 7.22% CAGR through 2031, led by Hindustan Aeronautics deliveries and expanding air-ambulance networks.

Which segment will add the most new helicopters by 2031?

Light platforms will grow fastest at an 8.82% CAGR as flight schools and corporates favor lower operating costs.

How big is the civil and commercial share compared with military demand?

Military missions held 58.89% in 2025, yet civil and commercial sectors are forecasted to expand at 7.94% CAGR, narrowing the gap by 2031.

Why are piston helicopters regaining popularity?

Training academies can cut annual fuel costs by around USD 120,000 compared with turbine models, driving a 7.57% CAGR for piston fleets.

What challenges could slow market growth?

Pilot shortages, currency volatility on imported aircraft, and evolving ESG standards are the main headwinds identified for the next four years.

Page last updated on: