Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

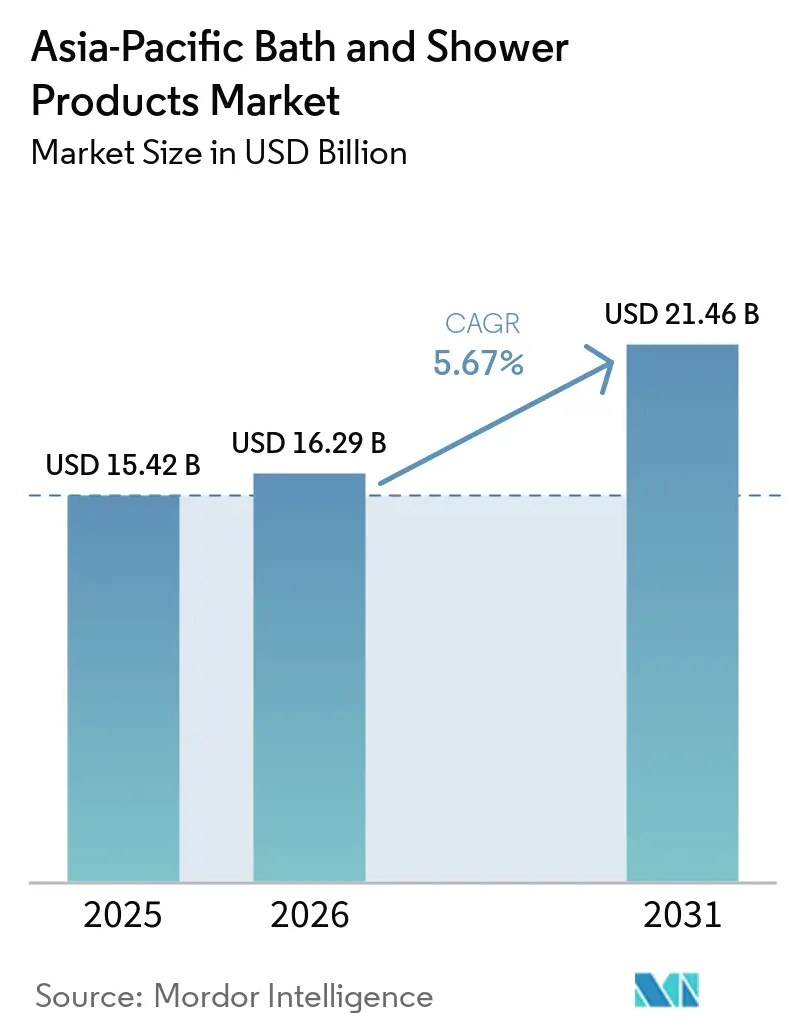

| Base Year Market Size (2025) | USD 15.42 Billion |

| Market Size (2026) | USD 16.29 Billion |

| Market Size (2031) | USD 21.46 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

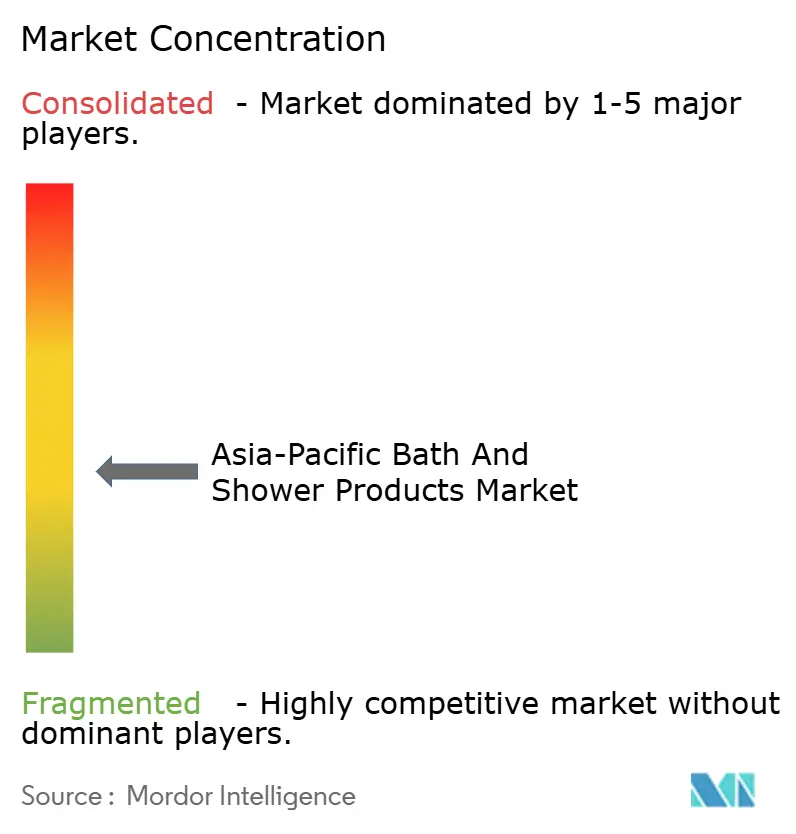

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Bath and Shower Products Market Analysis by Mordor Intelligence

Asia-Pacific Bath & Shower Products Market size in 2026 is estimated at USD 16.29 billion, growing from 2025 value of USD 15.42 billion with 2031 projections showing USD 21.46 billion, growing at 5.67% CAGR over 2026-2031. This growth trajectory reflects the region's evolving consumer preferences toward premium personal hygiene products and the increasing penetration of bath and shower products in Asia-Pacific across diverse demographic segments. The market's expansion is particularly driven by the convergence of traditional cleansing habits with modern formulation science, creating opportunities for brands that can bridge heritage practices with contemporary consumer expectations. Urbanization and a growing young population are fueling demand, alongside expanding e-commerce channels that enhance accessibility and product variety. Consumers increasingly seek premium, spa-like bathing experiences, boosting innovations in moisturizing, exfoliating, and aromatherapy products. Sustainability concerns also promote the adoption of eco-friendly packaging. These combined factors create a dynamic market environment focused on wellness, convenience, and environmentally responsible products.

Key Report Takeaways

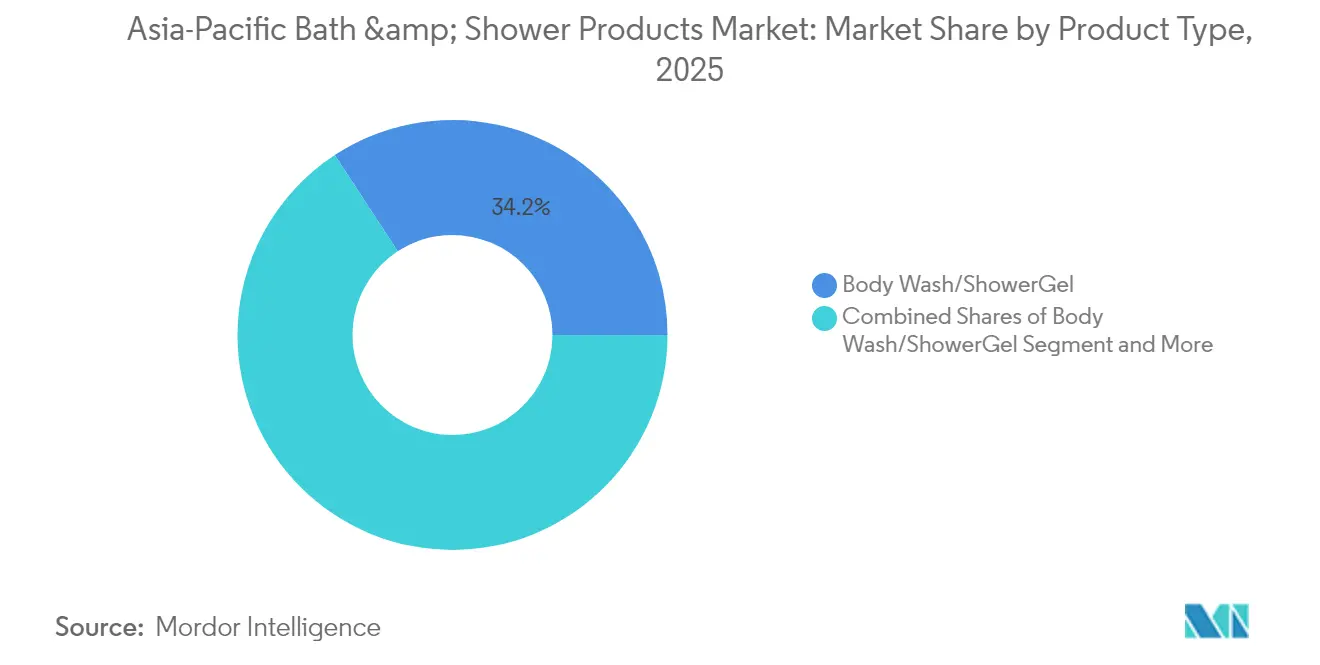

- By product type, body wash/shower gel captured 34.22% of the Asia-Pacific body care market share in 2025, while the segment is forecast to expand at a 5.74% CAGR to 2031.

- By category, conventional products dominated with 67.15% market share in 2025, though organic products are projected to achieve the fastest growth at 6.22% CAGR through 2031.

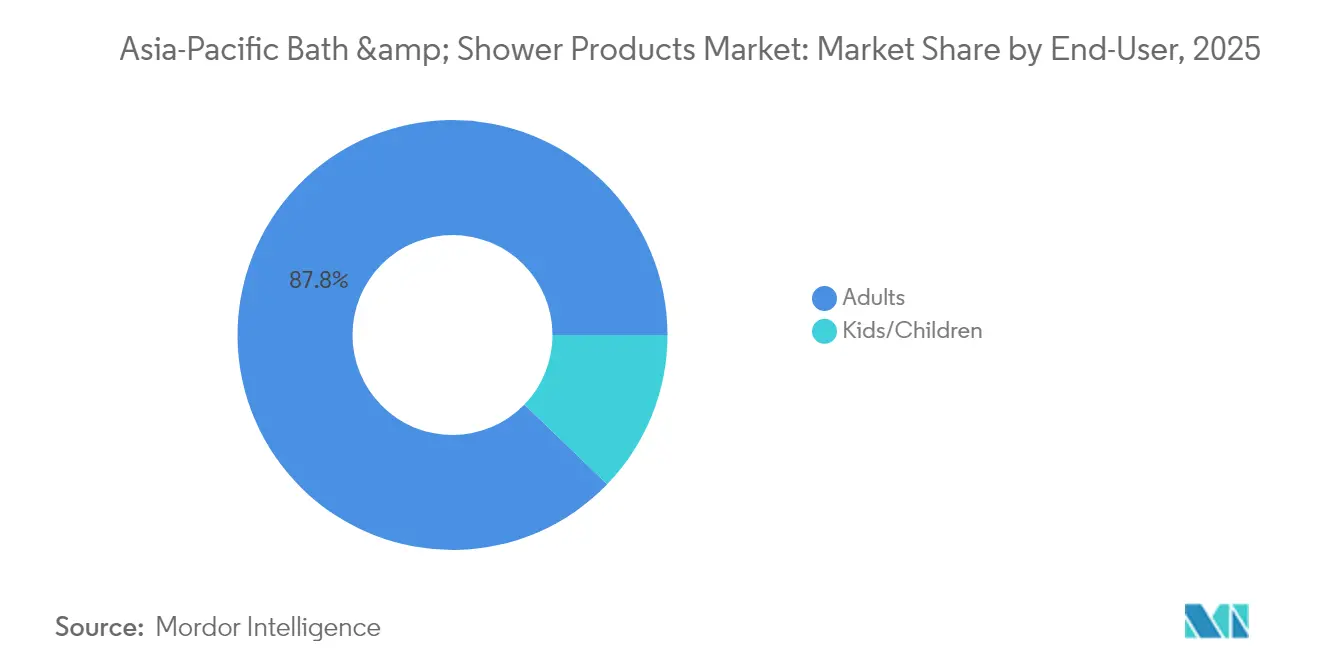

- By end-user, adults represented 87.78% of market share in 2025, while the kids/children segment is expected to register the highest growth rate at 7.26% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets held 36.10% market share in 2025, whereas online retail stores are anticipated to grow at the fastest pace of 6.05% CAGR through 2031.

- By geography, China commanded 37.55% of the Asia-Pacific body care market in 2025, while India is positioned to achieve the strongest regional growth at 6.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Bath and Shower Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in Moisturizing and Exfoliating Products | +1.2% | China, Japan, South Korea, with spillover to Southeast Asia | Medium term (2-4 years) |

| Demand for pH-Balanced, Sulfate-Free Products | +0.9% | Global, with early adoption in Australia, Singapore, urban China | Short term (≤ 2 years) |

| Natural and Organic Ingredient Demand | +1.1% | Australia, New Zealand, Japan, urban centers across Asia-Pacific | Medium term (2-4 years) |

| Sustainability and Eco-friendly Packaging | +0.8% | Australia, Japan, Singapore, with growing influence in China, India | Long term (≥ 4 years) |

| Influence of Social Media and Celebrity Endorsement | +0.7% | China, India, Thailand, South Korea, Vietnam | Short term (≤ 2 years) |

| Expansion of E-commerce Channels | +1.0% | China, India, Indonesia, Thailand, with moderate impact across Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Innovation in Moisturizing and Exfoliating Products

Product innovation in moisturizing and exfoliating formulations is reshaping consumer expectations across Asia-Pacific markets. Unilever's March 2025 launch of Lifebuoy's Skin Solutions range exemplifies this trend, combining premium skincare benefits with traditional hygiene functions to capture consumers seeking multifunctional products. The convergence of skincare and body care categories is particularly pronounced in markets like Japan, where consumers increasingly demand concentrated care products that address specific skin concerns while maintaining cleansing efficacy. This trend is driving brands to invest in advanced formulation technologies that can deliver visible skin benefits beyond basic cleansing. The shift toward specialized products targeting different body parts and skin conditions is creating new market segments and premium pricing opportunities. Asian consumers' growing sophistication in ingredient awareness is pushing manufacturers to develop products with clinically proven benefits rather than relying solely on traditional marketing claims.

Demand for pH-Balanced, Sulfate-Free Products

Consumer awareness of harsh chemical ingredients is driving unprecedented demand for gentler formulations across the region. Research on palm-based surfactants indicates that sodium laureth sulfate alternatives and amino acid-based surfactants demonstrate lower cytotoxicity while maintaining effective cleansing properties [1]Source: Science.gov, "Sample records for palm-based laureth surfactants", science.gov. This scientific validation is particularly relevant in markets like Australia and Singapore, where consumers actively seek products that minimize skin irritation while delivering superior cleansing performance. The trend extends beyond premium segments, with mass-market brands reformulating existing products to eliminate sulfates and adjust pH levels to match skin's natural acidity. Regulatory frameworks in several ASEAN countries are beginning to recognize these formulation improvements, with some markets considering preferential treatment for products meeting specific mildness criteria. Growing demand for ASEAN Sensitive Skin Care products is encouraging brands to launch mild, pH-balanced bath and shower formulations. The shift toward sulfate-free formulations is creating supply chain challenges as manufacturers source alternative surfactants, but it's also opening opportunities for brands that can effectively communicate these benefits to increasingly educated consumers.

Natural and Organic Ingredient Demand

The organic segment's 6.37% CAGR significantly outpaces the conventional category, reflecting deep consumer preference shifts toward natural formulations. Academic research demonstrates that packaging materials and certification labels like NATRUE, COSMOS, and EU Ecolabel strongly influence perceived product quality and naturalness. This consumer behavior is particularly pronounced in developed APAC markets where environmental consciousness intersects with personal care choices. The trend is creating opportunities for brands that can authentically communicate natural ingredient sourcing and sustainable production methods. Local ingredient sourcing is becoming increasingly important, with companies like The Body Shop leveraging Community Fair Trade partnerships across 14 countries to source raw materials while supporting local communities. The challenge lies in scaling natural ingredient supply chains while maintaining product consistency and cost competitiveness against conventional alternatives. Regulatory harmonization across ASEAN markets through the ASEAN Cosmetic Directive is facilitating easier market entry for organic products meeting standardized requirements.

Sustainability and Eco-friendly Packaging

Environmental packaging innovations are gaining traction as brands respond to consumer and regulatory pressure for sustainable solutions. Australian brand Conserving Beauty's adoption of Futamura's NatureFlex compostable films for sachet packaging demonstrates how companies are integrating renewable materials that meet industrial composting standards AS4736, EN13432, and ASTM D6400. The Body Shop's commitment to making all bath, body, and haircare products fully recyclable by 2025, with over 68% of packaging currently technically recyclable, illustrates how major brands are setting ambitious sustainability targets. This trend is creating competitive advantages for companies that can demonstrate measurable environmental impact reduction while maintaining product performance. The integration of post-consumer recycled materials and refillable packaging systems is becoming increasingly important in markets like Japan and Australia, where environmental regulations are becoming more stringent. The challenge for brands is balancing sustainability goals with practical considerations like product protection, shelf life, and cost-effectiveness across diverse APAC markets with varying waste management infrastructures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns Over Chemicals and Allergens | -0.6% | Global, with heightened sensitivity in Japan, Australia, urban China | Short term (≤ 2 years) |

| Presence of Counterfeit Products | -0.8% | China, Thailand, Indonesia, Malaysia, Philippines | Medium term (2-4 years) |

| Frequent Brand Switching Behavior | -0.4% | China, India, Southeast Asia markets | Short term (≤ 2 years) |

| Regulatory Ingredient Restrictions | -0.5% | ASEAN markets, China, with spillover effects across APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns Over Chemicals and Allergens

Consumer anxiety over chemical ingredients is constraining market growth as safety-conscious buyers delay purchases or avoid certain product categories entirely. Indonesia's BPOM identified 16 cosmetic products containing hazardous ingredients including mercury, retinoic acid, hydroquinone, lead, and Red K10 dye in early 2025, highlighting persistent safety concerns that undermine consumer confidence. These safety violations create ripple effects across the market, as consumers become more cautious about product selection and demand greater transparency in ingredient disclosure. The challenge is particularly acute for brands operating across multiple APAC markets with varying regulatory standards and consumer awareness levels. Companies must invest significantly in reformulation, safety testing, and consumer education to address these concerns while maintaining product efficacy. The trend toward ingredient transparency is creating competitive advantages for brands that can clearly communicate product safety and ingredient sourcing, but it's also increasing operational complexity and costs across the supply chain.

Presence of Counterfeit Products

Thailand's seizure of THB 46.2 billion worth of counterfeit cosmetics from China in February-March 2025 demonstrates how fake products undermine legitimate market growth by eroding consumer trust and diverting revenue from authentic brands. The Philippines' cosmetics industry response through a memorandum of understanding involving 18 companies and the Intellectual Property Office illustrates how the sector is mobilizing to combat online counterfeit sales. E-commerce platform dominance in markets like Indonesia, where Shopee controls 80.96% of moisturizer sales, creates both opportunities and vulnerabilities for counterfeit infiltration. The counterfeit problem is particularly damaging in developing markets where price sensitivity makes consumers more susceptible to fake products, while sophisticated counterfeiting operations exploit free trade zones and complex distribution networks to evade detection. This constraint requires coordinated industry and government responses, including enhanced authentication technologies, stricter platform oversight, and consumer education initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Body Wash Dominance Drives Innovation

Body wash and shower gel products captured 34.22% market share in 2025 while simultaneously achieving the fastest growth at 5.74% CAGR through 2031, reflecting consumer migration from traditional bar soaps toward liquid formulations. This dual leadership position underscores how liquid formats better accommodate modern formulation innovations like pH-balancing, sulfate-free surfactants, and specialized moisturizing ingredients that consumers increasingly demand. Bar soap maintains significant presence despite declining relative share, particularly in price-sensitive markets and rural areas where traditional cleansing preferences persist. The "Other Product Types" segment, encompassing body scrubs, exfoliators, bath salts, and shower oils, represents the most dynamic category as brands expand beyond basic cleansing to offer specialized treatments targeting specific skin concerns and wellness experiences.

The product type evolution reflects deeper changes in consumer behavior, particularly in developed APAC markets where bathing rituals are becoming more elaborate and wellness-focused. Japan's soap market demonstrates this transition, with solid soap gaining renewed interest for concentrated care and natural ingredients, while liquid formats dominate urban areas seeking convenience and advanced formulations. Innovation in moisturizing and exfoliating products is creating new subcategories within each format, as brands like Unilever introduce hybrid products that combine traditional hygiene functions with premium skincare benefits. This trend toward multifunctional products is reshaping traditional product boundaries and creating opportunities for brands that can effectively communicate enhanced benefits while maintaining competitive pricing across diverse APAC markets with varying consumer sophistication levels.

By Category: Organic Surge Challenges Conventional Dominance

The organic segment's 6.22% CAGR significantly outpaces conventional products despite the latter maintaining 67.15% market share in 2025, indicating a fundamental shift in consumer preferences toward natural formulations. This growth differential suggests that organic products are capturing an increasing share of new market entrants and category switchers, particularly among younger demographics and urban consumers with higher disposable incomes. Conventional products retain dominance through established distribution networks, competitive pricing, and brand loyalty, but face mounting pressure to reformulate with cleaner ingredients and sustainable packaging to remain competitive.

Consumer research demonstrates that packaging materials and certification labels strongly influence perceived naturalness and quality, creating competitive advantages for organic brands that invest in authentic sustainability credentials. The Body Shop's Community Fair Trade program, spanning 18 groups across 14 countries, exemplifies how organic brands are building authentic supply chain stories that resonate with environmentally conscious consumers. Regulatory harmonization through the ASEAN Cosmetic Directive is facilitating organic product market entry by standardizing certification requirements across member countries. The challenge for conventional brands lies in transitioning toward cleaner formulations while maintaining cost competitiveness and product performance standards that consumers expect from established brands.

By End-User: Adult Segment Stability Masks Children's Growth Potential

Adults constitute 87.78% of the market in 2025, reflecting the category's primary focus on working-age consumers with independent purchasing power and established personal care routines. However, the kids and children segment's 7.26% CAGR represents the fastest growth trajectory, driven by increasing parental awareness of gentle formulations and the emergence of specialized products designed for sensitive young skin. This demographic shift creates opportunities for brands that can develop age-appropriate formulations while building early brand loyalty that extends into adulthood.

The adult segment's dominance masks significant internal diversity, encompassing different age cohorts with varying preferences for product formats, ingredients, and price points. Social media influence research from Vietnam indicates that younger adults respond differently to influencer marketing compared to older demographics, with authenticity and expertise carrying more weight than celebrity endorsements. The children's segment growth is supported by regulatory frameworks that increasingly recognize the need for specialized safety standards for products intended for young users, with markets like Indonesia implementing specific labeling requirements for children's cosmetics. This regulatory evolution is creating barriers to entry but also opportunities for brands that can demonstrate superior safety profiles and age-appropriate formulations. The segment's growth potential is particularly strong in markets with young populations and rising household incomes, where parents are willing to invest in premium products for their children's care.

By Distribution Channel: Digital Transformation Reshapes Retail Hierarchy

Supermarkets and hypermarkets maintained 36.10% market share in 2025, leveraging their established presence and consumer shopping habits, while online retail channels achieved the fastest growth at 6.05% CAGR, fundamentally reshaping traditional distribution hierarchies. This channel evolution reflects changing consumer behaviors accelerated by digital adoption and the convenience of home delivery, particularly in urban areas where time-pressed consumers value the efficiency of online shopping. Convenience and grocery stores serve as important accessibility points for routine purchases, while other distribution channels including specialty beauty retailers and direct-to-consumer platforms are gaining traction in specific market segments.

E-commerce platform dynamics reveal significant concentration, with Shopee commanding 80.96% of Indonesia's moisturizer market, followed by Lazada at 11.48% and Tokopedia at 7.25%. Southeast Asian cosmetics sales across major platforms reached USD 620 million in May 2024, with Vietnam capturing 45% share and skincare representing the dominant product category. However, regulatory enforcement is intensifying, with Singapore's Health Sciences Authority removing 3,300 e-commerce listings for illegal health products, signaling stricter oversight that may favor established brands with robust compliance systems. The channel transformation creates opportunities for brands that can effectively navigate digital marketing, influencer partnerships, and platform-specific requirements while maintaining product authenticity and regulatory compliance across diverse APAC markets.

Geography Analysis

China's commanding 37.55% market share in 2025 reflects its massive consumer base and sophisticated beauty culture, yet the market faces headwinds from economic uncertainty and intensifying competition from domestic brands that now hold approximately 60% of the mass and masstige segments. The Chinese market's maturity is evident in consumer sophistication regarding ingredient awareness and brand authenticity. However, regulatory complexity under the National Medical Products Administration (NMPA) requires significant compliance investments, with new online supervision measures for cosmetics marketing adding operational complexity for both domestic and international brands. India emerges as the fastest-growing geography with 6.48% CAGR through 2031, driven by rising disposable incomes, urbanization, and increasing beauty consciousness among younger demographics. The market's growth potential is supported by rapid e-commerce adoption, with platforms like Nykaa and Purplle establishing strong positions in beauty retail while traditional channels maintain relevance in tier-2 and tier-3 cities.

Japan represents a mature but innovative market where consumer preferences are shifting toward natural ingredients and sustainable packaging, creating opportunities for brands that can combine traditional Japanese beauty philosophies with modern formulation science. Japanese companies like Shiseido, Kao, and Kosé are expanding internationally while investing heavily in domestic R&D capabilities, with Shiseido's new Ibaraki plant representing a EUR 400 million investment in high-automation manufacturing that exports 70% of production. Australia and New Zealand represent environmentally conscious markets where sustainability credentials significantly influence consumer purchasing decisions, creating competitive advantages for brands that can demonstrate authentic environmental commitments. South Korea's influence extends far beyond its domestic market size through the global K-beauty phenomenon, with companies like Amorepacific and LG H&H driving innovation in formulation science and digital marketing strategies.

Thailand's projected 11% growth in 2025 reflects strong domestic demand and the emergence of "T-beauty" brands that combine traditional Thai ingredients with modern formulation techniques. Singapore's USD 1.244 billion beauty and personal care market demonstrates high consumer sophistication and strong preference for premium products, with pharmacy chains accounting for approximately 80% of market share while rapidly expanding brand assortments. The market's hot, humid climate creates specific consumer needs for oil control and hydration products, while the population's high digital adoption rate supports e-commerce growth projected to reach a significant amount by 2027. The market's openness to international brands combined with high consumer spending power creates opportunities for premium products that can demonstrate superior quality and safety profiles while meeting specific climate-related consumer needs.

Competitive Landscape

The Asia-Pacific body care market's moderate fragmentation creates a dynamic competitive environment where established multinational brands compete alongside emerging local players and specialized niche brands. Market leaders like Unilever, Procter & Gamble, and Kao Corporation leverage global scale and R&D capabilities while adapting to local preferences yet face increasing pressure from domestic brands that better understand regional consumer nuances and can respond more quickly to market trends.

The competitive intensity is particularly pronounced in digital channels, where platform dominance by companies like Shopee creates new gatekeepers that influence brand visibility and consumer access. Opportunities exist in specialized segments like pH-balanced formulations, sustainable packaging, and age-specific products, where consumer demand is growing faster than established players can adapt their product portfolios. Technology adoption is becoming a key differentiator, with companies investing in advanced formulation science, sustainable packaging innovations, and digital marketing capabilities to maintain competitive positions.

Kao Corporation's recognition as one of the World's Most Ethical Companies for 19 consecutive years demonstrates how ESG credentials are becoming competitive advantages in markets where consumer values increasingly influence purchasing decisions. The regulatory landscape creates both barriers and opportunities, with companies that can navigate complex compliance requirements across multiple ASEAN markets gaining advantages over smaller competitors lacking regulatory expertise. However, enforcement actions like Korea's sanctions against 14 companies for cosmetics law violations highlight how regulatory compliance has become a critical operational requirement rather than a competitive differentiator.

Asia-Pacific Bath and Shower Products Industry Leaders

-

Unilever

-

L'Oréal S.A.

-

Procter & Gamble

-

Johnson & Johnson

-

Colgate-Palmolive Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sanrio teamed up with one of Japan's top facial care products to release a range of products in limited-edition packaging. "DETclear" is a well-known exfoliating product in Japan. The product was a gentle peeling gel designed to remove old, dead skin cells. It was formulated with fruit-derived AHA and plant-derived BHA to gently soften and lift away impurities. Sanrio also teamed up with Korean cosmetics brand CNP Laboratory to release another range of themed skincare.

- July 2025: Dove set a new benchmark in everyday cleansing with the launch of its innovation — the Dove Serum Bar. The Dove Serum Bar helped repair skin damage, giving visibly healthy, nourished skin. The Serum Bar featured plant-based cleansers, a minimalist and sustainable format, and a gentle formula suited for normal to dry and sensitive skin types.

- July 2025: Kao Corporation launched new products under its Sensai, Kanebo, and Curél brands to accelerate global expansion and solidify market positions. The company used ingredients that mimicked babies' skin protection in the womb, and ingredient synergies for deep cleansing and moisturizing.

Asia-Pacific Bath and Shower Products Market Report Scope

Bath and shower products refer to personal care products that help clean, exfoliate, and moisten the body.

The Asia-Pacific bath and shower products market is segmented by type, distribution channel, and geography. Based on the type, the market is segmented into shower cream/gel, bar soap, shower oil, and other types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online stores, specialty retail stores, and other distribution channels. Based on geography, the market is segmented into China, India, Japan, Australia, and the Rest of Asia Pacific.

The report offers the market size and forecasts in value (USD million) for the above segments.

By Product Type

| Bar Soap |

| Body Wash/ShowerGel |

| Other Product Types |

By Category

| Conventional |

| Organic |

By End-User

| Kids/Children |

| Adult |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| Australia |

| New Zealand |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Bar Soap |

| Body Wash/ShowerGel | |

| Other Product Types | |

| By Category | Conventional |

| Organic | |

| By End-User | Kids/Children |

| Adult | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What makes the Asia-Pacific body care market attractive for investment?

The market combines strong fundamentals (5.67% CAGR, USD 21.46 billion by 2031) with structural growth drivers including rapid digitalization, rising disposable incomes, and increasing consumer sophistication.

Which product categories offer the highest growth potential?

Body wash/shower gel products lead both in market share (34.22%) and growth rate (5.74% CAGR), driven by consumer preference for liquid formulations that accommodate advanced ingredients like pH-balancing and moisturizing compounds.

What role does e-commerce play in market growth?

Digital channels are transforming the market despite starting from a smaller base, with online retail achieving 6.05% CAGR.

Which geographic markets offer the best expansion opportunities?

India presents the strongest growth opportunity at 6.48% CAGR, driven by rising incomes and digital adoption.

Page last updated on: