Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 6.80 Billion |

| Market Size (2030) | USD 9.19 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

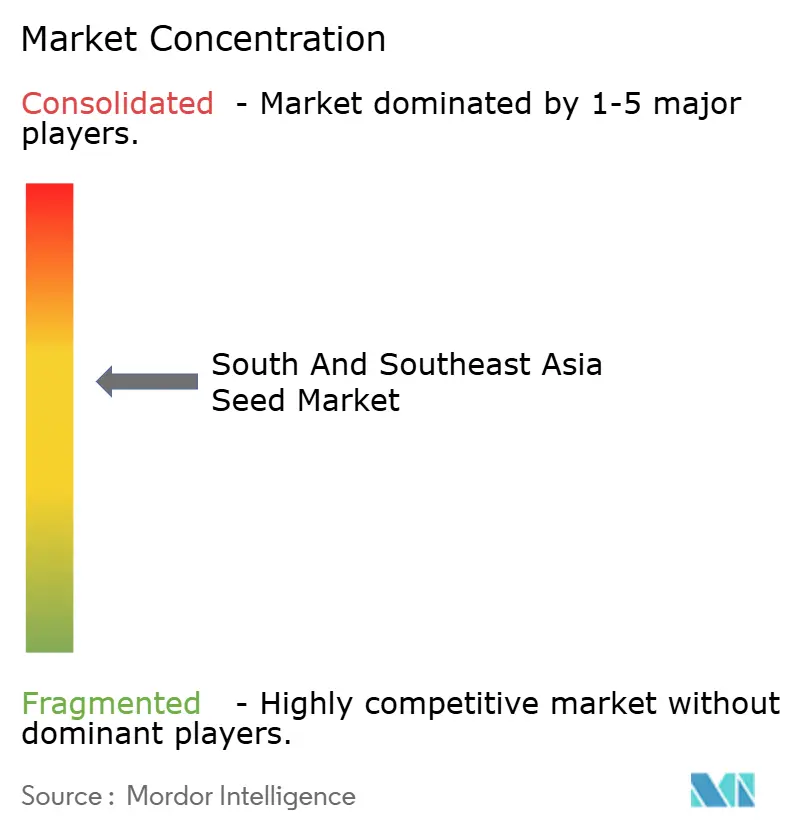

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South And Southeast Asia Seed Market Analysis by Mordor Intelligence

The South and Southeast Asia seed market size reached USD 6.80 billion in 2025 and is projected to expand to USD 9.19 billion by 2030, advancing at a 6.2% CAGR during the forecast period. Robust growth is fueled by sustained government subsidies for climate‐resilient hybrids, rapid urbanization that lifts demand for uniform fresh produce, and steady technology upgrades in seed packaging and delivery. Hybrid penetration rose sharply in rice, maize, and key vegetable crops as subsidy programs shaved 30%–50% off seed costs for smallholders. Retail consolidation across India, Thailand, and the Philippines stimulated near-continuous vegetable seed turnover because supermarket chains now contract farmers for specific varieties with tight color and size specifications. Parallel innovations, such as bamboo bio-capsule packs that cut moisture ingress by 85% and drone-guided seed placement that achieves 95% accuracy, are raising overall seed use efficiency. Together, these factors tighten links between plant genetics and supply-chain performance, reinforcing a virtuous cycle of productivity gains and higher input spend across the region.

Key Report Takeaways

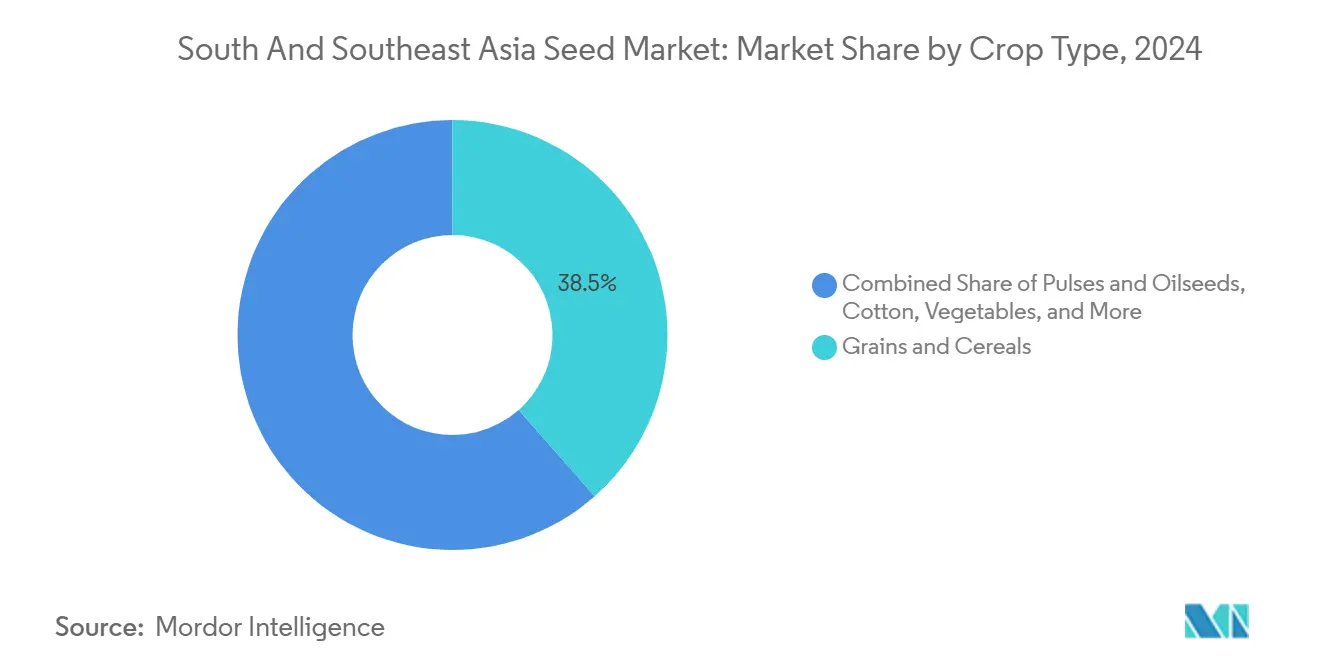

- By crop type, grains and cereals led with 38.5% revenue share of the South and Southeast Asia seed market in 2024, while vegetables are forecast to post the fastest 8.6% CAGR through 2030.

- By product type, non-GM hybrids accounted for 52.1% of the South and Southeast Asia seed market share in 2024, while GM seeds are anticipated to advance at an 11.4% CAGR through 2030.

- By geography, India commanded 44.3% of the South and Southeast Asia seed market size in 2024, whereas Vietnam is projected to register the highest CAGR of 9.8% between 2025 and 2030.

- By company concentration, the top five suppliers, including Bayer AG, Syngenta Group, East-West Seed International B.V., Advanta Seeds International (UPL Limited), and Nuziveedu Seeds Limited, controlled a majority share of the South and Southeast Asia seed market in 2024, with Bayer AG holding the largest single share.

South And Southeast Asia Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies Drive Climate-Resilient Hybrid Adoption | +1.8% | India, Bangladesh, Pakistan, Thailand | Medium term (2–4 years) |

| Organized Retail Networks Reshape Vegetable Seed Demand | +1.2% | Asia-Pacific core, spill-over to urban centers | Short term (≤ 2 years) |

| Technology Innovations Enable Precision Seed Delivery | +1.0% | ASEAN markets, India metro regions | Medium term (2–4 years) |

| Rapid Vegetable Seed Replacement in Peri-Urban Farming | +0.8% | Tropical Myanmar, Indonesia, and coastal belts | Long term (≥ 4 years) |

| Carbon-Credit Financed Regenerative Seed Programs | +0.6% | Thailand, Vietnam, and pilot projects in India | Long term (≥ 4 years) |

| Drone-Based Direct Seeding Bundles Proprietary Varieties | +0.7% | Precision farming clusters across Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies Drive Climate-Resilient Hybrid Adoption

Subsidy programs are a cornerstone of the South and Southeast Asia seed market. India’s Pradhan Mantri Krishi Sinchai Yojana allocated INR 1 trillion (USD 12.0 billion) in 2024, channeling 40% to drought-tolerant seed distribution[1]Source: Ministry of Agriculture, India, “Pradhan Mantri Krishi Sinchai Yojana Annual Report 2024,” AGRICOOP.NIC.IN. Bangladesh pushed hybrid rice coverage to 2 million farmers and logged yield jumps of 12% across target districts[2]Source: Bangladesh Ministry of Agriculture, “Hybrid Rice Program Impact Assessment 2024,” MOA.GOV.BD . Thailand scaled its Royal Initiative Program to 500,000 growers focused on flood-resistant paddy lines[3]Source: Thailand Board of Investment, “Agricultural Sector Investment Report 2024,” BOI.GO.TH . These campaigns lower adoption risk for smallholders, embed new varietal preferences, and sustain demand even after incentives sunset. As a result, hybrid seed replacement rates in subsidized zones surpassed 80% in 2025, underlining subsidy efficacy in shaping the South and Southeast Asia seed market.

Organized Retail Networks Reshape Vegetable Seed Demand

Modern retail chains expanded floor space and sourcing power across the Association of Southeast Asian Nations (ASEAN) capitals. Big C in Thailand and SM Markets in the Philippines now procure 70% of their fresh produce through contract farming, which requires cultivar specificity and year-round supply. That shift accelerated vegetable seed turnover to 95% of cultivated area in peri-urban belts compared with 60% in traditional wet markets. East-West Seed International B.V. capitalized on the surge by tailoring its tomato, chili, and cucumber lines to meet retailer protocols, achieving 18% revenue growth in 2024. These patterns establish predictable sales cycles in the South and Southeast Asian seed market, while enabling premium pricing for performance traits such as shelf-life extension.

Technology Innovations Enable Precision Seed Delivery

Moisture-barrier bamboo bio-capsules cut post-harvest seed damage by 85% in tropical climates, extending shelf life from four to nine months. Drone-guided seeding, validated in Vietnamese rice paddies, achieves 95% placement accuracy and integrates proprietary hybrid packages tied to service contracts. Bayer’s 2024 partnership with Source.ag layered blockchain traceability on top of these systems to authenticate origin and combat counterfeit trade, an issue that costs growers USD 400 million annually. SeedChain, a Vietnamese startup, has secured USD 3.2 million to scale a similar ledger platform across the Association of Southeast Asian Nations (ASEAN) and reduce farmers' exposure to fake seeds. These technologies strengthen intellectual property defenses and boost the functional value proposition of certified seed in the South and Southeast Asia seed market.

Rapid Vegetable Seed Replacement in Peri-Urban Farming

Peri-urban farms near Bangkok, Ho Chi Minh City, and Bengaluru supply high-frequency fresh produce to urban supermarkets. Quick crop cycles and penalty clauses for grade deviations compel growers to adopt new seed lots each season. Replacement rates hit 95% in leafy greens and 90% in solanaceous crops in 2024, dwarfing remote rural averages. Contract farming frameworks guarantee offtake, mitigating market risk, and energizing hybrid seed uptake. This trend spreads outward as logistics improvements expand urban catchments, enlarging the addressable base of the South and Southeast Asia seed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Informal Seed Networks Limit Commercial Penetration | -1.5% | Remote rural belts across Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Bottlenecks Constrain GM Seed Rollout | -1.2% | India, Indonesia, Thailand | Medium term (2–4 years) |

| Microplastic Regulations Challenge Seed Film-Coatings | -0.8% | Export-oriented supply chains | Medium term (2–4 years) |

| Cross-Border Counterfeit Seed Proliferation | -0.6% | Online marketplaces in ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Informal Seed Networks Limit Commercial Penetration

Around 65% of smallholders still rely on saved or exchanged seed, especially in rice paddies where heritage varieties carry cultural weight. Saving seed eliminates upfront cost, which remains decisive for farmers earning less than USD 2,000 per year. Community seed banks support varietal diversity yet impede rapid hybrid adoption. Yield gaps of 20%–30% relative to contemporary hybrids persist, but value perception hinges on trusted demonstration plots and localized extension. Until extension density improves, informal practice will keep a lid on addressable demand within the South and Southeast Asia seed market.

Regulatory Bottlenecks Constrain GM Seed Rollout

Biosafety evaluation cycles span 3–7 years in India, Indonesia, and Thailand. Indonesia’s moratorium on new GM crops since 2019 has blocked drought-tolerant maize release. Thailand’s cautious stance limited farmer access to biotech insect-resistant cotton despite rising pest pressure. India requires central and state sign-offs that extend timelines by another two to three years. Such delays raise development costs and deter private research and development, slowing GM seed’s penetration in the South and Southeast Asia seed market despite proven yield and sustainability paybacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Grains Anchor Value as Vegetables Accelerate

Grains and cereals accounted for 38.5% of the South and Southeast Asia seed market in 2024, driven by strong demand for rice and maize in India, Vietnam, and the Philippines. The South and Southeast Asia seed market size for grains and cereals is anticipated to expand at a significant CAGR, driven by the adoption of mechanization-ready hybrids and favorable bioethanol policy tailwinds. Rice hybrid adoption surpassed 2.3 million farmers in Bangladesh and Vietnam, while Thailand and the Philippines raised maize hybrid use by 12% to meet feed needs. Pulses and oilseeds deliver steady 7.9% growth as India scales nutrition initiatives that boost chickpea and lentil acreage. Specialty crops, such as dragon fruit in Vietnam and durian in Thailand, exhibit double-digit demand upswings, signaling diversification opportunities for breeders.

Vegetables represent the fastest-growing segment and are forecast to log an 8.6% CAGR through 2030, powered by organized retail and dietary shifts toward fresh produce. Leafy greens, tomato, and chili hybrids dominate, but emerging demand for colored capsicum, baby corn, and zucchini reflects palate diversification in metro areas. Replacement cycles approach one season in hydroponic setups, multiplying seed sales frequency. Vegetable growers benefit from premium price realization, crowding investment toward disease-resistant and long-haul transport varieties. These dynamics reinforce vegetables as the primary accelerator of value within the South and Southeast Asia seed market.

By Product Type: Hybrids Maintain Lead as GM Traits Gain Traction

Non-GM hybrids held a 52.1% share of the South and Southeast Asia seed market in 2024, driven by established regulatory clarity and broad farmer familiarity. Performance traits like drought tolerance and uniform maturation encourage continuous hybrid upgrade cycles among commercial grain growers. Varietal and open-pollinated seed retained a significant share, mainly within organic and self-sufficient systems that prioritize seed saving over input spending. Still, rising labor costs are pushing even smallholders toward hybrid maize and rice due to their shorter crop durations.

GM seeds, although only a fraction of the current volume, are projected to post the segment’s fastest 11.4% CAGR to 2030. The Philippines approved Golden Rice in 2024, opening a new front for biofortified crops. Bangladesh expanded Bt brinjal to 50,000 growers, citing a 30% yield increase and an 80% reduction in pesticide use. India’s Bt cotton remained a mainstay on more than 12 million hectares, while Indonesia and Thailand continued to evaluate biotech adoption frameworks. The South and Southeast Asia seed market size attributable to GM traits could double by 2030 if regulatory pipelines accelerate and trait royalties remain farmer-friendly.

Geography Analysis

India underpins the regional scale with a 44.3% share of the South and Southeast Asia seed market in 2024, driven by extensive hybrid portfolios and government subsidy granularity. Seed replacement rates reached 45% in rice and 85% in maize, increasing in tandem with the adoption of mechanization and contract farming. Bayer AG expanded its Dekalb corn research and development hub in Hyderabad, and Syngenta Group released climate-smart vegetable lines adapted to high‐temperature zones. Domestic champions Nuziveedu Seeds Limited and Kaveri Seed Company Limited plowed more than USD 150 million into cotton and rice breeding in 2024. These investments solidify India's position as both a consumption and innovation hub within the South and Southeast Asian seed market.

Southeast Asian markets deliver the highest incremental growth. Vietnam is forecasted to grow at a 9.8% CAGR, driven by 75% hybrid rice coverage and a strategic export drive for fruits and vegetables. Thailand leverages its well-oiled export logistics, recording seed export revenues of USD 280 million in 2024 and targeting premium vegetable lines for Japanese and European buyers. The Philippines accelerates GM adoption with three new biotech approvals in 2024, broadening trait diversity and boosting grower margins. Indonesia, despite hosting 47 million hectares of farmland, remains underpenetrated at sub-30% hybrid use, offering latent upside once biosafety regulations are clarified and distribution grids are densified.

Bangladesh and Pakistan occupy the middle tiers in terms of size yet exhibit distinct trajectories. Bangladesh is riding a hybrid rice and vegetable momentum, clocking significant annual growth even as it confronts rising saline intrusion along its coastal croplands. Pakistan’s 10.4% share is tempered by currency volatility and import curbs that slow access to novel genetics. Myanmar rounds out the regional picture as an emerging frontier, anticipated to benefit from ongoing agrarian reforms and donor-backed input subsidies; however, political headwinds may impede the full realization of the market potential.

Competitive Landscape

The South and Southeast Asia seed market is moderately concentrated, with the top five players accounting for a collective share of 47.8%. Bayer AG leads with differentiators through digitized traceability partnerships and multistack trait integration. Syngenta Group ranks second at 11.8% and refocused on core breeding after divesting FarMore seed treatment technology to Gowan SeedTech for USD 150 million in December 2024, a move designed to streamline research and development spend toward vegetable and specialty crop pipelines.

East-West Seed International B.V., although regionally focused, wields deep breeder–farmer linkages and commands a sizable vegetable share across Thailand, Vietnam, and the Philippines. The company raised USD 25 million in Series C funding in November 2024 to extend climate-resilient breeding infrastructure. Domestic firms, such as Nuziveedu Seeds Limited and Kaveri Seed Company Limited, defend their strongholds in India for cotton and rice through localized germplasm and extensive dealer networks. Agritech newcomers deploy AI breeding algorithms that claim to trim development cycles by two years, positioning them as future disruptors within the South and Southeast Asia seed market.

Cross-licensing and public–private partnerships proliferate as firms chase accelerated trait deployment. Advanta Seeds International (UPL Limited) sealed a joint venture with Indonesian state-owned PT Sang Hyang Seri in September 2024 to build locally adapted hybrid rice destined for two million hectares of paddy land. Such collaborations offer regulatory muscle and route-to-market leverage, imperative in jurisdictions with multi-layer approval gates. Overall, the competitive narrative reflects parallel developments in genetics, digital enablement, and farmer services that collectively accelerate the innovation tempo of the South and Southeast Asia seed market.

South And Southeast Asia Seed Industry Leaders

East-West Seed International B.V.

Nuziveedu Seeds Limited

Advanta Seeds International (UPL Limited)

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bayer CropScience introduced Vyconic soybean in Thailand, combining pest resistance and blockchain traceability for an initial 150,000-hectare rollout that targets USD 45 million revenue by 2027.

- November 2024: Nuziveedu Seeds has launched NP-8912, a new paddy variety that combines high yield potential with early maturity. Featuring strong disease resistance and wide adaptability.

- May 2023: Bangladesh’s National Committee on Biosafety (NCB) approved the field release of two Bt cotton hybrids, JKCH 1947 Bt and JKCH 1050 Bt.

South And Southeast Asia Seed Market Report Scope

A seed is the ripened fertilized ovule of a flowering plant containing an embryo and is generally capable of germination to produce a new plant. For this report, seeds have been defined as seeds for sowing at the farmer level. In this report, market sizing has been done at the farmer's level. The report provides an in-depth analysis of various parameters of the seeds market. The South and Southeast Asian seeds market is segmented by crop type (grains and cereals, pulses and oilseeds, cotton, vegetables, and other seeds), product type (non-GM/hybrid seeds, GM seeds, varietal seeds, and plant growth regulators), and geography (Bangladesh, Pakistan, India, Nepal, Vietnam, Indonesia, Thailand, Myanmar, Malaysia, Philippines, and Rest of South and Southeast Asia). The report offers market size and forecasts for the seed industry in volume (Metric Ton) and in value (USD).

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Cotton |

| Vegetables |

| Other Seeds |

By Product Type

| Non-GM Hybrid Seeds |

| GM Seeds |

| Varietal/Open-Pollinated Seeds |

By Geography

| Bangladesh |

| Pakistan |

| India |

| Nepal |

| Vietnam |

| Indonesia |

| Thailand |

| Myanmar |

| Philippines |

| Rest of South and South East Asia |

| By Crop Type | Grains and Cereals |

| Pulses and Oilseeds | |

| Cotton | |

| Vegetables | |

| Other Seeds | |

| By Product Type | Non-GM Hybrid Seeds |

| GM Seeds | |

| Varietal/Open-Pollinated Seeds | |

| By Geography | Bangladesh |

| Pakistan | |

| India | |

| Nepal | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Myanmar | |

| Philippines | |

| Rest of South and South East Asia |

Key Questions Answered in the Report

How large is the South and Southeast Asia seed market in 2025?

The market is valued at USD 6.80 billion in 2025 with a projected rise to USD 9.19 billion by 2030 at a 6.2% CAGR.

Which country leads regional seed sales?

India commands 44.3% of total revenues due to expansive hybrid adoption programs and a mature domestic seed sector.

What crop segment is growing fastest in the region?

Vegetable seeds are set to post an 8.6% CAGR through 2030, outpacing grains and other segments as urban diets shift toward fresh produce.

Are GM seeds widely adopted in South and Southeast Asia?

Adoption is uneven, with the Philippines and Bangladesh advance quickest, while Indonesia and Thailand maintain restrictive approval processes.

Page last updated on: