Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

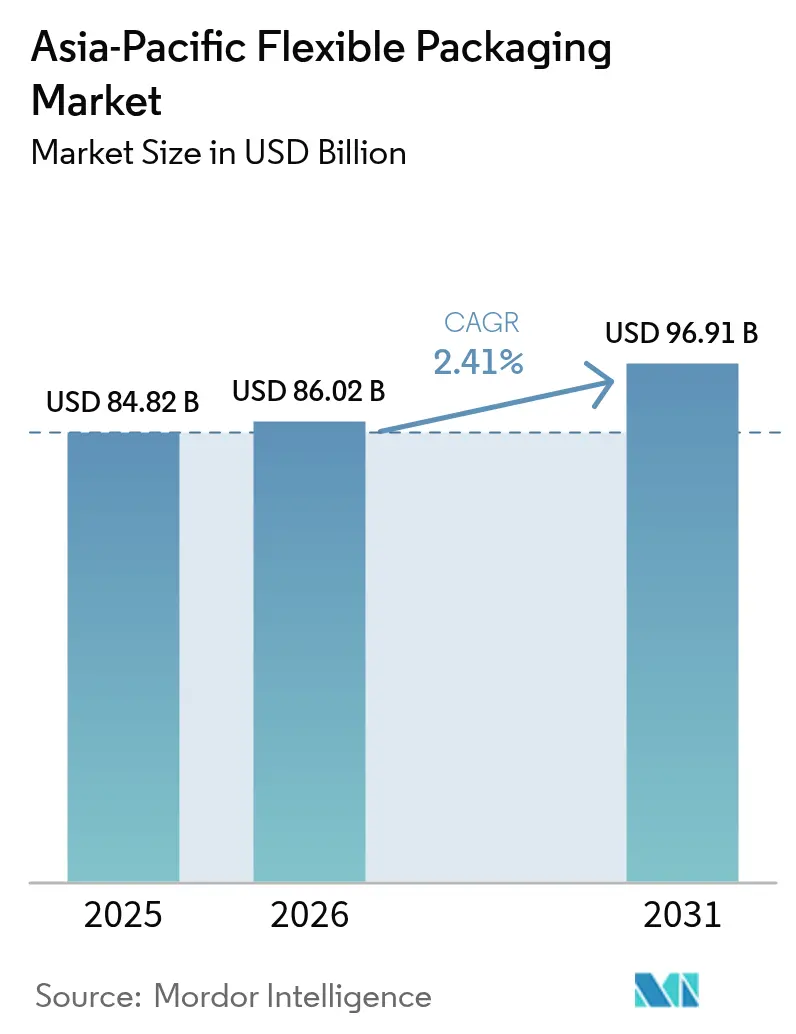

| Base Year Market Size (2025) | USD 84.82 Billion |

| Market Size (2026) | USD 86.02 Billion |

| Market Size (2031) | USD 96.91 Billion |

| Growth Rate (2026 - 2031) | 2.41% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Flexible Packaging Market Analysis by Mordor Intelligence

The Asia-Pacific flexible packaging market size is expected to increase from USD 84.82 billion in 2025 to USD 86.02 billion in 2026 and reach USD 96.91 billion by 2031, growing at a CAGR of 2.41% over 2026-2031. Plastics remained the dominant substrate in 2025, yet the mono-material pivot and digital-printing build-out are changing converter cost structures. Accelerating e-commerce shipments, cold-chain rollouts in Southeast Asia, and brand-owner sustainability pledges are boosting demand for lightweight, high-barrier formats that trim logistics costs and curb food waste. Regional regulations, from Japan’s positive list for food-contact additives to Australia’s 50% recycled-content target, are driving reformulation of legacy laminates, favoring plants with in-house recycling and solvent-free adhesive lines. Multinationals are expanding capacity in China and India, while regional specialists invest in chemical recycling alliances to secure food-grade recyclate, preserving margins despite resin volatility. The Asia-Pacific flexible packaging market continues to reward converters that can combine quick-turn digital presses, robust compliance systems, and access to traceable recyclate streams.

Key Report Takeaways

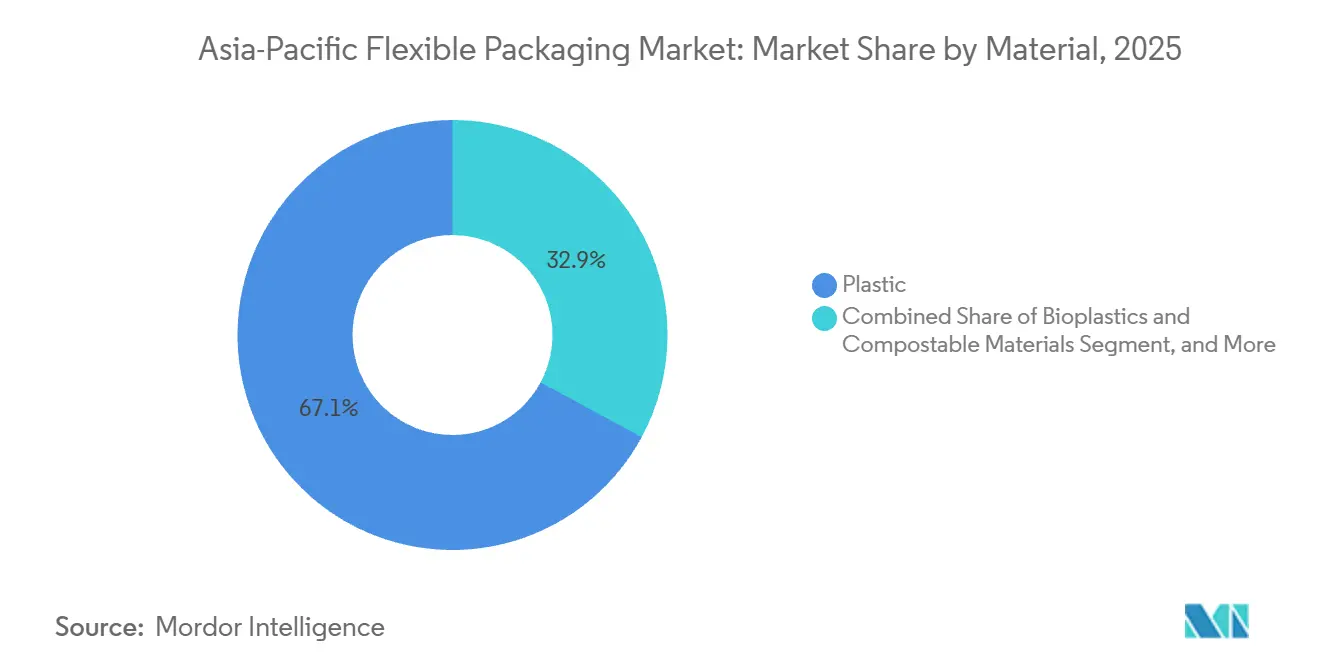

- By material, plastics captured 67.12% of the Asia-Pacific flexible packaging market share in 2025. Whereas, bioplastics and compostable substrates are projected to expand at a 4.12% CAGR through 2031.

- By product type, bags and pouches led with 48.63% market share in 2025, whereas sachets and stick packs are forecast to grow at a 3.54% CAGR over 2026-2031.

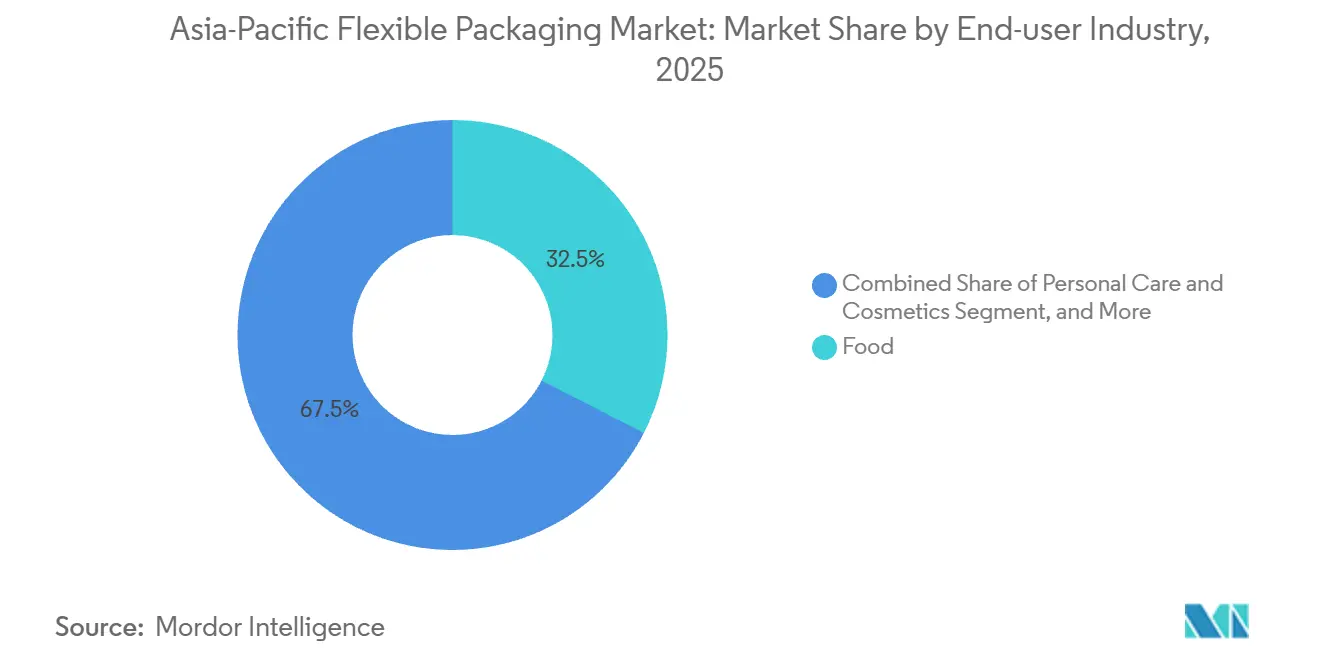

- By end-user, food accounted for 32.53% of the Asia-Pacific flexible packaging market size in 2025, while personal care and cosmetics are advancing at a 3.86% CAGR to 2031.

- By printing technology, flexography held 44.72% share of the Asia-Pacific flexible packaging market size in 2025, and digital printing is rising at a 3.79% CAGR through 2031.

- By geography, China commanded 28.12% of the Asia-Pacific flexible packaging market share in 2025; India is expected to expand at a 4.23% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Demand for Convenient Packaging | +0.8% | China, India, and Southeast Asia urban centers | Medium term (2-4 years) |

| Demand for Longer Shelf Life and Innovative Packaging | +0.7% | Core Asia-Pacific, exports to Middle East and Africa | Medium term (2-4 years) |

| Growing E-Commerce Penetration for Packaged Goods | +0.9% | China, India, Indonesia, Vietnam, Thailand | Short term (≤ 2 years) |

| Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates | +0.6% | Japan, Australia, Singapore, India | Long term (≥ 4 years) |

| Surge in Cold Chain Expansion for Fresh Produce Exports in Southeast Asia | +0.5% | Thailand, Vietnam, Indonesia | Medium term (2-4 years) |

| Brand Owner Shift Toward Digital Printing for Short-Run Personalization | +0.4% | China, India, Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Demand for Convenient Packaging

Single-serve and resealable designs are replacing rigid containers because they cut food waste and match on-the-go lifestyles in congested cities. Sachet retail value climbed to USD 98.4 billion in 2026, with India, Vietnam, and Indonesia contributing more than half of new volume. Beauty and hair-care applications dominate the format, but pharmaceuticals and beverages are adding scale as converters install quad-seal and doy-pack lines capable of 200-300 pouches a minute. Unit costs of USD 0.02-0.04 for plain PE keep margins slim, yet sachets remain pivotal in low-income markets where a 5 ml hair-oil pouch retails for USD 0.12. Rising middle-class incomes are also lifting demand for resealable stand-up pouches that extend freshness after first opening. Convenience, therefore, is both a volume and a value play in the Asia-Pacific flexible packaging market.

Demand for Longer Shelf Life and Innovative Packaging

High-barrier films using EVOH, PVDC, or aluminum foil now support extended cold-chain corridors across Southeast Asia. China consumed 88 million tonnes of meat in 2024, while India exported seafood worth USD 8.09 billion, prompting processors to adopt vacuum-skin and modified-atmosphere packs that add 10-14 days of shelf life.[1]Marine Products Export Development Authority, “Seafood Export Statistics FY2023-24,” mpeda.gov.in Premium technologies such as Sealed Air’s OptiDure are spreading as exporters face transit legs of 1,000-1,500 km. Academic trials showed bio-based polybutylene succinate films with halloysite nanotubes preserved produce an extra week at room temperature, signaling latent demand for compostable yet high-barrier options. Although these structures cost 40-50% more than standard layers, premium brands in Japan and South Korea pay for the extended protection, validating the strategy for converters that can blend barrier science with sustainability signaling.

Growing E-Commerce Penetration for Packaged Goods

The Asian Development Bank calculated that regional e-commerce plastic packaging doubled to 4.5 billion pounds in 2025, expanding far faster than the overall Asia-Pacific flexible packaging market.[2]Asian Development Bank, “E-Commerce Packaging in Asia-Pacific: Trends and Challenges,” adb.orgProtective mailers account for 35% of this volume, with stand-up pouches accounting for 31%. China’s parcel-packaging standard requires 90% recyclability or reusability by 2025, while South Korea bans multilayer combinations in online mailers, forcing converters to manage divergent SKUs and raising inventory costs. Parcel damage rates remain a pain point, so thicker mono-PE mailers are gaining share, even as extended producer responsibility fees rise. Online grocery growth is particularly strong in India and Indonesia, where chilled fulfillment drives demand for insulated pouches lined with recyclable BOPE.

Adoption of Mono-Material Flexible Packaging to Meet Recycling Mandates

Japan’s positive list for food-contact substances, effective June 2025, prohibits many legacy adhesives and inks. Australia targets 50% recycled content by 2030, yet kerbside recovery of flexible plastics is below 1%. China’s recycled-plastic traceability rule, active February 2026, establishes a 0.5% contamination ceiling. Converters, therefore, accelerate investment in solvent-free laminators, PE-PE or PP-PP barrier films, and chemical-recycling tie-ups to secure food-grade outputs priced 25-35% above virgin resin. Brands accept the premium only when supply is certified and stable, creating a moat for converters with captive recycling or advantaged offtake contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns About Environmental Impact and Recycling of Plastic Packaging | -0.5% | Japan, Australia, Singapore, India, global spillover | Long term (≥ 4 years) |

| Volatility in Raw Material Prices for Petrochemical Feedstocks | -0.4% | Asia-Pacific core, Middle East and Africa spillover | Short term (≤ 2 years) |

| Regulatory Restrictions on Multilayer Structures in Japan and Australia | -0.3% | Japan, Australia, possible uptake in South Korea, Singapore | Medium term (2-4 years) |

| Limited Food-Grade Recyclate Availability for Flexible Formats | -0.2% | Japan, Australia, India, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns About Environmental Impact and Recycling of Plastic Packaging

Public frustration with single-use plastics is mounting, yet recycling infrastructure for flexible formats lags behind that for rigid counterparts by several years. Kerbside recovery of flexible films sits below 1% in Australia, contrasting with 35-40% for PET bottles. Singapore’s mandatory reporting scheme ties producer fees to unrecycled tonnage, adding 3-5% to converter costs. India’s 2024 EPR revision compels the retrieval of 60% of post-consumer flexible films by 2026, even though collection capacity covers fewer than 20% of municipalities. These mismatches raise compliance risks and encourage brand owners to trim laminate layers or pivot to certified compostable films, even when shelf-life trade-offs persist.

Volatility in Raw Material Prices for Petrochemical Feedstocks

PE, PP, and PET swung 15-20% during 2024-2025 on crude fluctuations and cracker outages. HDPE CFR China eased to USD 1,050 per tonne in January 2025, while LDPE lingered near USD 1,100. BOPP film traded around USD 1,500 per tonne during Q4 2024. Such moves chip 200-300 basis points from converter margins when resin surges outpace contract pass-through. Long-term supply agreements cushion large incumbents, but smaller players exposed to spot markets face cash-flow strain, elevating consolidation prospects in the Asia-Pacific flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Challenge Conventional Resin Dominance

Plastics retained 67.12% of the Asia-Pacific flexible packaging market size in 2025, led by polyethylene, BOPP, and cast PP, which supply snack, noodle, and detergent pouches. Metal foil sticks to niche medical and confectionery wraps, while paper controls mid-single-digit share through kraft-lined coffee and pet-food bags. Bioplastics, though small, are growing at a 4.12% CAGR as Japanese and South Korean shoppers are willing to pay 10-15% more for TÜV-certified home-compostable packs. Converters wrestle with resin cost gaps: PLA sells for roughly USD 2,700 per tonne, compared with USD 1,100 for PE, but corporate carbon targets and EPR fees tilt the calculus. China’s traceability standard for recycled plastics, arriving in 2026, accelerates the adoption of mono-PE laminations that deliver an acceptable barrier while aligning with mechanical-recycling loops.

Paper-flexible hybrids, such as Mondi-Parkside peelable PE-lined pouches, broaden options for dry groceries yet still struggle with high-fat or high-moisture goods. Metalized films protect confectionery freshness when oxygen transmission limits fall below 0.1 cc/m²/24 h. Industrial composting shortfalls remain a drag on bioplastic growth, as only about 200 sites across Asia-Pacific meet the 58-60 °C composting benchmarks. Despite the hurdles, brands continue pilots to lock in reputational benefits, pushing the Asia-Pacific flexible packaging market toward a richer materials mix.

By Product Type: Sachets Gain Share in Personal Care

Bags and pouches dominated with 48.63% of Asia-Pacific flexible packaging market share in 2025, buoyed by stand-up versions that slim logistics costs up to 50% versus rigid jars. Sachets and stick packs, however, are accelerating at a 3.54% CAGR through 2031 as single-use shampoo, serums, and electrolyte powders fit trial-size and subscription models. Films and wraps guard pallet loads and produce crates, yet confront reusable tote uptake in e-commerce hubs. Quad-seal pouches, prized for shelf impact, now permeate premium coffee and protein-powder aisles where margins can exceed 20%.

India exemplifies sachet utility; a 5 ml hair oil pouch at USD 0.12 ensures daily affordability. Southeast Asian beverage startups mimic the template using narrow stick packs that enhance dosing precision in collagen or vitamin shots. At the other end, recyclable BOPE stretch wrap, delivered through Dow’s INNATE TF 220 resin, improves puncture resistance by 30-40%, winning over logistics providers that previously defaulted to thicker BOPP. Lidding films are evolving toward mono-PP seals for yogurt, but must still achieve peel strengths near 3 N/15 mm to satisfy fillers.

By End-User Industry: Personal Care Outpaces Food

Food accounted for 32.53% of the Asia-Pacific flexible packaging market in 2025, spanning snacks, baked goods, and chilled meat. Growth, though positive, slows as penetration saturates in Japan and Australia. Personal care and cosmetics, instead, are growing at a 3.86% CAGR, with refill pouches for body wash and shampoo, especially in urban China, where consumers accept a 10-15% markup for low-waste packs. Beverage flexible formats hold mid-teen share thanks to aseptic juice and dairy pouches that rely on foil-lined laminates to keep oxygen below 0.5 cc/m²/24 h.

Pharmaceutical demand rises on India’s export boom and Japanese aging demographics, favouring blister and sterile pouches that now tap Constantia’s mono-PE Flexible Blister. Agriculture sits in the residual bucket yet shows promise as agrochemical firms pivot from woven HDPE sacks to multi-layer PE-PA-EVOH pouches that cut leakage and lower shipping mass by 35%. Across categories, refill culture, e-commerce portioning, and the rise of cold-chain corridors collectively sustain volume in the Asia-Pacific flexible packaging market.

By Printing Technology: Digital Gains on Short Runs

Flexography led the Asia-Pacific flexible packaging market with 44.72% of the market share in 2025, balancing speeds around 400 m/min with plate costs near USD 250 each. Rotogravure follows for million-unit snack runs where image fidelity and 0.1 mm registration matter, despite cylinder fees of USD 5,000-8,000 per color. Digital presses are set for a 3.79% CAGR as FMCG brands test regional flavors or seasonal graphics in lots of fewer than 1,000 units.

HP Indigo and Konica Minolta installations in China and India reduce setup expense to USD 200-300 per design, slashing lead times from 8-12 weeks to 2-3 weeks. Ink cost hurdles remain USD 0.10/m² versus USD 0.03 for flexo, but data-driven personalization and e-commerce unboxing aesthetics keep demand buoyant. Water-based flexo inks are gaining traction in Japan and South Korea to meet VOC caps, though slower drying times are nudging converters toward higher-temperature driers, adding CapEx and increasing electricity load.

Geography Analysis

China held 28.12% of the Asia-Pacific flexible packaging market share in 2025, anchored by the world’s largest e-commerce ecosystem and strict recyclability rules that require 90% compliance with parcel packs by 2025.[3]State Administration for Market Regulation, “Standards for Recycled Plastics in Food Contact Applications,” samr.gov.cn Amcor’s USD 460 million investment in Changzhou signals confidence, even as macro softness dents near-term volumes. Cold-chain expansion for fresh produce and seafood, coupled with the rise of health snack startups, underscores the need for high-barrier, digitally printed pouches.

India advances at a 4.23% CAGR through 2031, propelled by 8-10% annual growth in packaged food processing and USD 25 billion in pharmaceutical exports. Uflex’s INR 13,224 crore (USD 1.59 billion) in revenue and its Poland holographic-film venture confirm its global ambition. EPR rules mandating 60% flexible collection by 2026, paired with nascent municipal pickup coverage, create both compliance strain and innovation opportunity.

Japan and Australia each hold high-single-digit shares, defined by rigorous food-contact laws and recycled-content targets. Japan’s positive list, in place since June 2025, is pushing converters toward solvent-less inks and adhesives. Australia’s 50% recycled-content mandate clashes with sub-1% kerbside film recovery, raising feedstock premiums that favor vertically integrated plants.

South Korea, with a mid-single-digit slice, pioneers digital printing for limited-run K-beauty launches and tough recyclability specs for e-commerce mailers. Rest of Asia-Pacific including Indonesia, Vietnam, Thailand, Malaysia, and the Philippines grows the fastest inside the bloc, courtesy of 6.1 million tonnes of cold-storage capacity that underpins exotic fruit exports sealed in EVOH pouches. The Economic Research Institute for ASEAN and East Asia foresees 12-14% annual cold-chain growth to 2028, ensuring robust downstream packaging pull.

Competitive Landscape

The Asia-Pacific flexible packaging market remains fragmented. Scale players deploy M&A to broaden their technology breadth; Sealed Air bought Liquibox for USD 1 billion in 2024 to add bag-in-box liquids, while Sonoco absorbed Eviosys for USD 3.9 billion, combining metal cans with pouches. Regional firms such as TCPL Packaging and Ester Industries carve niches by guaranteeing 15-20% shorter lead times and offering mono-PE structures already vetted for Japan’s and Australia’s EPR audits.

Digital printing differentiates mid-tier converters; sub-1,000-unit SKUs for e-commerce brands incur a setup outlay of USD 200 rather than USD 6,000 for rotogravure, enabling agile suppliers to capture premium margins. Constantia Flexibles’ mono-PE Flexible Blister gives pharmaceutical players a recyclable alternative just as Japan and Australia tighten multilayer rules. Aptar’s N-Sorb platform, accepted into the US FDA's Emerging Technology Program in 2024, positions the company to deliver nitrosamine-safe pill pouches coveted by Indian generics.

Feedstock hedging acts as a strategic moat. Large multinationals sign six-month PE contracts, softening resin spikes that erode small-converter EBITDA. Plants with captive solvent-free lamination and mechanical recycling loops earn higher returns because they meet recycled-content quotas and dodge external scrap shortages. Overall, competitive intensity is rising as e-commerce audits punish non-compliant suppliers, steering brands toward converters who blend regulatory fluency with fast-turn personalization.

Asia-Pacific Flexible Packaging Industry Leaders

Amcor plc

Sonoco Products Company

Sealed Air Corporation

Mondi plc

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: China’s State Administration for Market Regulation enforced 0.5% contamination limits for food-contact recycled plastics, accelerating mono-PE adoption while raising compliance costs by 3-5% for converters.

- July 2025: Dow launched INNATE TF 220 recyclable BOPE resin that boosts puncture resistance 30-40%, targeting heavy-duty stretch wrap applications.

- June 2025: Japan’s Ministry of Health, Labour and Welfare activated a positive-list for food-contact additives, triggering USD 50,000-100,000 reformulation spends per SKU among converters.

- May 2025: Constantia Flexibles debuted Flexible Blister, a mono-PE blister pack replacing aluminum-PVC formats in regulated pharmaceutical markets.

Asia-Pacific Flexible Packaging Market Report Scope

Flexible packaging refers to any package or component that can readily change shape when filled or used. Flexible packaging is primarily used for food, accounting for more than 60% of the total market, according to the Flexible Packaging Association. The market is experiencing healthy growth, having successfully implemented innovative solutions to address various packaging challenges.

The Asia-Pacific Flexible Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foil, and Bioplastics and Compostable Materials), Product Type (Bags and Pouches, Films and Wraps, Sachets and Stick Packs, and Other Product Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceutical, Personal Care and Cosmetics, Agriculture, and Other End-Use Industries), Printing Technology (Flexography, Rotogravure, Digital Printing, and Other Printing Technologies), and Country (China, India, Japan, Australia, South Korea, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

BY End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

By Country

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Material | Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Bioplastics and Compostable Materials | ||

| By Product Type | Bags and Pouches | |

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Other Product Types | ||

| BY End-user Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Agriculture | ||

| Other End-Use Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital Printing | ||

| Other Printing Technologies | ||

| By Country | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How big will Asia-Pacific flexible packaging demand be by 2031?

It is projected to reach USD 96.91 billion, up from USD 86.02 billion in 2026, at a 2.41% CAGR.

Which substrate is growing fastest in regional flexible packs?

Bioplastics and compostable films, expanding at a 4.12% CAGR because brands chase EPR compliance and premium positioning.

Why is digital printing gaining share in flexible packs?

Sub-1,000-unit runs for personalized or regional SKUs cost far less to start on digital presses than on rotogravure, shrinking lead times to two weeks.

What makes India a high-growth packaging market?

Rising food processing, booming pharmaceutical exports, and e-commerce uptake lift demand, pushing a 4.23% CAGR through 2031.

How are regulations shaping material choices in Japan and Australia?

Positive-list and recycled-content mandates force converters to adopt mono-material PE or PP structures and secure food-grade recyclate.

Which companies lead innovation in recyclable barrier films?

Amcor, Constantia Flexibles, and Dow are commercializing mono-material laminates and high-performance BOPE or PE blister packs.

Page last updated on: