Asia Pacific Enterprise Routers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

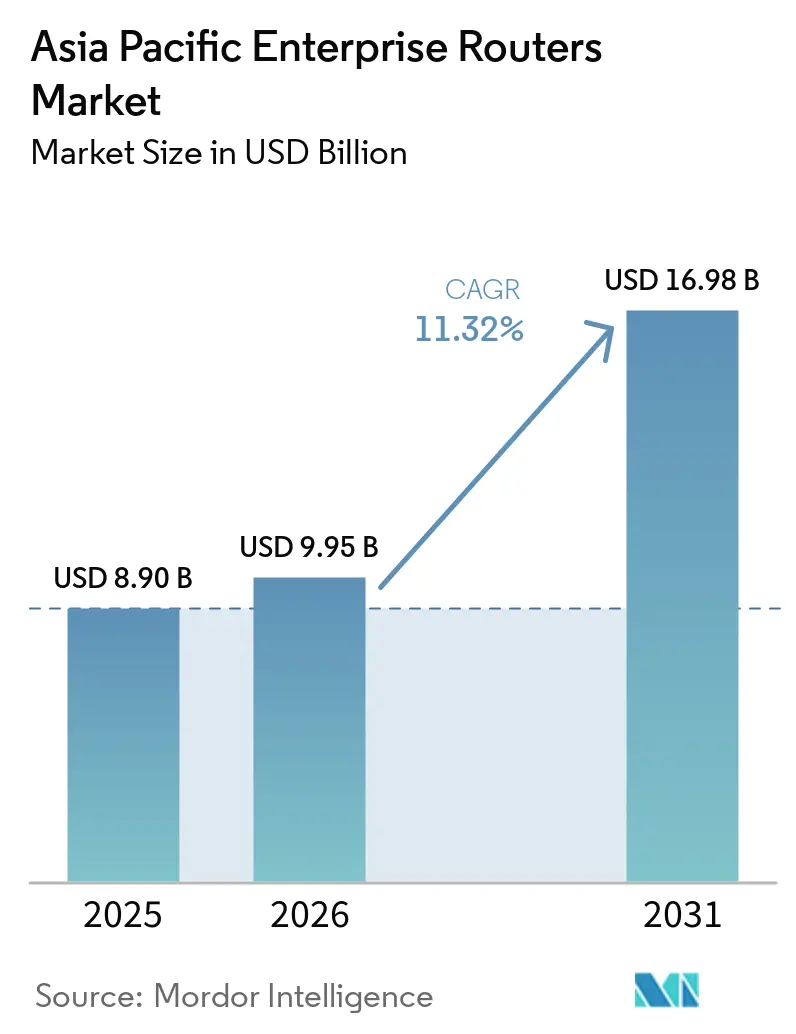

| Base Year Market Size (2025) | USD 8.90 Billion |

| Market Size (2026) | USD 9.95 Billion |

| Market Size (2031) | USD 16.98 Billion |

| Growth Rate (2026 - 2031) | 11.32% CAGR |

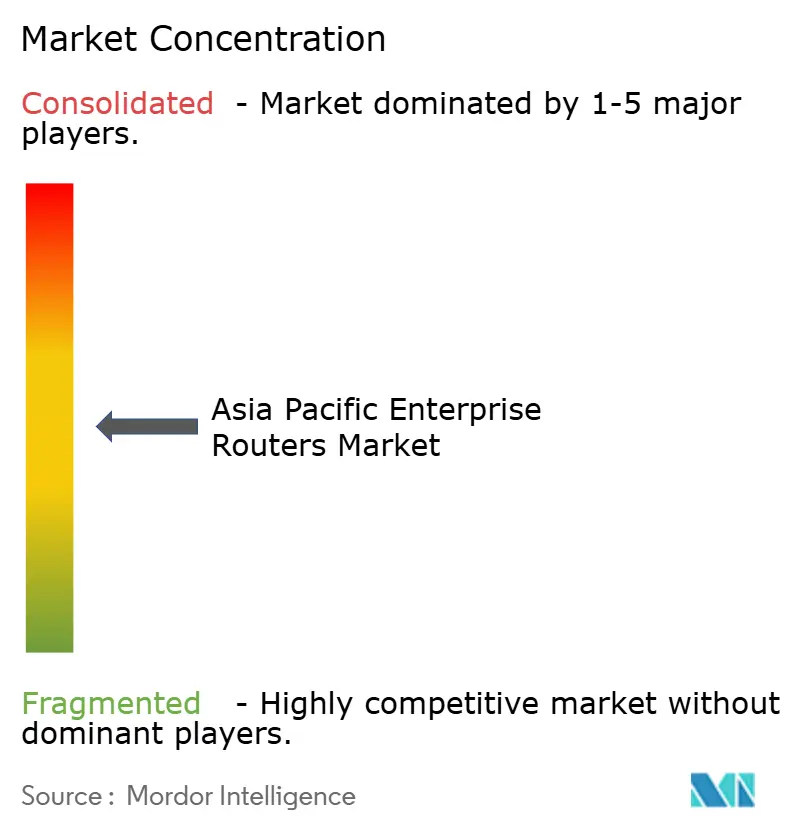

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Enterprise Routers Market Analysis by Mordor Intelligence

The Asia Pacific enterprise routers market size was valued at USD 8.90 billion in 2025, and estimated to grow from USD 9.95 billion in 2026 to USD 16.98 billion by 2031, at an 11.32% CAGR over 2026-2031. Demand is escalating because governments now require on-premises routing to satisfy data-localization rules, telecom operators are switching on 5G standalone cores that count on ultra-low-latency edge gateways, and the lingering semiconductor crunch is nudging buyers toward modular chassis that accept incremental upgrades instead of wholesale replacements. Competition among Chinese and Western vendors is intensifying, yet memory-component inflation has trimmed gross margins across the supply chain, prompting channel renegotiations and longer refresh cycles. Even so, routers remain central to hybrid-cloud adoption, industrial IoT corridors and SD-WAN overlays that let mid-market firms skip dedicated MPLS circuits in favor of encrypted broadband. The result is a double-digit growth trajectory that relies on wireless backhaul in territories where fixed broadband still covers less than one-third of businesses.

Key Report Takeaways

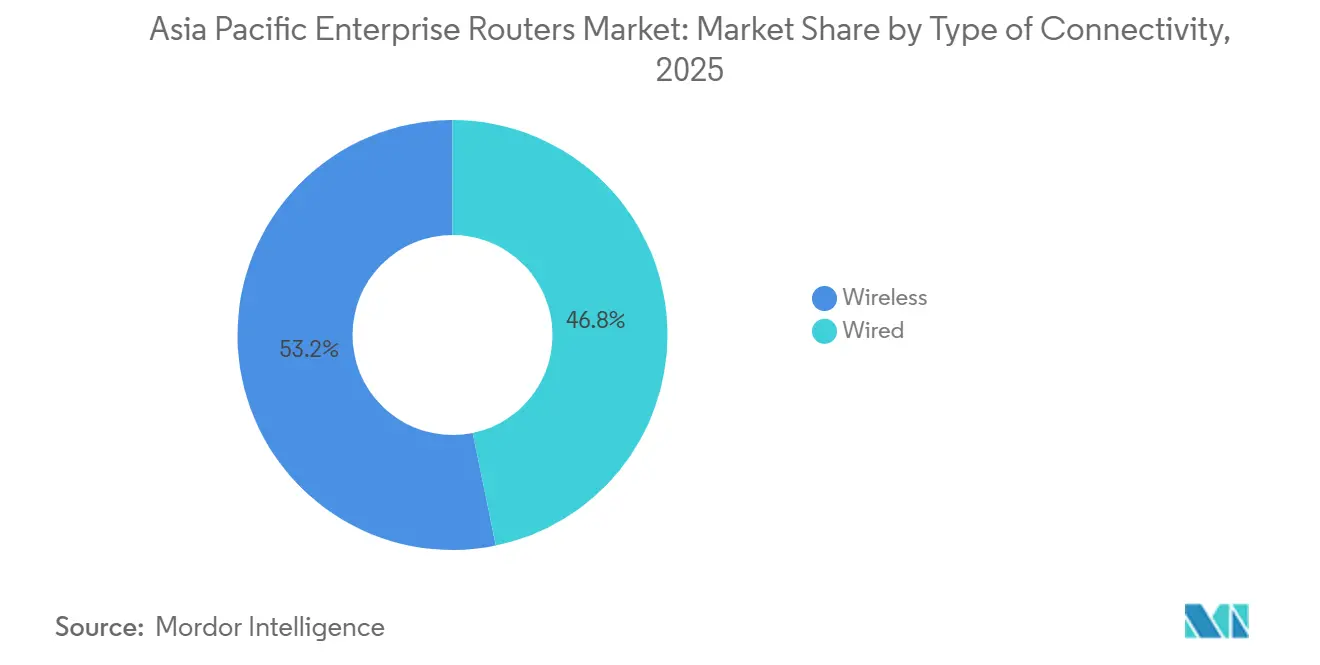

- By type of connectivity, wireless captured 53.23% of the Asia Pacific enterprise routers market share in 2025 and is advancing at a 12.11% CAGR to 2031.

- By type of port, modular chassis accounted for 68.40% of the Asia Pacific enterprise routers market size in 2025, while fixed-port units are rising faster at 11.70% through 2031.

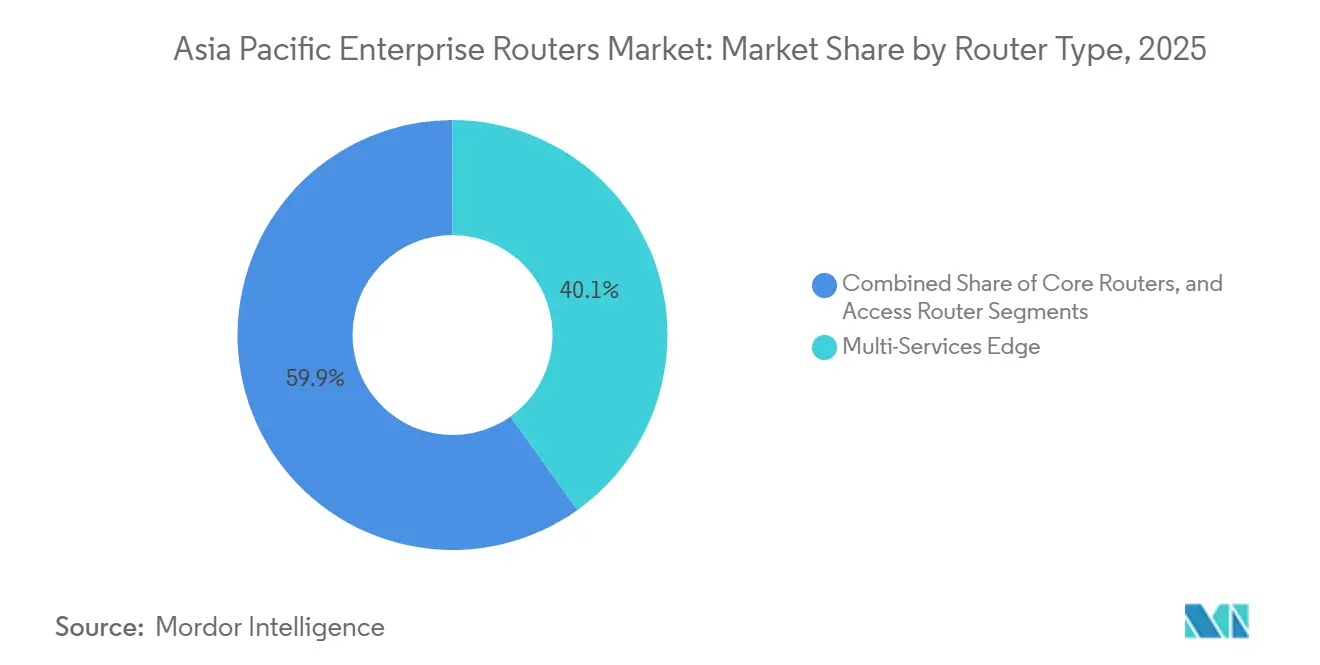

- By router type, core platforms recorded the quickest growth at 11.97% CAGR, whereas multi-services edge routers held a 40.13% shipment share in 2025.

- By end-user vertical, BFSI led with 24.81% revenue share in 2025, whereas IT and telecom is set to grow at a 12.65% CAGR during 2026-2031.

- By country, China represented 52.74% of the Asia Pacific enterprise routers market size in 2025 and Indonesia is set to expand at 12.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on enterprise routers market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia Pacific Enterprise Routers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Network Deployment Boosting Enterprise Bandwidth Demands | +2.8% | China, South Korea, Japan, Australia, Indonesia, Thailand | Short term (≤ 2 years) |

| Proliferation of Cloud Services and Data Centers in Asia Pacific | +2.5% | Singapore, Sydney, Mumbai, Tokyo, Seoul, Jakarta | Medium term (2-4 years) |

| Growing Digital Transformation Initiatives Among SMEs | +2.0% | Vietnam, Indonesia, Thailand, India, Malaysia | Medium term (2-4 years) |

| Rising Adoption of SD-WAN and Network Virtualization Technologies | +1.8% | Core APAC markets, Philippines, Vietnam | Short term (≤ 2 years) |

| Government-Led Industrial IoT Corridors Requiring URLLC | +1.5% | China, India, Japan, South Korea | Long term (≥ 4 years) |

| Surge in AI-Based Edge Computing for Manufacturing Quality Control | +1.2% | China, Thailand, Vietnam, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Network Deployment Boosting Enterprise Bandwidth Demands

Operators are upgrading from non-standalone to standalone 5G, exposing network slicing and low-latency capabilities directly to enterprises. Commercial launches in Australia and Singapore have already let businesses reserve guaranteed bandwidth slices for robotics, augmented-reality training and remote surgery. Vietnam’s Open RAN buildout reached 2,000 base stations in 2025 and 40,000 by early 2026, setting new benchmarks for edge-router throughput.[1]Viettel Group, “World’s First Commercial 5G Open RAN Network,” vietteltelecom.vn These advances replace legacy branch boxes with multi-services edge units that parse quality-of-service tags and enforce service-level agreements at the application layer, adding 2.8 percentage points to forecast growth.

Proliferation of Cloud Services and Data Centers in Asia Pacific

Hyperscalers have unveiled multibillion-dollar footprints in Australia, Thailand and Indonesia, pushing the regional data-center pipeline to nearly 20 gigawatts in late 2025. Hybrid architectures keep sensitive records on-premises yet burst compute-intensive workloads to the cloud, compelling enterprises to adopt routers with built-in encryption engines and dynamic path selection. Healthcare systems such as Singapore’s National University Health System now process patient telemetry over private 5G while enforcing strict data-residency mandates. The resulting refresh cycle is poised to lift the market by 2.5 percentage points over the medium term.

Growing Digital Transformation Initiatives Among SMEs

Subsidy programs in Vietnam, Malaysia and Indonesia are helping half a million small and midsize firms adopt e-invoicing and cloud CRM. Bundled SD-WAN subscriptions wrap routing, firewall licenses and 24-hour support into a predictable monthly fee, eliminating upfront capital outlays. Pre-configured router kits aimed at firms with fewer than 50 employees slash deployment times from weeks to hours. As these programs mature, demand from smaller companies adds 2.0 percentage points to the market’s CAGR.

Rising Adoption of SD-WAN and Network Virtualization Technologies

A 2025 regional survey shows that nearly every large enterprise is either live with SD-WAN or plans to be within a year.[2]Viettel Group, “World’s First Commercial 5G Open RAN Network,” vietteltelecom.vn Banks in Thailand and the Philippines are routing encrypted transactions over broadband plus 4G back-up lines, shaving operating costs by nearly one-third. The appeal lies in provisioning new sites via portal clicks rather than truck rolls, while unified controllers enforce ISO 27001 policies at scale. This shift lifts growth by 1.8 percentage points on a short-term horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Price Competition Compressing Vendor Margins | -0.90% | China, India, Indonesia, Vietnam | Short term (≤ 2 years) |

| Cybersecurity Concerns and Complex Threat Landscape | -0.70% | Global, acute in BFSI and healthcare | Medium term (2-4 years) |

| Supply Chain Disruptions for Semiconductor Components | -0.60% | Global manufacturing hubs: Taiwan, South Korea, Malaysia | Short term (≤ 2 years) |

| Fragmented Spectrum Regulations Delaying Advanced Feature Adoption | -0.40% | India, Indonesia, Thailand, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition Compressing Vendor Margins

Memory-component costs multiplied more than sixfold by early 2026, pushing DRAM and NAND flash to over one-fifth of router bills of materials.[3]Barracuda Networks, “97% of APAC Enterprises Adopt SD-WAN,” barracuda.com Domestic Chinese suppliers leveraged local subsidies to undercut Western brands by as much as 25% on like-for-like configurations, forcing rivals to compete on software and support quality instead of hardware price. Channel partners face stricter inventory terms while some enterprises defer refreshes, shaving 0.9 percentage points from market expansion.

Cybersecurity Concerns and Complex Threat Landscape

Ransomware incidents surged 59% in 2025, with 135,000 attacks logged against enterprise infrastructure. Edge devices now sit in the crosshairs of advanced persistent threats that exploit unpatched firmware, default credentials and tainted supply-chain images. Budgets for security jumped to 13.6% of total IT spend in 2026, yet many organizations still delay router deployments until trusted firmware versions become available or add additional security appliances in-line, subtracting 0.7 percentage points from forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Connectivity: Wireless Dominates Greenfield Deployments

Wireless links held 53.23% of the Asia Pacific enterprise routers market share in 2025. Viettel’s sweeping Open RAN program and millimeter-wave trials in Sydney prove that private 5G and Wi-Fi 6E can leapfrog copper trenching to connect forklifts, scanners and cameras at gigabit rates. Spectrum releases in Thailand, Malaysia and India now earmark mid-band channels specifically for enterprise networks, propelling a 12.11% CAGR through 2031. Demand intensifies wherever fixed broadband lags, yet wired options remain essential in data centers and trading floors where deterministic latency outweighs higher build cost.

Although wireless leads growth, policymakers in Indonesia want fixed broadband penetration to hit 50% by 2029, so headquarters and campuses still rely on fiber-anchored routers. Meanwhile, branch offices and pop-up sites favor plug-and-play wireless units that respect data-residency rules without routing traffic through telco cores. This hybrid model cements wireless as the expansion vector while wired retains its niche in performance-critical environments.

By Type of Port: Modular Chassis Hedge Against Component Shortages

Modular configurations commanded 68.40% of the Asia Pacific enterprise routers market size in 2025 because line cards, fabrics and power supplies can be swapped as traffic grows or components age. When memory shortages lengthened lead times to 16 weeks, banks and carriers simply upgraded existing chassis instead of ordering complete replacements. Fixed-port boxes grow faster at 11.70% CAGR because small and midsize users prefer lower entry prices and zero-touch provisioning. Yet high-variability sectors such as finance and telecom still favor chassis that scale to 800 Gbps per slot, ensuring bandwidth headroom during rapid digitalization bursts.[4]Lumen Technologies, “Edge Device Targeting and Memory Cost Pressures,” lumen.com

Retailers, clinics and schools adopt inexpensive fixed-port hardware like the DWM-314-G 5G router launched in Australia for AUD 1,249.95 (USD 820) and in New Zealand for NZD 1,499.99 (USD 920). Conversely, Chinese tier-one carriers sourced modular 400 Gbps core platforms that can quadruple capacity inside the same frame, reinforcing the split between predictable and volatile workloads.

By Router Type: Core Platforms Anchor AI and Cloud Traffic

Core routers post the quickest pace at 11.97% CAGR because hyperscalers and carriers now need 400 Gbps and 800 Gbps links to stitch together GPU clusters and metro backbones. Multi-services edge appliances, which held 40.13% of shipments in 2025, combine routing, firewall and SD-WAN features so that branch sites can collapse multiple boxes into one. Access routers connect IoT sensors and smart-building endpoints and continue to ship in high volumes, yet each unit commands lower revenue than a core chassis.

Developments such as Juniper’s PTX12000 AI fabric router and Huawei’s edge unit rolled out across 1,060 Thai bank branches illustrate how each tier of routing plays a specific role. Core platforms carry fewer but larger orders, edge boxes sell by the thousand and access devices sell by the tens of thousands as factories and logistics yards digitize.

By End-User Vertical: BFSI Leads, IT and Telecom Accelerates

Regulators oblige banks to segregate transactions and achieve sub-millisecond failover across data centers, so BFSI bought roughly one-quarter of all routers in 2025. Multinational lenders also insist on interoperability with U.S. and European headquarters, cementing Western vendors’ beachheads in Hong Kong, Singapore and Sydney. On the flip side, telecom carriers and cloud service providers are racing to monetize 5G and edge computing, lifting IT and telecom demand at a 12.65% CAGR through 2031.

Healthcare, retail and manufacturing sit in the middle. Hospitals adopt private 5G for remote surgery and electronic records, retailers integrate SD-WAN to unify real-time inventory, and factories embed routers directly into production lines for predictive maintenance. Government projects, from Indonesia’s national data-center consolidation to India’s industrial corridors, round out demand with strict data-residency and multi-tenant requirements.

Geography Analysis

China held 52.74% of the Asia Pacific enterprise routers market in 2025 due to massive state-enterprise buys, home-grown vendors and the Ministry of Industry and Information Technology’s ambition to link 120 million industrial devices by 2028. Contract awards from China Mobile and China Unicom for 400 Gbps and 800 Gbps platforms keep the replacement cycle brisk even as new site growth slows.

Indonesia is the breakout market, expanding at a 12.28% CAGR as the SATRIA-1 satellite and a rapidly growing fiber backbone bring government services to 30,000 public points by 2029. A collaborative public data network lets private clouds host ministry workloads, so routers must enforce data sovereignty while carrying mixed civilian and official traffic.

India’s 11 smart-manufacturing corridors, Japan and South Korea’s pursuit of 6G, Thailand and Vietnam’s manufacturing relocation and Australia’s mining and logistics digitization each carve distinct requirements.[5]Cisco Systems, “Catalyst 9000 Portfolio Update,” cisco.com Mature northeast Asian countries lean toward ultra-high-throughput upgrades, whereas Southeast Asia balances greenfield coverage and affordability. Rest of Asia Pacific, including Malaysia, the Philippines and Cambodia, remains a wireless-first arena where SD-WAN and private 5G sidestep expensive fiber builds.

Competitive Landscape

Competition is lively but not yet consolidated. Huawei, ZTE, H3C and Ruijie dominate state-run orders by pairing cost advantages with government ties, while Cisco, Juniper and HPE secure multinational subsidiaries and tier-one banks that value global interoperability. Gross-margin pressure from soaring memory prices caused Cisco to tighten inventory terms and Arista to warn investors of cost spikes, yet vendors pivot by adding software-defined overlays, AI-driven traffic steering and integrated zero-trust security.

Fortinet logged 40% year-on-year growth in unified SASE subscriptions, and Palo Alto Networks expanded regional clouds to cut latency for zero-trust access, underscoring the swing toward networking-security convergence. Smaller disruptors like TP-Link and Zyxel court SMEs with cloud-managed, zero-touch devices, while Open RAN initiatives let enterprises mix radios, basebands and routers at will. Compliance with ISO 27001 and new data-protection laws forms a fresh battleground as buyers favor hardware that proves encryption and audit readiness straight out of the box.

White-space pockets appear in mid-market manufacturing, healthcare and digital-identity programs where MPLS is fading and SD-WAN overlays enable granular segmentation without carrier lock-in. Arista projects AI networking sales of USD 3.25 billion in 2026 as GPU cluster demand spreads beyond U.S. hyperscalers into Asia Pacific cloud providers, hinting at the next wave of core-router upgrades.

Asia Pacific Enterprise Routers Industry Leaders

CISCO Systems Inc.

Huawei Technologies Co. Ltd

Hewlett Packard Enterprise

Juniper Networks Inc.

Extreme Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Juniper Networks, Inc. introduced next-generation PTX series routers (including PTX10002 and PTX10008 enhancements) designed for AI workloads, offering 800G interfaces, ultra-high throughput, and automation for hyperscale and enterprise backbone networks.

- December 2025: D-Link released the DWM-314-G 5G router in Australia for AUD 1,249.95 (USD 820) and New Zealand for NZD 1,499.99 (USD 920) to serve small offices needing cellular backup.

- September 2025: Fujitsu and Arrcus formed an alliance to deliver AI infrastructure that slashes routing TCO by 40% through white-box hardware.

- July 2025: Hewlett Packard Enterprise (HPE) completed the acquisition of Juniper Networks, Inc. to strengthen its AI-native networking and enterprise routing portfolio, combining HPE Aruba with Juniper’s routing, switching, and AI-driven automation capabilities.

Asia Pacific Enterprise Routers Market Report Scope

The Asia Pacific Enterprise Routers Market Report is Segmented by Type of Connectivity (Wired, and Wireless), Type of Port (Fixed Port, and Modular), Router Type (Core Routers, Multi-Services Edge, and Access Router), End-User Vertical (BFSI, IT and Telecom, Healthcare, Retail, Manufacturing, Government and Public Sector, Education, and Other End-User Verticals), and Geography (China, India, Japan, South Korea, Indonesia, Thailand, Vietnam, Australia and New Zealand, and Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Wired |

| Wireless |

| Fixed Port |

| Modular |

| Core Routers |

| Multi-Services Edge |

| Access Router |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom |

| Healthcare |

| Retail |

| Manufacturing |

| Government and Public Sector |

| Education |

| Other End-User Verticals |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Thailand |

| Vietnam |

| Australia and New Zealand |

| Rest of Asia Pacific |

| By Type of Connectivity | Wired |

| Wireless | |

| By Type of Port | Fixed Port |

| Modular | |

| By Router Type | Core Routers |

| Multi-Services Edge | |

| Access Router | |

| By End-User Vertical | Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom | |

| Healthcare | |

| Retail | |

| Manufacturing | |

| Government and Public Sector | |

| Education | |

| Other End-User Verticals | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Australia and New Zealand | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the current value of the Asia Pacific enterprise routers market?

The Asia Pacific enterprise routers market size stood at USD 9.95 billion in 2026 and is forecast to reach USD 16.98 billion by 2031.

Which segment is growing fastest within regional deployments?

Core routers are expanding at an 11.97% CAGR through 2031 as hyperscalers and carriers roll out 400 Gbps and 800 Gbps backbones.

Why are Indonesian deployments accelerating ahead of other Southeast Asian countries?

Indonesia’s Digital Government Master Plan is wiring 30,000 public service points and aims to lift fixed broadband coverage to 50% by 2029, driving a 12.28% CAGR for router purchases.

How are rising memory prices influencing vendor strategies?

DRAM and NAND flash inflation cut gross margins by up to five points, so vendors now emphasize software value, tighten distribution terms and delay some refresh cycles.

What role does SD-WAN play in small and midsize enterprise adoption?

Bundled SD-WAN subscriptions package routers, firewalls and support into monthly fees, letting SMEs skip capital expenditure and deploy secure broadband links in a matter of hours.

Which security risks most threaten enterprise router rollouts?

Ransomware, supply-chain firmware compromises and AI-driven adaptive attacks have escalated, causing some buyers to postpone deployments until patches and certifications are verified.

Page last updated on: