Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

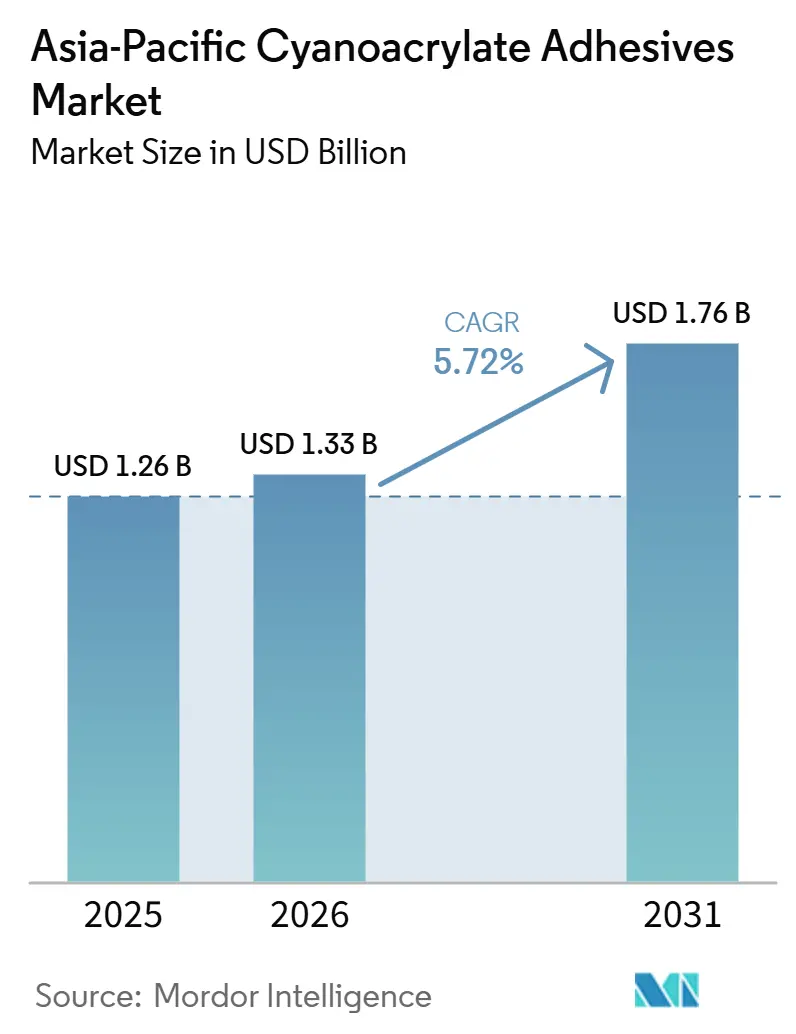

| Base Year Market Size (2025) | USD 1.26 Billion |

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

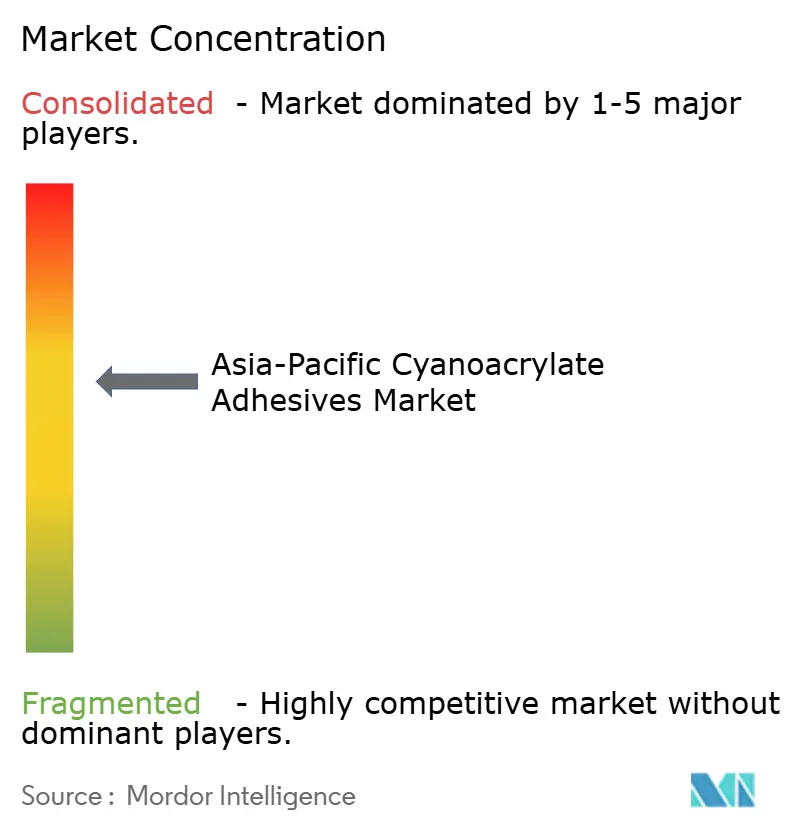

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cyanoacrylate Adhesives Market Analysis by Mordor Intelligence

The Asia-Pacific Cyanoacrylate Adhesives Market size was valued at USD 1.26 billion in 2025 and is estimated to grow from USD 1.33 billion in 2026 to reach USD 1.76 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Cyanoacrylate consumption rises as electronics assembly lines, electric-vehicle platforms, and medical-device factories scale output across China, India, South Korea, and Southeast Asia. Regulatory clarity on topical skin adhesives, voluntary VOC limits, and corporate carbon-footprint targets are pushing formulators toward low-odor, low-bloom chemistries that still cure in seconds. Consolidation among multinational suppliers is intensifying, with Henkel’s new Shanghai Inspiration Center and Singapore Science Park hub providing localized research and development and digital supply-chain capabilities. Price swings for key monomers and the limited heat resistance of instant adhesives compared with epoxies temper growth, yet rising automation in electronics, stringent automotive material bans, and do-it-yourself renovation trends keep demand on an upward trajectory in the Asia Pacific cyanoacrylate adhesives market.

Key Report Takeaways

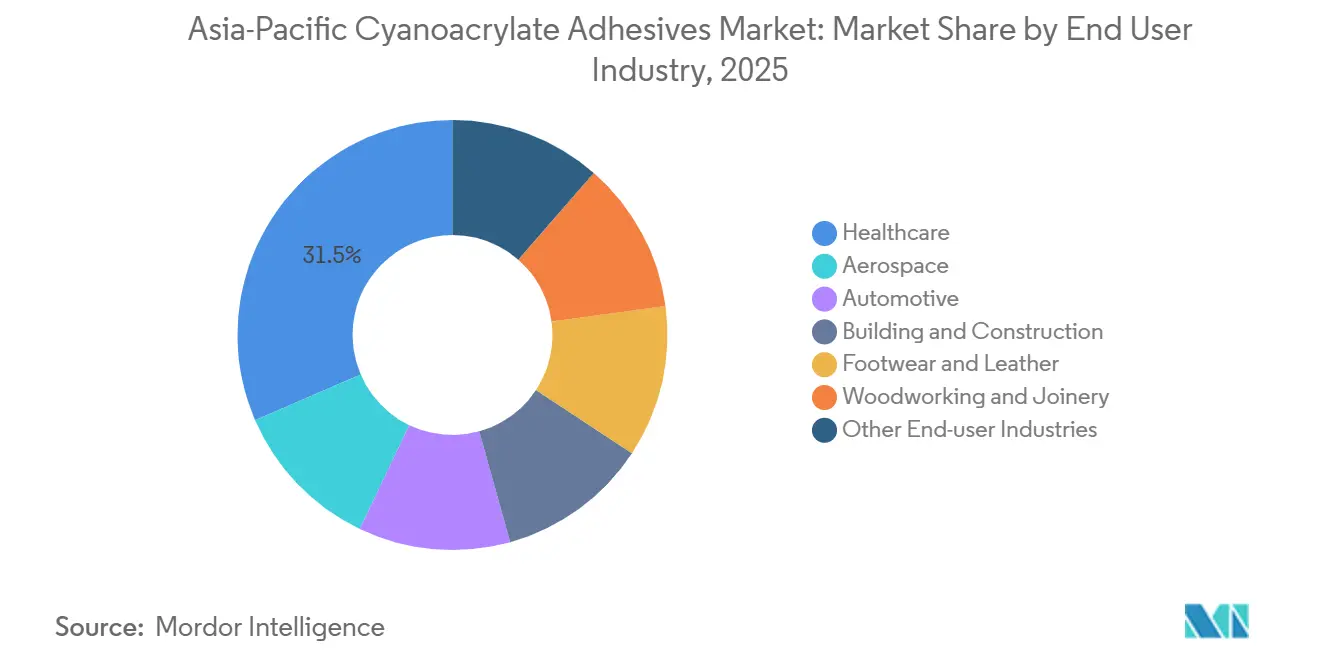

- By end-user industry, healthcare led with 31.48% of the Asia Pacific cyanoacrylate adhesives market share in 2025 while expanding at a 6.04% CAGR through 2026-2031.

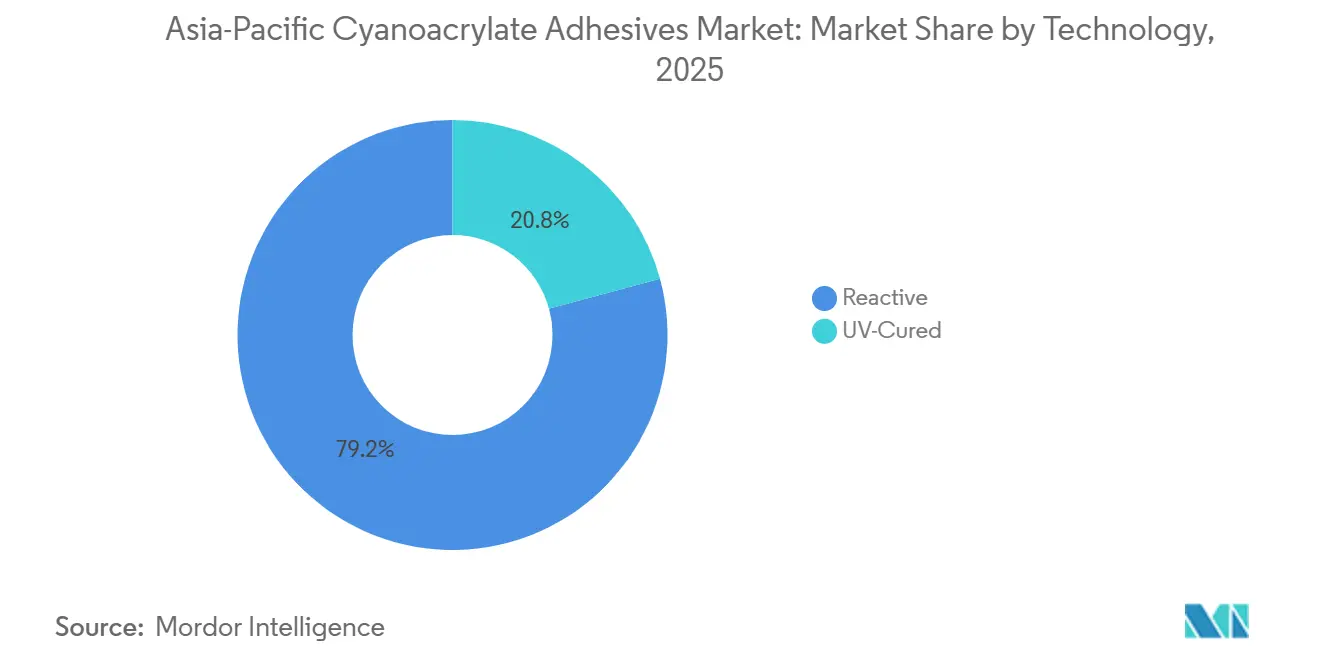

- By technology, reactive formulations dominated with a 79.22% share in 2025, whereas UV-cured grades are projected to record the fastest growth at 6.68% CAGR 2026-2031.

- By geography, China captured 47.18% of revenue in 2025, and India is poised for the quickest expansion with a 6.82% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Cyanoacrylate Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging electronics assembly demand | +1.80% | China, India, South Korea, Singapore, Malaysia | Medium term (2-4 years) |

| Rising automotive lightweighting initiatives | +1.30% | China, India, Japan, South Korea, Thailand | Medium term (2-4 years) |

| Booming residential DIY market | +0.90% | China, Singapore, Australia, urban India | Short term (≤ 2 years) |

| Growing medical device usage of topical skin adhesives | +1.10% | India, China, Japan, Australia | Long term (≥ 4 years) |

| Shift to low-odor/low-bloom formulations for worker safety | +0.70% | Global, with early adoption in Japan, Singapore, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Electronics Assembly Demand

Multiple projects approved under India’s Electronics Component Manufacturing Scheme by January 2026 are attracting billions in capital and thousands of new jobs, lifting instant-adhesive offtake for multilayer printed circuit boards (PCBs), camera modules, and optical devices. In China, strong gains in industrial-robot output and equipment manufacturing value add demonstrate expanding automation that boosts adhesive consumption on high-speed lines. Henkel's Singapore Technical Center now recreates dispensing, die-attach, and lamination processes, cutting qualification times for cyanoacrylates aimed at semiconductor packaging. UPM’s Johor Bahru coating line, coming online mid-2026, adds filmic constructions for durable labels and foldable-display films, catering to Southeast Asian electronics makers[1]UPM, “UPM Adhesive Materials Invests in Malaysia Factory,” inderes.fi .

Rising Automotive Lightweighting Initiatives

China has increased its production of motor vehicles and new-energy vehicles, boosting the demand for cyanoacrylate in battery pack housings, trims, and electronics. Consequently, Toagosei has experienced a notable rise in sales of its battery-related adhesives compared to previous levels, prompting subsidiaries in Vietnam and India to expand during 2024. Hyundai Mobis requires suppliers to declare substances and reduce heavy-metal and copper content, favoring fast-curing, low- volatile organic compound (VOCs) instant bonds that eliminate heat in mixed-material joints. As OEMs target bio-based or recycled plastics, cyanoacrylates complement structural acrylics by delivering quick green strength without ovens, supporting throughput in gigafactories.

Booming Residential DIY Market

Pidilite has rolled out its “Pidilite ki Duniya” network to tens of thousands of rural outlets, letting Fevikwik penetrate village hardware stores and quick-commerce channels alike. Despite China’s dip in construction value added during 2025, Beijing's Five-Year Plan secures infrastructure pipelines worth trillions and green-transition budgets that keep mortar and flooring adhesive uptake resilient. In India, more than 80% of furniture is still produced on site by carpenters, sustaining instant-adhesive demand for wood joinery and repair. Singapore’s Land Transport Master Plan funds new rail corridors and station upgrades, boosting fast-setting consumer adhesives used in home improvement projects aligned with transit expansion.

Growing Medical Device Usage of Topical Skin Adhesives

China’s revised August 2024 guidelines for α-cyanoacrylate medical adhesives spell out Class III classification, validated sterilization, and real-time stability studies, reducing dossier uncertainty for innovators. Meril Endo Surgery’s 510(k) for Meriglu was cleared in March 2024 after a 346-day review, proving Asia-based firms can navigate U.S. pathways and export premium tissue adhesives. H.B. Fuller bought GEM S.r.l. and Medifill Ltd. in December 2024, adding cleanrooms and advanced cyanoacrylate assets that serve growing outpatient and emergency-care demand for suture-free closures. Hospitals value rapid hemostasis, reduced needlestick risk, and lower procedure times, positioning instant tissue adhesives for wider adoption in the Asia Pacific cyanoacrylate adhesives market healthcare portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of cyanoacrylate monomers | -0.80% | Global, with acute exposure in China, India | Short term (≤ 2 years) |

| Stringent VOC and workplace exposure limits | -0.50% | China, Japan, Hong Kong, Singapore, Australia | Medium term (2-4 years) |

| Limited heat-resistance versus epoxies | -0.40% | China, Japan, South Korea (automotive underhood, power electronics) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Cyanoacrylate Monomers

Pidilite disclosed falling vinyl acetate monomer costs that widened gross margins but underscored susceptibility to feedstock swings. China’s producer price index fell in 2025, limiting pass-through room for adhesive makers even as ethylene investment rose. Japan’s chemicals database shows modest local alkyl-cyanoacrylate production volumes, constraining scale economies. Smaller converters, lacking hedging tools, absorb spot spikes or lose share, pushing many toward tolling deals with integrated multinationals in the Asia Pacific cyanoacrylate adhesives market.

Stringent Volatile Organic Compound (VOC) and Workplace Exposure Limits

China’s GB 33372-2020 caps α-cyanoacrylate bulk adhesives at 20 grams per kilogram VOC and mandates precise test methods, requiring periodic third-party audits. Hong Kong’s rule restricts general adhesives to 250 grams per liter (g/L)VOC, with civil penalties for exceedance. OSHA Method 55 prescribes refrigerated air sampling and High-Performance Liquid Chromatography Ultraviolet (HPLC-UV) analysis for workplace monitoring, raising compliance costs in global export plants[2]OSHA, “Method 55 Methyl and Ethyl 2-Cyanoacrylate,” osha.gov . Multinationals amortize these costs across global volumes, whereas small and medium-sized enterprises (SMEs) face higher per-kilogram certification expenses, tilting the Asia Pacific cyanoacrylate adhesives market toward consolidated suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Healthcare Benefits from Regulatory Clarity and Export Momentum

Healthcare held 31.48% of the Asia Pacific cyanoacrylate adhesives market share in 2025 and is projected to grow at 6.04% CAGR through 2026 to 2031. The segment advances as China’s Class III rules remove ambiguity and Indian firms win U.S. clearances, encouraging capital inflows into sterile production lines. Hospitals prefer topical skin adhesives to speed wound closure and cut needlestick risk. Cross-border demand from Asia-based OEM contract sterilizers also supports volume growth. Rising disposable incomes across ASEAN expand elective surgery counts, further lifting medical-grade cyanoacrylate uptake within the Asia Pacific cyanoacrylate adhesives market size for this segment.

Consumer DIY and woodworking remain steady contributors. Pidilite’s rural channel expansion strengthens category resilience during urban slowdowns. Footwear and leather workshops leverage instant bonds for sole attachment and trim finishing. Construction uptake moderates in China, yet stays positive due to green-transition retrofits. Automotive and electronics retain double-digit share as lightweighting and miniaturization continue, though heat-critical joints migrate to epoxies. Aerospace demand is niche but stable, focused on non-critical cabin and avionics fastening.

By Technology: UV-Cured Grades Accelerate in High-Value Electronics

Reactive formulations dominated with 79.22% share in 2025 and still address high-volume footwear, DIY, and general maintenance uses. UV-cured cyanoacrylates, however, are clocking a 6.68% CAGR through 2026 to 2031 as chiplet architectures and optical modules demand on-demand cure control to limit blooming and shrink cycle times. This niche commands premium pricing because it reduces rework and downtime on automated lines. Indian subsidy programs for multilayer PCBs and optical transceivers stimulate UV-system capex, widening adoption footprints. Reactive products nonetheless remain price leaders and require no curing equipment, ensuring broad diffusion in rural construction, furniture making, and aftermarket automotive repair across the Asia Pacific cyanoacrylate adhesives market size spectrum. Innovation centers in Shanghai and Singapore are expected to advance hybrid chemistries that combine moisture and light triggers, further blurring lines between the two categories.

Geography Analysis

China’s 47.18% revenue share in 2025 confirms its standing as the manufacturing hub of the Asia Pacific cyanoacrylate adhesives market. Strong EV production, bigger chemical output, and Henkel’s Shanghai Inspiration Center reinforce local supply chains. Factories are transitioning to low-odor formulas due to the VOC cap under GB 33372, while overall volume remains unaffected. Although the construction sector is experiencing a slowdown, it is being offset by increased infrastructure investments aligned with the net-zero roadmap.

India shows the fastest regional trajectory at 6.82% CAGR through 2026-2031. Supported by the Electronics Components Manufacturing Scheme and a growing automotive base, Pidilite has achieved significant growth in rural sales. Meanwhile, Toagosei's establishment of a greenfield site near Ahmedabad reflects confidence in the region's potential. Additionally, Meriglu's recent FDA clearance highlights India's capability to export regulated medical-grade cyanoacrylates.

Japan, South Korea, Singapore, Malaysia, Indonesia, Thailand, and Australia form the balance of consumption. Japan’s voluntary VOC code drives premium low-odor niches. Singapore’s Science Park hosts Henkel’s largest electronic adhesives application lab in Southeast Asia, serving original equipment manufacturers (OEMs) across the subregion. UPM’s Malaysia expansion boosts the supply of filmic laminate substrates for flexible displays and smartphone housings. Australia and Thailand record steady consumer DIY and automotive-repair adhesives demand, aided by e-commerce penetration and electric-two-wheeler adoption.

Competitive Landscape

The Asia-Pacific Cyanoacrylate Adhesives Market is moderately consolidated. Strategic white space includes UV-cured instant adhesives for chiplet packaging, methoxyethyl low-bloom grades for camera modules, and bio-based monomers aligned with Hyundai Mobis recycling targets. AI-driven formulation platforms and digital twin pilot lines, exemplified by Henkel’s Singapore Digital Lab, shorten go-to-market timelines. Collaborative supplier original equipment manufacturer (OEM) initiatives on lifecycle assessment and carbon accounting will influence buying decisions through the forecast horizon.

Asia-Pacific Cyanoacrylate Adhesives Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

ThreeBond Holdings Co.,Ltd.

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Henkel has announced the opening of its new Inspiration Center for Adhesive Technologies in Shanghai to accelerate sustainable solution development, enhance customer collaboration, and support long-term growth in the Asia-Pacific market.

- January 2025: Sika AG inaugurated new plants in Singapore and Xi’an, China, strengthening regional supply, reducing logistics costs, and driving sustainable innovation in the Asia-Pacific Cyanoacrylate Adhesives Market.

Asia-Pacific Cyanoacrylate Adhesives Market Report Scope

Cyanoacrylate adhesives, commonly known as super glues, are fast-acting bonding agents that cure rapidly in the presence of moisture. They form strong, rigid joints by polymerizing into a solid plastic upon contact with surfaces. These adhesives bond a wide range of materials such as plastics, metals, ceramics, and rubber. Their quick setting time and high strength make them ideal for household, industrial, and medical applications.

The Asia-Pacific Cyanoacrylate Adhesives Market is segmented by end user industry, technology, and geography. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, woodworking and joinery, and other end user industries. By technology, the market is segmented into reactive and UV-cured. The report also covers the market size and forecasts for the Asia-Pacific Cyanoacrylate Adhesives Market in 9 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

End User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Woodworking and Joinery |

| Other End-user Industries |

Technology

| Reactive |

| UV-Cured |

Geography

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Singapore |

| South Korea |

| Thailand |

| Australia |

| Rest of Asia-Pacific |

| End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| Technology | Reactive |

| UV-Cured | |

| Geography | China |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Thailand | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the cyanoacrylate adhesives market.

- Product - All cyanoacrylate adhesive products are considered in the market studied

- Resin - Under the scope of the study, cyanoacrylates based on Alkoxy Ethyl, Ethyl Ester, Methyl Ester, and Others are considered

- Technology - For the purpose of this study, Reactive and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms