Split Air Conditioner Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

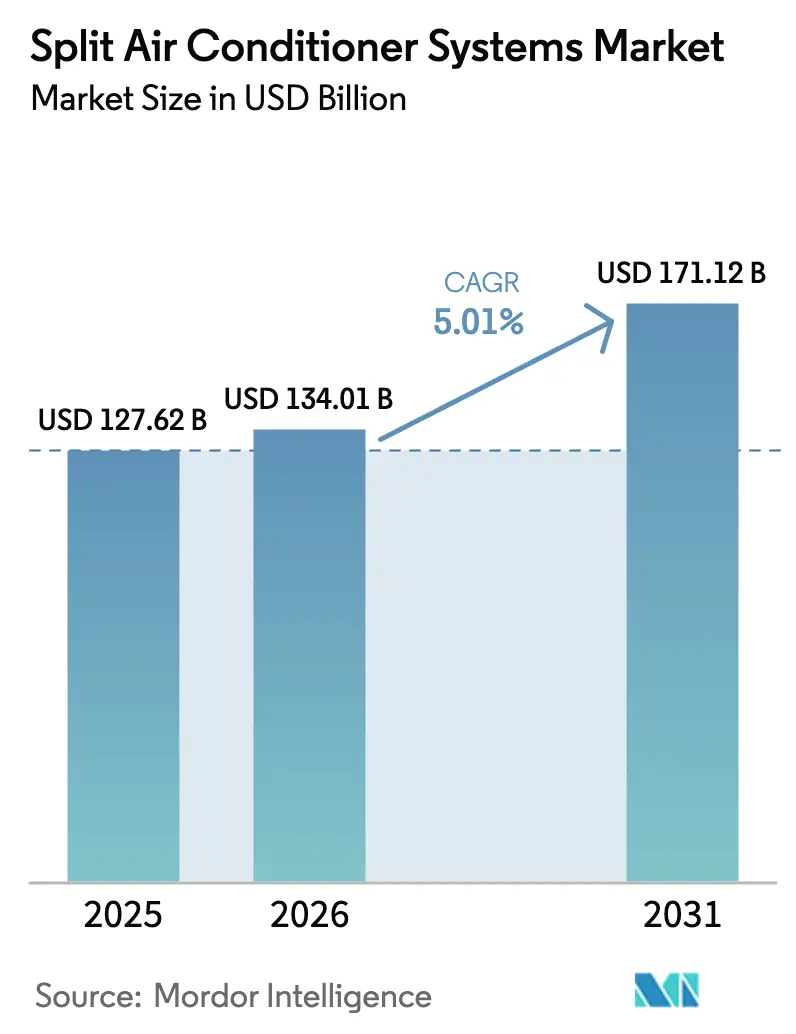

| Market Size (2026) | USD 134.01 Billion |

| Market Size (2031) | USD 171.12 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

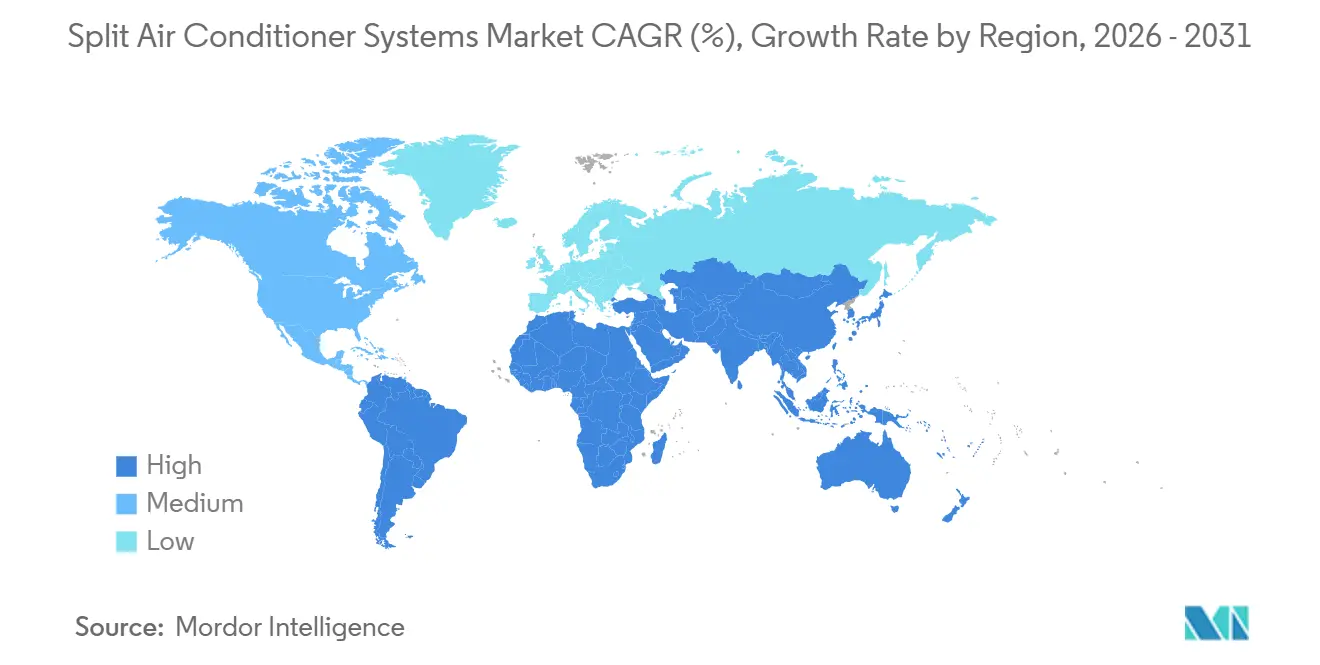

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Split Air Conditioner Systems Market Analysis by Mordor Intelligence

The Split Air Conditioner Systems Market size was valued at USD 127.62 billion in 2025 and is estimated to grow from USD 134.01 billion in 2026 to reach USD 171.12 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031).

The split air conditioner systems market is advancing on the back of inverter-driven compressors, integrated IoT controllers, and progressively tougher energy-efficiency mandates that shorten replacement cycles. Asia-Pacific remains the center of gravity for new installations thanks to urbanization in China and India, while early electrification programs and climate-resilience policies are opening fresh demand pockets in Africa. Commercial retrofits are embracing variable refrigerant flow (VRF) for granular zoning, and e-commerce platforms are reshaping how households and small businesses buy and service equipment. Competitive intensity is rising as Japanese and South Korean incumbents defend intellectual-property moats while Chinese challengers scale through cost leadership and rapid product iteration.

Key Report Takeaways

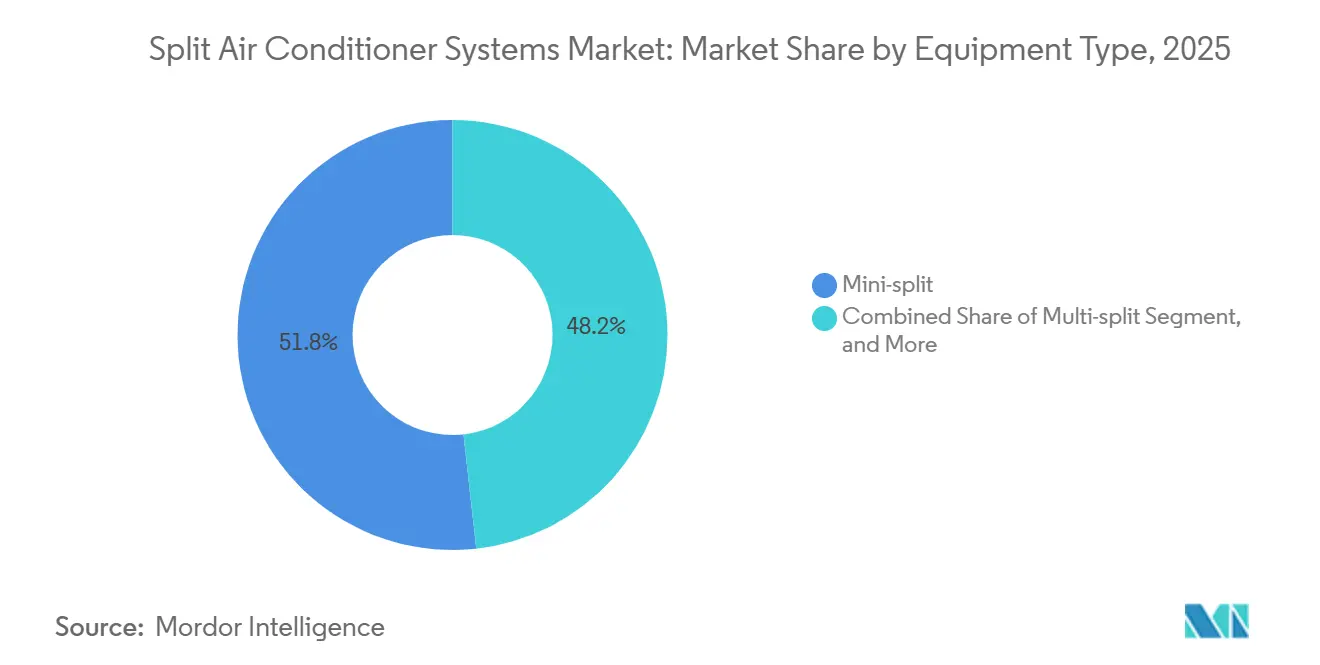

- By equipment type, mini-split configurations held 51.76% of split air conditioner systems market share in 2025, whereas VRF systems are projected to grow at a 5.76% CAGR through 2031.

- By application, the residential segment accounted for a 66.43% share of the split air conditioner systems market size in 2025, while commercial installations are expected to expand at a 5.43% CAGR to 2031.

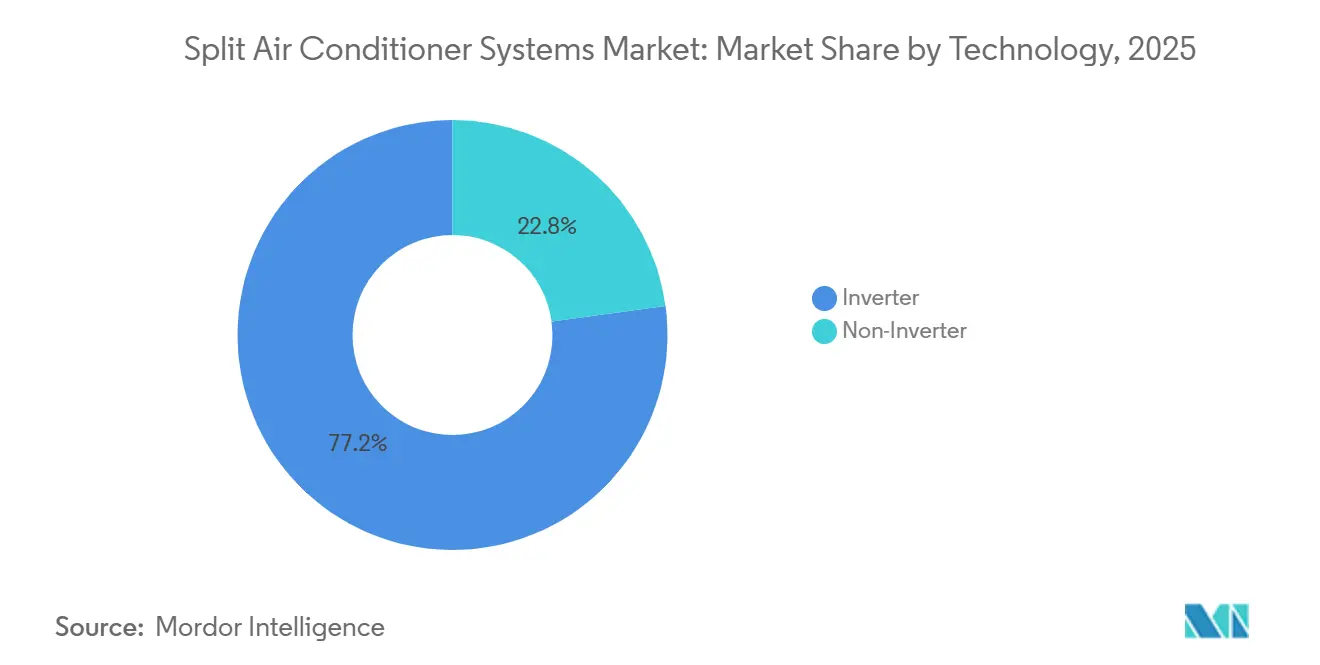

- By technology, inverter units commanded 77.16% of 2025 revenue and are advancing at a 5.51% CAGR, outpacing non-inverter alternatives.

- By cooling capacity, the 12,001-24,000 BTU segment captured 37.34% of the split air conditioner market share in 2025, whereas units above 36,000 BTU are the fastest-growing, with a 5.84% CAGR.

- By distribution channel, multi-brand retail stores led with 42.81% share in 2025, yet e-commerce is the quickest channel with a 5.67% CAGR.

- By geography, Asia-Pacific generated 63.31% of global revenue in 2025, while Africa is set to post the highest regional growth at a 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Split Air Conditioner Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-Change Induced Heat-Wave Frequency | +1.2% | Global with acute exposure in South Asia, Middle East, Sub-Saharan Africa | Long Term (≥ 4 Years) |

| Boom in Smart-Home and Smart-Office Retrofits | +0.9% | North America, Europe, Urban Asia-Pacific | Medium Term (2–4 Years) |

| IoT-Enabled Predictive-Maintenance Platforms Lowering TCO | +0.7% | Global, early adoption in North America and Europe | Medium Term (2–4 Years) |

| Government Energy-Efficiency Rebate Programs | +0.8% | United States, European Union, India, China | Short Term (≤ 2 Years) |

| Rising Disposable Income in Developing Countries | +0.6% | Asia-Pacific, Africa, South America | Long Term (≥ 4 Years) |

| Rapid Electrification in Off-Grid Asian and African Towns (Micro-Grids) | +0.4% | Sub-Saharan Africa, Rural India, Southeast Asia | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Climate-Change Induced Heat-Wave Frequency

Heat-wave length and severity are accelerating, lifting baseline cooling loads in tropical and subtropical regions. Peer-reviewed data show that global heat-wave duration has increased by 0.37 days per decade since 1979, with South Asia and the Middle East experiencing the sharpest rise.[1]R.J.H. Dunn, “Nonlinear Acceleration of Heatwave Duration,” Nature Geoscience, nature.com The World Meteorological Organization ranked 2025 as the third-warmest year on record, and the United States National Oceanic and Atmospheric Administration linked land temperatures 1.8 °C above pre-industrial norms to wider adoption of residential splits in the Pacific Northwest.[2]National Oceanic and Atmospheric Administration, “2025 Was 3rd Warmest Year on Record,” NOAA, noaa.gov India’s National Disaster Management Authority rolled out heat-action plans in 23 cities that fund community cooling centers and subsidize inverter models. As peak-load stress rises, building owners favor inverter technology that modulates compressor speed rather than oversizing equipment for extreme events. The International Energy Agency warns that without efficiency gains, electricity demand for space cooling could triple by 2050.

Boom in Smart-Home and Smart-Office Retrofits

Smart-building retrofits are embedding splits into connected ecosystems that align operation with occupancy and real-time tariffs. U.S. Department of Energy field pilots showed that pairing smart thermostats with inverter splits trimmed cooling bills by up to 20% in Texas and Arizona during 2025. Samsung SmartThings and LG ThinQ collectively manage more than 10 million HVAC endpoints, issuing predictive alerts that cut truck rolls by 25-30%. Europe’s revised Energy Performance of Buildings Directive mandates the use of automation systems in new non-residential buildings above 1,000 m² by 2026, a direct catalyst for IoT-ready splits. Although proprietary protocols have slowed interoperability, the Matter standard, backed by Apple, Google, and Amazon, aspires to unify device communication by late 2026.

IoT-Enabled Predictive-Maintenance Platforms Lowering TCO

Machine-learning algorithms that monitor vibration, refrigerant pressure, and coil temperature can predict failures 30-60 days in advance with 85% accuracy, slashing lifetime ownership costs by up to 30%. Daikin’s Service Intelligence platform reported a 28% drop in unplanned downtime across 500,000 connected commercial units in 2025. Carrier’s Abound software optimizes VRF zone allocation and realizes 12-15% energy savings in mixed-use buildings. Edge analytics are migrating to on-device processors, which are vital for installations on microgrids where internet access is intermittent. The retrofit challenge remains substantial because only 15% of the installed split base carries adequate sensor suites for high-resolution diagnostics.

Government Energy-Efficiency Rebate Programs

Fiscal incentives are expediting the retirement of low-efficiency legacy units. The United States Inflation Reduction Act allocated USD 8.8 billion in rebates, covering up to USD 8,000 per qualifying household. India’s Bureau of Energy Efficiency backs 5-star splits with state subsidies worth INR 5,000-10,000 (USD 60-120). The European Union earmarked EUR 3 billion (USD 3.3 billion) for heat-pump and split installations in social housing. China’s 2025 trade-in program awarded 10-15% discounts on inverter splits, triggering 12 million replacement sales in H1 2025. Such incentives accelerate demand yet risk market distortion if subsidies lapse without a commensurate cost decline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Volatility of Key Refrigerants (HFC-32, R-410A) | -0.6% | Global, acute in North America and Europe | Short Term (≤ 2 Years) |

| Stricter SEER/EER Regulations Inflating Upgrade Capex | -0.5% | United States, European Union, China | Medium Term (2–4 Years) |

| High Installation and Maintenance Cost | -0.3% | Emerging Markets in Asia-Pacific, Africa, South America | Long Term (≥ 4 Years) |

| Skilled-Labour Shortage for VRF Commissioning | -0.3% | North America, Europe, Urban Asia-Pacific | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility of Key Refrigerants (HFC-32, R-410A)

The accelerated phase-down of hydrofluorocarbons under the Kigali Amendment has tightened quarterly quotas by roughly 10% in both the United States and the European Union.[3]United States Environmental Protection Agency, “AIM Act,” epa.gov R-410A still accounts for 60% of the global installed base and has a global warming potential of 2,088, well above the 700 ceiling that applies to new U.S. equipment from 2025. Substitution to R-32 is hindered by a production fire in Zhejiang that removed 15% of capacity and lifted spot prices by 40% during Q1 2025. R-454B offers a lower GWP of 466 but entails compressor redesigns, adding cost and delaying rollouts. Recovery infrastructure is lagging; the United States reclaimed only 35% of refrigerants from retired units in 2024, deepening supply stress.

Stricter SEER/EER Regulations Inflating Upgrade Capex

Minimum performance thresholds are marching upward worldwide. The United States raised SEER2 minimums to 14.3 in northern states and 15.2 in southern zones from January 2026, adding USD 300-600 per unit because of variable-speed compressors and larger heat exchangers. Europe’s Ecodesign Directive now requires a seasonal energy efficiency ratio of 6.1 for small splits, relegating most of today’s stock to grade C or below on the energy label. China’s GB 21455-2024 lifted minimum EER benchmarks by 10% and introduced seasonal metrics that favor inverter architectures.[4]ITC Standards Map, “GB 21455-2024 Standard,” standardsmap.org For emerging-market households, a 20% price hike can push purchase decisions out by a year, especially when ceiling fans cost one-tenth as much. In the commercial sphere, owners often recoup higher upfront costs within seven years, yet small enterprises still face capital constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Mini-Splits Dominate, VRF Systems Accelerate

Mini-split systems accounted for 51.76% of 2025 revenue because ductless retrofits dominate the residential space, where ceiling cavities are shallow and existing wiring is constrained. Variable refrigerant flow units captured a smaller base yet are forecast to outpace at a 5.76% CAGR as office landlords embrace multi-zone demand profiles. The split air conditioner systems market for VRF installations is projected to expand steadily as developers focus on the total cost of ownership rather than the acquisition price. VRF can route refrigerant runs up to 150 m, supporting distributed indoor units without rooftop ductwork. Energy modeling studies from the U.S. Department of Energy show 20-30% lower consumption than rooftop packaged units.

Commercial adopters appreciate VRF’s ability to heat and cool simultaneously, reclaiming waste heat from south-facing zones and lifting system COP above 4.0. Daikin’s VRV X platform extended piping lengths, while Mitsubishi Electric’s CITY MULTI series offers BACnet and Modbus integration for facility managers. The split air conditioner systems market share of VRF is constricted by commissioning complexity that demands technicians proficient in precise refrigerant charging and multi-point leak testing. Labor shortages, especially in North America where 50,000 HVAC vacancies were reported in 2025, continue to cap near-term adoption.

By Application: Commercial Retrofits Accelerate

Residential buyers commanded 66.43% of 2025 installations, driven by an expanding urban middle class and government housing schemes in India and China. Yet commercial retrofits are advancing at 5.43% CAGR, buoyed by smart-office mandates and green-building certification demands. The split air conditioner systems market size in office renovations is growing as facility owners migrate from constant-volume rooftop units to zone-controlled VRF systems. LEED-certified projects in the United States reported that nearly half specified inverter splits or VRF in 2025.

Hotels, hospitals, and co-working centers view predictive maintenance as a service continuity lever, reducing unplanned outages that harm customer satisfaction. Residential decision-making remains cost-sensitive; mini-splits dominate because inverter VRF often exceeds household budgets. Programs such as India’s Pradhan Mantri Awas Yojana pre-wire low-income housing to accept splits post-occupancy, creating pent-up replacement demand. Commercial owners, in contrast, calculate net present value over a 10-15-year horizon, favoring high-efficiency equipment despite higher tickets.

By Cooling Capacity: Larger Units Serve Expanding Floorplates

Units rated 12,001-24,000 BTU held 37.34% of 2025 shipments because the category aligns with typical bedrooms and small retail bays. However, demand for units above 36,000 BTU is set to expand at 5.84% CAGR as open-plan offices and large showrooms proliferate. The split air conditioner systems market share of high-capacity segments is climbing in response to glass façades that amplify solar gain. Inverter modulation makes oversizing unnecessary; a 4-ton unit can throttle down to 30% load, holding setpoints without energy-wasting on-off cycling.

Field measurements run by the U.S. Department of Energy in 2025 showed that inverter splits over 3 tons saved 18-22% electricity versus fixed-speed peers. Software such as EnergyPlus and eQUEST now refine sizing by hour-of-year loads, slashing the historical oversize margin. As building owners retrain staff on software workflows, procurement has begun to shift from conservative oversizing to right-sizing, driving a more granular capacity mix in the overall split air conditioner systems market.

By Technology: Inverter Dominance Solidifies

Inverter equipment accounted for 77.16% of global turnover in 2025 and is growing at a 5.51% CAGR, signaling its establishment as the default architecture for new orders. The split air conditioner systems industry continues to phase out fixed-speed designs because variable-frequency drives reduce electricity use by up to 40% in homes and 25% in offices. Regulatory regimes reinforce the lead: Japan’s Top Runner program and South Korea’s Minimum Energy Performance Standards both require inverter compressors for larger splits.

Compatibility with new refrigerants remains an engineering frontier. R-32 and R-454B demand synthetic oils and upgraded seals, prompting supply-chain coordination between compressor and refrigerant providers. Component costs are declining as scale improves, shrinking the price gap with legacy models and further expanding the split air conditioner market, driven by inverter units.

By Distribution Channel: E-Commerce Disrupts Traditional Models

Multi-brand showrooms still accounted for 42.81% of 2025 revenue, as in-person consultations and bundled installation reassure buyers. Yet online platforms are growing at a 5.67% CAGR as manufacturers deploy direct-to-consumer storefronts. Amazon and Alibaba together control roughly 8-10% of U.S. and Chinese residential split sales, and both offer same-day delivery in major cities.

Installation quality is the stumbling block. Improper vacuuming and charge levels void warranties, so brands now assign certified installers and extend extra warranty years when online purchases are professionally commissioned. Commercial-grade VRF remains within the domain of HVAC contractors because system design requires load calculations and pipe routing. As instructional videos and augmented-reality guides spread, the split air conditioner systems market share for e-commerce is expected to climb within the residential arena while remaining ancillary for complex projects.

Geography Analysis

Asia-Pacific generated 63.31% of global revenue in 2025, reflecting a confluence of population density, rising disposable income, and severe climatic stress. China’s tier-1 cities reach saturation levels above 120 units per 100 households, yet rural penetration is under one-third, leaving ample headroom for replacement and first-time purchases. India recorded 47 days above 45 °C in Delhi during the 2025 summer season, an escalation from 32 days in 2020, and the government opened rebate windows to accelerate inverter adoption. Japan’s mature market now revolves around replacements and the switch to heat-pump splits in northern prefectures, where combined heating-cooling performance drives purchasing.

Africa exhibits the fastest trajectory, with a 6.04% CAGR through 2031, driven by micro-grid electrification and cold-chain expansion. Sub-Saharan Africa’s cooling access gap stood at 78% in 2025, yet donor-funded solar mini-grids are powering clinics and schools, enabling split installations for the first time. Nigeria and Kenya lead cold-chain adoption for vaccines and perishables, specifying small-capacity inverter splits paired with battery storage.

North America and Europe are expanding steadily, driven by replacement cycles and retrofit incentives. The United States struggles with a 50,000-person HVAC technician shortfall that stretches installation lead times. Southern Europe remains cooling-centric, while northern countries adopt reversible heat pumps that cannibalize single-function splits. The Middle East posts the highest per-capita cooling intensity and is tightening SEER regulations above global norms as part of Saudi Vision 2030 VISION2030. South America, led by Brazil, is benefitting from urbanization, though currency fluctuations periodically slow import volumes.

Competitive Landscape

The top 10 manufacturers commanded roughly 55-60% of 2025 revenue, leaving the split air conditioner systems market moderately fragmented. Japanese and South Korean incumbents, Daikin, Mitsubishi Electric, LG, and Samsung, capitalize on compressor patents and global service networks. Chinese firms Gree and Midea exploit vertical integration to undercut rivals while scaling aggressively into Africa and South America. Patent analytics confirm leadership priorities; Daikin leads VRF control innovations with more than 1,200 active filings, Mitsubishi Electric dominates compressor efficiency, and LG concentrates on IoT integration.

Strategically, players focus on three themes: securing low-GWP refrigerant supply, embedding products into proprietary IoT ecosystems, and penetrating under-cooled geographies. Daikin’s acquisition of Goodman strengthened U.S. distribution, while Gree launched photovoltaic-direct-drive units that bypass unstable grids. E-commerce introduces margin compression as manufacturers must differentiate on post-sale support rather than on hardware specifications alone.

Regional specialists are also gaining momentum. Voltas in India emphasizes dust-resistant coatings for high-particle environments and targets ultra-compact outdoor units for dense urban apartments. Competitive intensity will likely escalate as regulatory bans on high-GWP refrigerants force simultaneous product refreshes, leveling the playing field across incumbents and challengers.

Split Air Conditioner Systems Industry Leaders

Daikin Industries, Ltd.

LG Electronics Inc.

Mitsubishi Electric Corporation

Gree Electric Appliances Inc. of Zhuhai

Midea Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daikin committed USD 500 million to expand R-32 refrigerant capacity in Alabama to ease supply constraints and secure a long-term feedstock position.

- December 2025: Mitsubishi Electric introduced the CITY MULTI Z-Series VRF in Europe with a heat-recovery module achieving a COP of 4.2 in simultaneous heating-cooling mode.

- November 2025: LG Electronics integrated ThinQ residential splits with Google Nest for unified smart-home control across North America.

- October 2025: Gree opened a 2-million-unit inverter split plant in Hefei, China, dedicated to R-32 refrigerants.

Global Split Air Conditioner Systems Market Report Scope

The Split Air Conditioner Systems Market Report is Segmented by Equipment Type (Mini-Split, Multi-Split, Variable Refrigerant Flow, Ductless Packaged and Other Equipment Types), Application (Residential, Commercial), Cooling Capacity (≤12,000 BTU, 12,001-24,000 BTU, 24,001-36,000 BTU, >36,000 BTU), Technology (Inverter, Non-Inverter), Distribution Channel (Direct HVAC Contractors/OEM Dealers, Multi-Brand Retail Stores, E-Commerce), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Mini-Split |

| Multi-Split |

| Variable Refrigerant Flow (VRF) |

| Ductless Packaged and Other Equipment Types |

| Residential |

| Commercial |

| Less Than or Equal to 12,000 (1 Ton) BTU |

| 12,001-24,000 (1-2 Ton) BTU |

| 24,001-36,000 (2-3 Ton) BTU |

| Greater Than 36,000 (Greater Than 3 Ton) BTU |

| Inverter |

| Non-Inverter |

| Direct HVAC Contractors / OEM Dealers |

| Multi-Brand Retail Stores |

| E-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Equipment Type | Mini-Split | |

| Multi-Split | ||

| Variable Refrigerant Flow (VRF) | ||

| Ductless Packaged and Other Equipment Types | ||

| By Application | Residential | |

| Commercial | ||

| By Cooling Capacity (Ton) (BTU/hr) | Less Than or Equal to 12,000 (1 Ton) BTU | |

| 12,001-24,000 (1-2 Ton) BTU | ||

| 24,001-36,000 (2-3 Ton) BTU | ||

| Greater Than 36,000 (Greater Than 3 Ton) BTU | ||

| By Technology | Inverter | |

| Non-Inverter | ||

| By Distribution Channel | Direct HVAC Contractors / OEM Dealers | |

| Multi-Brand Retail Stores | ||

| E-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is demand for VRF equipment growing worldwide?

Variable refrigerant flow systems are projected to register a 5.76% CAGR from 2026-2031, the quickest pace within equipment types.

Which region shows the highest future growth potential?

Africa is forecast to achieve a 6.04% CAGR through 2031, underpinned by solar mini-grid electrification and rising heat exposure.

What share do inverter units already command?

Inverter technology controlled 77.16% of global revenue in 2025 and continues to expand faster than the overall market.

Why is e-commerce important for residential splits?

Online channels offer price transparency, virtual sizing tools, and certified installer networks, supporting a 5.67% CAGR for e-commerce sales.

How will refrigerant regulation influence product design?

U.S. and EU bans on high-GWP refrigerants are prompting manufacturers to retool for R-32 and R-454B, raising short-term costs but lowering lifecycle emissions.

What is the main obstacle to faster commercial retrofits?

A shortage of technicians skilled in VRF commissioning delays projects, particularly in North America and Europe.

Page last updated on: