Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

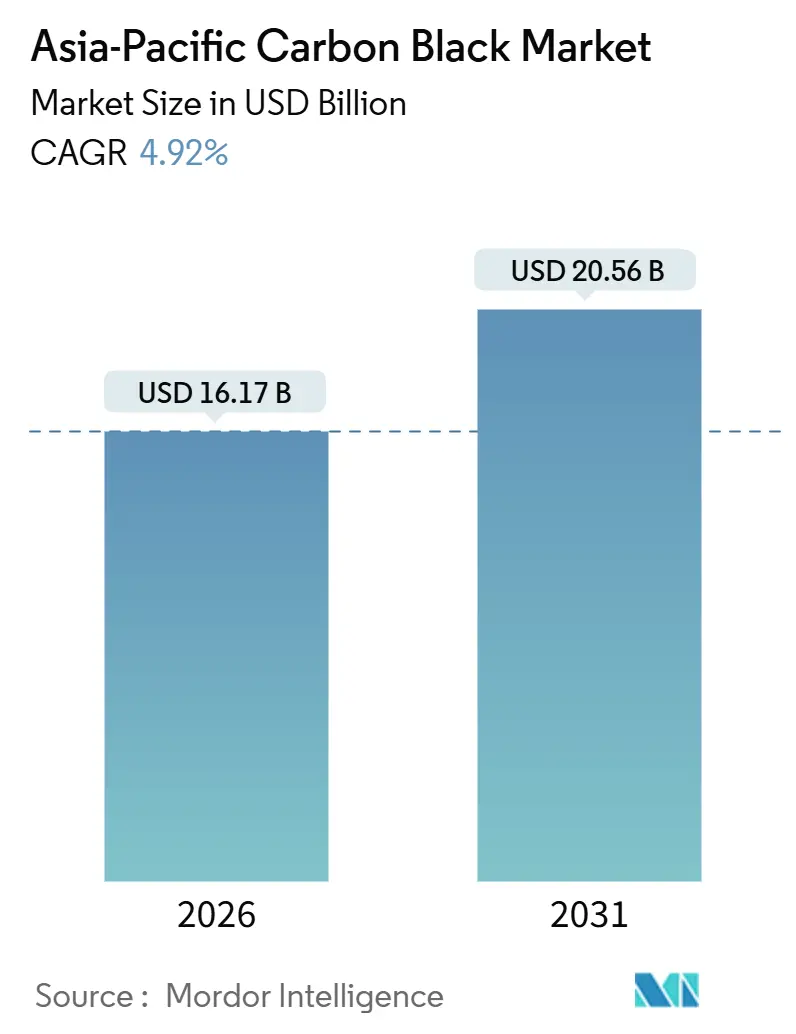

| Market Size (2026) | USD 16.17 Billion |

| Market Size (2031) | USD 20.56 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

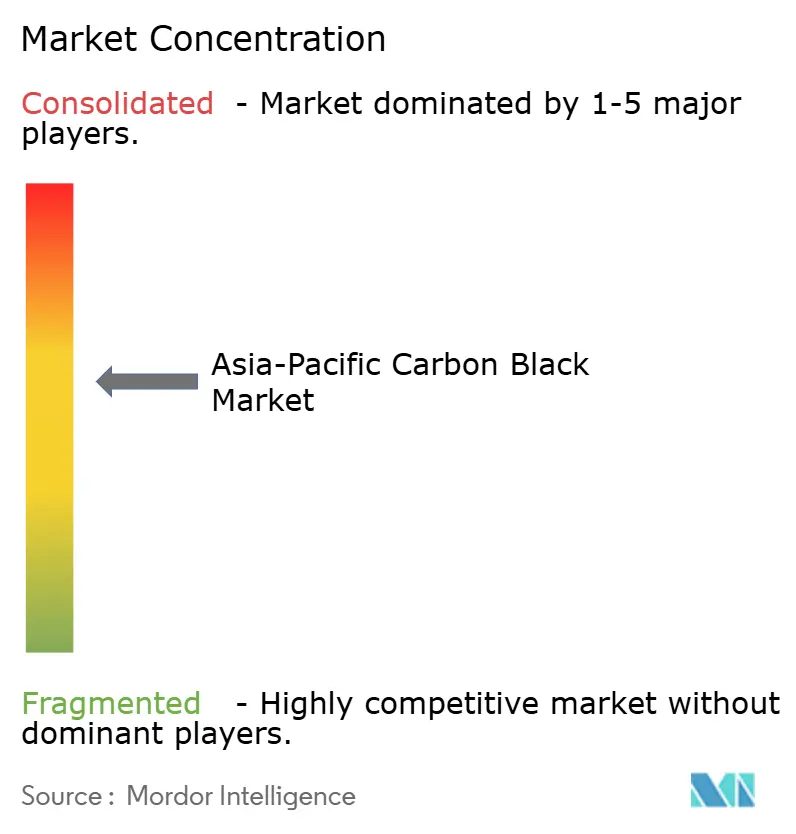

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Carbon Black Market Analysis by Mordor Intelligence

The Asia-Pacific Carbon Black Market size is estimated at USD 16.17 billion in 2026, and is expected to reach USD 20.56 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). The region’s shift from high-volume commodity grades toward specialty blacks that serve electric-vehicle battery casings and high-performance tires is reinforcing margin expansion, while China’s energy-efficiency mandates are accelerating plant modernization and capacity consolidation. Integrated producers with captive feedstock pipelines are cushioning earnings against crude-linked tar price volatility, whereas mid-tier firms are differentiating through recovered-carbon-black and acetylene-black innovations. Demand tailwinds stem from India’s fast-growing two-wheeler and commercial-vehicle tire replacement cycle, expanding regional digital printing output, and stricter battery safety standards that require conductive blacks. Conversely, silica substitution in green tread compounds and tightening sulfur-oxide limits on furnace-black plants weigh on growth, although these restraints are offset by the region’s resilient vehicle-miles-traveled trajectory and policy support for circular-carbon initiatives.

Key Report Takeaways

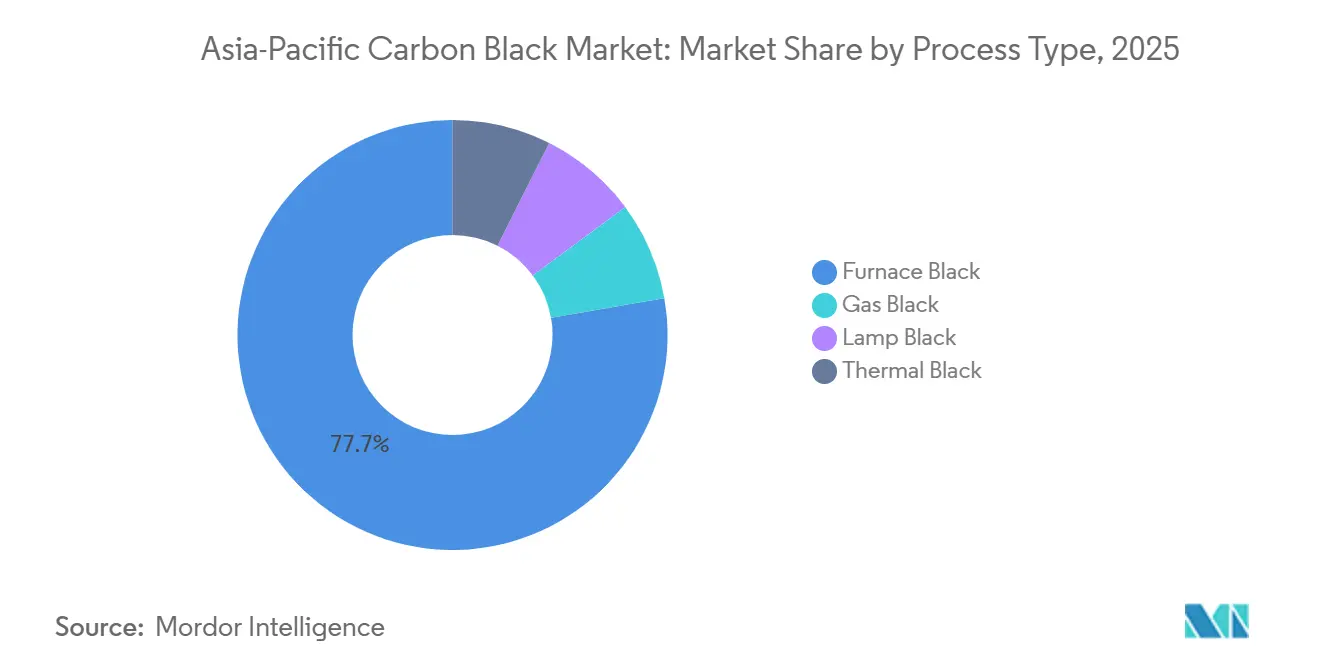

- By process type, Furnace Black held 77.74% of the Asia-Pacific carbon black market share in 2025, whereas Lamp Black is projected to grow at a 5.21% CAGR through 2031.

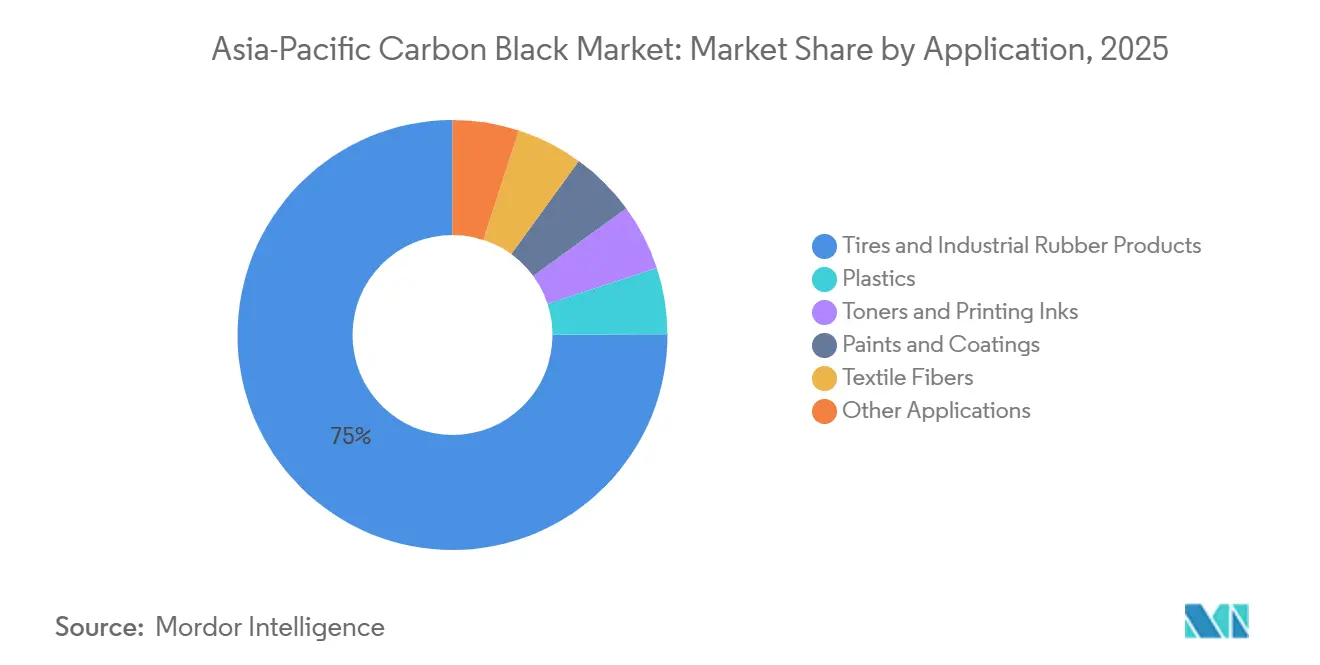

- By application, Tires and Industrial Rubber accounted for 74.89% of the Asia-Pacific carbon black market size in 2025, while Toners and Printing Inks are advancing at a 6.26% CAGR through 2031.

- By geography, China dominated with a 54.18% share in 2025; India is forecast to expand at a 5.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising tire-replacement demand across China and India | +1.2% | China, India, ASEAN core | Medium term (2-4 years) |

| Specialty black uptake in high-performance EV tires | +0.9% | China, Japan, South Korea | Medium term (2-4 years) |

| Regulations phasing out low-grade wet-granulation units | +0.7% | China, spillover to ASEAN | Short term (≤ 2 years) |

| Recovered carbon black mandates in Japan and South Korea | +0.5% | Japan, South Korea | Long term (≥ 4 years) |

| OEM shift to conductive blacks for Li-ion battery casings | +0.8% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Tire-Replacement Demand Across China and India

China and India together consume over 60% of regional tires, yet their replacement cycles differ. China’s mature passenger-car fleet generates steady aftermarket pull for high-abrasion grades, while India’s expanding commercial-vehicle and two-wheeler base underpins faster incremental volume. CRISIL projects India’s tire-replacement demand to rise 7-8% in fiscal 2026, supported by infrastructure spending and higher freight tonnage. The International Monetary Fund expects Asia-Pacific GDP to grow 4.6% in 2025, adding road-travel demand and tire wear. Phillips Carbon Black Limited is enlarging its Mundra facility to capture this growth and coastal export opportunities, evidencing producer confidence in sustained aftermarket momentum.

Specialty Black Uptake in High-Performance EV Tires

Electric vehicles need tires that balance low rolling resistance with greater load-bearing capacity. Cabot’s 2024 PROPEL E8 grade lowers hysteresis by 15% relative to traditional N200 series blacks, enabling tire makers to reduce silica content without compromising wet traction. Goodyear’s supply agreement with Monolith Materials, also announced in 2024, sources methane-pyrolysis carbon black that cuts production emissions by 90%, aligning with OEM Scope 3 carbon accounting. Tokai Carbon reported JPY 37.4 billion in segment sales during Q3 2024 and is co-developing a recovered-carbon-black line with Bridgestone, showing that specialty grades lift average selling prices by 20-30% even though they represent less than 5% of volume.

Regulations Phasing Out Low-Grade Wet-Granulation Units

China’s GB 29449-2024 caps energy use in carbon-black production at 3,200 kWh per tonne, a threshold older wet-granulation lines exceed by 20-30%. The 2024 pollutant-discharge permit system layers real-time monitoring for sulfur dioxide and particulates, driving compliance costs higher[1]Ministry of Ecology and Environment, “2024 Pollutant-Discharge Permit Measures,” mee.gov.cn. Longxing Chemical reported RMB 2.89 billion revenue in the first half of 2024 and credited margin gains to the closure of 12 competing lines in Shandong, illustrating how regulation is lifting the Herfindahl index. As the top five Chinese producers now hold 65% of domestic capacity, energy standards are hastening consolidation that favors scale players with dry-pellet technology.

Recovered Carbon Black Mandates in Japan and South Korea

Japan’s Ministry of Economy, Trade and Industry targets 10-15% substitution of virgin carbon black with recovered grades by 2030[2]Ministry of Economy, Trade and Industry, “Carbon Recycling Roadmap 2024,” meti.go.jp . Bridgestone and Tokai Carbon formed a joint venture in 2024 to build a 5,000-tonne-per-year facility, scheduled for fiscal 2032. South Korea’s 2024 Framework Act on Resources Circulation imposes extended producer responsibility on tire makers, spurring investments such as Marubeni’s USD 15 million stake in LD Carbon to boost output to 10,000 tonnes by 2027. Although pyrolysis material carries higher ash and broader particle-size distribution, its 30-40% lower carbon intensity supports adoption in medium-performance applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-derived feedstock prices | -0.8% | Global, import-dependent ASEAN | Short term (≤ 2 years) |

| Growing silica substitution in green tread compounds | -0.6% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Stricter SOx/NOx emission caps on furnace black plants | -0.5% | China, spillover to India and ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Derived Feedstock Prices

Carbon black relies on fluid catalytic-cracking tar and coal-tar pitch whose prices track Brent benchmarks with a 2-3-month lag. The World Bank projects Brent at USD 64 per barrel in 2025 and USD 60 in 2026. A USD 10 swing moves feedstock costs 8-10%, compressing producer margins by up to 300 basis points when pass-through lags OEM contracts. Himadri Specialty Chemical disclosed that coal-tar-pitch volatility shaved 150 basis points off gross margin in Q2 2024. ASEAN producers that import 70-80% of tar feedstock saw landed costs surge 12% in H1 2024 due to freight spikes and currency depreciation, underlining how crude swings destabilize smaller, non-integrated players.

Growing Silica Substitution in Green Tread Compounds

Silica paired with silane agents reduces tire rolling resistance by up to 35%, improving fuel economy and meeting fleet-average standards. Evonik’s ULTRASIL system demonstrated 8% fuel-saving gains in testing, prompting passenger-car tire makers to adopt 30-50% blends. Tokai Carbon’s 2024 annual report estimated a 15,000-20,000-tonne demand loss in Japan from silica substitution. Biosilica from rice-husk ash, validated in a 2024 Journal of Applied Polymer Science study, is widening supply and pushing prices down. Carbon-black producers are developing hybrid blacks grafted with silica, but these niche grades have not stemmed share erosion in passenger tires, which represent the bulk of demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace Black Retains Volume Leadership

Furnace Black accounted for 77.74% of Asia-Pacific carbon black market share in 2025 and continues to anchor bulk demand among tire and industrial-rubber users. Lamp Black, though smaller in tonnage, is forecast to expand at 5.21% CAGR through 2031 as ink and coating formulators value its ultra-fine particle size and lower polycyclic-aromatic content. Thermal and Gas Blacks, together below 5% of volume, serve high-purity plastics and conductive coatings where large or ultra-fine particles are critical.

Major producers are investing in oxidation and encapsulation to widen the performance envelope of furnace grades, yet the capital cost limits widespread adoption. China’s GB 29449-2024 energy cap is accelerating the retirement of inefficient wet-granulation lines, which consumed 20-30% more power, thereby shifting volume to integrated firms with dry-pellet technology. Birla Carbon’s 2024 Raven 1185 Ultra launch shows how Lamp Black can secure premium niches in digital printing. Meanwhile, Orion’s PRINTEX 3 gas black dominates magnetic toner applications, demonstrating specialty demand resilience despite its small share.

By Application: Tires Dominate, Toners Accelerate

Tires and Industrial Rubber consumed 74.89% of regional carbon black in 2025, supported by a replacement cycle that is still expanding in India and by high-abrasion requirements for Chinese truck retreads. Toners and Printing Inks are the fastest-growing segment at 6.26% CAGR to 2031, propelled by rising digital press installations across packaging and commercial print shops. Plastics secure 8-10% of volume in conductive fuel lines and electrostatic-dissipative parts for electric vehicles, while Paints and Coatings absorb specialty blacks for automotive basecoats and low-VOC architectural finishes. Textile fibers remain a small but stable outlet.

DIC’s iron-treated carbon black patent delivers 30% higher magnetic saturation, illustrating how formulation advances unlock speed gains in copiers. Cabot’s PROPEL E8 demonstrates that application-specific reinforcement can offset silica encroachment by cutting hysteresis without sacrificing wet grip. Plastics users in ASEAN are adopting conductive blacks to meet ISO 23907 electrostatic standards for fuel systems that took effect in 2024. Surface-treated lamp blacks that disperse in waterborne paints align with China’s 2024 volatile-organic-compound limits, sustaining specialty demand growth despite a commodity-heavy base.

Geography Analysis

China consumed 54.18% of regional carbon black in 2025, anchored by the world’s largest tire manufacturing hub and a mature replacement cycle that pulls over 1.2 million tons annually. The Asia-Pacific carbon black market size for China is consolidating as GB 29449-2024 and pollutant-discharge permits force sub-scale plants to shut or modernize, pushing the top five players’ combined share to 65%. Integrated coal-chemical groups supply aromatic feedstock at transfer prices below spot, reinforcing cost leadership.

India is set to post the region’s fastest growth at 5.10% CAGR through 2031, underpinned by commercial-vehicle and two-wheeler tire demand where carbon-black intensity per unit exceeds passenger cars. Phillips Carbon Black Limited’s Mundra expansion will add 50,000 tons by 2027, positioning the firm to serve both domestic OEMs and Middle-Eastern exports. The Asia-Pacific carbon black market benefits from India’s coastal logistics that lower freight costs and shorten shipping times to Gulf customers.

Japan’s market is flat as shrinking passenger-car output and silica substitution erode volume, yet the country remains a technology leader in recovered and acetylene blacks that command 20-30% premiums. South Korea’s Framework Act on Resources Circulation is expected to divert 5,000-8,000 tons of virgin demand toward pyrolysis-derived substitutes by 2028. ASEAN economies - Indonesia, Thailand, Vietnam, and Malaysia - are witnessing rising demand for carbon black, with Indonesia’s tire industry absorbing up to 100,000 tons of imports each year. The Rest of Asia-Pacific, including Australia and Taiwan, represents specialty niches reliant on imports from Japan and South Korea.

Competitive Landscape

The Asia-Pacific carbon black market is moderately consolidated. Vertical integration provides feedstock security and shields margins from tar volatility, as seen in Birla Carbon’s captive distillation units and Jiangxi Black Cat’s coal-chemical parent. Specialty-grade innovation is the main competitive lever; Orion’s acetylene-black expansion in South Korea targets fast-growing battery-casing demand, while Cabot’s PROPEL E8 responds to EV tire specifications. White-space opportunities lie in recovered-carbon-black and bio-based feedstocks. Technology gaps are widening: leaders deploy machine-learning controls to fine-tune particle-size distributions, whereas laggards run legacy batch systems with 10-15% higher energy use. Regulatory tightening will force sub-100,000-tonne producers, especially in ASEAN, to either modernize or exit by 2028, further lifting regional concentration.

Asia-Pacific Carbon Black Industry Leaders

Birla Carbon

Jiangxi Black Cat Carbon Black Co., Ltd.

Cabot Corporation

Orion Engineered Carbons

Tokai Carbon Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Bridgestone and Tokai Carbon agreed to build a 5,000-tonne recovered-carbon-black facility in Japan, targeting 10-15% blend ratios in domestic tire plants.

- September 2024: Phillips Carbon Black Limited announced a 50,000-tonne capacity expansion at Mundra, India, scheduled for completion in 2027.

- August 2024: Cabot Corporation introduced PROPEL E8, a specialty black for EV tires that lowers hysteresis by 15% versus N200 grades.

Asia-Pacific Carbon Black Market Report Scope

Carbon black is a fine carbon powder made by the incomplete combustion or thermal decomposition of gaseous or liquid hydrocarbons under controlled conditions. It is extensively used as a color pigment in paints and inks and as a reinforcing filler in rubber products.

The Asia-Pacific carbon black market is segmented by process type, application, and geography. By process type, the market is segmented into furnace black, gas black, lamp black, and thermal black. By application, the market is segmented into tires and industrial rubber products, plastics, toners and printing inks, paints and coatings, textile fibers, and other applications. The report also covers the market size and forecasts across 4 countries in the Asia-Pacific region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Process Type

| Furnace Black |

| Gas Black |

| Lamp Black |

| Thermal Black |

By Application

| Tires and Industrial Rubber Products |

| Plastics |

| Toners and Printing Inks |

| Paints and Coatings |

| Textile Fibers |

| Other Applications |

By Geography

| China |

| India |

| Japan |

| South Korea |

| ASEAN Countries |

| Rest of Asia-Pacific |

| By Process Type | Furnace Black |

| Gas Black | |

| Lamp Black | |

| Thermal Black | |

| By Application | Tires and Industrial Rubber Products |

| Plastics | |

| Toners and Printing Inks | |

| Paints and Coatings | |

| Textile Fibers | |

| Other Applications | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific carbon black market in 2026?

The Asia-Pacific carbon black market size reached USD 16.17 billion in 2026 and is forecast to rise to USD 20.56 billion by 2031.

Which process segment leads regional volume?

Furnace Black dominates with a 77.74% share in 2025, reflecting its cost advantage and suitability for tire reinforcement.

What is the fastest-growing application through 2031?

Toners and Printing Inks are expanding at a 6.26% CAGR as digital printing scales across packaging and commercial print.

Why is India outpacing China in growth?

India’s commercial-vehicle and two-wheeler replacement cycles are earlier in maturity, delivering a 5.10% CAGR versus China’s mature market.

How are regulations impacting smaller producers?

Energy-efficiency and emission caps in China and circular-carbon mandates in Japan and South Korea are raising compliance costs, pressuring sub-scale plants to modernize or exit.

What opportunity does recovered carbon black provide?

Policy targets in Japan and South Korea aim for 10-15% substitution by 2030, opening premium niches for producers that master pyrolysis material processing.

Page last updated on: