Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

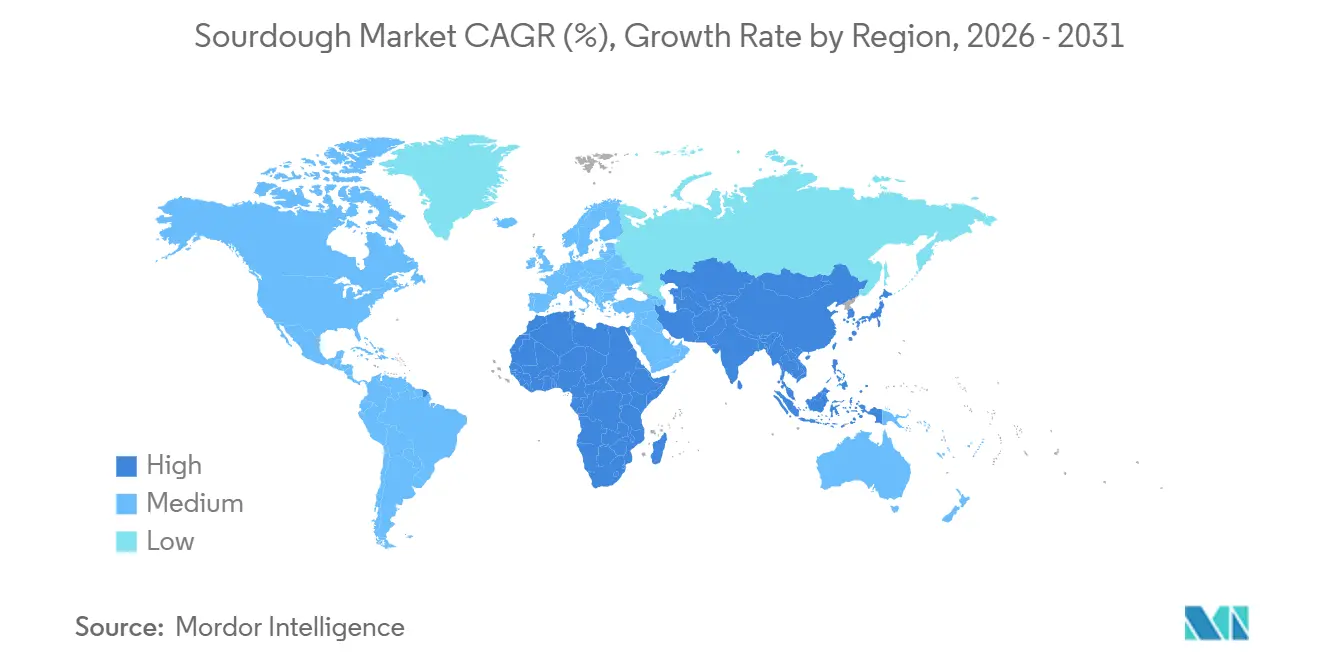

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

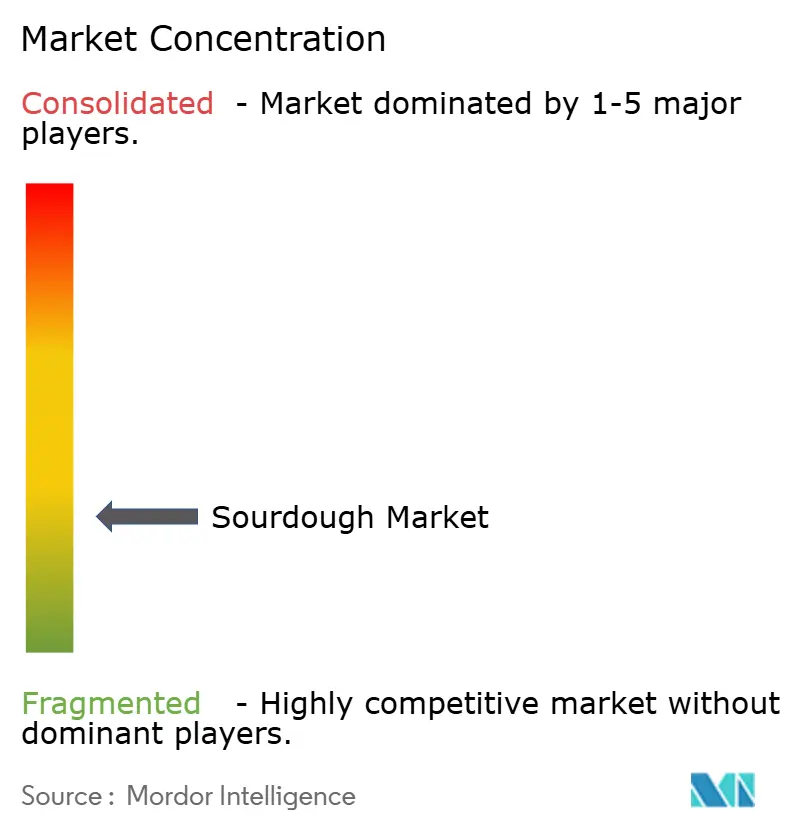

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sourdough Market Analysis by Mordor Intelligence

The sourdough market size is expected to increase from USD 3.24 billion in 2025 to USD 3.45 billion in 2026 and reach USD 4.69 billion by 2031, growing at a CAGR of 6.33% over 2026-2031. The growth is driven by the rising demand for naturally fermented bread, which is perceived as healthier and more flavorful. Supportive food-safety regulations in North America and the European Union further contribute to this trend. Industrial bakeries are expanding their offerings with ready-to-bake sourdough products, while artisan producers focus on traditional methods such as long fermentation and heritage grains to justify higher prices. Technological advancements in spray- and freeze-drying processes are improving the shelf life of sourdough starters, making it easier to distribute them across borders and reducing the risk of spoilage. Meanwhile, rapid urbanization in the Asia-Pacific region is driving the adoption of Western-style bakery products, making it the fastest-growing market for sourdough globally. The market remains highly fragmented.

Key Report Takeaways

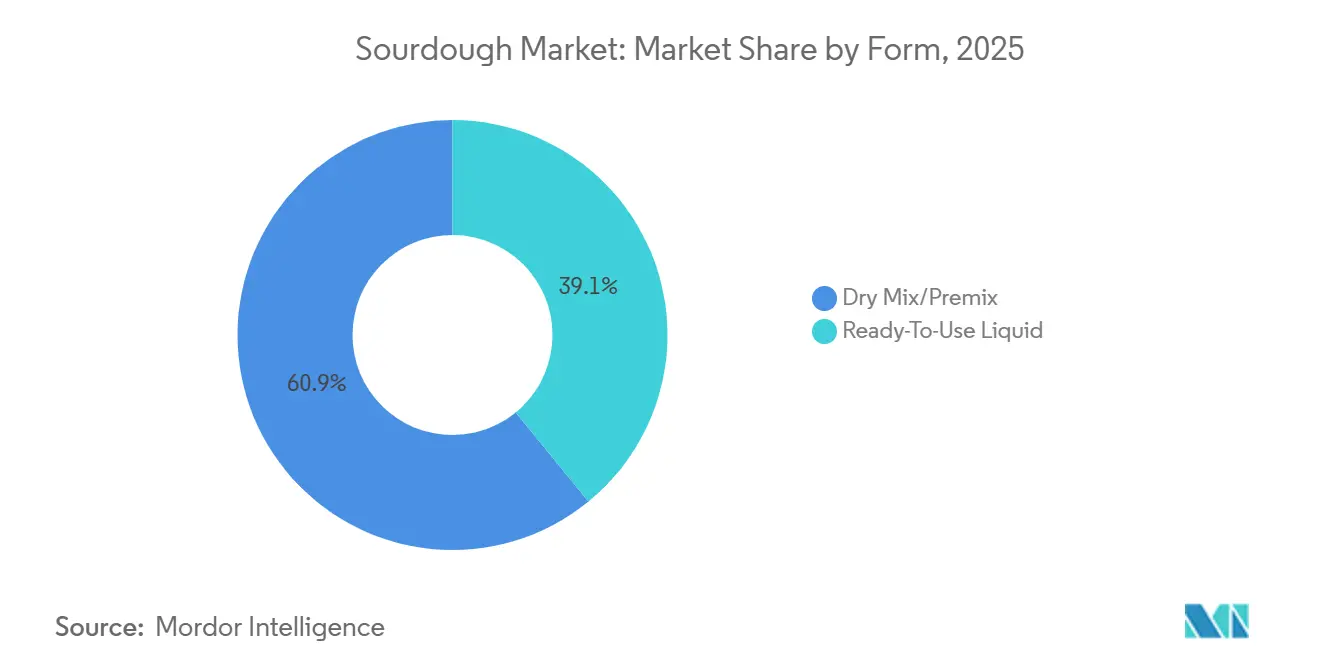

- By form, dry mix/premix captured 60.89% of the sourdough market share in 2025, whereas ready-to-use liquid formats are projected to grow at a 7.21% CAGR through 2031.

- By processing type, type III powder held the largest revenue share at 43.10% in 2025, while type II dried sourdough is forecast to expand at a 7.55% CAGR to 2031.

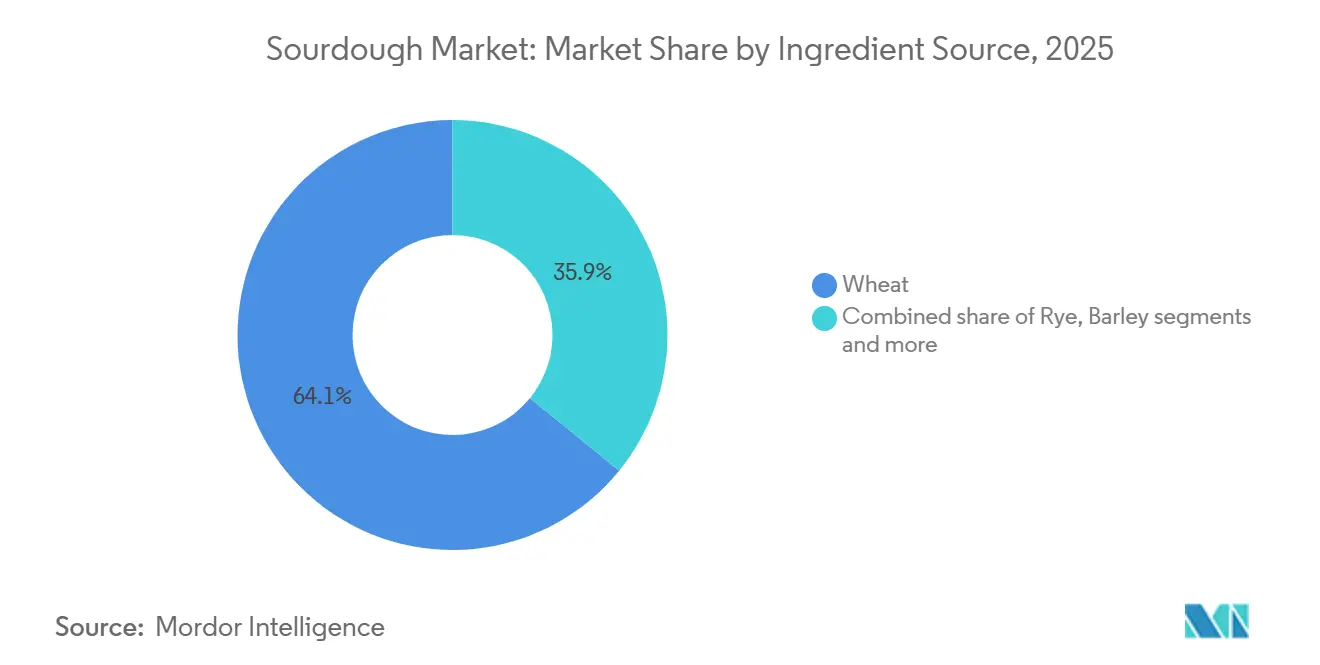

- By ingredient source, wheat-based variants accounted for 64.12% of the sourdough market size in 2025, and rye leads future growth with a 7.05% CAGR over 2026-2031.

- By application, breads and buns dominated with 59.85% revenue share in 2025; pizza crust is set to advance at an 8.05% CAGR through 2031.

- By distribution channel, retail outlets held 67.95% share of the sourdough market size in 2025, whereas foodservice is the fastest-rising channel at 7.70% CAGR.

- By geography, Europe led with 34.01% revenue share in 2025, and Asia-Pacific is positioned for the highest 8.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Sourdough Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of perceived health benefits associated with sourdough, such as easier digestibility and lower glycemic response | +1.2% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Clean-label and minimal ingredient preference | +0.9% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Innovation in sourdough product formats, including packaged loaves, snacks, and ready-to-bake options | +0.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising participation in baking and home fermentation trends | +0.5% | North America and Europe, declining in United Kingdom but stable in United States/Canada | Short term (≤ 2 years) |

| Expansion of premium bakery offerings across retail and foodservice channels | +1.0% | Global, with Asia-Pacific and Middle East showing accelerated growth | Long term (≥ 4 years) |

| Growing consumer focus on gut health and digestive wellness driving demand for naturally fermented sourdough products | +1.1% | Global, particularly strong in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing awareness of perceived health benefits associated with sourdough, such as easier digestibility and lower glycemic response

Awareness of the health benefits of sourdough is driving the market's growth. Sourdough bread has a glycemic index of approximately 55, which is close to the low glycemic threshold of 50 or less. This makes it a preferred choice for individuals looking to manage their blood sugar levels effectively, as highlighted by the Cleveland Clinic in July 2024[1]Source: Cleveland Clinic, "Is Sourdough Bread Healthy for You?", health.clevelandclinic.org. The natural fermentation process used in sourdough production not only makes it easier to digest but also enhances nutrient absorption, making it appealing to health-conscious consumers. With the increasing prevalence of lifestyle-related health issues such as diabetes and obesity, there is a growing demand for bakery products that are functional and have a low glycemic index. In response, bakeries and ingredient manufacturers are introducing a wider range of sourdough products that focus on promoting digestive health and balanced nutrition.

Rising participation in baking and home fermentation trends

The growing interest in baking and home fermentation is driving the sourdough market. Consumers are increasingly drawn to artisanal and homemade foods, boosting the popularity of sourdough products. A survey conducted by the Agriculture and Horticulture Development Board in February 2025 revealed that 11% of people in the United Kingdom baked at least once a week, while 20% baked at least once a month[2]Source: Agriculture and Horticulture Development Board, "Baking Trends in 2024: To Bake Or To Buy, That Is The Question", ahdb.org.uk. This highlights consumers' consistent engagement in home baking. As a result, demand for sourdough starters, premixes, and fermentation ingredients has steadily risen, and these products are widely available at retail and specialty stores. Furthermore, more people are becoming aware of the benefits of natural fermentation, clean-label food options, and traditional baking techniques. This growing awareness has encouraged consumers to try sourdough baking at home, further expanding the market.

Growing consumer focus on gut health and digestive wellness is driving demand for naturally fermented sourdough products.

Consumers are increasingly focusing on gut health and digestive wellness, driving growth in the global sourdough market. Digestive diseases affect a significant portion of the population, with the National Institute of Diabetes and Digestive and Kidney Diseases reporting in October 2025 that around 60 to 70 million people in the United States suffer from such conditions[3]Source: National Institute of Diabetes and Digestive and Kidney Diseases, "Digestive Diseases Statistics for the United States", niddk.nih.gov. This has led to a rising demand for foods that promote better digestion. Sourdough, made through natural fermentation, produces compounds that make it easier to digest and help maintain a healthy balance of gut bacteria. As a result, bakeries and ingredient manufacturers are marketing sourdough as a healthier and gut-friendly option in the bakery segment. Growing awareness about the importance of digestive health and preventive nutrition is expected to further boost the demand for sourdough products worldwide, as consumers increasingly seek functional foods that support overall well-being.

Innovation in sourdough product formats, including packaged loaves, snacks, and ready-to-bake options

Innovation in sourdough product formats is significantly driving market growth by making sourdough products more accessible and versatile. Companies are expanding beyond traditional fresh bread to offer convenient options such as ready-to-bake kits, frozen dough, and packaged sourdough snacks. These innovations aim to meet the growing demand for easy-to-use, longer-lasting products. For example, in 2024, East Pizzas in the United Kingdom introduced 48-hour fermented retail pizza bases, providing consumers with a premium-quality product that is convenient for home use. Similarly, leading bakery companies like Bimbo Bakeries and Flowers Foods have launched sliced sourdough bread enriched with protein and fiber, targeting health-conscious consumers. These developments are helping manufacturers reach a broader audience while meeting the demand for both convenience and health-focused options.

Restraints Impact Analysis of Sourdough Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensitivity of sourdough cultures to temperature and humidity | -0.7% | Global, particularly challenging in tropical and subtropical regions (Southeast Asia, Latin America, Sub-Saharan Africa) | Medium term (2-4 years) |

| Competition from faster-rising yeast-based and packaged bread alternatives | -0.9% | Global, most acute in price-sensitive emerging markets (India, Indonesia, Nigeria) | Short term (≤ 2 years) |

| Longer fermentation cycles increase production complexity and constrain scalability | -0.8% | Global, affecting both artisan bakeries and industrial producers | Long term (≥ 4 years) |

| Higher retail prices compared to conventional bread | -0.6% | Global, with strongest impact in emerging markets and lower-income consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensitivity of sourdough cultures to temperature and humidity

The sensitivity of sourdough cultures to temperature and humidity is a significant challenge for the sourdough market, as stable fermentation conditions are crucial for maintaining consistent product quality. The main bacteria in sourdough, Lactobacillus sanfranciscensis, thrive within a specific temperature range of 28 °C to 32 °C. Any deviation from this range or exposure to low humidity can slow down microbial activity, weaken the starter, and negatively impact the final product. This issue is particularly problematic in regions with extreme weather conditions, such as high heat or excessive humidity, where maintaining optimal fermentation conditions becomes difficult. To address this, bakeries often rely on specialized fermentation chambers and controlled production environments. However, these solutions come with high costs, making it especially challenging for smaller or artisanal bakeries to adopt them.

Competition from faster-rising yeast-based and packaged bread alternatives

Competition from faster-rising yeast-based alternatives poses a significant challenge to the growth of the global sourdough market. Yeast-based bread offers key advantages, such as quicker production times and lower costs. Unlike sourdough, which requires a long fermentation process that can take several hours or even days, yeast-based bread can be produced in just a few hours. This faster production process allows manufacturers to increase output and meet higher demand more efficiently. The cost difference between sourdough and yeast-based bread impacts consumer choices, especially in price-sensitive regions like India and Indonesia. In these markets, conventional white bread made with yeast is much more affordable, making it the preferred option for most consumers. This affordability ensures that yeast-based bread remains a staple in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Sourdough Market Segment Analysis

By Form:

Dry Formats Dominate, Liquid Variants AccelerateDry mix and premix products held the largest share of the sourdough market in 2025, accounting for 60.89% of the total market. These products are popular due to their longer shelf life, ease of storage, and convenience compared to traditional sourdough starters. They ensure consistent fermentation results, making them a preferred choice for commercial bakeries and large-scale food manufacturers. Premixes simplify the baking process by reducing preparation time and minimizing technical challenges. This convenience has driven their widespread use across both developed and emerging markets, furthering their dominance.

Ready-to-use liquid sourdough products are expected to grow at a CAGR of 7.21% between 2026 and 2031, driven by increasing demand for authentic flavors and artisanal-quality baked goods. These products save time by eliminating the need for fermentation preparation while delivering consistent taste and texture. They are particularly popular in premium bakery applications, such as specialty breads and clean-label products, which align with consumer preferences for natural and minimally processed ingredients. The growing availability of these products through commercial bakeries and foodservice channels is further boosting their adoption, contributing to their strong growth during the forecast period.

By Processing Type:

Powder Leads, Dried Formats SurgeType III powder starters accounted for 43.10% of sourdough market revenue in 2025, primarily due to their suitability for high-speed industrial production. These starters can be directly added to automated mixing systems, helping save time and boost efficiency in large-scale operations. Their consistent composition ensures uniform flavor, texture, and fermentation quality across different production sites. This makes them a preferred choice for commercial bakeries and packaged food manufacturers that prioritize reliability and scalability. The growing need for standardized and efficient production processes continues to drive the dominance of this segment.

Type II dried starters are projected to grow the fastest, with a CAGR of 7.55% through 2031. Recent advancements in spray drying and freeze-drying technologies have enhanced the ability to preserve flavors and maintain the viability of microorganisms. These improvements ensure better fermentation performance while retaining the authentic sourdough taste. Additionally, the extended shelf life and ease of transportation make dried starters ideal for global distribution. The rising demand for stable and high-quality sourdough solutions, both in industrial-scale baking and artisanal production, is expected to fuel the growth of this segment significantly.

By Ingredient Source:

Wheat Dominates, Rye RisesWheat-based sourdough accounted for 64.12% of total revenue in 2025. This dominance is primarily due to the widespread availability of wheat and its well-established global supply chains. Wheat sourdough is highly favored for its soft texture, versatile use in various bakery products, and familiar taste. The presence of advanced milling infrastructure ensures consistent flour quality, making it suitable for large-scale production. Commercial bakeries also prefer wheat sourdough for its reliable fermentation, further solidifying its leading position in the market.

Rye-based sourdough is expected to grow at a CAGR of 7.05% through 2031, driven by increasing consumer interest in health and nutrition. Rye is rich in fiber and has a lower glycemic index, which helps regulate blood sugar levels, making it a healthier option for many consumers. Its natural prebiotic properties also promote better digestive health, enhancing its appeal among health-conscious buyers. Furthermore, the rising demand for artisanal and specialty breads is boosting the adoption of rye-based sourdough. As awareness of its nutritional benefits grows, rye sourdough is anticipated to gain a stronger foothold in the market.

By Application:

Bread Anchors, Pizza Crust OutpacesBreads and buns made up 59.85% of the sourdough market revenue in 2025, making them the most significant application of sourdough fermentation. These products are widely consumed across both retail and foodservice channels, ensuring steady demand. Sourdough improves the flavor, texture, and shelf life of breads and buns, making it a preferred choice for both artisan and packaged breads and bunsrising consumer interest in natural and fermented ingredients is encouraging manufacturers to incorporate sourdough into. Its tangy taste and unique crumb structure appeal to consumers, especially those seeking premium and clean-label bakery options. This strong consumer preference continues to drive the dominance of breads and buns in the sourdough market.

Pizza crust is projected to grow at a CAGR of 8.05% between 2026 and 2031, fueled by increasing demand for artisanal and high-quality pizza options. Sourdough-based crusts offer a better texture, richer flavor, and easier digestion than traditional dough. The growing popularity of specialty pizza chains and gourmet foodservice outlets is further boosting the adoption of sourdough crusts. Additionally, the rising interest in natural and fermented ingredients among consumers is encouraging manufacturers to use sourdough in pizza recipes. These factors are expected to drive significant growth in the pizza crust segment during the forecast period.

By Distribution Channel:

Foodservice Ascends Amid Menu PremiumizationRetail channels, such as supermarkets, hypermarkets, and online stores, made up 67.95% of the sourdough market revenue in 2025. This dominance is due to the easy availability of sourdough products and their visibility to consumers. Many supermarkets now offer in-store bakery programs that produce fresh sourdough daily, attracting customers and allowing retailers to charge higher prices for artisan-quality products. The growing demand for both fresh and packaged sourdough items has boosted retail sales. The expansion of organized retail networks, especially in emerging markets like Latin America and Southeast Asia, is further driving growth in this segment.

The foodservice sector is expected to grow at the fastest rate, with a projected CAGR of 7.70% through 2031. Restaurants, cafes, and specialty bakeries are increasingly incorporating sourdough into their menus to stand out and offer premium options. Sourdough’s traditional fermentation process and artisanal appeal add value for consumers, making it a popular choice. The recovery of the foodservice industry after the pandemic has also contributed to this growth. As more consumers seek premium dining experiences and naturally fermented bakery products, the foodservice segment is likely to see sustained demand in the coming years.

Geography Analysis

Western Europe Sourdough Market

Europe contributed 34.01% of the sourdough market revenue in 2025, driven by its strong baking traditions and recognition of natural fermentation processes by regulators. Countries like Germany, France, and the United Kingdom have a high demand for sourdough, as consumers prefer products made with heritage grains and artisanal techniques. Western Europe benefits from well-established bakery networks and premium product positioning, which maintain steady growth. Meanwhile, Eastern Europe is seeing new opportunities with the introduction of convenient options like ready-to-bake kits. These factors ensure Europe remains a key player in the global sourdough market while gradually expanding into emerging areas.

APAC Sourdough Market

The Asia-Pacific region is the fastest-growing market, with a CAGR of 8.60% through 2031. Rapid urbanization and the expansion of the bakery industry are driving demand for sourdough, especially as consumers increasingly show interest in premium, fermented bakery products. Global and regional ingredient suppliers are investing in the region through acquisitions and training programs to strengthen their presence. Countries like China, India, and Australia are seeing a rise in organized bakeries, boosting sourdough adoption. Additionally, the growing popularity of artisanal bakery products in urban areas is further fueling market growth in this region.

The Americas and MEA Sourdough Market

North America continues to see steady growth in the sourdough market, supported by consumer interest in artisanal baking and fermented foods. Major commercial bakeries are driving innovation, while strong retail distribution networks ensure product availability. In Latin America, sourdough is gradually gaining traction, particularly in premium bakery segments and among urban consumers. The Middle East and Africa are also experiencing growth, supported by expatriate communities and the modernization of bakery operations. Investments in controlled production environments and the expansion of bakery infrastructure are helping producers meet the rising demand for artisanal products in these regions.

Regulatory Landscape

In the European Union, traditional sourdough is generally treated as a non-novel food based on documented consumption prior to 15 May 1997, which supports broad commercialization of classic sourdough breads and starter-derived ingredients. At the same time, there is no harmonized legal definition of "sourdough" across the EU or the United Kingdom, so product naming and claims typically need to align with general food information rules, including Regulation (EU) No 1169/2011 for ingredient disclosure, and with industry codes of practice, such as guidance from FEDIMA and UK industry initiatives. This keeps the need for substantiated on-pack communication around fermentation, starter use, and ingredient composition in focus.

Controls around additives and cross-border movement of preparations also affect formulation and trade. In January 2026, the EU published Commission Regulation (EU) 2026/196, updating purity specifications and related criteria for several commonly used additives, including hydrocolloids used for texture and stability, with applicability from February 2026 and transition periods extending to 2028. That change is expected to prompt audits of sourdough mixes and ready-to-use liquid products that include stabilizers. In the United Kingdom, HM Revenue and Customs guidance classifies liquid sourdough starter as a complex food preparation (CN 2106 90 98) rather than flour or a pure culture, so correct customs classification remains relevant for importers of liquid formats, alongside the 2024 updates to additives and novel foods rules that tightened limits such as ethylene oxide residues in authorized additives.

Competitive Landscape

The sourdough market is highly fragmented, with both large multinational ingredient manufacturers and smaller regional or artisan producers playing key roles. Major companies such as Puratos Group, Lesaffre International, Lallemand Inc., IREKS GmbH, and Ernst Böcker GmbH dominate the global supply of starter cultures, premixes, and fermentation solutions. These companies leverage their strong research capabilities, extensive distribution networks, and established partnerships with commercial bakeries to maintain their market position. Meanwhile, smaller bakeries contribute to the market's diversity by offering regionally specialized products and catering to local tastes.

Large ingredient manufacturers are focusing on strategies like vertical integration, acquisitions, and product innovation to strengthen their market presence. By investing in advanced fermentation technologies, proprietary starter cultures, and scalable production methods, they ensure consistent product quality and operational efficiency. These companies are also responding to consumer demand for clean-label and health-focused products by offering natural fermentation solutions. Their ability to support large-scale production gives them a competitive edge in meeting the needs of industrial bakeries and commercial operations.

On the other hand, artisan bakeries differentiate themselves by focusing on traditional techniques, unique flavors, and premium-quality products. They often use heritage grains and locally sourced ingredients to appeal to consumers seeking authentic and high-quality sourdough. However, smaller producers face challenges in scaling their operations and maintaining consistent production conditions. Despite these limitations, the rise of online bakery platforms and specialty retail channels is creating new opportunities for artisan producers to reach niche markets and cater to the growing demand for premium sourdough products.

Sourdough Industry Leaders

-

Puratos Group

-

Lesaffre International

-

Lallemand Inc.

-

IREKS GmbH

-

Ernst Böcker GmbH

- *Disclaimer: Major Players sorted in no particular order

Sourdough Market Companies Covered in this Report

- Puratos Group

- Lesaffre International

- Lallemand Inc.

- IREKS GmbH

- Ernst Böcker GmbH

- AB Mauri

- GoodMills Group

- Alpha Baking Co. Inc.

- Truckee Sourdough Company

- Philibert Savours

- Semifreddi’s Bakery

- Morabito Baking Company

- Bread SRSLY

- Backaldrin International

- Dr. Otto Suwelack GmbH & Co. KG

- Peak Rock Capital (Gold Coast Bakery)

- Riverside Sourdough

- The Health Factory

- Seven Stars Bakery

- Emu AG

Market Opportunities and Future Outlook

Industrialization of sourdough is creating room for suppliers that can deliver consistent fermentation at scale, especially through dry premixes and stabilized cultures that reduce operational complexity associated with handling live starters. The market already reflects that dry formats dominate, with dry mix/premix accounting for 60.89% share in 2025. Technology upgrades such as spray-drying and freeze-drying are also improving starter shelf life and enabling broader cross-border distribution, supporting expansion into organized retail and foodservice networks that prioritize repeatable quality.

Process control and data-driven fermentation are another area where industrial bakeries can differentiate, particularly when targeting clean-label positioning while maintaining throughput. Industry activity includes showcasing sourdough mixes engineered for frozen stability and handling tolerance, such as Lallemand Baking Solutions presenting new sourdough mixes for pizza applications at Pizza Expo 2026, along with continued uptake of controlled fermentation equipment and automation to limit batch variability. With Europe holding 34.01% share in 2025 and Asia-Pacific identified as the fastest-growing region, suppliers that combine standardized starter formats with training, application support, and fermentation control capabilities are positioned to align with premiumization in retail bakeries and menu differentiation in foodservice, including faster-growing applications such as pizza crust.

Recent Industry Developments in Sourdough Market

- March 2026: Puratos Group announced a definitive agreement to acquire Dawn Foods, a global bakery ingredients supplier, subject to regulatory approvals, with closing targeted by the end of 2026. The combination broadens Puratos' reach across bakery ingredient solutions, strengthening its ability to supply industrial and artisan customers that use sourdough starters, mixes, and related fermentation inputs. It also raises competitive pressure on other global ingredient suppliers as customers consolidate sourcing for clean-label and fermented bakery ranges.

- June 2025: Lesaffre announced an exclusive global license and collaboration agreement with MicroBioGen to drive innovation in baking and broader food markets using yeast biotechnology. The partnership reinforces the strategic importance of fermentation R&D and performance consistency, which can translate into improved starter and culture solutions that support scalable sourdough production. It also signals continued investment in differentiated microbial capabilities alongside conventional bakery ingredient portfolios.

- May 2024: Puratos Group launched Sapore Lavida, described as Belgium's first fully traceable active sourdough, produced using 100% wholewheat flour linked to regenerative agriculture cooperatives. The launch adds a premium, provenance-led option for bakers targeting sustainability and transparency requirements in Europe. It also highlights a pathway for sourdough ingredient suppliers to compete beyond functionality, using traceability and farming practices as product differentiators.

Sourdough Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the sourdough market is defined as the value generated from selling sourdough starter and sourdough ingredients used to make sourdough-based baked foods across retail, food processing, and foodservice channels, measured in USD.

Scope exclusions: We exclude at-home baking equipment and non-sourdough yeast and improvers that are not directly sold as sourdough inputs.

Segments Covered in This Report

-

By Form

- Ready-To-Use Liquid

- Dry Mix/Premix

-

By Processing Type

- Type I (Fresh)

- Type II (Dried)

- Type III (Powder)

-

By Ingredient Source

- Wheat

- Rye

- Barley

- Others (Oats, etc.)

-

By Application

- Breads and Buns

- Cakes and Pastries

- Pizza Crust

- Cookies and Crackers

- Others

-

By Distribution Channel

- Food Processing Industry

- Foodservice

-

Retail

- Supermarkets/Hypermarkets

- Online Stores

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the market to repeatable public signals that explain how sourdough demand forms in each region. We reviewed official food production and trade statistics, then linked them to bakery consumption behavior and ingredient usage patterns.

Sources used typically included USDA datasets, Eurostat, FAOSTAT, national customs and trade statistics portals, and peer-reviewed food science journals that discuss fermentation, shelf life, and formulation shifts. We also used company annual reports, investor presentations, association and bakery federation publications, and reputed press coverage to map product launches and route-to-market changes. In addition, a paid subscription for company financials and news, plus a paid patent database, supported revenue cross-checks and helped spot new processing and drying technologies. The desk sources listed here are illustrative and not exhaustive, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test how sourdough is actually bought and used, since the same label can mean different things across bakery formats and channels. We spoke with ingredient suppliers, bakery operators, distributors, and category managers across APAC, EMEA, and the Americas to confirm conversion factors, pricing direction, and the share of sourdough used by application.

These discussions also helped us close gaps from desk research, such as how much demand is met through dry mixes versus ready-to-use formats, and how industrial usage differs from artisan usage in everyday procurement.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 20% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach once, where bakery production and consumption indicators were used to reconstruct the addressable sourdough demand pool by region, and then split by form and application based on observed usage and channel presence. To keep the totals realistic, we corroborated the results with selective bottom-up approximations such as sampled supplier revenue ranges, a price-per-kg check for dry and liquid formats, and volume proxies tied to bakery throughput.

Inputs that mattered most in the model included bread and bakery output trends, penetration of sourdough-style products in packaged and fresh bakery shelves, mix shift between dry and ready-to-use formats, average selling price movement by form (including inflation pass-through timing), and channel mix between retail, food processing, and foodservice. When a country-level indicator was missing, we used adjacent proxy series, for example related bakery output measures, and validated the implied ratios through primary feedback.

For forecasting, scenario analysis was applied around a base case that reflected likely adoption in packaged bakery, premiumization in artisan offerings, and stability of wheat and rye input costs. The final trajectory was checked against expert expectations so near-term price and penetration assumptions did not drift away from what buyers and suppliers are planning.

Data Validation & Update Cycle

Validation was done through several checks, starting with basic variance tests across regions and applications so any unusual jumps were flagged early. We compared outputs with independent signals like bakery production direction, trade flows for relevant ingredient categories, and observed pricing in packaged bakery and ingredient listings.

Before sign-off, the model is reviewed in steps, and outliers trigger re-checks of conversion factors and price assumptions. If the gap is still not explained, we re-contact selected respondents. Reports are refreshed annually, and interim updates are made when material events affect demand or pricing. Right before delivery, a final analyst pass is completed so clients receive the most current view available.

Mordor Intelligence's Sourdough Market Estimate Compared With Other Published Estimates

Published market sizes for sourdough can differ more than expected because the product boundary is not always treated the same, and the year used as the starting point is also not consistent. Differences show up quickly when one estimate is closer to retail baked goods value, and another is closer to ingredient and starter value that feeds multiple bakery applications.

Bakery output signals, application mix checks, and price tracking by dry versus liquid formats are used as evidence to keep Mordor Intelligence's 2026 estimate tied to an ingredient-led demand pool, instead of counting the full shelf value of sourdough-branded baked products.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.45 B (2026) | |

| Industry Publisher A | USD 2.86 B (2024) | Uses a different base year and a longer horizon, and the scope appears to blend broader sourdough product categories without the same form-by-form price checks, which can compress the near-term value. |

| Industry Publisher B | USD 3.30 B (2023) | Anchors sizing earlier and may reflect a wider baked goods framing in parts of the scope, which can lift the starting value depending on how finished-product revenue is counted versus ingredient demand. |

Across the three figures, the spread is mainly explained by starting year choice and how closely the market boundary is kept to sourdough inputs versus sourdough-branded finished foods. By tying the model to observable bakery volume direction, form-level pricing, and application allocation, the estimate stays transparent and can be rechecked with the same steps each update cycle.

Key Questions Answered in the Report

How large will the global sourdough market be by 2031?

Forecasts show the global sourdough market size reaching USD 4.69 billion by 2031, up from USD 3.45 billion in 2026.

Which region offers the fastest growth for sourdough products?

Asia-Pacific is projected to post an 8.60% CAGR through 2031, driven by urbanization and Western bakery adoption.

What product form leads sales in sourdough?

Dry Mix/Premix formats dominate with 60.98% revenue share in 2025 due to their shelf stability and ease of use.

Why are rye-based sourdough breads gaining attention?

Rye offers higher prebiotic fiber and lower glycemic response than wheat, spurring a 7.05% CAGR for rye sourdough products.

Page last updated on: