Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

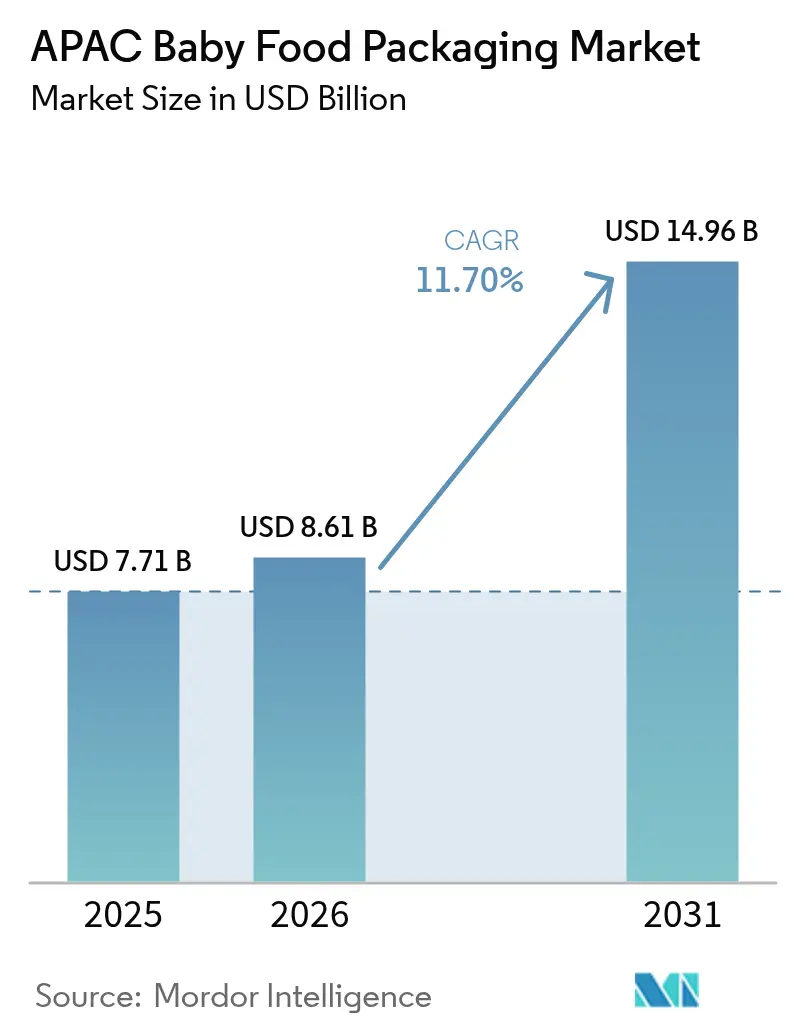

| Base Year Market Size (2025) | USD 7.71 Billion |

| Market Size (2026) | USD 8.61 Billion |

| Market Size (2031) | USD 14.96 Billion |

| Growth Rate (2026 - 2031) | 11.70% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

APAC Baby Food Packaging Market Analysis by Mordor Intelligence

The APAC Baby Food Packaging Market size is expected to grow from USD 7.71 billion in 2025 to USD 8.61 billion in 2026 and is forecast to reach USD 14.96 billion by 2031 at 11.70% CAGR over 2026-2031. This expansion reflects the region’s demographic momentum, strong urbanization and the growing preference for premium infant nutrition. Rising birth registrations during China’s Year of the Dragon lifted super-premium infant formula sales by 44.3%, while H&H Group captured 15.6% share of that price tier.[1]NutraIngredients-Asia, “H&H Group rebounds from low infant formula sales in China in Q1,” nutraingredients-asia.com Material innovation is another growth catalyst. Plastic retained 46.7% revenue share in 2024, yet bioplastics are climbing fastest at 18.4% CAGR, supported by NatureWorks’ USD 600 million Ingeo PLA complex in Thailand scheduled for 2025. Convenience-led pouches already hold 33% share and are growing at 15.9% CAGR, reshaping packaging line investments and retail shelf layouts. Geographic concentration remains evident as China commands 35% share, while India is registering the quickest 14% CAGR through 2030. E-commerce sales of baby food packaging accelerate at 19.4% CAGR, forcing a pivot toward shipping-robust, lighter formats that minimize breakage and dimensional weight.

Key Report Takeaways

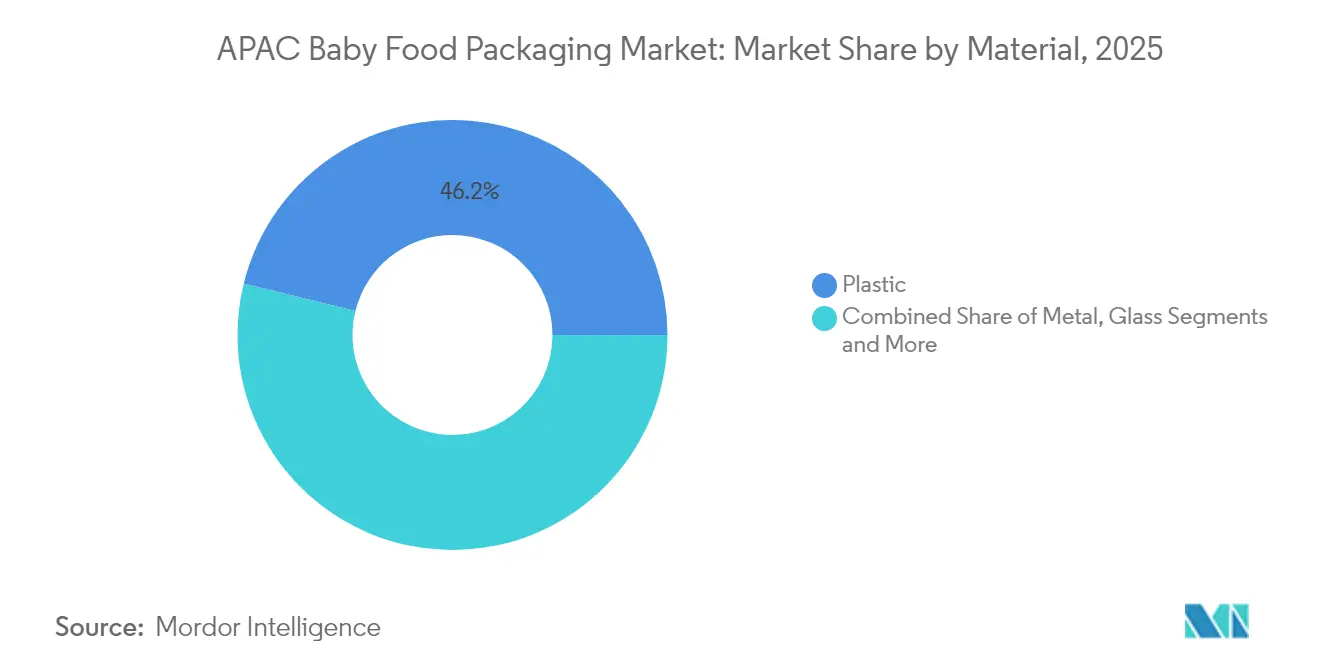

- By material, plastic led with 46.15% of the APAC baby food packaging market share in 2025; bioplastics are forecast to expand at an 17.85% CAGR through 2031.

- By package type, pouches accounted for 32.55% revenue share in 2025 and are projected to advance at a 15.35% CAGR to 2031.

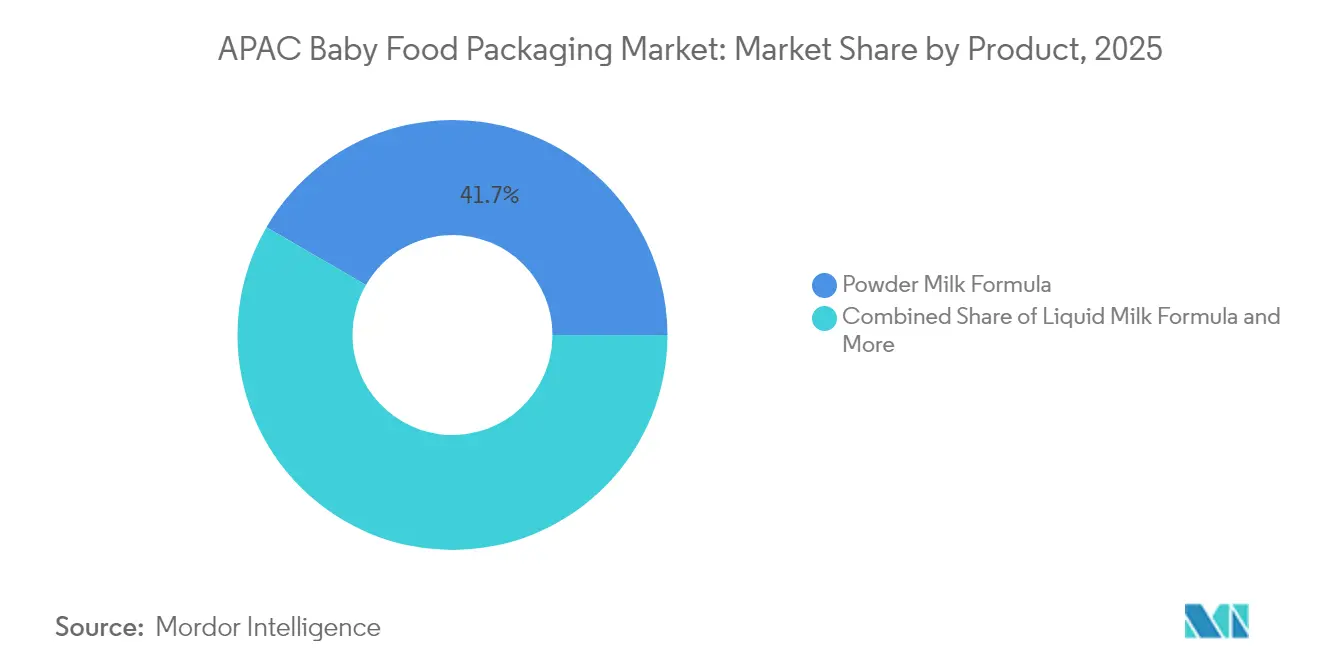

- By product, powder milk formula held 41.65% share of the APAC baby food packaging market size in 2025, while snacks and finger foods are expected to grow at a 14.55% CAGR through 2031.

- By age group, 6-12 months captured 38.62% share in 2025; the 2-3 years cohort is estimated to rise at a 13.95% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 45.95% share in 2025, whereas online retail is poised for 18.85% CAGR growth through 2031.

- By country, China retained 34.65% share in 2025, while India is forecast to register a 13.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

APAC Baby Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for packaged baby food & infant formula | +3.2% | China, India, Southeast Asia | Medium term (2-4 years) |

| Rising dual-income urban households | +2.8% | Urban centers across APAC | Long term (≥ 4 years) |

| Expansion of organised retail & e-commerce | +2.1% | China, India, Indonesia, Thailand | Short term (≤ 2 years) |

| Brand-led shift toward convenience pouch formats | +1.9% | Global APAC | Medium term (2-4 years) |

| Government subsidies for bio-based packaging lines | +1.4% | Thailand, Vietnam, Malaysia | Long term (≥ 4 years) |

| OEM investment in in-house flexible converting capacity | +1.1% | China, India, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for packaged baby food and infant formula

China’s infant formula segment stayed resilient in 2024 as foreign brands logged 8% sales growth, with the super-premium tier securing 37% share.[2]China International Import Expo, “Several foreign infant formula brands see strong growth in China in 2024,” ciie.org Parents in urban APAC favor products that guarantee safety, extended shelf life and superior nutrition, prompting demand for multi-layer barrier films and premium finishes. Generational wealth transfer brings millennial purchasing power that privileges convenience and perceived quality over homemade alternatives. Urban-rural divides remain, yet metropolitan centers have become high-density demand clusters.

Rising dual-income urban households

Households with two earners value packaging that supports hectic routines. Spouted pouches enable on-the-go feeding, easy resealability and reduced mess, aligning with parental expectations. Affluence in South Korea and Singapore accelerates adoption of premium, portion-controlled packs, while Vietnam and Indonesia are beginning to mirror the trend as female labor participation rises. Brands are therefore prioritizing ergonomic shapes, soft-touch laminates and quick-open closures suitable for one-hand use.

Expansion of organised retail and e-commerce

Digital commerce is scaling at 19.4% CAGR, reshaping distribution physics. Packages require higher drop-test thresholds and optimized cube efficiency to survive courier networks. Direct-to-consumer brands use e-commerce to bypass shelf competition, so on-pack graphics must convey trust and quality during thumbnail-level browsing. In markets like Indonesia, rising supermarket penetration still contributes to volume growth, yet omnichannel models dominate strategic planning.

Brand-led shift toward convenience pouch formats

Pouches captured more than 30% share globally, led by Cheer Pack designs that integrate tamper-evident, no-spill spouts.[3]Cheer Pack North America, “Food & Beverage — Baby Food,” cheerpack.com For producers, lighter weight means lower logistics emissions and shelf-count maximization. Custom silhouettes and photo-realistic printing upgrade shelf impact, while aseptic filling widens application scope. Developed APAC economies exhibit rapid pouch uptake whereas glass jars maintain relevance in certain niche or gifting occasions.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent bans on single-use plastics | -2.3% | India, Southeast Asia, Australia | Short term (≤ 2 years) |

| Volatility in food-grade resin pricing | -1.8% | Global APAC | Short term (≤ 2 years) |

| Cultural preference for home-cooked baby food | -1.5% | Rural APAC, traditional markets | Long term (≥ 4 years) |

| Recycling-infrastructure gaps across emerging SE-Asian economies | -1.2% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent bans on single-use plastics

India mandates 30% recycled content by 2025 in many rigid categories, forcing accelerated R&D and qualification cycles.[4]Lorax EPI, “Revolutionising packaging: The rise of post-consumer recycled content,” loraxcompliance.com Producers face added costs for certified PCR resin and tighter specifications on migration and odor. Parallel measures in Singapore and Indonesia add complexity for multinational supply chains that must juggle differing compliance deadlines.

Volatility in food-grade resin pricing

Polyethylene and polypropylene each rose multiple cents per pound in late 2024 amid feedstock tightness. Such swings compress converter margins and disrupt pricing commitments to brand owners. Several packagers hedge by forward-buying or diversifying into bio-resin blends, but smaller firms struggle to absorb the volatility. Investment in digital procurement platforms and long-term offtake agreements is therefore rising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics drive sustainable transformation

Plastic dominated the APAC baby food packaging market in 2025 with 46.15% revenue share. Bioplastics, however, are charting an 17.85% CAGR to 2031, supported by Thailand’s pro-investment regime and multinational brand pledges on carbon neutrality. The APAC baby food packaging market size for bioplastics is expected to grow the fastest as capacity from NatureWorks and SKC reduces cost differentials with petro-based polymers. Government subsidies in Thailand and Vietnam lower capital thresholds, while improved processability allows bio-based PLA and PBAT films to match heat resistance and sealing integrity of conventional flexibles.

Price sensitivity still limits uptake in several emerging economies, yet premium and organic baby food brands are using compostable packs as a brand story. Glass maintains relevance in luxury gifting, yet its weight and fragility reduce competitiveness in e-commerce. Metal can demand is retreating in favor of lighter barrier laminates. Paperboard, often coupled with bio-barrier coatings, retains a niche for premium secondary packs.

By Package Type: Pouches revolutionize convenience

Pouches held 32.55% share of the APAC baby food packaging market in 2025. They are forecast to expand at 15.35% CAGR, propelled by spouted designs that support independent toddler feeding. The APAC baby food packaging market size for pouches is therefore widening more quickly than rigid formats. Bottles stay important for ready-to-drink formula, but SIG and Tetra systems now compete with mono-material flexibles that claim lower carbon footprints. Metal cans are losing shelf appeal due to weight penalties and are being displaced in club stores by stand-up pouches with fitments that offer similar barrier levels.

Manufacturers appreciate the logistics benefits of pouches, which reduce inbound freight volumes and warehouse space. Retailers gain faced-up shelf density and improved sell-through as consumers embrace the lighter format. Sachets remain a cost-effective option in Indonesia and the Philippines, where single-use affordability trumps sustainability concerns. Jars persist for premium organic purées but are trending toward lightweight PET rather than glass.

By Product: Snacks drive category expansion

Powder milk formula led with 41.65% share in 2025, underpinning the category’s scale. Snacks and finger foods show a 14.55% CAGR thanks to parents prioritizing motor skill development and taste exploration. Flexible pouches with nitrogen flushing maintain crispness and portion control, while canisters with peel-off foil offer tamper evidence. Dried baby food remains popular in Japan and Korea due to reconstitution convenience. Liquid milk formula registers lower growth because its higher transport cost and shorter shelf life favor domestic supply, whereas powder formats dominate export trade.

Brand owners increasingly launch organic rice puff sticks and fruit-vegetable melts that carry higher profit margins. Packaging must therefore balance oxygen barrier with dispersion convenience, driving multi-layer film innovation. Specialized nutrition SKUs for allergy management and sensitive digestion are also on the rise, often requiring opaque high-barrier laminates to protect probiotic efficacy.

By Age Group: Toddler segment accelerates growth

The 6-12 months cohort retained 38.62% share in 2025, reflecting the traditional weaning window when solid food is introduced. The 2-3 years segment is projected to climb at 13.95% CAGR as brands extend portfolios into developmental nutrition. Pouch formats with textured nozzles encourage self-feeding and sensory exploration, while resealable cups support portion flexibility. The APAC baby food packaging market share by age group suggests packaging sizes diversify, with single-serve packs targeting infants and multi-serve tubs aimed at toddlers.

Extended breastfeeding trends keep the 0-6 months segment steady rather than rising. The 1-2 years group experiences moderate growth as cross-over snacks blur the line between toddler and mainstream categories. Safety features such as choke-proof caps and tamper rings remain mandatory across all ages, yet ergonomic design is most pronounced for the actively mobile 2-3 years group.

By Distribution Channel: E-commerce transforms retail

Supermarkets and hypermarkets delivered 45.95% of 2025 value, yet online retail is growing fastest at 18.85% CAGR. The APAC baby food packaging market size attributable to e-commerce necessitates designs that resist compression and temperature swings. Drop-testing standards for courier networks are stricter than for palletized retail, influencing material choices such as thicker pouch laminates or HDPE bottles with impact modifiers.

Click-and-collect models blend brick-and-mortar with digital convenience, so secondary packaging must carry clear QR codes and damage-resistant labels that survive multiple handling points. Pharmacies remain trusted outlets for specialty formulas and therapeutic nutrition, demanding premium blister seals and traceability codes. Convenience stores in metro transit hubs cater to immediate needs with small-format SKUs. Direct-to-consumer subscription boxes provide predictable demand which helps packagers optimize production runs.

Geography Analysis

China retained 34.65% share of the APAC baby food packaging market in 2025 and remains the innovation center for barrier films tailored to super-premium formula. The super-premium tier achieved 37.00% share that year, while foreign brands enjoyed 8% sales growth despite demographic softness. Packaging suppliers benefit from China’s stringent GB 4806.15-2024 adhesive rules effective February 2025, which raise safety benchmarks and foster demand for high-purity raw materials. Investment in closed-loop recycling is also growing, as local governments prioritize waste reduction and consumers show heightened eco-concerns.

India is forecast to post a 13.75% CAGR to 2031, supported by rapid urbanization and dual-income families. Dhunseri Group earmarked INR 22 billion (USD 254.4 million) for PET film capacity expansion by 2029 that will underpin domestic supply. Regulatory frameworks are modernizing as FSSAI tightened labeling obligations in June 2024, prompting packagers to adopt clearer nutrition panels. E-commerce growth in tier-two and tier-three cities widens access, while competitive pricing dynamics favor flexible packs over rigid glass.

Southeast Asia forms a patchwork of opportunities. Thailand benefits from USD 600 million NatureWorks and USD 19.3 billion Braskem Siam bio-chem projects that anchor a regional biopolymer hub. Vietnam attracts biodegradable plastic ventures and shows strong e-commerce uptake. Indonesia and the Philippines record high birth rates, but recycling infrastructure deficits restrain sustainable material rollouts. Malaysia’s amendment of Food Regulations 1985 in 2025 and Thailand’s new labeling mandate issued in 2024 raise compliance hurdles. Across the bloc, rising disposable income and smartphone penetration reinforce demand for premium packaging aligned with digital retail.

Regulatory Landscape

Regulation in the Asia-Pacific baby food packaging market is tightening around food-contact safety, infant-specific labeling, and material restrictions, which is pushing brand owners and converters toward higher-purity inputs and stronger compliance documentation. In China, GB 4806.15-2024 tightened requirements for food-contact adhesives effective February 2025, and the national standard GB 10770-2025 for canned complementary foods for infants and young children entered into force on March 16, 2026, replacing GB 10770-2010. China also released T/CFCA 0040-2026 (General Requirements for Children's Prepackaged Food) on February 2, 2026, implemented from March 2, 2026, indicating broader standardization beyond infant formula into children's packaged food categories.

In India, FSSAI's compendium for infant nutrition requires infant foods to be packed in hermetically sealed, clean containers or appropriate flexible materials, and it specifies BPA-free packaging expectations for infant nutrition. This reinforces material selection and supplier qualification needs. Australia and New Zealand continue to operate under FSANZ Standard 2.9.1 (Infant formula products), with a transitional period for labeling and packaging variations running from September 13, 2024, to September 13, 2029, creating a defined compliance window for redesigns and inventory transitions for regional SKUs.

Competitive Landscape

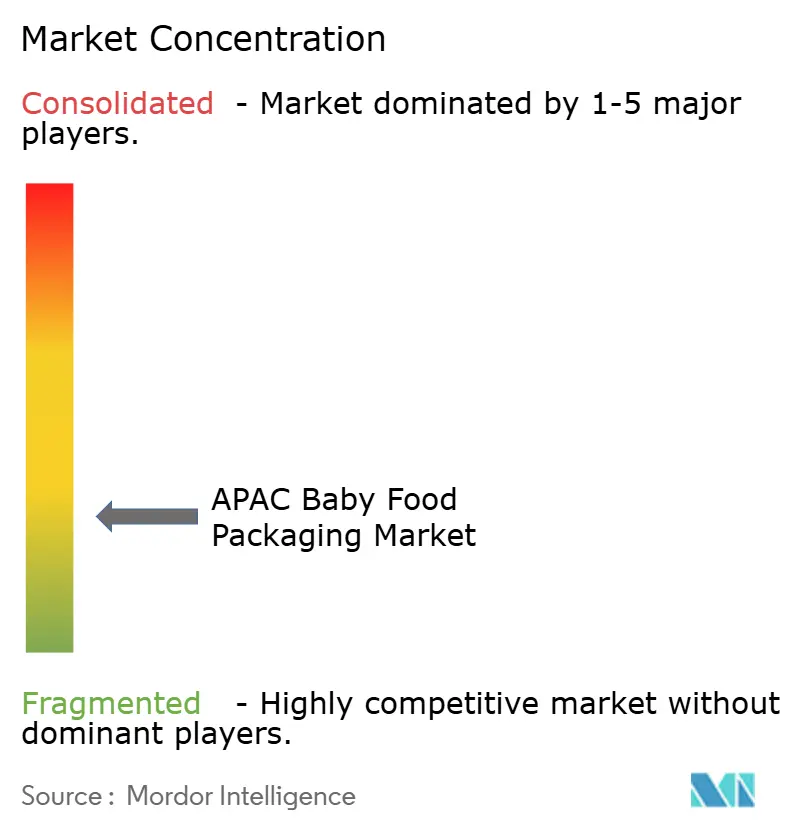

The APAC baby food packaging market is moderately consolidated. Amcor’s USD 8.4 billion purchase of Berry Global, finalized in April 2025, created an entity with 400 plants across 140 countries and USD 650 million synergy potential. Scale expansion allows deeper R&D budgets for recyclable laminates and barrier papers. Huhtamaki, Tetra Laval and SIG intensify competition through proprietary coating and aseptic filling technologies that enhance nutrient protection while shrinking pack weight.

Sustainability steers rivalry. Firms race to secure patents on bio-based or mono-material structures that meet emerging collection systems. Amcor’s AmFiber Performance Paper patent granted in January 2025 underscores the strategic value of IP in low-carbon packaging. Smaller disruptors such as Accredo Packaging exploit agility to launch sugarcane-based pouches that comply with USDA Biobased labeling. Partnerships between converters and biotech companies are common, linking fermentation science with extrusion competency.

Vertical integration gains traction as OEMs bring printing and lamination in-house to mitigate resin price shocks. Investment in robotics and vision systems improves line speeds and defect detection, reducing downtime and ensuring food safety. Digital watermarking pilots in Japan and South Korea enable pack traceability and facilitate sortation for recycling. White-space opportunities persist in child-resistant closures for supplement lines, smart temperature indicators for cold-chain monitoring and subscription-ready ship-in-own-container formats.

APAC Baby Food Packaging Industry Leaders

Amcor PLC

Huhtamaki Oyj

Aptar Group Inc.

Berry Global Inc.

DS Smith Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Infant-nutrition regulations and public scrutiny on packaging safety are creating whitespace for verified low-migration, BPA-free, high-barrier structures and upgraded quality assurance systems across flexible and rigid formats. India’s FSSAI infant nutrition requirements for hermetically sealed packs and BPA-free packaging, together with country-level plastic restrictions in parts of APAC, support demand for redesigned laminates, controlled-odor PCR pathways where feasible, and alternative substrates that still meet barrier and sealing performance for formula, purees, and snacks.

Pouch format growth is also intersecting with material-safety concerns, shaping procurement and innovation priorities. In May 2026, Greenpeace reported microplastic findings in plastic squeeze pouches used by major brands (including Nestle Gerber and Danone Happy Baby Organics), and subsequent industry coverage broadened attention on pouch material selection, liner choices, and particle-shedding risk controls. In this setting, opportunities center on mono-material retortable pouches, paper-based or fiber-hybrid solutions with functional barriers where validated, and closure and fitment designs that improve tamper evidence and reduce contamination risks while maintaining e-commerce durability and drop resistance.

Recent Industry Developments

- May 2026: China implemented GB 10770-2025 for canned complementary foods for infants and young children, replacing GB 10770-2010 and raising the bar for compliant packaging and product protection. The change reinforces demand for verified food-contact materials, tighter quality controls, and pack integrity suited to infant and toddler foods.

- June 2025: Japan launched a Positive List system for synthetic resins in food contact materials, increasing compliance requirements for resin selection and documentation. Packaging suppliers serving baby food brands faced added validation work to ensure material eligibility and audit readiness.

- June 2024: India’s FSSAI tightened labeling obligations, prompting infant nutrition brands to revisit label layouts and information hierarchies on primary and secondary packaging. The update accelerated adoption of clearer on-pack communication and traceability-oriented print features across organized retail and online channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of packaging used to pack baby food sold across Asia Pacific, counted across common materials and formats (for example, pouches, cartons, jars, cans, and bottles) for infant formula and baby food products.

Scope exclusions: We exclude baby food product value, feeding accessories, and bulk transport packaging that is not used as the consumer pack.

Segmentation Overview

- By Material

- Plastic

- Paperboard

- Metal

- Glass

- Bioplastics

- By Package Type

- Bottles

- Metal Cans

- Cartons

- Jars

- Others

- By Product

- Dried Baby Food

- Liquid Milk Formula

- Powder Milk Formula

- Snacks and Finger Foods

- Others

- By Age Group

- 0-6 Months

- 6-12 Months

- 1-2 Years

- 2-3 Years

- By Distribution Channel

- Supermarkets / Hypermarkets

- Convenience Stores

- Pharmacies and Drugstores

- Online Retail

- Others

- By Country

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Malaysia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the model structure and to anchor key demand signals that show up in public data. We referenced sources such as national statistics offices and customs portals for trade flows, the UN Comtrade database for cross-country consistency, and FAO and World Bank indicators for population and income context. We also used journals that discuss infant nutrition and packaging safety standards.

Along with this, we reviewed company annual reports, investor presentations, packaging association publications, and reputable press to understand changes in packaging mix and the direction of pricing. A paid subscription for company financials and a shipment-level trade database were used selectively to sanity-check supplier exposure and major import routes. These sources are illustrative only, and we used many other public and paid references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to fill gaps that desk sources cannot answer cleanly, especially around packaging format shares, typical pack sizes, and price ranges by material. We spoke with participants across packaging conversion, brand procurement, and channel-facing stakeholders, and then used their inputs to confirm assumptions country by country across APAC, so the final totals aligned with what the market is actually buying.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 40% | |

| Smaller Players: 16% | Managers: 45% |

Market-Sizing & Forecasting

Sizing started from a top-down build where baby population, category consumption patterns, and pack format penetration were combined to reconstruct the addressable packaged volume and value in each key APAC country. Those totals were then cross-checked with selective bottom-up approximations, such as sampling average selling price by material and format and applying it to estimated unit or weight throughput visible in the supply chain.

Inputs that mattered most included birth cohort trends, infant formula and prepared baby food sales momentum, shifts toward pouches and liquid cartons, and lightweighting trends that change grams of packaging per pack. We also tracked resin, paperboard, and metal price movement because it influences packaging ASPs. Where bottom-up coverage was incomplete, we handled gaps by using verified mix ratios from interviews and applying them to adjacent countries with similar category structure, followed by a review pass to avoid overstating smaller markets.

Forecasts were developed using scenario analysis supported by short time series smoothing for packaging ASPs, then adjusted with expert views on premiumization, regulatory pushes on recyclability, and expected capacity additions for relevant packaging formats. The final forecast kept country-level assumptions visible, so changes in a single driver could be traced through to the market total.

Data Validation & Update Cycle

Each market output was checked against independent signals, including trade direction, material pricing cycles, and the implied packaging intensity per unit of baby food sold, and then outliers were investigated before sign-off. When large variances appeared, we re-contacted selected respondents to confirm whether the issue came from scope interpretation, timing of price changes, or a one-off demand spike.

A multi-step internal review was completed so calculations, conversions, and growth logic were consistent across countries and packaging formats. The report is refreshed annually, and material events are monitored in between, so a focused update can be made when pricing, regulation, or demand conditions shift meaningfully. Before delivery, a fresh analyst pass is completed to ensure the latest public releases and interview learnings are reflected.

Mordor Intelligence's Asia Pacific Baby Food Packaging Market Size Compared With Other Published Estimates

Published market values for baby food packaging in Asia Pacific often vary because studies do not always count the same packaging formats, price timing, and country coverage in the same way. Differences also show up when one estimate is closer to consumer pack value, while another blends in adjacent food packaging streams.

The main gap drivers here were whether flexible packs and closures are fully counted, how packaging weight per pack is treated as formats shift, and whether 2024 or 2025 pricing is used when currency and polymer costs moved. Some sources also apply a single regional growth rate across APAC, even though category mix and premiumization differ widely by country.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.71 B (2025) | |

| Global Consultancy A | USD 16.60 B (2024) | This figure appears to lean on a broader packaging revenue view by material type, which can inflate totals if adjacent food packaging revenue, heavier packaging assumptions, or fuller inclusion of components like caps and closures are applied across APAC. |

| Industry Data Publisher B | USD 8.61 B (2026) | A forward-year value can look higher or lower depending on how quickly price normalization is assumed, and whether pouch penetration and pack-size shifts are modeled country by country or applied as a regional average. |

The spread across sources is largely explained by scope boundaries, the priced year used in each study, and how format mix changes are translated into value. By keeping the count tied to consumer baby food packs across APAC countries and re-checking material and format price assumptions with interviews, the estimate remains more traceable to clear drivers. This is the approach used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the APAC baby food packaging market?

The market is valued at USD 8.61 billion in 2026 and is projected to reach USD 14.96 billion by 2031.

Which packaging material is growing fastest?

Bioplastics are expanding at an 17.85% CAGR through 2031, supported by large-scale PLA and PBAT investments in Thailand and Vietnam.

Why are pouches gaining popularity in baby food?

Pouches offer portability, reduced breakage and easy self-feeding, helping them grow at a 15.35% CAGR and hold 32.55% market share in 2025.

Which country will drive the highest growth?

India is forecast to register the fastest 13.75% CAGR due to urbanization, dual-income families and improved retail infrastructure.

How is e-commerce changing packaging design?

Online retail’s 18.85% CAGR forces packagers to engineer more robust, cube-efficient formats that withstand parcel shipping while maintaining product integrity.

What regulatory changes are shaping material choices?

China’s GB 4806.15-2024 adhesive rules, India’s updated labeling standards and Japan’s Positive List for resins tighten safety requirements and accelerate the shift to compliant, sustainable materials.

Page last updated on: