Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.13 Billion |

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific General Aviation Market Analysis by Mordor Intelligence

The Asia-Pacific general aviation market size was valued at USD 3.13 billion in 2025 and estimated to grow from USD 3.33 billion in 2026 to reach USD 4.52 billion by 2031, at a CAGR of 6.31% during the forecast period (2026-2031). This expansion is unfolding against a backdrop of low-altitude airspace liberalization, new propulsion technologies, and sustained wealth creation across major economies. Rotorcraft currently provides the largest revenue share, but fast-rising eVTOL programs, hybrid-electric powerplants, and asset-light ownership models are beginning to alter competitive dynamics. China’s policy push for a low-altitude economy and India’s Bharatiya Vayuyan Adhiniyam 2024 together unlock the region’s most enormous pool of previously restricted airspace. OEMs respond by relocating assembly lines and service centers closer to demand, while operators deploy digital flight-planning and predictive-maintenance tools to counter infrastructure and pilot-capacity constraints.

Key Report Takeaways

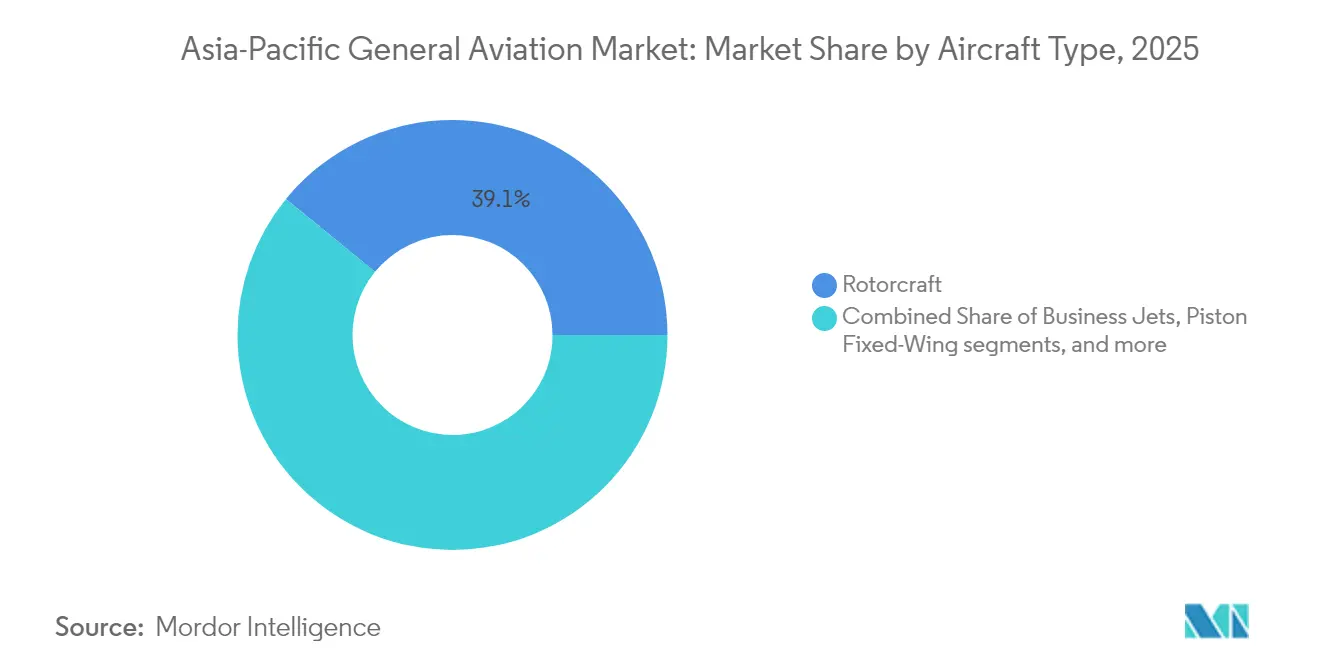

- By aircraft type, rotorcraft led with 39.10% of the Asia-Pacific general aviation market share in 2025; AAM eVTOLs are forecasted to expand at a 7.01% CAGR through 2031.

- By propulsion, conventional piston and turbine systems accounted for 80.45% of the Asia-Pacific general aviation market size in 2025, while all-electric aircraft are projected to grow at a 7.44% CAGR.

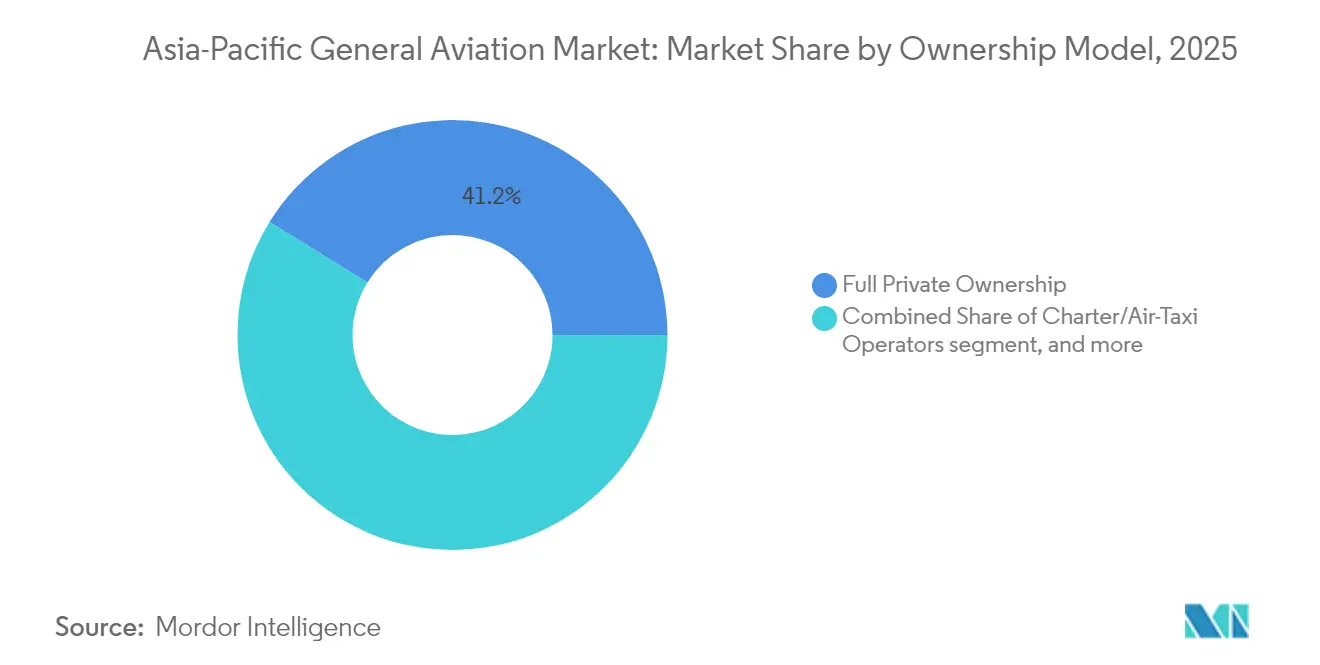

- By ownership model, full private ownership held 41.20% of the Asia-Pacific general aviation market size in 2025; charter and air-taxi fleets record the fastest growth at 6.38% CAGR.

- By end-user application, business and corporate transport commanded 43.92% of the Asia-Pacific general aviation market share in 2025; emergency medical and air-ambulance missions are advancing at a 9.31% CAGR.

- By geography, China dominated with 44.80% of regional revenue in 2025, while India is expected to post the highest 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific General Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HNWI population in the Asia-Pacific | +1.2% | China, India, Singapore, Australia | Medium term (2-4 years) |

| Liberalization of low-altitude airspace | +1.8% | China, India; spillover to Southeast Asia | Short term (≤ 2 years) |

| OEM investments in Asia-Pacific final-assembly and service centers | +0.9% | China, Singapore, Japan, India | Long term (≥ 4 years) |

| Corporate travel rebound post-COVID | +1.1% | Business hubs across the Asia-Pacific | Short term (≤ 2 years) |

| Urban Air Mobility (UAM) infrastructure pilots | +0.7% | Singapore, South Korea, Japan, Australia | Medium term (2-4 years) |

| Carbon-credit financing for hybrid/electric general aviation fleets | +0.6% | Developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HNWI Population in the Asia-Pacific

In 2024, high-net-worth individuals (HNWIs) in the region controlled USD 17.4 trillion in investable assets, equal to 31% of global HNWI wealth. Purchases of large-cabin jets and long-range turboprops are no longer viewed as discretionary spending but as productivity tools that bridge thin commercial airline networks. Secondary Chinese and Indian cities lacking nonstop airline service are seeing the sharpest uptick in point-to-point general aviation demand. At the same time, Singapore’s tax-efficient registration regime lures aircraft relocations from Hong Kong.

Low-altitude Airspace Liberalization

China’s 2024 low-altitude economy regulations opened roughly 70% of sub-1,000 m airspace by eliminating routine military approvals, cutting average business-aviation flight times by 23% in early trials.[1]Civil Aviation Administration of China, “Low-Altitude Economy Regulations 2024,” caac.gov.cn India’s Bharatiya Vayuyan Adhiniyam 2024 introduced risk-based access criteria that replaced blanket restrictions, creating a combined 2.1 million km² corridor of liberalized airspace across both markets.[2]Directorate General of Civil Aviation India, “Bharatiya Vayuyan Adhiniyam 2024,” dgca.gov.in Within six months, Hainan’s pilot zone recorded 340% growth in general-aviation movements, signaling pent-up regional demand.

OEM Final-assembly and Service Investments

Manufacturers committed USD 2.8 billion to regional plants and MRO capacity in 2024.[3]Airbus, “Annual Report 2024,” airbus.com Airbus extended its Tianjin line to ACJ variants, while Bombardier and Mitsubishi Heavy Industries opened Japan’s first Western business-jet service hub.[4]Bombardier, “Investor Presentation 2024,” bombardier.com Textron Aviation broke ground on a Hyderabad joint-venture facility that targets annual delivery of 25 Cessna Caravans from 2026, underscoring confidence in India’s supply-chain depth. In-region completions shorten ferry times and lower tariff exposure, making the total cost of ownership more predictable for operators. Local outfitters can also tailor interiors to cultural preferences, such as tatami suites for Japanese buyers, creating incremental aftermarket revenue potential.

Corporate Travel Rebound

Business-aviation flight hours in Asia-Pacific surpassed 2019 by 12% in 2024 as executives prioritized schedule control and health security. Charter load factors hit 89%, while fractional programs logged 156% growth in regional hours. Asian Sky Group projects the addition of 95 large-cabin jets between 2025 and 2028, indicating a durable tailwind for OEM order books. Regional governance codes that require in-person board meetings in Japan and Indonesia sustain baseline demand even as virtual conferencing persists. VistaJet’s deployment of eight new Global jets in 2024 signals operator confidence in a structurally higher utilization plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slot scarcity at primary airports | -0.8% | Tokyo, Singapore, Hong Kong | Long term (≥ 4 years) |

| High import tariffs and luxury taxes | -1.3% | India, Thailand, Indonesia, Malaysia | Medium term (2-4 years) |

| Shortage of certified general aviation pilots and mechanics | -1.0% | Developing Asia-Pacific markets | Long term (≥ 4 years) |

| Grid and battery-supply limitations for eVTOL uptake | -0.5% | Singapore, Seoul, Tokyo, Sydney | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slot Scarcity at Primary Airports

General aviation slot allocation at Asia-Pacific’s top hubs fell 23% between 2019 and 2024 as scheduled carriers reclaimed peak-hour capacity. Tokyo Haneda caps business-jet movements at 4% of daily slots, while Singapore Changi restricts non-scheduled departures to off-peak windows. Crews often endure ground delays exceeding 90 minutes during congested periods, eroding the time savings that justify premium charter rates. IATA forecasts a further 38% rise in passenger movements by 2030, widening the slot gap for general aviation. Governments in Indonesia and Vietnam are exploring vertiport networks to bypass runway congestion, yet full deployment remains at least five years away.

High Import Tariffs and Luxury Taxes

India levies a 28% Goods and Services Tax (GST) on imported aircraft, Thailand imposes 30% duties, and Indonesia layers a 15% tariff with a 10% luxury tax, inflating acquisition costs by USD 3-8 million on large-cabin jets. Operators in Thailand increasingly resort to dry-leasing to sidestep upfront duties, but the structure limits customization and exposes lessees to foreign-exchange swings. Fleet-age disparities appear: aircraft imported via duty-free registries average eight years old versus 11.5 years for domestically purchased jets. Asian Business Aviation Association lobbying for harmonized duty relief has met political resistance due to sensitivities around luxury goods taxation. Fragmented policies slow fleet modernization and divert economic value to offshore registries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Rotorcraft Leadership Faces eVTOL Disruption

Rotorcraft, supported by offshore energy, EMS, and law-enforcement missions, captured 39.10% of the Asia-Pacific general aviation market share in 2025. Business jets followed at 35.05%, while turboprops and piston fixed-wing aircraft held 18.88% and 6.97%, respectively. eVTOL vehicles, though starting from a small base, are forecast to post a 7.01% CAGR, challenging helicopter operators with lower direct-operating costs and minimal noise. The EH216-S received the world’s first eVTOL type certificate in October 2024, signaling regulatory momentum.

Persistent rotorcraft demand stems from archipelagic geographies in Indonesia and the Philippines, where point-to-point vertical lift is indispensable. Yet UAM trials in Singapore, Seoul, and Tokyo show early evidence of eVTOL commercial viability, prompting incumbent helicopter OEMs to revisit product roadmaps.

By Propulsion Type: Electric Systems Challenge Conventional Dominance

Conventional piston and turbine powerplants controlled 80.45% of the 2025 revenue base, reflecting decades-old maintenance networks and ubiquitous jet-fuel infrastructure. Hybrid-electric aircraft occupy 19.55%, bridging range limitations while lowering fuel burn. All-electric models are poised for a 7.44% CAGR through 2031, driven by city-pair missions under 100 km and stringent metropolitan emission targets. Rolls-Royce and Safran lead demonstrator programs, while Singapore pledges carbon-neutral domestic aviation by 2030.

Cost-of-ownership economics continue to favor conventional engines on longer sectors, yet battery-specific energy gains and rapid-charging networks will narrow the gap in the medium term. Government incentives in China and Malaysia accelerate commercialization by reducing import duties on electric aircraft.

By Ownership Model: Asset-light Models Gain Traction

Full private ownership retained 41.20% of revenue in 2025, driven by availability guarantees and the desire for customized interiors among UHNWIs in China and Japan. Charter and air-taxi fleets are the fastest-growing model at 6.38% CAGR, fueled by corporate cost control and app-based booking convenience. Fractional programs expand at 5.69% CAGR, offering share-based access with predictable budgeting. Training institutions hold a 12.55% foothold, while government and special-mission operators account for 8.95%.

Operator economics are tilting toward pay-as-you-fly services as maintenance, crew, and parking costs climb. Digital platforms that optimize fleet scheduling and empty legs further reinforce the asset-light trend.

By End-User Application: Medical Services Drive Growth

Business and corporate transport dominated 2025 revenue at 43.92%, reflecting the Asia-Pacific general aviation market’s core value proposition of time-efficient executive travel. Personal and leisure flying accounted for 28.84%, supported by rising discretionary incomes in Australia, Japan, and coastal China. Emergency-medical and air-ambulance missions represent the fastest-growing niche at 9.31% CAGR, addressing aging populations and remote‐area healthcare gaps. Special-mission roles, including maritime surveillance and border patrol, command 15.31%, while pilot training fills 11.93% of demand as airlines struggle with cockpit-crew pipelines. Governments are subsidizing EMS rotorcraft fleets, most notably in Indonesia and the Philippines, and integrating telemedicine links to improve response times to outlying islands.

Geography Analysis

China held 44.80% of the Asia-Pacific general aviation market revenue in 2025. The low-altitude economy program has reduced flight-planning lead times and encouraged domestic OEMs to ramp production. India is set for an 8.52% CAGR, propelled by airspace reforms and an expanding UHNW population. Japan follows with an 17.60% share, underpinned by offshore-energy helicopter contracts and corporate-jet charters. Australia's 12.10% proportion reflects mining-sector transport and widespread EMS needs across remote interiors.

Southeast Asia, aggregating Singapore, Malaysia, Thailand, Indonesia, and the Philippines, accounts for 19.30% in 2025. Singapore's aircraft-registry incentives and MRO ecosystem place it at the center of regional fleet basing, while Malaysia and Thailand invest in pilot-training academies. South Korea maintains 6.20% in 2025 with a strategic focus on UAM test beds, supported by chaebol-backed investment.

Regulatory fragmentation remains the principal impediment to cross-border operations, but the pilot program's success in Singapore and China is helping to establish harmonized standards for eVTOL certification and UTM protocols.

Competitive Landscape

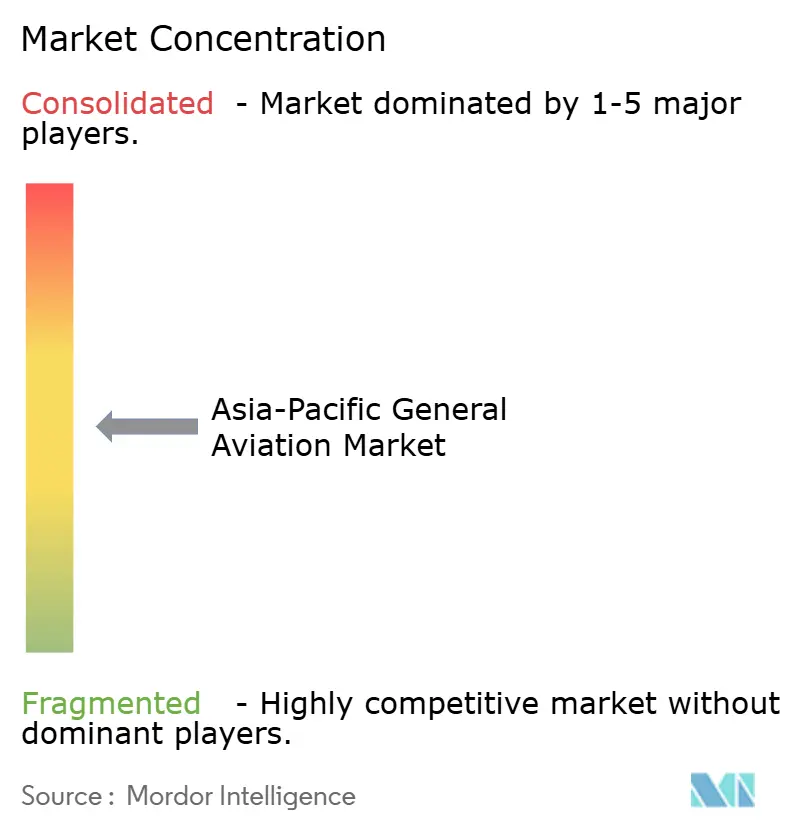

The Asia-Pacific general aviation market is moderately fragmented; the top five OEMs control most regional deliveries. Airbus, Bombardier, Textron, and Gulfstream retain brand recognition, yet regional challengers EHang, AVIC, and AutoFlight use home-market policies and cost advantages to penetrate UAM niches. Charter and fractional operators such as VistaJet and NetJets are scaling fleets to exploit asset-light demand.

OEM strategies emphasize proximity assembly and localized completions. Airbus’ Tianjin A320/ACJ line compresses delivery schedules by six months, while Honda Aircraft’s USD 50 million Singapore MRO hub trims maintenance downtime by 40%. Technology differentiators center on real-time health-monitoring systems and SAF compatibility, with early adopters securing a competitive advantage in cost and sustainability metrics.

Intellectual-property barriers are shrinking as joint ventures pair Western avionics suppliers with East-Asian assemblers, underscoring the need for robust cybersecurity and export-control compliance.

Asia-Pacific General Aviation Industry Leaders

Airbus SE

Textron Inc.

Robinson Helicopter Company

Embraer S.A.

Gulfstream Aerospace Corporation (General Dynamics Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shanghai-based TCab Tech signed a USD 1 billion agreement with UAE-based Autocraft to supply 350 five-seat E20 eVTOLs for deployment across the Middle East and North Africa.

- September 2025: Soracle Corporation announced a collaboration with Osaka Prefecture and Osaka City to support the commercialization of eVTOLs in Osaka.

- October 2023: Textron Aviation entered into a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, with options for 16 additional aircraft.

Asia-Pacific General Aviation Market Report Scope

By Aircraft Type

| Business Jets | Large Jet |

| Mid-Size Jet | |

| Light/Very-Light Jet | |

| Turboprop Fixed-Wing | |

| Piston Fixed-Wing | |

| Rotorcraft | |

| Advanced Air Mobility eVTOLs |

By Propulsion Type

| Conventional Piston/Turbine |

| Hybrid-Electric |

| All-Electric |

By Ownership Model

| Full Private Ownership |

| Fractional Ownership |

| Charter/Air-Taxi Operators |

| Training and Academic Institutions |

| Government and Special-Mission Operators |

By End-User Application

| Business/Corporate Transport |

| Personal and Leisure Flying |

| Special Mission (ISR, Surveillance, Law Enforcement) |

| Emergency Medical/Air-Ambulance |

| Pilot Training |

By Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Singapore |

| Philippines |

| Malaysia |

| Indonesia |

| Thailand |

| Rest of Asia-Pacific |

| By Aircraft Type | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light/Very-Light Jet | ||

| Turboprop Fixed-Wing | ||

| Piston Fixed-Wing | ||

| Rotorcraft | ||

| Advanced Air Mobility eVTOLs | ||

| By Propulsion Type | Conventional Piston/Turbine | |

| Hybrid-Electric | ||

| All-Electric | ||

| By Ownership Model | Full Private Ownership | |

| Fractional Ownership | ||

| Charter/Air-Taxi Operators | ||

| Training and Academic Institutions | ||

| Government and Special-Mission Operators | ||

| By End-User Application | Business/Corporate Transport | |

| Personal and Leisure Flying | ||

| Special Mission (ISR, Surveillance, Law Enforcement) | ||

| Emergency Medical/Air-Ambulance | ||

| Pilot Training | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Philippines | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific |

Market Definition

- Aircraft Type - General Aviation includes aircraft used for corporate aviation, business aviation and other aerial works.

- Sub-Aircraft Type - Business Jets, Piston Fixed-Wing Aircraft, and helicopters and turboprop aircraft are taken into consideration.

- Body Type - Light Jets, Mid-Size Jets, and Large Jets according to their ability to carry passengers and flying distance ranges have been included under this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms