Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.89 Billion |

| Market Size (2026) | USD 12.56 Billion |

| Market Size (2031) | USD 16.49 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fighter Aircraft Market Analysis by Mordor Intelligence

The Asia-Pacific fighter aircraft market size was valued at USD 11.89 billion in 2025 and estimated to grow from USD 12.56 billion in 2026 to reach USD 16.49 billion by 2031, at a CAGR of 5.60% during the forecast period (2026-2031). Growth is propelled by rising regional tensions, continuous fleet modernization, and accelerating 6th-generation development programs reshaping the Asia-Pacific fighter aircraft market landscape. China’s USD 314 billion defense allocation and Japan’s 21% budget jump to USD 55.3 billion illustrate the scale of near-term demand. At the same time, collaborative R&D frameworks such as GCAP reinforce long-term momentum in the Asia-Pacific fighter aircraft market. Supply-chain vulnerabilities around engines and semiconductors temper the outlook, yet robust offset packages and export-linked financing continue to widen buyer access across the Asia-Pacific fighter aircraft market. Overall, competitive intensity is increasing as Western primes confront capable regional manufacturers, many of whom leverage domestic production incentives and relaxed export rules to win share.

Key Report Takeaways

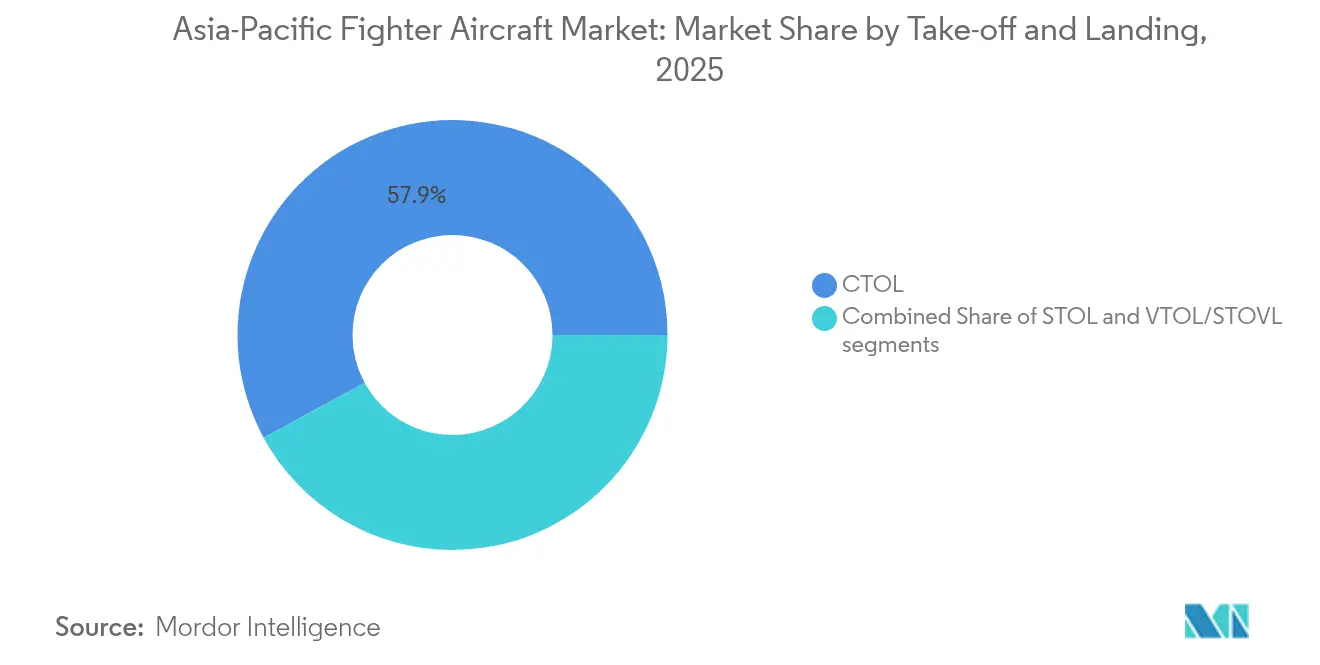

- By take-off and landing, conventional CTOL platforms commanded 57.92% of the Asia-Pacific fighter aircraft market share in 2025, while VTOL/STOVL aircraft are projected to clock the fastest 6.62% CAGR through 2031.

- By fighter generation, 4.5th-generation jets led with a 41.25% revenue share in 2025; 6th-generation programs are forecasted to post an 8.15% CAGR between 2026 and 2031.

- By engine configuration, single-engine designs accounted for 51.88% of the Asia-Pacific fighter aircraft market size in 2025. In contrast, twin-engine platforms are on track for a 6.95% CAGR over the same span.

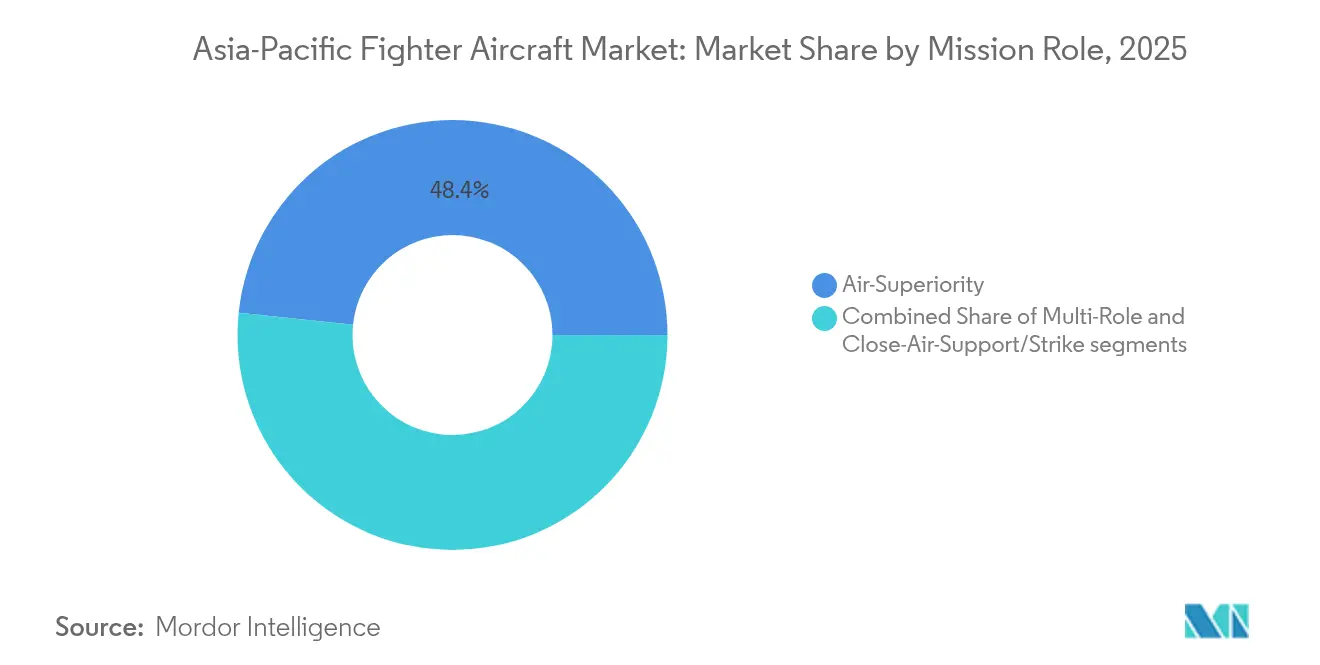

- By mission role, air-superiority variants held 48.35% share of the Asia-Pacific fighter aircraft market size in 2025; multi-role fighters are advancing at a 6.69% CAGR to 2031.

- By end user, air forces retained 52.26% revenue share in 2025, yet naval aviation is set to expand at an 7.84% CAGR, outpacing all other segments.

- By geography, China dominated the Asia-Pacific fighter aircraft market with a 36.62% share in 2025, leveraging expansive domestic production that skirts export-control risks. India is projected to grow at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Fighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating defense budgets amid rising regional tensions | +1.80% | China, Japan, South Korea, Taiwan, India | Short term (≤ 2 years) |

| Fleet modernization replacing 3rd-generation fighters | +1.20% | India, Indonesia, Thailand, Malaysia, Philippines | Medium term (2-4 years) |

| 6th-generation R&D collaborations accelerate procurement cycles | +0.90% | Japan, Australia, South Korea | Long term (≥ 4 years) |

| Export-linked financing and tech-transfer packages widen buyer base | +0.70% | Southeast Asia, India | Medium term (2-4 years) |

| Indigenous fighter programs unlock domestic spending | +0.60% | India, South Korea, China | Medium term (2-4 years) |

| Carrier-air-wing expansion (China, India, Japan) drives naval fighter demand | +0.40% | China, India, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Defense Budgets Amid Rising Regional Tensions

Regional defense outlays climbed to USD 433 billion in 2024, a 7.80% jump that directly underwrites higher fighter procurement lines. China allocated USD 314 billion and Japan boosted its budget by 21% to USD 55.3 billion, enabling multi-year contract awards that lock in output for the Asia-Pacific fighter aircraft market. Taiwan’s USD 16.50 billion spending emphasizes air-defense platforms, while South Korea’s USD 2.9 billion F-15K upgrade shows legacy fleet refresh absorbing expanded funding.[1]Royal Aeronautical Society, “AEROSPACE, May 2025,” aerosociety.com Policymakers see airpower as an asymmetric lever in potential multi-domain conflicts, sustaining high capital expenditure on combat aircraft. Local-content mandates, such as India’s 30% offset threshold, further channel new money into domestic industrial ecosystems, reinforcing near-term demand.

Fleet Modernization Replacing 3rd-Generation Fighters

Retirement of Jaguars, MiG-29s, and other legacy assets compels steady intake of newer jets, anchoring the Asia-Pacific fighter aircraft market well beyond pure fleet expansion. India alone needs 35-40 fresh airframes each year to hold squadron numbers as older types phase out. Thailand’s USD 3.65 billion Gripen E/F award over rival bids, plus Indonesia’s USD 8.1 billion Rafale order, highlight modernization choices that prioritize technology transfer alongside performance. Upgrade paths sustain production lines and fund R&D for next-step platforms, while HAL’s goal of 30 Tejas Mk1A jets annually by 2027 illustrates how domestic suppliers ride the same replacement wave.

6th-Generation R&D Collaborations Accelerate Procurement Cycles

Joint development—epitomized by the GCAP initiative and Boeing’s USD 20 billion NGAD win—compresses decision timelines as nations commit funds during design phases. Cost-sharing makes 6th-generation capability accessible to mid-tier budgets, while broader industrial participation builds political backing for the Asia-Pacific fighter aircraft market. Japan’s 2024 export-policy reform allows fighter tech transfer to 15 partners, unlocking broader involvement and diluting unit cost. Among prospective entrants, India must weigh standalone development against consortium membership, accelerating strategic budget allocations that pull forward procurement.

Export-Linked Financing and Tech-Transfer Packages Widen Buyer Base

Comprehensive offset deals and long-tenor financing are growing determinants of contract wins in the Asia-Pacific fighter aircraft market. Turkey offered Indonesia a USD 10 billion KAAN fighter jet proposal that combines multiple financing options with domestic manufacturing capabilities. This approach is similar to the Philippines' USD 5.58 billion F-16 package, which includes extended payment terms and integrated performance-based logistics. Flexible structures lower entry barriers for smaller defense budgets, broadening the buyer field while cementing aftermarket revenue streams for OEMs.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep acquisition and life-cycle costs | -1.10% | Southeast Asia, smaller economies | Short term (≤ 2 years) |

| ITAR and export-control constraints on critical subsystems | -0.80% | Global, especially US transfers | Medium term (2-4 years) |

| Engine and semiconductor supply-chain bottlenecks | -0.60% | Global, acute in India and South Korea | Short term (≤ 2 years) |

| Production backlogs and delivery slippages | -0.40% | Global, all suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steep Acquisition and Life-Cycle Costs

Unit prices between USD 40–116 million and life-cycle expenses that often double program outlays squeeze smaller defense budgets, slowing orders within the Asia-Pacific fighter aircraft market. With defense spending ranging from 0.78% of GDP in Indonesia to 4.09% in Myanmar, affordability gaps push nations toward light combat jets, used platforms, or leasing. The KAI FA-50’s USD 700 million Philippine follow-on order underlines how lower-cost fighters with logistics packages appeal to constrained buyers. OEMs respond through performance-based logistics and export-credit financing, yet capital intensity remains a structural brake.

ITAR and Export-Control Constraints on Critical Subsystems

Separate licensing for US-origin engines, sensors, or weapons can stall timelines and limit capability configurations, complicating procurement inside the Asia-Pacific fighter aircraft market.[2]John P. Barker et al., “AUKUS at Last — Commerce and State Announce Rules to Reduce U.S. Export Barriers for Australia and the UK,” Arnold & Porter, arnoldporter.com India’s Tejas program has endured GE F404 delays that pushed first deliveries to mid-2025, spotlighting dependency risks. Evolving frameworks such as AUKUS carve out exemptions, but overarching export-control regimes continue to shape platform selection toward suppliers with more streamlined transfer protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Take-off and Landing: Naval Operations Drive VTOL Growth

Conventional CTOL aircraft dominated the Asia-Pacific fighter aircraft market with 57.92% share in 2025, mirroring entrenched land-based force structures. VTOL platforms, although niche, are forecast to record a 6.62% CAGR as carrier programs and distributed basing concepts raise demand. Japan’s decision to embark F-35Bs on Izumo-class vessels demonstrates how VTOL capability extends reach without new supercarriers. Meanwhile, China’s Type 003 Fujian carrier and envisioned Type 004 nuclear ship will amplify VTOL procurement once indigenous designs mature.

Technological advances in thrust-vectoring reduce the payload-range penalties historically associated with VTOL, enhancing attractiveness for expeditionary roles. Combined with evolving ICAO guidelines that enable military VTOL operations in controlled civil airspace, the segment’s role in regional humanitarian response augments its growth trajectory within the Asia-Pacific fighter aircraft market.

By Fighter Generation: 6th-Generation Programs Reshape Procurement

4.5th-generation jets held 41.25% Asia-Pacific fighter aircraft market share in 2025, thanks to a balance of proven reliability and upgraded avionics. 6th-generation efforts such as GCAP and NGAD are projected to post an 8.15% CAGR, even though prototypes remain in development. The lingering utility of 4th-generation fleets sustains upgrade business, while 5th-generation purchases fill interim capability gaps.

Manufacturers capitalize on bridge upgrades—active electronically scanned array radars, infrared search-track, and network gateways—to keep incumbents relevant ahead of 6th-generation arrival. China’s unveiling of advanced prototypes exerts competitive pressure, prompting earlier commitments that bolster the Asia-Pacific fighter aircraft market size for next-generation platforms.

By Engine Configuration: Twin-Engine Demand Reflects Range Requirements

Single-engine fighters captured a 51.88% share of the Asia-Pacific fighter aircraft market in 2025, favored for cost efficiency and simpler maintenance. Yet twin-engine variants are on a 6.95% CAGR trajectory as maritime nations prioritize range and redundancy for overwater missions. Despite higher acquisition costs, long-range strike and patrol needs tilt procurement toward twin-engine designs.

Delivery setbacks on GE F404 and F414 lines have exposed the vulnerability of single-engine programs like Tejas, intensifying interest in diversified powerplants and twin-engine alternatives. As engine reliability gains shrink the cost delta, twin-engine offerings gain traction across the Asia-Pacific fighter aircraft market.

By Mission Role: Multi-Role Versatility Commands Premium

Air-superiority variants preserved a 48.35% share in 2025, yet budget realities are steering procurements toward multi-role fighters, anticipated to grow 6.69% annually. Operators seek single-platform air-to-air, strike, and reconnaissance solutions to limit training pipelines and inventories. Thailand’s Gripen E selection underscores how all-domain flexibility outweighs narrowly focused performance in evaluation matrices.

Advances in sensor fusion and modular weapons stations allow rapid task reconfiguration, lifting utilization rates, and underpinning premium pricing. Therefore, the Asia-Pacific fighter aircraft market is shifting toward platforms that deliver mission agility without sacrificing survivability.

By End User: Naval Aviation Growth Outpaces Traditional Air Forces

Air Forces retained 52.26% of 2025 revenues, yet Naval Aviation is projected to outstrip all other customers with an 7.84% CAGR. China’s rapid carrier fleet expansion and Japan’s F-35B embarkation create sustained orders for carrier-capable fighters. Specialized corrosion protection and arrestor hooks elevate unit prices, boosting value growth even as absolute volumes remain lower than land-based fleets.

India’s prospective third carrier further reinforces long-term naval demand, while Indonesia’s interest in acquiring a legacy Italian carrier signals latent appetite among emerging navies. These factors make Naval Aviation the highest-growth customer subset in the Asia-Pacific fighter aircraft market.

Geography Analysis

China dominated the Asia-Pacific fighter aircraft market with a 36.62% share in 2025, leveraging expansive domestic production that skirts export-control risks. Indigenous output of 5th-generation J-20s, forecasted to exceed 500 units by 2025, anchors value creation, while naval J-35 variants feed a growing carrier force. Beijing’s integrated supply chain and export ambitions reinforce its leadership position, though geopolitical headwinds may limit sales to select partners.

India represents the fastest-growing geography with a 6.78% CAGR through 2031. The country’s urgent need for 35-40 fighters annually drives parallel tracks: foreign buys such as Rafale and indigenous programs encompassing Tejas Mk1A, Mk2, and AMCA. HAL’s collaboration with private industry to hit 30 Tejas deliveries a year illustrates scale-up underway, yet engine bottlenecks remain a risk to meeting timelines.

Japan, South Korea, Indonesia, and the wider Southeast Asian bloc together compose a diversified demand pool. Tokyo’s relaxed export rules enable fighter technology transfers to 15 nations, adding incremental revenue streams and deepening its stake in the Asia-Pacific fighter aircraft market. Seoul’s KF-21, buoyed by a 2025 UAE Letter of Intent, signals emergence of a new regional supplier with 120 domestic orders set by 2032. Indonesia’s multi-vendor strategy—Rafale, potential Su-35 revival, and KAAN participation—reflects a pragmatic pursuit of capability, financing, and industrial gain. Budget-constrained Southeast Asian states lean toward light combat aircraft, an area amplified by KAI’s FA-50 successes and performance-based logistics model.

Competitive Landscape

Competition is intensifying as regional OEMs erode Western primes' historical dominance in the Asia-Pacific fighter aircraft market. Lockheed Martin, Boeing, and Airbus still command advanced technology portfolios, yet they must contend with delivery slippages, rising unit costs, and ITAR-linked constraints. Turkey's KAAN, South Korea's KF-21, and China's J-series fighters offer credible alternatives, often bundled with generous offsets and flexible financing that resonate with emerging economies.

Strategic moves showcase adaptive postures: Boeing is ramping F-15EX lines to two jets monthly to clear backlogs and free capacity for NGAD prototypes. KAI signed the first export performance-based logistics deal with the Philippines, locking in long-tail revenue and highlighting service differentiation. Dassault's tight production schedules for Rafale—24 jets annually through 2033—underline supply pressures that could open windows for agile competitors.[4]Michael Peck, “France’s Rafale fighter jet is so popular its manufacturer can’t keep up,” Business Insider, businessinsider.com

Technology objectives center on sensor fusion, secure networking, and manned-unmanned teaming rather than raw speed or altitude. Vendors adept at integrating open-architecture avionics and offering sovereign software rights gain bargaining power, especially where export-control anxieties persist. Consequently, the Asia-Pacific fighter aircraft market is moving toward a balanced contest in which value, autonomy, and regulatory ease weigh as heavily as classic performance metrics.

Asia-Pacific Fighter Aircraft Industry Leaders

Mitsubishi Heavy Industries, Ltd.

Lockheed Martin Corporation

Hindustan Aeronautics Limited (HAL)

The Boeing Company

Aviation Industry Corporation of China

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Thailand selected the Saab Gripen E for USD 3.65 billion, prioritizing technology transfer over competing F-16 and Rafale bids.

- June 2025: The Philippines placed a USD 700 million order for 12 FA-50PH Block 20 fighters, doubling its fleet to 24 and extending KAI’s performance-based logistics footprint.

- April 2025: UAE and South Korea signed an LoI on KF-21 cooperation, marking the first potential export for the Boramae.

Asia-Pacific Fighter Aircraft Market Report Scope

A fighter aircraft can be termed as a high-speed military aircraft, which can carry out air-to-air combat missions. High speed, ease in maneuvering, and relatively smaller size are considered the fighter aircraft's hallmarks. These aircraft can also carry heavy payloads and perform electronic warfare, ground attacks, and air-to-air combat. The report also covers the increasing adoption of fighter aircraft in the Asia-Pacific region. It analyzes the conventional take-off and landing, short take-off and landing, and vertical take-off and landing segments.

By Take-off and Landing

| Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) |

| Vertical Take-off and Landing (VTOL/STOVL) |

By Fighter Generation

| 4th Generation |

| 4.5th Generation |

| 5th Generation |

| 6th Generation/NGAD |

By Engine Configuration

| Single-Engine |

| Twin-Engine |

By Mission Role

| Air-Superiority |

| Multi-Role |

| Close-Air-Support/Strike |

By End User

| Air Force |

| Naval Aviation |

| Marine/Army Aviation |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Rest of Asia-Pacific |

| By Take-off and Landing | Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) | |

| Vertical Take-off and Landing (VTOL/STOVL) | |

| By Fighter Generation | 4th Generation |

| 4.5th Generation | |

| 5th Generation | |

| 6th Generation/NGAD | |

| By Engine Configuration | Single-Engine |

| Twin-Engine | |

| By Mission Role | Air-Superiority |

| Multi-Role | |

| Close-Air-Support/Strike | |

| By End User | Air Force |

| Naval Aviation | |

| Marine/Army Aviation | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific fighter aircraft market in 2026?

The Asia-Pacific fighter aircraft market size reached USD 12.56 billion in 2026 and is on a 5.60% CAGR growth path to 2031.

Which segment is expanding fastest?

Naval aviation demand is projected to rise at an 7.84% CAGR as China, India, and Japan grow carrier forces.

What share do 4.5th-generation fighters hold today?

5th-generation aircraft commanded 41.25% Asia-Pacific fighter aircraft market share in 2025, making them the current revenue leader.

Why are twin-engine fighters gaining ground?

Twin-engine designs are forecasted to grow 6.95% annually because regional operators need longer-range, over-water safety margins.

How is Japan’s export-policy change affecting suppliers?

Relaxed rules now let Japan transfer fighter technology to 15 nations, widening consortium participation and intensifying competition in the region.

Page last updated on: