Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

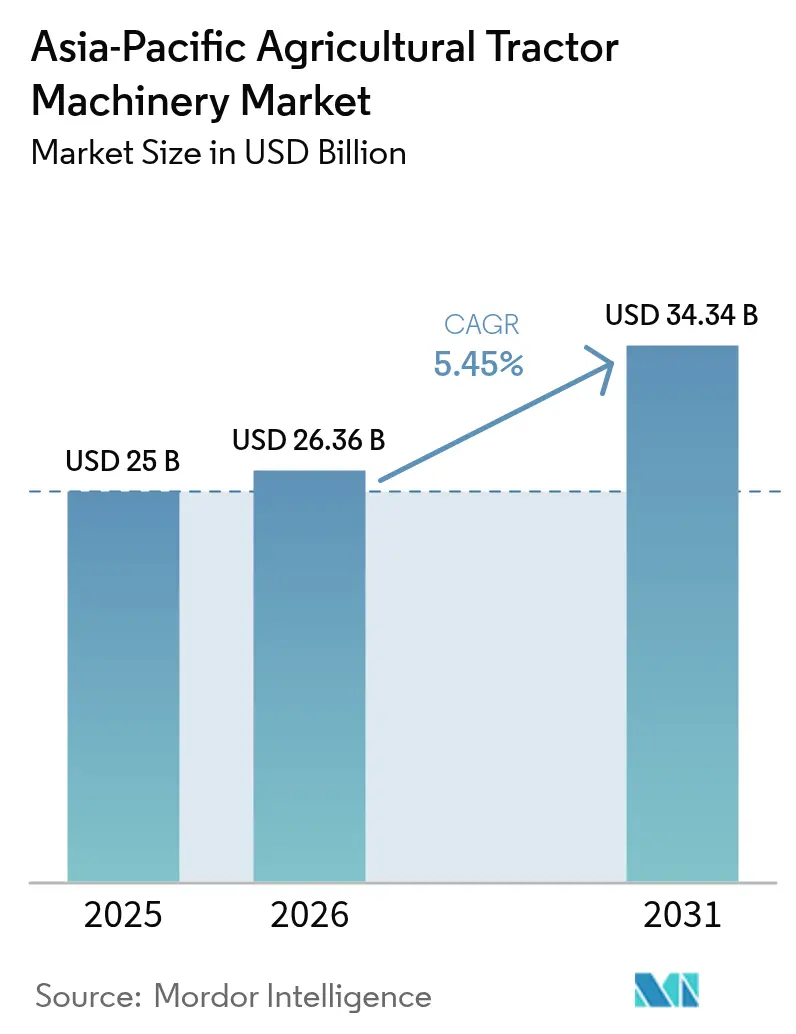

| Base Year Market Size (2025) | USD 25 Billion |

| Market Size (2026) | USD 26.36 Billion |

| Market Size (2031) | USD 34.34 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The Asia-Pacific agricultural tractor machinery market size is expected to grow from USD 25 billion in 2025 to USD 26.36 billion in 2026 and is forecast to reach USD 34.34 billion by 2031 at 5.45% CAGR over 2026-2031. Heightened mechanization incentives, shrinking rural workforces, and improving access to subsidized credit jointly underpin this expansion. China currently anchors regional revenue, yet India’s faster eight-plus percent growth signals a demand pivot toward small-horsepower models aligned with fragmented holdings. Telematics-enabled machinery-as-a-service models are reshaping ownership economics, particularly in India, where custom hiring centers expanded in 2024 under the Sub-Mission on Agricultural Mechanization, allowing farmers to access high-capacity equipment without upfront capital outlays[1]Source: Ministry of Agriculture and Farmers Welfare, India. "Sub-Mission on Agricultural Mechanization." Accessed December 2, 2025. . Precision farming, especially variable-rate sprayers and section control, is diffusing from early adopters to mainstream grains and horticulture, lifting attachment sales and aftermarket service revenues. OEM (Original Equipment Manufacturer) strategies now favor local assembly hubs that shave landed costs by nearly one-fifth, while connected-tractor platforms lower downtime and unlock usage-based insurance opportunities. Moderate competitive concentration gives space for domestic specialists to target the 60-90 horsepower sweet spot preferred by contract-farming clusters.

Key Report Takeaways

- By product category, plowing and cultivating machinery led with 39.95% market size in 2025, while sprayers are forecast to expand at a 9.12% CAGR to 2031.

- By geography, China contributed 29.95% of regional sales in 2025, while India is projected to register an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Asia-Pacific Agricultural Tractor Machinery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mechanization subsidies and credit programs | +1.2% | India, China, Thailand, Vietnam, Indonesia, Philippines | Medium term (2–4 years) |

| Acute rural labor shortages driving tractor demand | +1.4% | India, China, Thailand, Vietnam, Japan | Short term (≤ 2 years) |

| Rising average farm size and contract-farming models | +0.8% | China, Australia, Thailand, Vietnam, Indonesia | Long term (≥ 4 years) |

| Surge in precision-farming adoption | +1.0% | Australia, China, Japan, South Korea, India, Thailand | Medium term (2–4 years) |

| Telematics-enabled machinery-as-a-service business models | +0.4% | India, Thailand, and Indonesia | Medium term (2-4 years) |

| Climate-resilient equipment suited for erratic monsoon patterns | +0.2% | China, Japan, and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mechanization Subsidies and Credit Programs

Direct subsidy outlays surpassed USD 4.2 billion in 2024 across Asia-Pacific, trimming acquisition costs by roughly one-quarter. India’s Aadhaar-linked benefit transfers guarantee timely payments, while China now reimburses up to 60% of sub-100-horsepower tractor prices in designated counties[2]Source: Ministry of Agriculture and Farmers Welfare, India, “Sub-Mission on Agricultural Mechanization,” agricoop.gov.in. Thailand and Vietnam complement grants with zero-interest or capped-rate loans, nudging growers toward connected equipment that feeds usage data to extension services. These initiatives collectively accelerate fleet replacement, steer demand toward mid-range horsepower, and stabilize OEM order pipelines.

Acute Rural Labor Shortages Driving Tractor Demand

Asia-Pacific lost 8.3 million agricultural workers between 2020 and 2024 as migrants shifted to urban factories. Rising daily wages now INR 600–700 (USD 7.2–8.4) in Punjab compress margins for labor-intensive crops, pushing growers toward mechanized tillage and transplanting[3]Source: Ministry of Agriculture and Farmers Welfare, India. "Sub-Mission on Agricultural Mechanization." Accessed December 2, 2025. . Japan’s aging farmer base and China’s Hukou reforms further drain seasonal labor pools, boosting cooperative tractor purchases and spurring intuitive user interfaces that shorten operator training time.

Rising Average Farm Size and Contract-Farming Models

Land-transfer markets allow absentee owners to lease plots, expanding China’s average farm to 0.65 hectares in 2024[4]Source: Food and Agriculture Organization, “Land Use Statistics and Indicators,” FAO.org. Australia’s 3,200-hectare estates favor articulated tractors above 300 horsepower, while Thai and Vietnamese contract growers leverage pooled machinery to maintain uniform agronomic quality demanded by exporters[5]Source: World Bank, “Agriculture and Rural Development Data,” worldbank.org. Mid-horsepower (60–90 hp) tractors thus balance maneuverability with implement compatibility, enticing Korean firms to establish assembly hubs in India and Thailand.

Surge in Precision-Farming Adoption

Section-control sprayers and GPS auto-steer penetrated 18% of new tractor sales in Australia and 9% in China during 2024, driven by documented 8–12% fertilizer savings. Deere equips over one-third of its regional shipments with factory-installed precision bundles, while China’s Beidou network delivers 10-centimeter accuracy at half the legacy GNSS cost. Subsidies for IoT sensors in Japan and input-price inflation in India sharpen the economic appeal of variable-rate spreads even on four-hectare holdings.

Restraints Impact Analysis of Asia-Pacific Agricultural Tractor Machinery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront acquisition and financing costs | -0.9% | India, Indonesia, Vietnam, Philippines with moderate impact in Thailand | Short term (≤ 2 years) |

| Fragmented land holdings curbing high-horsepower sales | -0.6% | India, China, Bangladesh, Vietnam, Indonesia with limited impact in Australia and Thailand | Long term (≥ 4 years) |

| Expansion of custom-hiring centers reducing ownership need | -0.4% | India, China, Thailand with emerging presence in Vietnam and Indonesia | Medium term (2-4 years) |

| Non-harmonized safety regulations delaying certifications | -0.3% | ASEAN member states (Thailand, Vietnam, Indonesia, Philippines, Malaysia) with spillover to India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Acquisition and Financing Costs

Entry-level 35-horsepower units list at INR 550,000–650,000 (USD 6,600–7,800) in India, more than double a marginal farmer’s annual net income[6]Source: National Bank for Agriculture and Rural Development, “Annual Report 2024,” nabard.org. Indonesian loan rates average 11.5%, and Vietnam enforces 30% down-payments that sap working capital. Collateral gaps in the Philippines drive applicants toward second-hand markets with higher maintenance risks. These financial frictions postpone purchases, especially for higher-spec models.

Fragmented Land Holdings Curbing High-Horsepower Sales

Holdings under two hectares dominate India and parts of Southeast Asia, making 50-plus-horsepower tractors uneconomic due to fuel and implement costs. Despite China’s consolidation trend, 62% of parcels remain below 0.4 hectares, limiting market potential for articulated and wide-span equipment. The resulting split channels OEM efforts toward compact platforms and custom-hiring solutions rather than outright high-horsepower sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Asia-Pacific Agricultural Tractor Machinery Market Segment Analysis

By Product Type

Plowing and cultivating machinery accounted for 39.95% of the segment share in 2025, underscoring its critical role in seedbed preparation across Asia-Pacific's diverse cropping systems. This includes China's mechanized wheat zones and India's fragmented rice paddies, where rotovators are widely used for wet-land puddling operations. The dominance of this category is driven by the universal need for tillage across all crop types. Moldboard plows remain significant in Australia's broadacre wheat regions, where deep inversion buries weed seeds and incorporates lime amendments. Meanwhile, disc harrows are preferred in Southeast Asia's double-cropping systems, which require a quick turnaround between harvest and planting. The segment's growth is slowing as conservation tillage practices gain momentum. Rotovators and cultivators are being upgraded with features such as adjustable tine depths and hydraulic side-shift capabilities, which enable precise seedbed leveling. These advancements, which command a 15-20% price premium, also deliver measurable fuel savings by reducing the need for additional harrowing passes.

Sprayers are projected to grow at a 9.12% CAGR from 2026 to 2031, outpacing all other product categories. This growth is driven by advancements in precision application technologies and drone-mounted systems, which are transforming crop protection practices. For instance, DJI's Agras T50 drone sprayer, launched in 2024, can cover 16 hectares per hour at one-tenth the labor cost of manual knapsack spraying. This significant productivity improvement is accelerating adoption in India's cotton belt and China's fruit orchards. Planting machinery, including seed drills and precision planters, is gaining traction in contract-farming clusters. These machines enable uniform plant spacing, resulting in 8-12% yield improvements. Variable-rate planters, which adjust seed populations based on soil fertility maps generated from satellite imagery, are becoming increasingly popular. Harrows are experiencing renewed interest in Australia's no-till wheat zones. Chain harrows are used to manage stubble residue without disturbing soil structure, helping to preserve moisture during the critical germination phase. Spreaders for granular fertilizers are incorporating GPS-guided section control, which prevents overlap in headlands and reduces input costs by 6-9% in large-scale operations.

Geography Analysis

APAC Agricultural Tractor Machinery Market

China retained 29.95% of the Asia-Pacific agricultural tractor machinery market share in 2025 but now leans on replacement demand, with around 68% of sales addressing fleet renewal rather than first-time buyers. Subsidies increasingly favor 100-plus-horsepower units that fit large-scale farming policy goals while domestic brands offer three-year warranties to fortify loyalty.

India Agricultural Tractor Machinery Market

India is on course for an 8.25% CAGR, fueled by around INR 180 billion (USD 2.2 billion) direct benefit transfers in 2024 and a thriving network of 12,800 custom-hiring centers that operate 87,000 tractors. Sub-40-horsepower tractors dominate, but rising contract farming for vegetables is nudging mid-range demand. Punjab and Haryana alone accounted for 19% of national sales, supported by waterlogged paddy conditions that favor four-wheel-drive variants.

Japan, Australia and ASEAN Agricultural Tractor Machinery Market

Japan’s replacement-driven market prizes ergonomic compact models suited to a 1.2-hectare average farm and a 67-year-old median farmer age. Australia, conversely, emphasizes 300-plus-horsepower articulated tractors for 3,200-hectare wheat estates, where auto-steer and variable-rate tools now permeate one-third of the fleet. Emerging Southeast Asian economies such as Thailand, Vietnam, and Indonesia are advancing at 6.6-7.2% CAGR as subsidy ceilings cover up to 60% of certified equipment costs.

Regulatory Landscape

Government subsidy eligibility and public procurement rules remain the most direct regulatory levers shaping tractor and implement demand across Asia-Pacific. In India, the Sub-Mission on Agricultural Mechanization (SMAM) links financial assistance to performance testing and certification at designated government institutes (including Farm Machinery Training and Testing Institutes). This approach pushes OEMs and attachment makers to localize test-compliant variants and documentation, enabling faster inclusion in state-level subsidy lists.

At the regional level, the Asian and Pacific Network for Testing of Agricultural Machinery (ANTAM) supports harmonization of testing codes, safety, and performance standards across participating countries. This addresses one of the market restraints around non-harmonized safety regulations in parts of ASEAN. In China, the Ministry of Agriculture and Rural Affairs (MARA) continues to formalize appraisal and guidance for agricultural machinery, reinforcing a compliance-driven pathway for new equipment types and upgrades entering subsidized channels.

Competitive Landscape

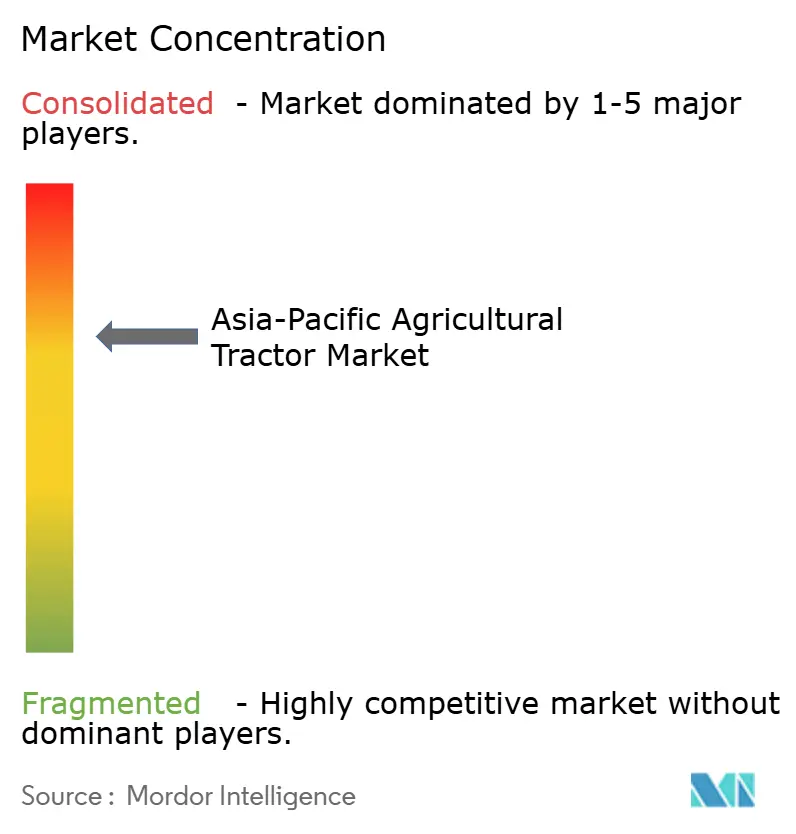

The Asia-Pacific agricultural tractor machinery market demonstrates moderate concentration, scoring 5.0 on a 10-point scale. Competitors leverage localized assembly, dealer financing, and attachment ecosystems tailored to specific crop requirements. Kubota Corporation is driven by its dominance in Japan's compact tractor segment and its expanding presence in ASEAN markets. The company's CKD (completely knocked down) assembly operations in Thailand and Vietnam reduce landed costs by 18-22% and shorten delivery lead times to 4-6 weeks compared to fully imported units.

White-space opportunities are emerging in the 60-90 horsepower segment, particularly for contract-farming clusters in Thailand and Vietnam. Lead firms in these regions are seeking standardized equipment packages that ensure uniform tillage depth and planting density across aggregated smallholder plots. This procurement model favors suppliers offering bundled implement attachments and operator training programs. Telematics integration is becoming a key competitive differentiator. Manufacturers are embedding GPS modules and cellular connectivity to provide predictive maintenance alerts, geofence theft protection, and utilization-based insurance products. These features reduce the total cost of ownership by 12-15% over a 5-year ownership cycle. Chinese manufacturers are disrupting the sub-80 horsepower segment with aggressive strategies, including 3-year warranty programs and dealer floor-plan financing. This approach has enabled distributors to stock inventory without upfront capital, contributing to a 34% increase in Lovol's dealer count in 2024.

AGCO Corporation's 2024 patent filing for a modular tractor platform highlights a shift toward mass customization. The platform supports interchangeable powertrains ranging from 75 to 150 horsepower, reducing manufacturing complexity while offering buyers flexibility as farm sizes evolve. Regulatory compliance remains a significant challenge in ASEAN markets, where non-harmonized safety standards across 10 member states require manufacturers to maintain parallel certification tracks. Established OEMs with in-country testing facilities are better positioned to navigate these complexities compared to new entrants relying on third-party labs.

Asia-Pacific Agricultural Tractor Machinery Industry Leaders

-

Kubota Corporation

-

Mahindra and Mahindra Ltd.

-

Deere and Company

-

CNH Industrial N.V.

-

Yanmar Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Asia-Pacific Agricultural Tractor Machinery Market Companies Covered in this Report

- Kubota Corporation

- Mahindra and Mahindra Ltd.

- Deere and Company

- Yanmar Co., Ltd.

- Iseki & Co., Ltd.

- Escorts Kubota Ltd. (Kubota Corporation)

- CNH Industrial N.V.

- Lovol Heavy Industry Co., Ltd.

- Daedong Corporation

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Shandong Shifeng Group Co., Ltd.

- AGCO Corporation

- SDF Group

- CLAAS KGaA mbH

- TYM Corporation

Read Analysis of Asia-Pacific Agricultural Tractor Machinery Companies

Market Opportunities and Future Outlook

Large manufacturing and financing moves in India are creating opportunity for suppliers of tractor-compatible implements, precision-ready attachment ecosystems, and localized components. In February 2026, Mahindra announced its largest integrated auto and tractor manufacturing facility in Maharashtra with stated capacity of 100,000 tractors annually, while CNH India outlined an INR 1,800 crore investment program including a greenfield tractor plant and capacity expansion. These projects expand the addressable base for plowing and cultivating implements (the leading product category by share in 2025) and support faster adoption of sprayer platforms that increasingly integrate section control, telematics, and rate-control hardware.

Export-oriented localization and embedded finance are also widening the focus beyond core tractor sales, particularly in price-sensitive smallholder markets constrained by high upfront acquisition costs. In June 2026, Kubota disclosed plans for a fifth factory in northern India to support exports, and in February 2026 Kubota approved a capital infusion into Escorts Kubota Finance Limited to expand financial services for agricultural machinery. Combined with India’s custom hiring center expansion under SMAM, these actions support growth pathways for machinery-as-a-service fleets, bundled implement packages for 60-90 hp tractors used in contract-farming clusters, and OEM-backed credit and service models aimed at improving aftermarket utilization and uptime.

Recent Industry Developments in Asia-Pacific Agricultural Tractor Machinery Market

- July 2026: CNH Industrial marked the rollout of the 800,000th tractor from its Greater Noida facility in India. The milestone highlights the scale and maturity of India as a manufacturing hub for domestic supply and regional sourcing strategies, and it supports dealer capacity for parts and tractor-linked machinery.

- June 2026: Kubota announced plans to build its fifth production facility in northern India to manufacture tractors and construction machinery, with an export-oriented rationale. The company positioned the expansion to lower landed costs and shorten lead times, supporting broader attachment penetration and service networks around the installed base.

- August 2024: Mahindra and Mahindra ramped up rotavator production at its dedicated unit in Nabha, Punjab, expanding tillage implement availability across 15-70 HP compatibility ranges. Higher local output supports bundled tractor-plus-implement offerings and improves delivery reliability for the dominant plowing and cultivating machinery segment.

Asia-Pacific Agricultural Tractor Machinery Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers agricultural tractor machinery used on farms across Asia Pacific, measured in value terms. It includes tractors and key tractor-driven implements used for field preparation, planting, spraying, and forage operations, as they are purchased and applied for crop production.

Scope exclusions: Used equipment re-sales and purely manual farm tools are not counted in this market size.

Segments Covered in This Report

-

By Product Type

-

Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Equipment

-

Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

- Sprayers

-

Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

- Other Types

-

Plowing and Cultivating Machinery

-

By Geography

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Vietnam

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand and supply structure for tractor machinery across the region, then assumptions were stress-tested using inputs gathered from field-facing participants. We relied on public sources such as agriculture ministries and national statistics offices in major countries, FAO datasets, World Bank indicators, and UN Comtrade trade statistics for machinery categories. These sources helped track import intensity and cycle changes over time.

We also reviewed mechanization program publications from associations and extension agencies, plus company annual reports, investor decks, and reputable press, to map pricing direction, product launches, and channel shifts. Where needed, paid subscriptions that compile company financials and news, along with patent databases and shipment-level trade datasets, were used to cross-check supplier presence and technology adoption signals. These desk sources are illustrative, and additional public references were used during data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work involved interviews and surveys with tractor OEM-facing stakeholders, dealers, rental and service providers, and large farm and contractor users across key Asia Pacific markets. The respondent input was used to confirm replacement cycles, the typical attachment mix, and how incentives and financing affect purchase timing. Results were then used to tighten assumptions taken from desk research.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 42% | Functional/Unit leaders: 42% | |

| Smaller Players: 21% | Managers: 46% |

Market-Sizing & Forecasting

Sizing started with a top-down build where tractor population and annual sales signals were translated into an equipment demand pool, then allocated across countries using mechanization intensity and cropping pattern differences. To keep totals realistic, the outputs were corroborated with selective bottom-up checks such as sampled dealer throughput, attachment penetration for commonly used implements, and price bands for volume-moving horsepower classes.

A few inputs materially shaped the model: tractor sales momentum by major country, the share of farm area under mechanized operations, subsidy and credit program coverage, replacement and refurbishment cycles by usage intensity (particularly for contractor fleets), and average selling price movement by horsepower and implement type. For markets where data was thin, proxy ratios were used from similar agronomic conditions and income levels, and the estimates were adjusted after dealer and channel checks.

For forecasting, scenario analysis was used, with growth paths tied to variables like rural labor availability, farm income trends, lending conditions, and government mechanization budgets, then filtered through primary feedback on expected policy continuity. Short-term volatility was handled with smoothing on sales and pricing series so that an unusual year did not over-pull the multi-year curve.

Data Validation & Update Cycle

Model results were validated through triangulation across multiple angles, including trade flows for relevant machinery codes, reported tractor sales trends, and dealer inventory commentary, then compared with what users described as normal seasonal buying behavior. Where variances were large, assumptions were re-checked, and follow-up calls were used to determine whether the driver was pricing, policy timing, or a one-off stock correction.

Before sign-off, numbers go through multi-step reviews by analysts who check for year-over-year breaks, country mix shifts, and currency conversion consistency. Reports are refreshed annually, and interim updates are done when a material change affects pricing, incentives, or demand visibility. Immediately before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Agricultural Tractor Machinery Market Sizing Compared With Other Published Estimates

Published market sizes for agricultural tractor machinery in Asia Pacific can appear far apart, even when they target a similar theme. The differences usually come from scope choices, which year is treated as the base, and how pricing and replacement cycles are handled across different farm structures.

The main gap comes from mixing tractor-only values with wider machinery baskets. In this approach, Mordor Intelligence counts tractor machinery tied to field-use demand signals, including implement categories such as planting and spraying, and keeps pricing anchored to common horsepower and attachment mixes rather than extending the total with adjacent equipment types.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.00 B (2025) | |

| Industry Research House A | USD 17.71 B (2023) | Uses an earlier base year and a type-led tractor framing that can under-represent implement-led value capture and later-cycle price effects when compared with a country demand-pool build. |

| Sector Publisher B | USD 17.92 B (2025) | Covers only wheeled tractor machinery and excludes tracked units, and the narrower product definition can also shift the implied ASP and volume mix versus a broader tractor machinery view. |

The spread across sources is mainly explained by scope choices (tractor types and implement coverage), the base year selected, and how prices are carried forward across mixed country conditions. By tying estimates back to measurable demand indicators and then checking them with channel reality, the final number remains transparent and repeatable for planning discussions.

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific agricultural tractor machinery market by 2031?

The market is expected to reach USD 34.34 billion by 2031, growing at a 5.45% CAGR.

Which country is forecast to record the fastest growth through 2031?

India is projected to expand at an 8.25% CAGR, underpinned by direct subsidy transfers and custom-hiring centers.

Which product category currently leads regional revenue?

Plowing and cultivating machinery led with 39.95% revenue share in 2025.

Why are precision-farming tools gaining traction?

Proven fertilizer and fuel savings of 8–12% and falling hardware costs are driving adoption of GPS auto-steer and variable-rate systems.

What financial barrier restricts tractor purchases among smallholders?

Entry-level tractors cost more than double the annual net income of many marginal farmers, and loan rates in several economies exceed 11%.

Page last updated on: