Solid-State Transformer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

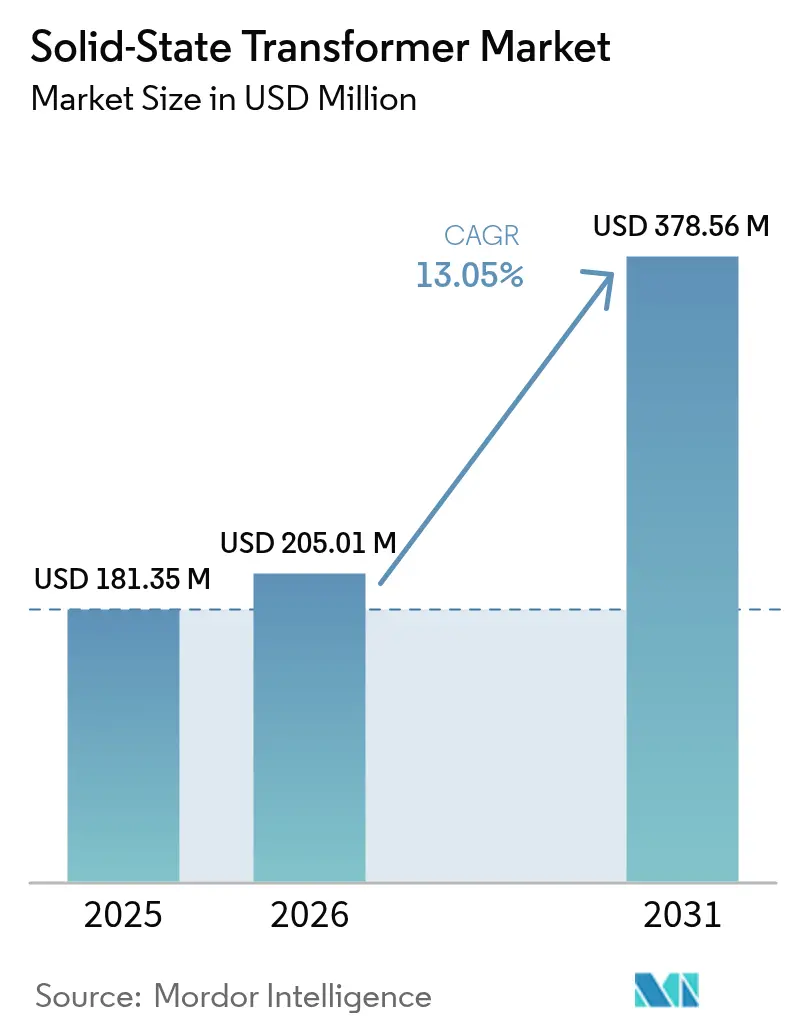

| Market Size (2026) | USD 205.01 Million |

| Market Size (2031) | USD 378.56 Million |

| Growth Rate (2026 - 2031) | 13.05% CAGR |

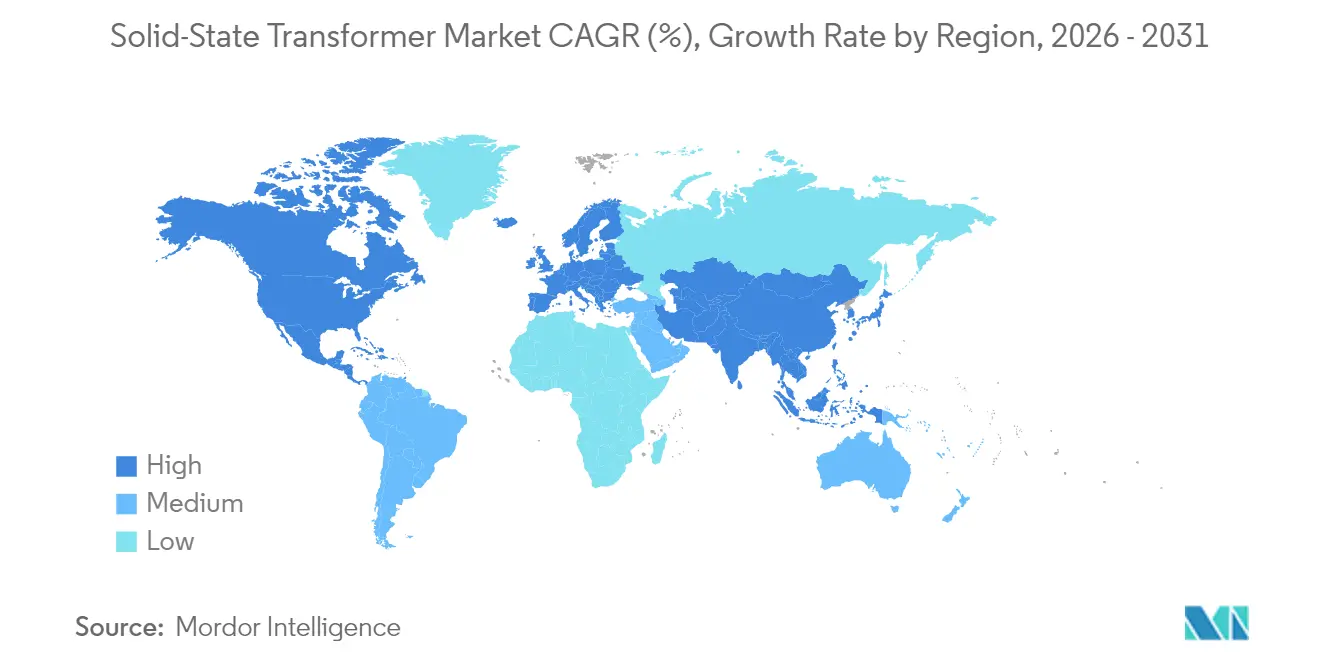

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid-State Transformer Market Analysis by Mordor Intelligence

The Solid-State Transformer Market size was valued at USD 181.35 million in 2025 and estimated to grow from USD 205.01 million in 2026 to reach USD 378.56 million by 2031, at a CAGR of 13.05% during the forecast period (2026-2031).

Robust momentum stems from utilities, rail operators, data center owners, and EV charging providers that increasingly value bidirectional power flow, real-time voltage regulation, and compact footprints that conventional oil-filled units cannot match. SiC and GaN semiconductors now block higher voltages at lower switching losses, enabling lighter magnetic cores and extending deployment to space-constrained urban substations and rolling stock. The Asia-Pacific region leads the adoption as China, India, and Japan channel stimulus toward grid resilience, rail electrification, and domestic semiconductor supply, elements that compress payback periods even when upfront costs remain elevated. Policy directives in Europe to phase out SF₆ switchgear, combined with North American defense standards mandating rugged microgrids, add multi-year visibility across the solid-state transformer market.

Key Report Takeaways

- By product type, Distribution systems captured 40.85% of the solid-state transformer market share in 2025, while traction units are forecast to expand at a 14.95% CAGR to 2031.

- By voltage level, Medium-voltage equipment (2–36 kV) accounted for 55.65% of the solid-state transformer market size in 2025; high-voltage systems above 36 kV are expected to grow at a 14.72% CAGR over the same horizon.

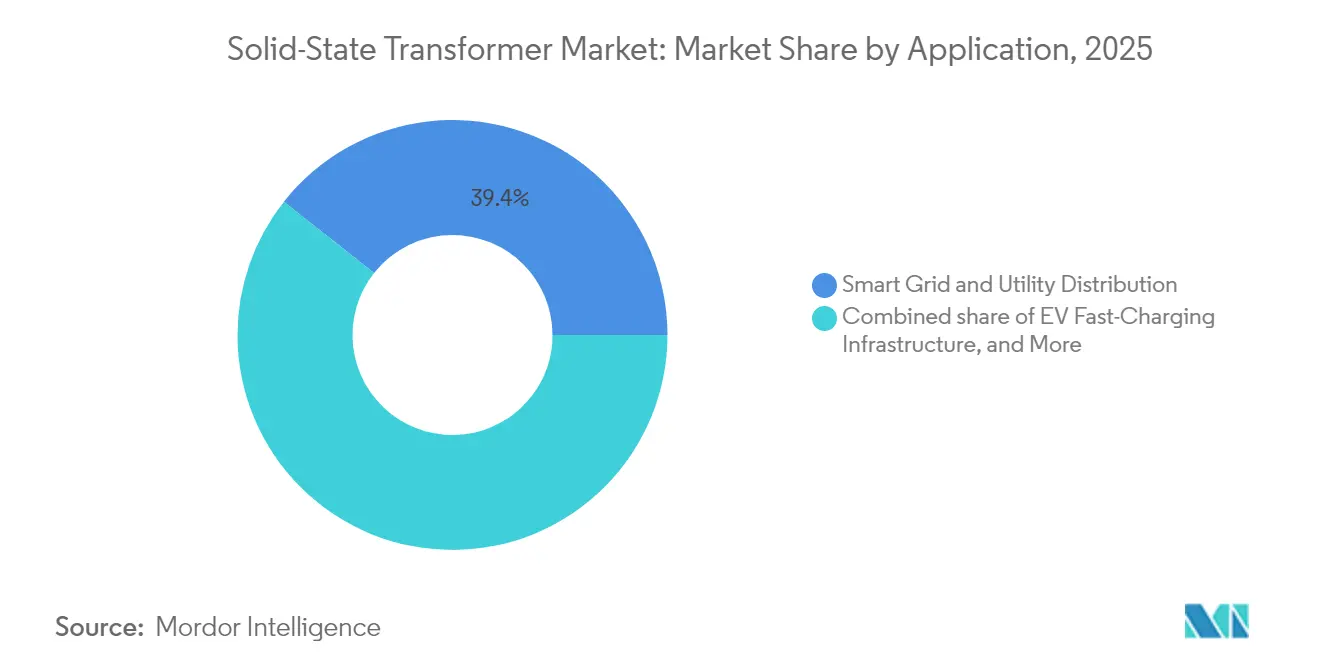

- By application, Smart-grid and utility distribution applications led with 39.35% revenue share in 2025; EV fast-charging infrastructure is projected to post the quickest 15.98% CAGR through 2031.

- By geography, the Asia-Pacific region commanded 40.10% of the 2025 revenue and is set to progress at a 13.76% CAGR, outpacing every other regional segment of the solid-state transformer market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Solid-State Transformer Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smart-grid rollout | 2.8% | Global, with early gains in North America, Europe, and China | Medium term (2-4 years) |

| Renewable integration requirements | 2.5% | Global, particularly strong in Europe, California, and APAC renewable hubs | Long term (≥ 4 years) |

| Rail electrification & traction demand | 2.2% | APAC core, spill-over to Europe and select emerging markets | Medium term (2-4 years) |

| AI-data-centre power-density push | 1.8% | North America & EU, expanding to APAC hyperscale regions | Short term (≤ 2 years) |

| Urban EV fast-charging hub build-out | 2.0% | Global, with early concentration in China, Europe, and North American metros | Short term (≤ 2 years) |

| Defense micro-grid modernization | 1.2% | North America & EU, with selective adoption in allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Smart-Grid Rollout

Distribution companies are accelerating capital plans that incorporate digital protection, advanced metering, and flexible transformers into the same cabinet. The U.S. Department of Energy earmarked USD 3.5 billion in 2024 for distribution upgrades that prioritize solid-state platforms able to furnish bidirectional power flow, harmonic filtering, and islanding within a single enclosure.[1]U.S. Department of Energy, “Grid Modernization Initiative,” energy.gov A parallel EU network-code mandate compels utilities to integrate distributed resources more actively, providing OEMs with predictable order pipelines and encouraging volume pricing. ABB’s Smart Substation Control and Protection SSC600 SW demonstrates how virtualized SST controls reduce installation complexity and lower lifecycle expenses by up to 15% in dense urban feeders. As thermal imaging and cybersecurity analytics migrate into firmware, operators gain real-time situational awareness that reinforces regulatory confidence in next-generation grid hardware.

Renewable Integration Requirements

Wind- and solar-heavy feeders face voltage flicker and reactive-power swings that mechanical tap changers cannot contain at millisecond speeds. Solid-state units compensate instantaneously, thereby bolstering grid codes that demand firm power quality in scenarios with 50% renewable penetration. Hitachi Energy’s SVC Light STATCOM, installed with SP Energy Networks, freed 280 MW of incremental clean-energy headroom on a legacy UK corridor without stringing new lines.[2]Hitachi Energy, “SVC Light STATCOM Enables 280 MW Renewable Integration,” hitachi.com High-frequency operation shrinks core steel, letting developers mount SSTs closer to inverter blocks on constrained sites. As distributed solar portfolios aggregate under virtual power plant contracts, unified control of voltage regulation and fault isolation speeds market clearing, underpinning revenue streams that reward plant owners for ancillary service availability across the solid-state transformer market.

Rail Electrification and Traction Demand

Rail agencies specify lighter transformers to hit axle-load limits and free cabin space for passengers or cargo. India’s pledge to electrify its entire broad-gauge network by 2027 underpins multi-billion-dollar traction orders that embed solid-state modules for onboard step-down duties. Modular cartridges enable depot technicians to swap power-electronics boards in under an hour, slashing downtime in remote dispatch yards. ABB demonstrated scalability beyond passenger rail by completing a battery-electric mining haul truck that leverages traction SST architecture for regenerative braking and steep-grade torque.[3]ABB Ltd., “Smart Substation Control and Protection SSC600 SW,” abb.com Similar designs align with Chinese high-speed rail expansions and EU Green Deal corridors, solidifying rail as the fastest-growing segment of the solid-state transformer market.

Urban EV Fast-Charging Hub Build-out

Megawatt chargers for electric heavy trucks concentrate loads that can swing from zero to multi-MW in seconds. SST cabinets, located downstream of the medium-voltage service entrance, mitigate inrush currents and backfeed power for vehicle-to-grid programs, thereby reducing feeder upgrade costs for municipal utilities. The EU Alternative Fuels Infrastructure Regulation calls for 3.5 million public chargers by 2030, while the United States deploys USD 5 billion through NEVI to establish coast-to-coast corridors capable of 350-kW to 1-MW sessions.[4]European Commission, “Alternative Fuels Infrastructure Regulation,” europa.eu Compact footprints enable operators to co-locate battery storage for peak shaving, thereby enhancing station economics and accelerating momentum in this high-growth segment of the solid-state transformer market.

Restraints Impact Analysis of Solid-State Transformer Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex versus legacy transformers | -1.8% | Global, particularly acute in cost-sensitive emerging markets | Medium term (2-4 years) |

| Lack of standards & interoperability | -1.5% | Global, with fragmented approaches across regions | Long term (≥ 4 years) |

| SiC / GaN wafer supply bottlenecks | -1.2% | Global, with supply concentrated in Asia and capacity constraints | Short term (≤ 2 years) |

| Thermal-management issues in arid zones | -0.8% | Middle East & Africa, Southwest US, and select APAC regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex Versus Legacy Transformers

A solid-state platform can cost two to three times more than an oil-filled equivalent at the same kVA rating, deterring managers who report to tariff-focused regulators. Yet, operating data show 20-year maintenance savings, lower no-load losses, and deferred reactive-compensation capital expenditures that, together, compress payback to seven years in most distribution feeders. Wolfspeed and ON Semiconductor are spending USD 6.5 billion and USD 2 billion, respectively, on 8-inch SiC wafer fabs that, once at scale in 2027, could reduce semiconductor input costs by up to 30%.[5]Wolfspeed Inc., “Mohawk Valley SiC Fab Expansion,” wolfspeed.com Utilities bridge interim affordability gaps through leasing models or power-purchase agreements that bundle hardware, software, and uptime guarantees—a financing innovation that is spreading across the solid-state transformer market.

Lack of Standards and Interoperability

IEEE 1547-2018 establishes rules for interconnecting inverter-based resources but falls short of prescribing Specific performance tests or communication protocols.[6]IEEE Power & Energy Society, “IEEE 1547-2018 Overview,” ieee.org IEC 61850 extensions remain in draft, leaving buyers to navigate proprietary firmware and spare-parts inventories that lock them into single vendors. The U.S. military’s MIL-STD-3071 offers a template for rugged microgrid topologies, yet commercial utilities still must lobby national standards bodies for harmonised type-testing. Until that process concludes, multiple certifications are still required; however, commercial utilities must still lobby national standards bodies for harmonization paths that inflate engineering costs and slow bulk tenders across the solid-state transformer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Solid-State Transformer Market Segment Analysis

By Product Type:

Traction Units Propel UptakeTraction designs logged just 17.85% revenue in 2025, yet are forecast to outpace every peer at 14.95% CAGR through 2031. The solid-state transformer market size linked to rail and on-board applications is expected to more than double as national electrification programs in Asia-Pacific and Europe accelerate. Weight savings of up to 40% compared to oil-filled predecessors directly translate into higher passenger capacity or freight volume, thereby elevating line profitability without requiring new rolling stock purchases.

Distribution models up to 10 MVA accounted for 40.85% of 2025 sales, as utilities integrated SST pilots into mainstream asset-replacement cycles. Integrated voltage regulation, fault isolation, and power-quality conditioning eliminate the need for discrete capacitor banks and static switches, simplifying inventory management. Power-class SSTs above 10 MVA serve bulk-intertie points but remain a niche owing to bespoke engineering and rigorous high-voltage test protocols. Nevertheless, ABB’s SACE Infinitus solid-state breaker demonstrates convergence between protection and conversion, setting the stage for integrated switchgear-plus-transformer racks that could enlarge this slice of the solid-state transformer market.

By Voltage Level:

High-Voltage Momentum BuildsMedium-voltage units (2–36 kV) accounted for 55.65% of 2025 turnover, as their ratings align with distribution feeders and industrial campuses. They remain the workhorses of the solid-state transformer market, but systems exceeding 36 kV will grow faster, at a 14.72% CAGR, as utilities connect gigawatt-scale wind, solar, and storage clusters. High-voltage prototypes now employ series-stacked SiC MOSFETs capable of blocking 15 kV per die, enabling cabinet footprints comparable to those of legacy gas-insulated transformers.

Hitachi Energy’s USD 1.5 billion capacity ramp earmarks dedicated high-voltage lines for SF₆-free switchgear integrated with electronic cores, aligning with Europe’s 2030–2032 greenhouse-gas phase-out timetable. Dynamic voltage-support functions embedded in SST controllers reduce the need for external STATCOMs, thereby improving the total installation economics for grid operators. As field references accumulate, insurance underwriters become more comfortable with electronic insulation schemes, unlocking wider procurement and deeper penetration across the voltage band of the solid-state transformer market.

By Application:

EV Charging Spurs InnovationSmart-grid and utility feeders retained 39.35% of 2025 revenue, cementing their role as the largest commercial anchor in the solid-state transformer market. Municipalities fund resilience upgrades that combine battery storage and advanced feeder management, all orchestrated by SST hubs that can island communities during storms or cyber incidents.

EV fast-charging is poised to scale at a 15.98% CAGR, the fastest among applications, as megawatt-class charge plazas for trucks and buses emerge along freight corridors. SST cabinets permit direct medium-voltage connection, avoiding bulky step-down transformers and copper wiring runs that erode project ROI. Data centers and ICT demand rank smaller in volume yet generate high margins due to stringent uptime and harmonic distortion limits. Defense, marine, and microgrid niches continue to push the reliability and thermal-management envelopes, which then filter into mainstream utility offerings, reinforcing iterative innovation across the solid-state transformer market.

Geography Analysis

APAC Solid-State Transformer Market

The Asia-Pacific region led with 40.10% revenue in 2025 and is projected to grow at an annual rate of 13.76%, reflecting state-backed spending on semiconductor fabs, rail corridors, and resilient distribution grids. China fuses AI algorithms with dispatch centers, creating demand for self-optimizing transformers that feed predictive-maintenance dashboards. India allocates multiyear capital to electrify its entire broad-gauge rail network, a mandate that alone could absorb thousands of traction modules. Japan emphasizes island-capable microgrids after typhoon outages, while South Korea’s smart-city blueprints integrate SST-based EV hubs and rooftop solar arrays. These complementary policy thrusts ensure that the solid-state transformer market in Asia-Pacific sustains top-line leadership and technology learning-curve benefits that spill over to emerging suppliers.

Europe Solid-State Transformer Market

Europe boasts the most mature regulatory environment, with the Green Deal and Fit-for-55 packages catalyzing investment in switchgear that is free of SF₆, a potent greenhouse gas. Utilities such as TenneT and SSEN Transmission have already signed multiyear framework agreements for SF₆-free, SST-equipped substations. Germany’s Energiewende and the UK’s net-zero legislation channel funds into voltage-regulation nodes that align with high-voltage direct current (HVDC) corridors, thereby boosting the regional solid-state transformer market, even in areas with modest GDP growth. Collaborative R&D among universities, OEMs, and national labs maintains Europe’s edge in control algorithms and advanced packaging techniques.

North America Solid-State Transformer Market

North America commands a diversified demand profile. The U.S. Department of Defense mandates MIL-STD-3071 microgrid architectures at every domestic base by 2035, anchoring a defense-specific pipeline for hardened SST skids. Hyperscale cloud operators are establishing AI campuses in Virginia, Iowa, and Texas that rely on medium-voltage busways supplied by SST switchboards to reduce copper usage and maintain 99.9% uptime. Canada leverages its hydro resources to dispatch clean power over long distances, utilizing SST nodes for dynamic voltage support, while Mexico’s USMCA-aligned industrial parks adopt SST-based feeders that facilitate interconnection with rooftop solar and behind-the-meter storage. Collectively, the region delivers steady, high-margin segments that reinforce global competitiveness within the solid-state transformer market.

Competitive Landscape

The solid-state transformer market remains moderately fragmented. ABB, Siemens, and Hitachi Energy leverage decades of transformer expertise and service fleets to secure early-mover advantages, winning turnkey substation contracts that bundle installation, training, and multi-year digital service subscriptions. ABB expanded its reach by acquiring a Siemens Gamesa power-electronics unit, consolidating converter boards, firmware, and field crews under one roof. Hitachi Energy’s global USD 1.5 billion capacity expansion targets both conventional and SST lines, signaling confidence that semiconductor price declines will unlock mass-market volumes before 2030.

Semiconductor specialists such as STMicroelectronics and Wolfspeed market SiC modules that drop directly into OEM drawer systems, enabling mid-tier transformer builders to field competitive offerings without owning fabs. Defense-grade integrators carve out niches by qualifying hardware for shock, vibration, and electromagnetic-pulse criteria that commercial utilities rarely require, garnering premium margins but lower volumes. Emerging manufacturers in South America and Southeast Asia are exploring cost-optimized, lower-rating designs for rural electrification; however, constrained access to high-voltage SiC dies and advanced thermal substrates limits their reach. Over the 2025-2030 period, supplier power will hinge on blended portfolios that marry semiconductor roadmaps with digital-service ecosystems, an alignment that top-five players already deploy across the solid-state transformer market.

Solid-State Transformer Industry Leaders

Hitachi Energy Ltd

ABB Ltd.

Siemens AG

Mitsubishi Electric Corp.

GE Vernova

- *Disclaimer: Major Players sorted in no particular order

Solid-State Transformer Market Companies Covered in this Report

- ABB Ltd.

- Siemens AG

- Hitachi Energy

- Mitsubishi Electric Corp.

- GE Vernova

- Eaton Corp.

- Schneider Electric SE

- Alstom SA

- Kirchner Solar Group

- Beta Transformer Technologies

- Varentec Inc.

- Hillcrest Energy Technologies

- Amantys Power Electronics

- Astrol Electronic AG

- Delta Electronics Inc.

- Fuji Electric Co. Ltd.

- Toshiba Energy Systems

- GridBridge LLC

- Jiangsu Zhongtian Technology

- JSHP Transformers

Recent Industry Developments in Solid-State Transformer Market

- July 2025: ABB introduced the SACE Emax 3 air circuit breaker, featuring predictive-maintenance analytics and zero-trust cybersecurity layers for AI data center feeders.

- April 2025: ABB E-mobility launched the MCS1200 Megawatt Charging System, delivering up to 1,200 kW for heavy vehicles, easing depot electrification bottlenecks.

- April 2025: Hitachi Energy committed an additional USD 1.5 billion to expand transformer and SST production in Finland, Germany, and North America.

- March 2025: The U.S. Air Force has tapped a GE Vernova-led consortium to pilot geothermal-powered microgrids that integrate SST nodes at domestic bases.

- January 2025: The U.S. Army commissioned a hydrogen-powered nanogrid at White Sands Missile Range featuring SST-based power conditioning to support silent-watch missions.

Global Solid-State Transformer Market Report Scope

The scope of the solid-state transformer market report includes:

Segmentation Overview

| Power SST (Above 10 MVA) |

| Distribution SST (Up to 10 MVA) |

| Traction SST (Rail/On-board) |

| Medium-Voltage (2 to 36 kV) |

| High-Voltage (Above 36 kV) |

| Smart Grid and Utility Distribution |

| Renewable and Micro-grid Integration |

| EV Fast-Charging Infrastructure |

| Traction and Rail Systems |

| Data Centres and ICT Power |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Power SST (Above 10 MVA) | |

| Distribution SST (Up to 10 MVA) | ||

| Traction SST (Rail/On-board) | ||

| By Voltage Level | Medium-Voltage (2 to 36 kV) | |

| High-Voltage (Above 36 kV) | ||

| By Application | Smart Grid and Utility Distribution | |

| Renewable and Micro-grid Integration | ||

| EV Fast-Charging Infrastructure | ||

| Traction and Rail Systems | ||

| Data Centres and ICT Power | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global revenue be by 2031?

The solid-state transformer market is forecast to reach USD 378.56 million in 2031, almost doubling 2025 levels.

Which product category is expanding fastest?

Traction units for rail and onboard vehicles are projected to grow at 14.95% CAGR through 2031, the highest among product segments.

Why are utilities willing to pay more for solid-state designs?

Lifecycle models show maintenance savings, lower no-load losses, and integrated power-quality functions that shrink payback to about seven years despite higher purchase prices.

Which region represents the largest opportunity today?

Asia-Pacific holds 40.10% of global revenue and is adding capacity at a 13.76% CAGR backed by infrastructure spending in China, India, and Japan.

How do SSTs improve EV fast-charging economics?

They connect directly to medium-voltage feeders, cut copper runs, manage bidirectional power, and decrease feeder upgrades, allowing quicker site commissioning.

What limits wider deployment in cost-sensitive markets?

Capital costs remain 2–3 times higher than oil-filled units, and standardization gaps add integration risk, though falling SiC prices and leasing models are narrowing the gap.

Page last updated on: