ASEAN Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

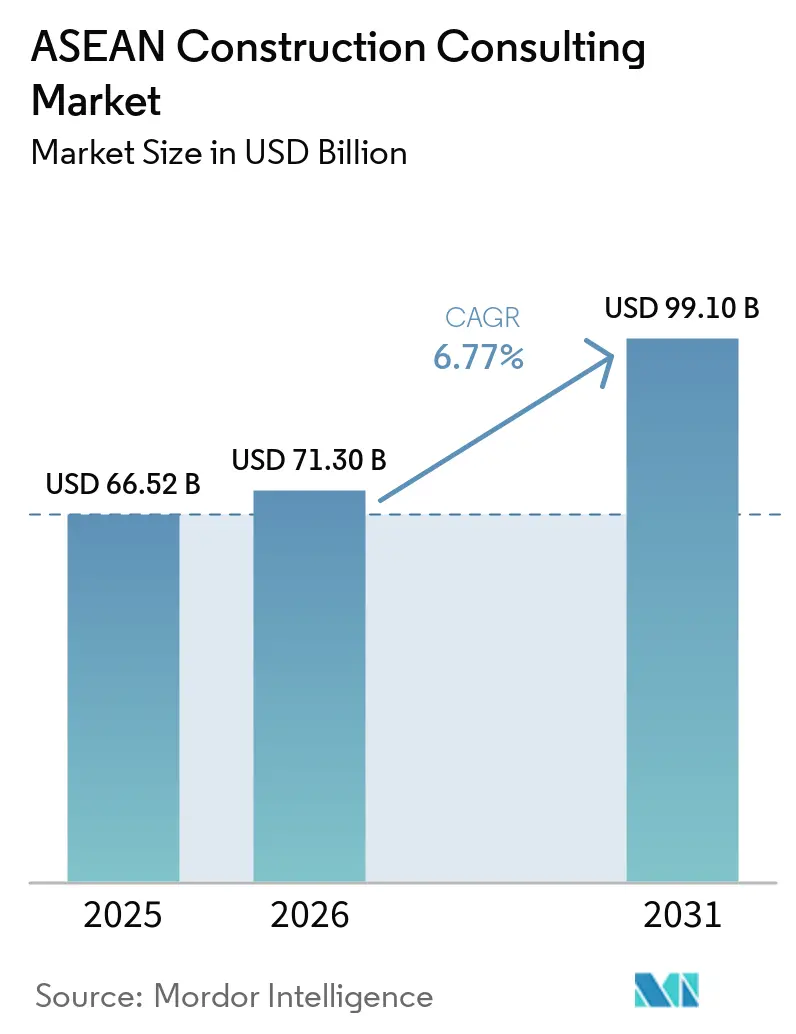

| Base Year Market Size (2025) | USD 66.52 Billion |

| Market Size (2026) | USD 71.30 Billion |

| Market Size (2031) | USD 99.10 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Construction Consulting Market Analysis by Mordor Intelligence

The ASEAN construction consulting market size is expected to grow from USD 66.52 billion in 2025 to USD 71.3 billion in 2026 and is forecast to reach USD 99.10 billion by 2031 at 6.77% CAGR over 2026-2031. Digitization mandates, smart-city programs, and semiconductor mega-projects are pulling advisory spending toward integrated lifecycle services rather than lowest-bid supervision contracts. Firms with in-house Building Information Modeling (BIM) teams are winning complex packages tied to Singapore’s CORENET X roll-out and Malaysia’s National BIM e-Submission, while Indonesia’s Nusantara capital relocation anchors the largest single pipeline of work across housing, transit, and utilities. A regional pivot toward private financing is quickening decisions, as data-center and electric-vehicle investors bypass slow public tenders. At the same time, sustainability rules under the ASEAN Taxonomy Version 4 have turned energy audits and green-bond verification into recurring revenue streams.

Key Report Takeaways

- By service type, Project Management Consultancy led with 46.55% of ASEAN construction consulting market share in 2025, whereas Design & Engineering Services is projected to advance at an 8.67% CAGR through 2031.

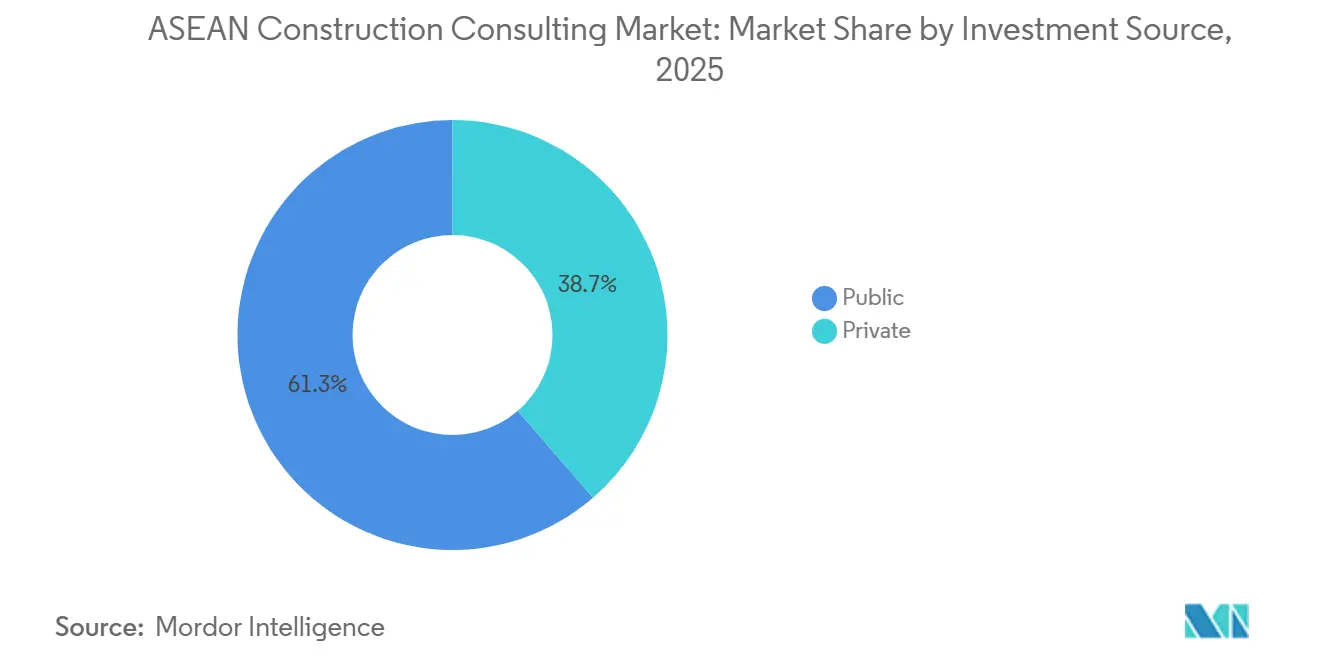

- By investment source, the public sector accounted for 61.33% of the ASEAN construction consulting market size in 2025; private-sector spending is rising fastest at an 8.06% CAGR to 2031.

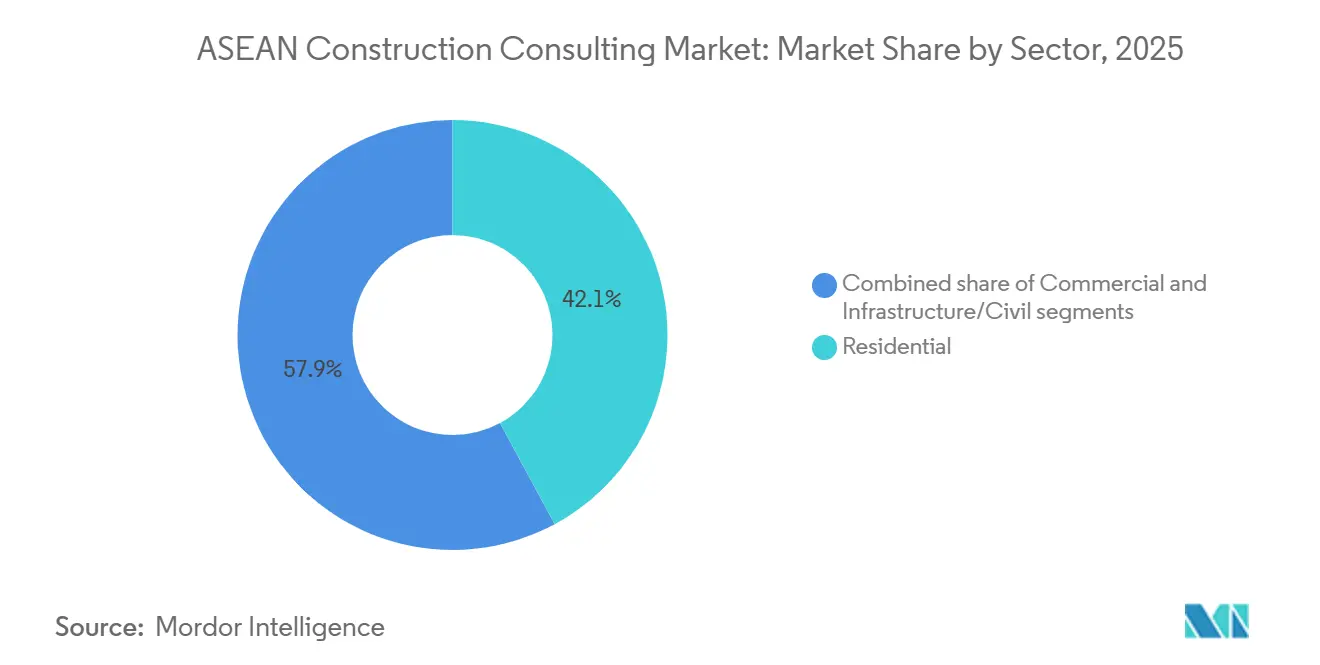

- By sector, Residential construction commanded 42.12% of consulting spend in 2025, yet Infrastructure consulting is expanding at the fastest pace with a 7.85% CAGR through 2031, driven by the ASEAN Power Grid's USD 764 billion cumulative investment requirement through 2045.

- By construction type, New construction dominated with 68.44% market share in 2025, while Renovation is forecast to grow at 8.19% CAGR through 2031, propelled by ASEAN Taxonomy Version 4 energy-performance thresholds and LEED recertification mandates.

- By geography, Indonesia captured 33.22% of regional consulting spend in 2025, anchored by Nusantara's Rp 130 trillion PPP pipeline, whereas Vietnam leads growth velocity at 8.19% CAGR, driven by semiconductor FDI exceeding USD 14.2 billion across 241 projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nusantara relocation unlocks megaproject pipelines | +1.5% | Indonesia, spillover to Malaysia & Singapore | Long term (≥ 4 years) |

| Semiconductor & EV clusters need specialized infra advice | +1.3% | Vietnam, Thailand, Malaysia | Long term (≥ 4 years) |

| Smart-city flagships expand integrated advisory scopes | +1.2% | Indonesia, Thailand, Philippines, Singapore | Medium term (2-4 years) |

| Multilateral blended-finance lifts PPP advisory volume | +1.1% | Vietnam, Philippines, Indonesia, Thailand | Medium term (2-4 years) |

| BIM mandates speed digital PMC adoption | +1.0% | Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Green-finance taxonomy drives sustainability consulting | +0.9% | ASEAN-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Indonesia’s Nusantara Capital-City Relocation Unlocking Megaproject Pipelines

Public-private commitments worth USD 8.6 billion were in place by mid-2025 for housing, toll roads, and urban rail. The U.S. Trade and Development Agency’s February 2026 smart-city planning grant confirms foreign appetite to test digital-twin concepts from day one. Relocating executive and legislative functions requires social infrastructure, utilities, and high-capacity transit, each with separate feasibility, design, and supervision scopes. International firms with Jakarta outposts are securing joint-venture roles, enlarging their foothold in the ASEAN construction consulting market.

Semiconductor & EV Manufacturing Clusters Driving Specialized Infra-Advisory

Vietnam logged USD 14.2 billion in chip investments across 241 projects, while Thailand’s draft Semiconductor Roadmap targets USD 70 billion by 2050. Factories require ultra-pure water, Class 100 cleanrooms, and hazardous-waste systems—disciplines beyond standard building services. Cross-border design-build-operate consortia are emerging to meet these needs, keeping specialized fees inside the ASEAN construction consulting market.

ASEAN Smart-City Flagship Projects Boosting Integrated Consulting Demand

The ASEAN Smart Cities Network listed 134 active initiatives in its 2025 review, and 81% remain under construction, ensuring multi-year demand for transit-oriented master plans and precinct design. Bangkok’s Bang Sue hub, Davao’s 600-kilometer bus rapid-transit grid, and Nusantara’s integrated command center illustrate how civil works now bundle data, cybersecurity, and Internet-of-Things layers. Winning consultants therefore field cross-disciplinary teams spanning civil, electrical, and data science, a combination that smaller local firms often lack. Integrated scopes translate into higher average fees and longer contract durations, underpinning revenue visibility across the ASEAN construction consulting market[1]ASEAN Taxonomy Board, “ASEAN Taxonomy Version 4,” asean.org .

ADB/AIIB Blended-Finance Envelopes Lifting PPP Transaction-Advisory Volumes

The Asian Infrastructure Investment Bank’s USD 300 million Project Crane loan to Philippine port terminals epitomizes a pipeline where sovereigns leverage private capital. Consultants craft risk-allocation matrices, tariff models, and bankable engineering studies. Expressways such as Vietnam’s Nam Dinh-Thai Binh BOT deal underscore the need for traffic forecasts, lender-engineer services, and safeguard compliance, deepening advisory workstreams across the ASEAN construction consulting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lowest-bid procurement bias shrinks value-added scopes | -0.8% | Indonesia, Philippines, Thailand | Short term (≤ 2 years) |

| Political-cycle project pauses disrupt cashflow | -0.6% | Thailand, Philippines, Malaysia | Short term (≤ 2 years) |

| Shortage of certified BIM/LEED/EDGE staff limits capacity | -0.5% | Thailand, Vietnam, Philippines, Indonesia | Medium term (2-4 years) |

| Cross-border labor accreditation gaps raise delivery frictions | -0.4% | ASEAN-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lowest-Bid Procurement Bias Shrinking Value-Added Scopes

Many sub-national tenders still weight 70-80% on price, deterring consultants from including lifecycle-cost analyses or digital-twin services. Multilateral guidelines advocate quality-cost evaluation, yet implementation remains patchy. Until ministries align on best-value procurement, margin pressure will linger. This dynamic particularly hurts mid-size firms within the ASEAN construction consulting market.

Political-Cycle Project Pauses Disrupt Cashflow

Thailand halted USD 40 billion in rail and flood schemes during its 2025 caretaker period, while the Philippines delayed the Manila Bay Bridge amid security reviews. Such pauses leave consultants holding idle staff and unrecovered bid costs. Diversification across sectors and borders is now a defensive priority for firms active in the ASEAN construction consulting market[2]Reuters, “Manila Bay Bridge Delay,” reuters.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Demand Shifts Toward Front-End Design Excellence

Project Management Consultancy captured 46.55% of ASEAN construction consulting market share in 2025 as owners sought single-point control from concept to commissioning. However, Design & Engineering Services is forecast to expand at 8.67% CAGR through 2031 thanks to BIM mandates that elevate model validation and digital coordination. CORENET X requires consultants to submit parametric files, pushing premiums for clash detection and 5D cost control. Feasibility and Detailed Project Reports remain smaller but carry high margins when tied to multilateral finance, often serving as gateways to later PMC roles. Master planning work accelerates in smart-city corridors, yet typically flows to niche urban-design studios partnering larger firms. Collectively, these shifts rebalance fees while raising technical barriers across the ASEAN construction consulting market.

Traditional PMC packages once centered on daily site supervision and progress reporting. Today, owners demand predictive scheduling, drone-based quantity verification, and carbon-tracking dashboards. Design houses with in-house software teams are edging into PMC territory, bundling concept, permitting, and construction analytics. Conversely, big PMCs are acquiring boutique designers to lock in the front end. The ASEAN construction consulting market size tied to integrated design-build-operate scopes, therefore, grows faster than standalone supervision contracts, rewarding firms that blur historic service lines.

By Sector: Infrastructure Consulting Gains on Residential Base

Residential projects accounted for 42.12% of ASEAN construction consulting spend in 2025 as Indonesia rushed housing in Nusantara and Metro Manila densified. Infrastructure consulting, though smaller, is expanding at a 7.85% CAGR, paced by power-grid interconnectors, expressways, and container terminals. The ASEAN construction consulting market size attached to transmission corridors alone could top USD 12 billion by 2031 if the Power Grid initiative hits scheduled milestones. Commercial segments lag in net new area but enjoy retrofit upside as landlords chase LEED Platinum recertification to secure cheaper green loans. Data-center campuses anchor a fast-growing sub-niche, demanding high-availability power studies and heat-recovery designs.

Transportation remains the single largest slice of infrastructure fees, driven by Vietnam’s USD 780 million Nam Dinh-Thai Binh expressway BOT and Thailand’s delayed but sizeable double-track rail pipeline. Energy and utilities trail closely, with cross-border high-voltage lines and on-site solar plus battery systems inside chip fabs. Social infrastructure, schools, and hospitals continue under lowest-bid rules in many countries, capping margins. Yet even here, pandemic-era air-quality standards create fresh advisory add-ons, helping firms defend pricing in the ASEAN construction consulting market.

By Construction Type: Renovation Outpaces New-Build Growth

New builds retained 68.44% of 2025 consulting revenue, but renovation work is on track for an 8.19% CAGR through 2031. Landlords in Jakarta, Kuala Lumpur, and Bangkok face stranded-asset risk if towers miss energy benchmarks, prompting deep-retrofit projects. Consultants earn performance-linked fees tied to verified kilowatt-hour savings, transforming what was once a one-off fit-out advisory into a five-year engagement. The ASEAN construction consulting market size attached to renovation is therefore climbing faster than the headline market, though from a smaller base.

New construction benefits from standardized digital libraries and modular off-site fabrication that shorten design cycles. Renovations, by contrast, need intrusive surveys, phased works, and tenant coordination, raising hourly rates by up to 20%. Firms that master laser scanning and point-cloud BIM earn a technological edge. Multilaterals now bundle resilience upgrades into waterway and port loans, blurring renovation with expansion scopes and enriching the ASEAN construction consulting market opportunity.

By Investment Source: Private Capital Accelerates

Public entities contributed 61.33% of 2025 consulting spend, yet private investment posts the faster 8.06% CAGR to 2031. Data-center clusters in Singapore and Johor, electric-vehicle gigafactories in Thailand, and semiconductor fabs in Vietnam select advisors based on time-to-market and technology depth, not the lowest fee. Contracts, therefore, carry performance bonuses and stiff delay penalties, lifting blended fee rates. Resultantly, the share of the ASEAN construction consulting market size funded by private sponsors rises steadily.

Government pipelines remain vital, especially for social and rural infrastructure. However, sovereign borrowing headroom is tightening, and blended-finance envelopes now push more risk to concessionaires. Consultants able to traverse both financing styles, sovereign and corporate, are cornering a larger wallet-share. Framework agreements with multilateral banks also lock in long-term visibility, stabilizing earnings within the ASEAN construction consulting market.

Geography Analysis

Indonesia generated 33.22% of regional advisory spend in 2025, anchored by Nusantara’s USD 8.6 billion pipeline and roads such as Package F, awarded at USD 37 million in June 2025. Japanese consultants, including Nippon Koei, dominate rail packages, while local firms backfill environmental and land-acquisition studies. Vietnam leads growth pace at an 8.19% CAGR, with USD 14.2 billion in chip and electronic projects demand specialty cleanroom and utilities design. The World Bank’s Southern Waterway Corridor revamp widens the scope further, embedding climate-resilience modeling in every detailed design.

Thailand absorbed political shocks in 2025 when caretaker rules froze USD 40 billion of work, yet its January 2026 semiconductor roadmap seeks USD 70 billion over 25 years, creating deep benches of design and supervision contracts. Concurrently, the electric-vehicle ecosystem has mobilized an additional USD 4 billion, sustaining factory utilities consulting. The Philippines relies on blended-finance ports and Davao’s transport overhaul, but project pauses, such as the Manila Bay Bridge, show how security reviews can stall pipelines. Malaysia’s value rests on data-center campuses and BIM pilots that cut permitting times; digital-ready consultants capture outsized fees here[3]Malaysia Construction Industry Development Board, “National BIM e-Submission,” cidb.gov.my.

Singapore commands premium pricing thanks to CORENET X compliance and serves as a hub for ASEAN headquarters of global firms like Meinhardt and WSP. Smaller economies, Laos, Cambodia, Brunei, Myanmar, account for limited spend yet throw up greenfield opportunities such as Vientiane’s water-supply expansion. Overall, Southeast Asia’s consulting geography is re-balancing toward Vietnam and Thailand on manufacturing pull, while Indonesia remains the volume anchor for the ASEAN construction consulting market.

Competitive Landscape

The ASEAN construction consulting market is highly fragmented; the five largest firms together account for under 20% of revenue. International giants such as WSP deepened regional reach by buying Ricardo plc in June 2025, adding energy and carbon expertise popular with data-center and chip-fab investors. Japanese specialists, Nippon Koei and Oriental Consultants, are teaming with local entities for permitting.

Regional integrators are responding with strategic alliances. Meinhardt’s January 2025 pact with Japan Overseas Infrastructure Investment Corporation secures soft financing and early-stage smart-city roles. Surbana Jurong, supported by a USD 1.5 billion revolving credit line, bundles master planning, project management, and guarantee underwriting, attractive to fiscally constrained municipalities. Korean, Indian, and Thai firms increasingly form tri-partite joint ventures to win complex aviation and port jobs, evidenced by the July 2025 U-Tapao runway award.

Technology is becoming the new battleground. Cloud-based digital-twin platforms allow clients to self-perform progress tracking, forcing consultants to add predictive analytics and performance guarantees. Firms without proprietary data tools risk relegation to low-margin supervision. Talent scarcity compounds challenges; wage inflation favors employers who offer cross-border career paths. As fee structures shift from hours to outcomes, the ASEAN construction consulting market rewards players that marry domain depth with software fluency.

ASEAN Construction Consulting Industry Leaders

WSP

Mott MacDonald

Arup

Stantec

SMEC (Surbana Jurong)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Asian Infrastructure Investment Bank approved a USD 300 million loan for International Container Terminal Services’ Philippine port upgrade.

- February 2026: USTDA issued a USD 2.49 million grant for Nusantara smart-city master planning with seven U.S. tech partners.

- January 2026: Viettel began construction on Vietnam’s first 32-nm semiconductor fab, targeting 2028 pilot output.

- October 2025: ADB and World Bank launched a combined USD 12.5 billion ASEAN Power Grid financing window.

ASEAN Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design & Engineering Services |

| Master Planning & Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Indonesia |

| Vietnam |

| Thailand |

| Philippines |

| Malaysia |

| Singapore |

| Rest of ASEAN |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design & Engineering Services | ||

| Master Planning & Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Key Countries | Indonesia | |

| Vietnam | ||

| Thailand | ||

| Philippines | ||

| Malaysia | ||

| Singapore | ||

| Rest of ASEAN | ||

Key Questions Answered in the Report

What is the current value of the ASEAN construction consulting market?

The market stands at USD 71.3 billion in 2026 and is projected to reach USD 99.10 billion by 2031.

Which service type captures the largest revenue share?

Project Management Consultancy leads with 46.55% of 2025 revenue, reflecting demand for single-point accountability across project phases.

Where is growth fastest geographically?

Vietnam posts the quickest expansion with an 8.19% CAGR, fueled by semiconductor and power-grid investments.

How are BIM mandates influencing consultancy selection?

Digital submission rules in Singapore and Malaysia favor firms with certified BIM teams, driving consolidation and premium pricing.

What is driving the rise in private-sector consulting spend?

Data-center, semiconductor, and electric-vehicle investors award design-build-operate advisory packages outside slow public tenders, pushing private spend to an 8.06% CAGR.

Page last updated on: