ASEAN Probiotic Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

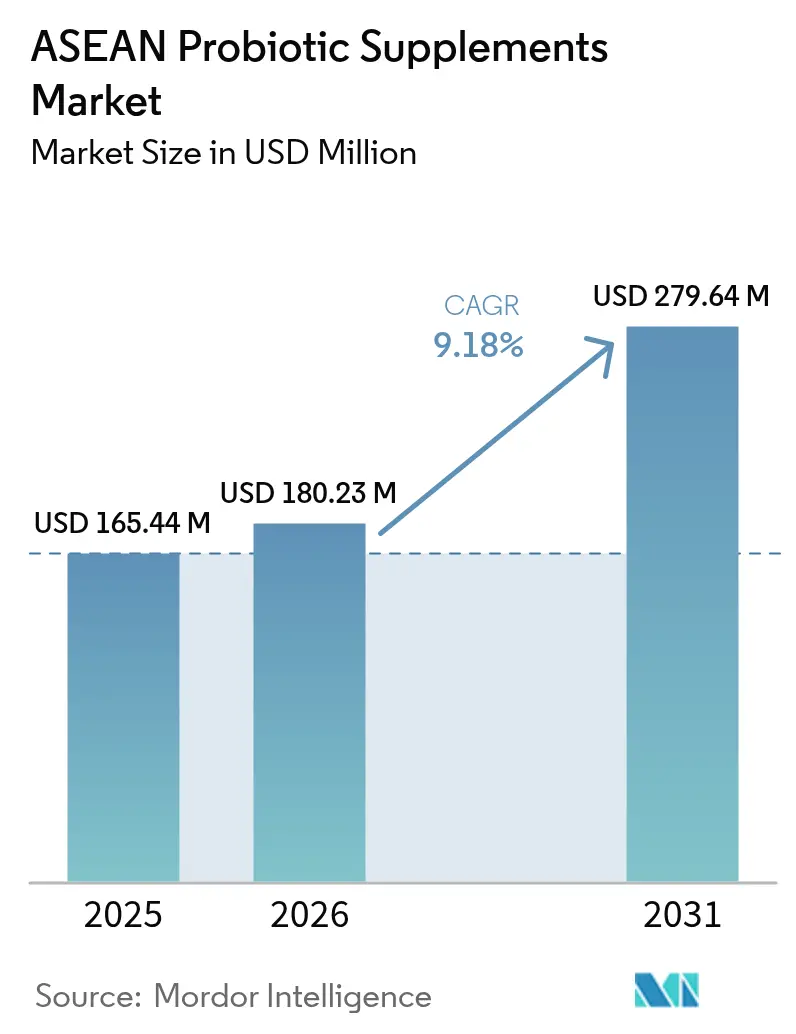

| Base Year Market Size (2025) | USD 165.44 Million |

| Market Size (2026) | USD 180.23 Million |

| Market Size (2031) | USD 279.64 Million |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

ASEAN Probiotic Supplements Market Analysis by Mordor Intelligence

The ASEAN probiotic supplements market size was valued at USD 165.44 million in 2025, and estimated to grow from USD 180.23 million in 2026 to reach USD 279.64 million by 2031, registering a CAGR of 9.18% during 2026-2031. The ASEAN probiotic supplements market is growing due to increasing consumer awareness of digestive health and immunity, alongside a rise in lifestyle-related gut disorders caused by urban diets and stress. The demand is further driven by a shift toward preventive healthcare and natural remedies, particularly among younger and aging populations seeking daily wellness solutions. The rapid expansion of e-commerce and pharmacy retail chains has enhanced product accessibility, while manufacturers are offering diverse formats such as gummies, sachets, and capsules to cater to local preferences. Additionally, heightened interest in the gut-brain connection, supported by endorsements from healthcare professionals and influencers, is promoting regular probiotic consumption across Southeast Asia.

Key Report Takeaways

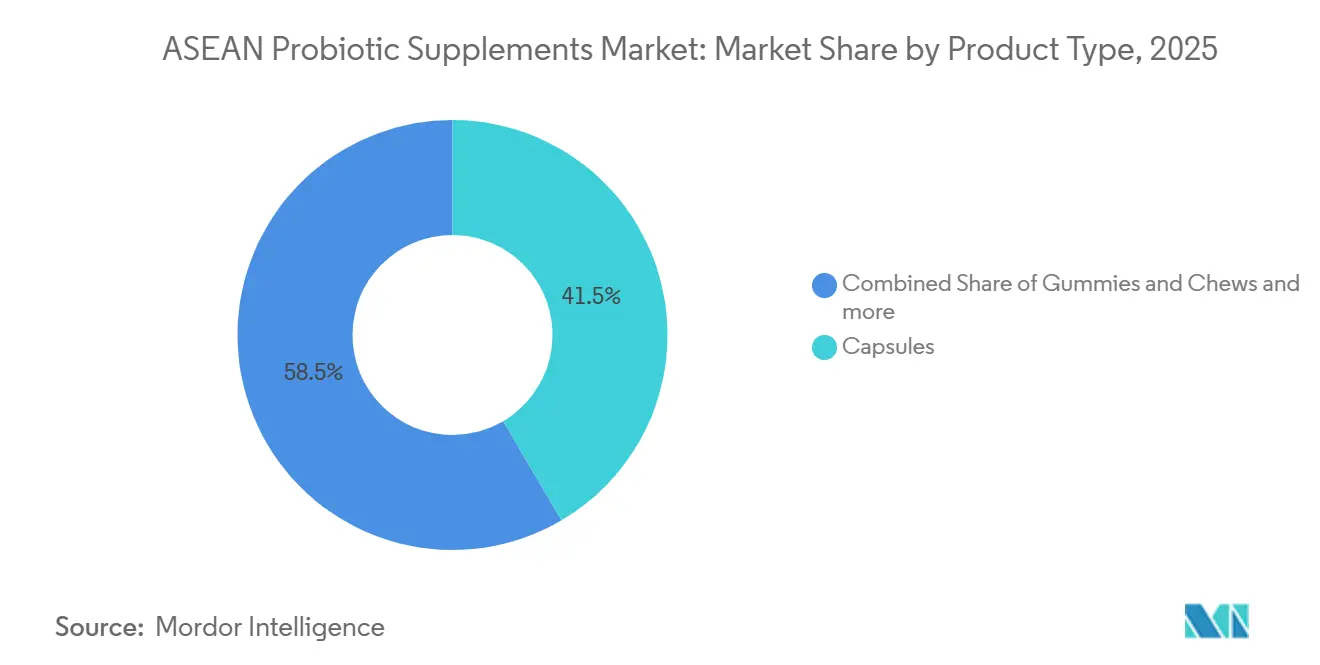

- By product type, capsules led with 41.53% of ASEAN probiotic supplements market share in 2025; gummies and chews are projected to expand at a 10.46% CAGR through 2031.

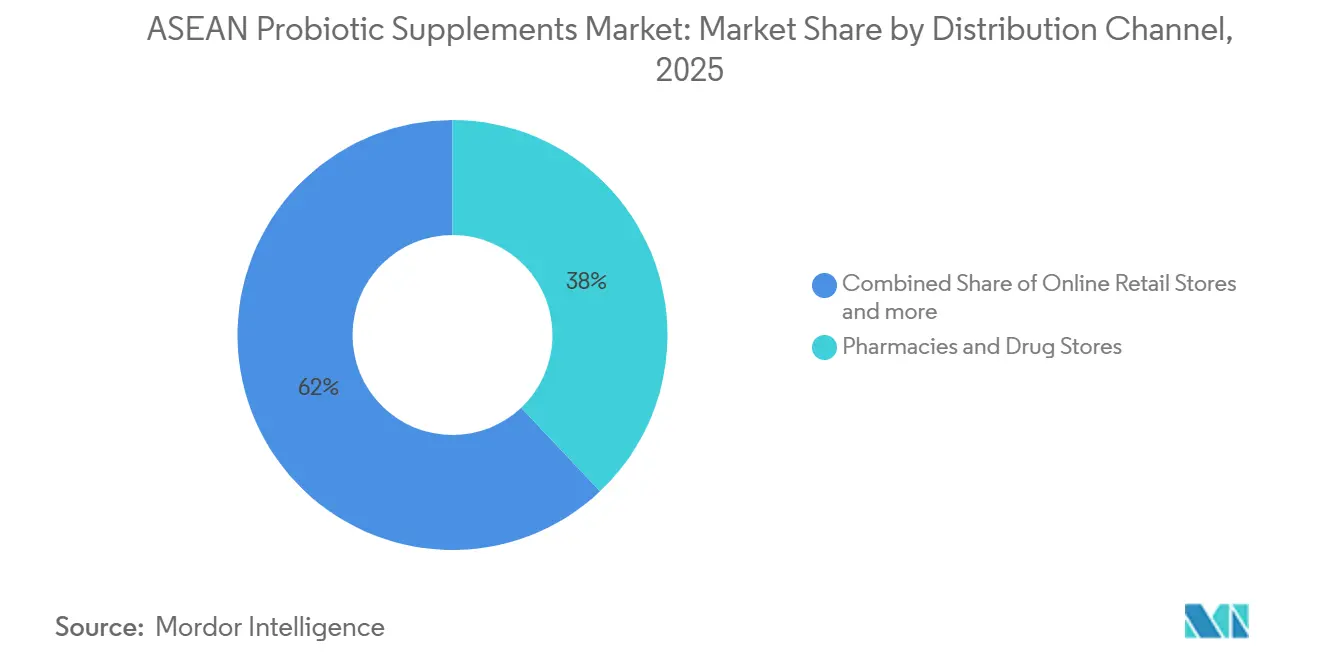

- By distribution channel, pharmacies and drug stores held 37.96% share of the ASEAN probiotic supplements market size in 2025; online retail stores are forecast to advance at a 12.23% CAGR to 2031.

- By geography, Singapore dominated with 39.75% revenue share in 2025; the Philippines is projected to record a 10.23% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Probiotic Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on health and overall wellbeing | +2.0% | Strongest uptake in Singapore, Thailand, and urban Indonesia | Medium term (2-4 years) |

| Rising incidence of gastrointestinal disorders | +1.5% | Indonesia, Philippines, Vietnam; lower in Singapore | Long term (≥ 4 years) |

| Shift toward natural, preventive healthcare solutions | +1.8% | Vietnam, Thailand, Malaysia; integration with traditional medicine practices | Medium term (2-4 years) |

| Continuous product innovation and varied formulations | +1.2% | Singapore, Malaysia, Thailand; R&D hubs and ingredient suppliers | Short term (≤ 2 years) |

| Promotion through influencers and digital platforms | +1.5% | Philippines, Indonesia, Vietnam; high social-media penetration | Short term (≤ 2 years) |

| Increasing recognition of the gut–brain connection | +0.8% | Singapore, urban Malaysia, Thailand; educated consumer segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on health and overall wellbeing

The growing focus on personal wellness across ASEAN countries is significantly driving the adoption of probiotic supplements, as consumers increasingly prioritize preventive care over treatment-based healthcare. Urban populations are actively seeking to maintain immunity, digestion, and energy levels through daily nutritional support, particularly following heightened health awareness in recent years. This shift is reflected in rising healthcare expenditures; for instance, Singapore’s health expenditure per capita reached USD 3,921.60 in 2023, demonstrating a greater willingness to invest in products that support long-term health[1]Source: The World Bank Group, "Current health expenditure per capita (current US$) - Singapore," data.worldbank.org. Consequently, probiotics are becoming an integral part of routine self-care, promoting gut balance, metabolic health, and overall well-being, thereby sustaining demand across the region.

Rising incidence of gastrointestinal disorders

The increasing prevalence of digestive issues in ASEAN countries is driving the demand for probiotic supplements, as consumers seek non-pharmaceutical solutions to address gut discomfort, bloating, and irregular bowel movements. In Indonesia, rapid urbanization and the adoption of Western dietary habits have led to a rise in lactose intolerance and microbiome imbalances, prompting greater use of gut-supportive products. In line with this trend, the national regulator BPOM introduced Peraturan No. 15 in September 2024, mandating clearer labeling of probiotic strain names and colony-forming unit (CFU) counts to help consumers select appropriate formulations[2]Source: The Indonesian Food and Drug Administration (BPOM), "BPOM Regulation No. 17 of 2025," pom.go.id. This regulatory focus underscores the significance of digestive health concerns and enhances consumer trust, thereby supporting the growth of probiotic supplement adoption across the ASEAN market.

Shift toward natural, preventive healthcare solutions

Consumers in ASEAN are increasingly shifting from reactive treatment methods to preventive care by incorporating naturally derived products, which is boosting the demand for probiotic supplements. Concerns about the long-term reliance on synthetic medicines and their potential side effects have led individuals to adopt microbiome-supportive nutrition to enhance immunity, digestion, and metabolic balance before health issues develop. Probiotics are viewed as mild, food-based wellness solutions that integrate seamlessly into daily routines, aligning with the region's established tradition of functional foods and herbal remedies. This proactive approach to health maintenance, rather than addressing illnesses after they occur, is driving steady adoption of probiotic supplements across various age groups.

Continuous product innovation and varied formulations

Innovation in probiotic supplement design is driving market growth across ASEAN, as manufacturers introduce formats tailored to diverse consumer lifestyles and preferences. Companies are expanding beyond traditional capsules to include gummies, chewables, sachets, stick packs, and ready-to-mix powders, enhancing convenience and appeal for children, adults, and the elderly. Developments in strain stability, shelf-life technology, and targeted formulations for immunity, women’s health, and digestive health further improve product effectiveness and differentiation. These specialized and user-friendly options promote trial and repeat usage, increasing consumer engagement and boosting demand for probiotic supplements in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated R&D and manufacturing expenses | -0.9% | Acute pressure on smaller ASEAN manufacturers lacking scale | Medium term (2-4 years) |

| Competition from functional and fortified food products | -0.7% | Thailand, Vietnam, Indonesia; strong yogurt and fermented-beverage markets | Short term (≤ 2 years) |

| Limited consumer understanding and trust issues | -0.5% | Indonesia, Philippines, Vietnam; lower health literacy and regulatory enforcement | Long term (≥ 4 years) |

| Presence of counterfeit and substandard products | -0.5% | Malaysia, Indonesia, Philippines; porous borders and e-commerce gray markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from functional and fortified food products

The ASEAN probiotic supplements market is challenged by the increasing presence of functional and fortified foods that naturally include beneficial bacteria in daily diets. Items such as probiotic yogurt, fermented beverages, fortified dairy alternatives, and nutrition bars offer comparable digestive and immunity benefits while being viewed as more convenient and familiar compared to pills or powders. These products integrate seamlessly into regular meals and snacks, making them a preferred choice for many consumers, particularly in price-sensitive markets. This preference reduces the adoption of standalone supplements and hampers repeat purchases, thereby constraining overall market growth.

Presence of counterfeit and substandard products

The ASEAN probiotic supplements market faces challenges due to the prevalence of counterfeit and low-quality products, which undermine consumer trust in the safety and efficacy of these supplements. Issues such as inconsistent strain viability, inaccurate labeling, and improper storage conditions often result in products delivering fewer live cultures than advertised, fostering skepticism among consumers. Regulatory authorities are taking steps to address these concerns. For example, Singapore’s Health Sciences Authority intensified its enforcement efforts in 2024, confiscating 970,707 units of illegal health products and removing 7,351 online listings through coordinated surveillance and joint operations[3]Source: The Health Sciences Authority (HSA) Singapore, "HSA Seized Over 970,000 Units of Illegal Health Products and Removed More Than 7,000 Illegal Product Listings in 2024," hsa.gov.sg. These incidents underscore the extent of unauthorized sales, prompting greater consumer caution and slowing the adoption of legitimate probiotic supplements in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gummies Reshape Format Preferences

Capsules held a 41.53% market share in 2025, reflecting their established position as the default delivery format for probiotic supplements, yet gummies and chews are projected to grow at 10.46% CAGR through 2031, signaling a fundamental shift in consumer preferences toward palatability and convenience. The demand for capsule-based probiotic supplements in ASEAN is influenced by consumer preferences for precise dosage, clinical reliability, and extended shelf life. Capsules are commonly associated with pharmacy-grade products, appealing to adults and older consumers seeking targeted digestive or immunity support as recommended by healthcare professionals. They are also convenient for daily use, easy to carry during travel, and suitable for formulations that require protection from moisture and heat, particularly in tropical climates. Furthermore, increasing awareness of specific probiotic strains and CFU counts drives consumers to prefer capsules, as they are perceived to offer consistent potency and therapeutic efficacy.

The growth of probiotic gummies and chewable formats in ASEAN is driven by rising demand for convenient and enjoyable wellness products, particularly among children, teenagers, and young adults. These formats address the discomfort of swallowing pills and align with the regional preference for functional foods and snack-like nutrition. Features such as appealing flavors, vibrant presentation, and options with reduced sugar or added vitamins promote regular consumption and spur impulse purchases, especially through online retail platforms. Additionally, busy urban lifestyles and increasing interest in preventive health further bolster this segment, as consumers look for supplements that easily fit into their daily routines.

By Distribution Channel: E-Commerce Disrupts Pharmacy Dominance

Pharmacies and drug stores commanded a 37.96% market share in 2025, yet online retail stores are expanding at 12.23% CAGR through 2031. Probiotic supplement sales through pharmacies and drug stores in ASEAN are driven by strong consumer trust in pharmacists' guidance and the perception of medical reliability. Many consumers prefer purchasing probiotics from regulated outlets where they can obtain advice on strain suitability, dosage, and compatibility with medications, particularly for digestive disorders or post-antibiotic recovery. These channels also benefit from doctor recommendations, insurance-linked purchases, and the availability of clinically positioned brands, making them the preferred choice for adults and older consumers seeking safe and verified products.

Online channels are experiencing rapid growth due to their convenience, broader product selection, and competitive pricing compared to physical stores. These platforms enable consumers to compare strains, CFU levels, and reviews, facilitating informed purchasing decisions without the need to visit a pharmacy. E-commerce platforms often provide discounts, subscription-based delivery options, and access to international brands that are not commonly available offline, appealing particularly to younger, tech-savvy consumers. Additionally, factors such as social media influence, health-focused content marketing, and doorstep delivery contribute to repeat purchases, positioning online retail as a significant driver of probiotic supplement sales across ASEAN.

Geography Analysis

Singapore accounted for 39.75% of ASEAN probiotic supplement revenue in 2025, driven by the fast-paced urban lifestyle, where irregular eating habits and frequent dining out prompt consumers to adopt daily digestive support routines. The highly educated population actively monitors nutritional information and is open to science-based wellness trends, such as microbiome testing and personalized nutrition plans. Preventive health screenings and corporate wellness programs further encourage individuals to prioritize internal health balance. Additionally, strong purchasing power and exposure to international health brands contribute to the adoption of premium formulations targeting performance, skin health, and metabolic balance, beyond basic digestive support.

The Philippines is forecast to grow at 10.23% CAGR through 2031, driven by a young population focused on daily vitality, skin health, and weight management, fostering interest in microbiome-support products beyond digestive health. The frequent consumption of sweetened beverages and fast food in urban areas has led consumers to incorporate nutritional supplements into their modern lifestyle routines for balance. The influence of beauty and wellness communities, particularly those emphasizing the connection between gut health, acne, and energy levels, further enhances acceptance. Moreover, the increasing availability of probiotics in convenience stores and bundled wellness packs has improved accessibility for middle-income households, contributing to consistent market growth.

In Thailand, the demand for probiotic supplements is driven by a strong cultural association with fermented foods, fostering consumer receptiveness to microbiome-supporting nutrition in supplement form. The emphasis on holistic wellness practices, including traditional remedies and spa-based health routines, encourages the use of products aimed at maintaining internal balance as part of daily self-care. Additionally, increasing participation in fitness activities and weight management programs has heightened interest in supplements that support metabolism and nutrient absorption. Moreover, active promotion by pharmacies and wellness clinics, through health check packages and personalized recommendations, is contributing to the growing adoption of probiotics among urban populations.

Regulatory Landscape

Regulatory approaches differ across ASEAN. Indonesia, Malaysia, Philippines, and Thailand have enacted specific probiotic regulations, while Singapore and Vietnam allow sales without country-specific probiotic regulations. Malaysia's Food Safety and Quality Division (FSQD) of the Ministry of Health regulates probiotics under the Food Regulation 1985, with Regulation 26A gazetted in April 2017. Thailand's Ministry of Public Health uses Notifications 339/2011 and 346/2012 to define probiotic use in food and supplements.

Competitive Landscape

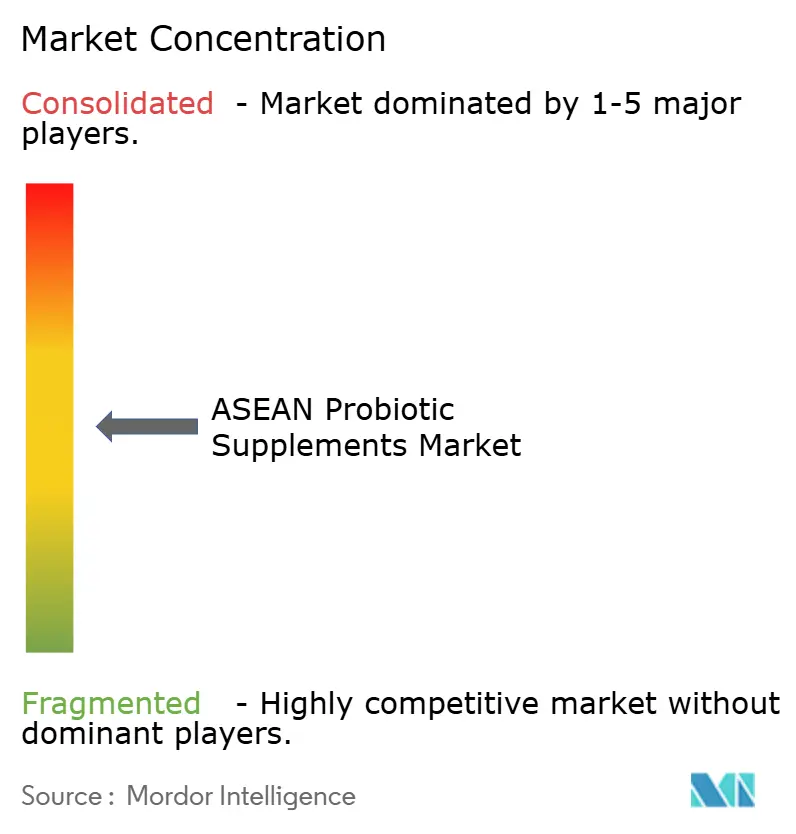

The ASEAN probiotic supplements market is moderately fragmented, characterized by a mid-level concentration. Global companies leverage strong brand recognition and extensive distribution networks, while regional players focus on competitive pricing and formulations tailored to local health preferences. Established brands benefit from cross-category visibility, supported by probiotic beverage portfolios distributed through large retail networks in countries such as Indonesia, Thailand, and the Philippines. This visibility enhances consumer awareness and indirectly boosts supplement sales. Additionally, ingredient manufacturers are increasingly moving downstream by collaborating to develop synbiotic blends for infant and early-life nutrition, signaling a shift toward direct participation in finished consumer products rather than solely supplying raw materials.

Ongoing consolidation is evident as smaller firms without proprietary strains or extensive retail networks face challenges in sustaining research investments and competing with diversified multinational portfolios. Despite this, several growth opportunities remain, particularly in psychobiotic products targeting mental well-being, postbiotic solutions that eliminate refrigeration requirements, and strain-specific offerings addressing regional health concerns, such as Helicobacter pylori prevalence. Retail chains are also fostering domestic wellness brands by providing integrated offline and digital distribution support. Online-first labels, in particular, are gaining traction due to stronger consumer engagement and higher repeat purchase rates compared to traditional products.

Technology adoption is transforming competition in the market. Innovations such as authentication tools to prevent counterfeits, interactive packaging linked to educational content, and AI-based personalization platforms recommending strains based on consumer health profiles are gaining prominence. Investments in delivery technologies, including lipid carriers and protective bead systems, underscore the importance of formulation intellectual property as a key differentiator. Concurrently, regional regulatory coordination efforts aimed at harmonizing testing standards may reduce compliance complexities and facilitate faster cross-border expansion for probiotic supplement manufacturers operating across Southeast Asia.

ASEAN Probiotic Supplements Industry Leaders

-

Reckitt Benckiser

-

BioGaia AB

-

Nestlé

-

Procter & Gamble

-

Church & Dwight

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The ASEAN probiotic supplements market is estimated at USD 1.8 billion in 2026. Demand is supported by functional food integration, gut-brain axis research applications, and the expansion of e-commerce platforms. For product and brand planning, pediatric and women's health segments in ASEAN markets offer clear room for product fit and range expansion. In logistics, Thailand functions as a key regional gateway, with the Laem Chabang Deep Sea Port supporting probiotic movement into nearby markets.

Recent Industry Developments

- July 2026: Nestlé Thailand Co., Ltd. launched S-26 Progress Smart-C 3 infant formula containing L. reuteri probiotics imported from Switzerland in Thailand. The product adds to Nestlé's premium probiotic infused formula options in the ASEAN market and reinforces its position in the Thai pediatric segment.

- April 2026: BioGaia AB expanded availability of Prodentis Fresh Breath into China via cross-border trade e-commerce. The move highlights how the company is using cross-border online retail to access a larger, faster-growing consumer base for probiotic health products.

- February 2026: BioGaia AB launched Fresh Breath probiotic supplement in South Korea; exploring distribution in Malaysia and Singapore. The launch introduces BioGaia's probiotic oral health product in South Korea with a pathway for further regional distribution.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers retail and practitioner-sold probiotic supplements across ASEAN, counted in value terms at the point of sale and converted into USD for consistent comparison across countries.

Scope exclusions: We exclude fermented foods and beverages, conventional pharmaceuticals without live probiotic positioning, and bulk probiotic ingredients sold only for manufacturing use.

Segmentation Overview

-

By Product Type

- Tablets

- Capsules

- Gummies and Chews

- Liquids

- Others

-

By Distribution Channel

- Pharmacies and Drug Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Singapore

- Philippines

- Rest of ASEAN

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the basic demand and supply picture for supplements in ASEAN, and then narrowing it down to probiotic formats that shoppers actually buy. We lean on public statistics and reference material such as national health and food regulators across ASEAN, UN Comtrade for cross-border flows, World Bank macro indicators, and WHO guidance that helps interpret health claim and labeling signals.

To make the numbers usable for sizing, we also read brand and distributor disclosures such as annual reports and investor presentations, supported by reputable press and association updates on vitamins and dietary supplements. Where helpful, we use paid subscriptions for company financials and news, import or export shipment level signals, and patent databases to validate which strains and delivery formats are actively being commercialized. These examples are not exhaustive, and many other public and paid sources are reviewed to collect data, cross-check assumptions, and close clarity gaps.

Primary Interviews and Surveys

Primary work is used to confirm what is really sold as a probiotic supplement in each country, and to pressure-test pricing, pack sizes, and channel splits before totals are locked. We speak with a mix of supplement brands, distributors, retailers, and healthcare linked stakeholders across key ASEAN markets, and then use their inputs to triangulate coverage gaps that desk sources cannot fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 21% | |

| Mid tier: 43% | Functional/Unit leaders: 30% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Sizing begins from a top-down view where country supplement spending, channel development, and trade signals are used to reconstruct the realistic addressable pool for probiotic supplements, and then split by formats and selling channels. Once that structure is in place, selective bottom-up checks are run, such as sampled shelf price tracking by pack size and dosage form, and volume sense-checks using distributor throughput discussions, which are then used to adjust totals where the first pass looks stretched.

Key inputs that shape the model include average selling prices by format (capsules, tablets, gummies and chews, liquids), online versus pharmacy share movement, pack size mix shifts that affect unit economics, import reliance versus local manufacturing intensity, and regulation-driven claim constraints that can cap premium pricing. When data is missing for smaller countries, we fill gaps using proxy ratios tied to population, income, and channel maturity, and then validate those ratios through interviews. Forecasts are built using scenario analysis anchored on expected channel expansion and price progression, with assumptions kept consistent across countries so the regional total stays internally coherent.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number does not depend on any single dataset. We compare outputs against independent signals like import directionality, shelf price ranges, and the implied per-capita spend, and then investigate variances that sit outside a reasonable band before sign-off.

Each model pass is reviewed by another analyst, followed by a final consistency review that looks for currency conversion timing issues, unusual price jumps, and channel shares that do not match interview feedback. Reports refresh annually, and interim updates are triggered when material events occur, such as regulation changes or sudden pricing shocks. Right before delivery, a fresh scan is performed so clients receive the latest updated view.

Mordor Intelligence's Asean Probiotic Supplements Market Size Versus Other Published Estimates

Published market values for probiotic supplements in ASEAN often differ because the inputs behind them are not fully aligned, even when the titles look similar. The most common reasons are different country coverage within ASEAN, different rules on what qualifies as a supplement versus a functional food, and different treatment of online pricing and promotional discounting.

In this report, extra attention is placed on refresh timing, consistent FX conversion windows, and repeat checks on shelf prices by pack size and dosage form, which is why the value anchored by Mordor Intelligence can land away from figures that use older exchange rates or a single average price for all formats.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 165.44 M (2025) | |

| Global Consultancy A | USD 1.80 B (2026) | This figure appears to apply a broader probiotic scope and a higher average price assumption, and it also uses a different base year, which can inflate ASEAN totals when currency timing and discount depth are not normalized. |

| Industry Report B | USD 0.96 B (2023) | This number is stated for a wider Southeast Asia probiotics space and not strictly supplements, and it is anchored to an earlier year, so later channel expansion and the mix shift into gummies and chews are not reflected the same way. |

Overall, the spread is mainly explained by scope boundaries and timing choices, rather than arithmetic differences. By keeping pricing logic tied to observable pack sizes and channel realities, and by aligning currency conversion to the sizing year, the resulting estimate stays traceable to inputs that can be rechecked and updated with each annual refresh.

Key Questions Answered in the Report

What is the current value of the ASEAN probiotic supplements market?

The market is valued at USD 179.99 million in 2026 and is projected to reach USD 278.45 million by 2031.

How big is the ASEAN probiotic supplements market today and how fast is it growing?

It reached USD 180.23 million in 2026 and is on track to hit USD 279.64 million by 2031, advancing at a 9.18% CAGR over 2026-2031.

Which product format currently sells the most?

Capsules account for 41.53% of 2025 revenue, retaining leadership owing to clinician recommendation and shelf stability.

Which format is expected to grow fastest through 2031?

Gummies and chews lead growth with a projected 10.46% CAGR, driven by taste appeal and pediatric acceptance.

Which country contributes the most revenue?

Singapore generated 39.75% of regional sales in 2025, reflecting high per-capita health spending and strict quality controls

Page last updated on: