North America Probiotics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

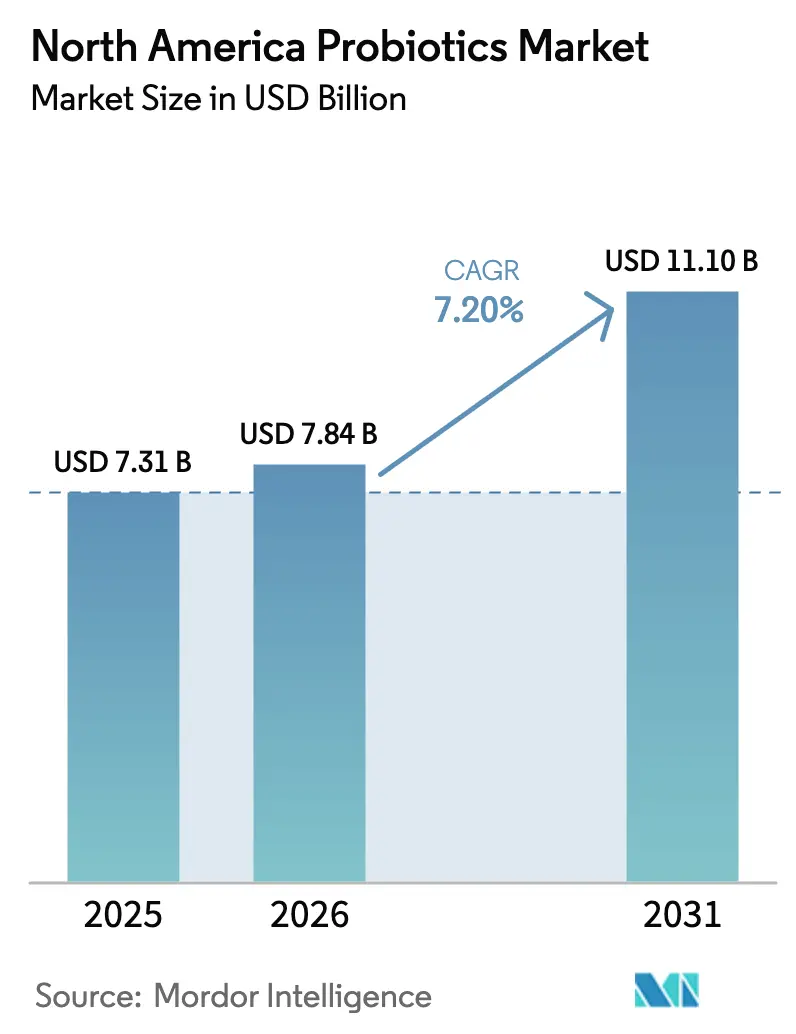

| Base Year Market Size (2025) | USD 7.31 Billion |

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 11.10 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

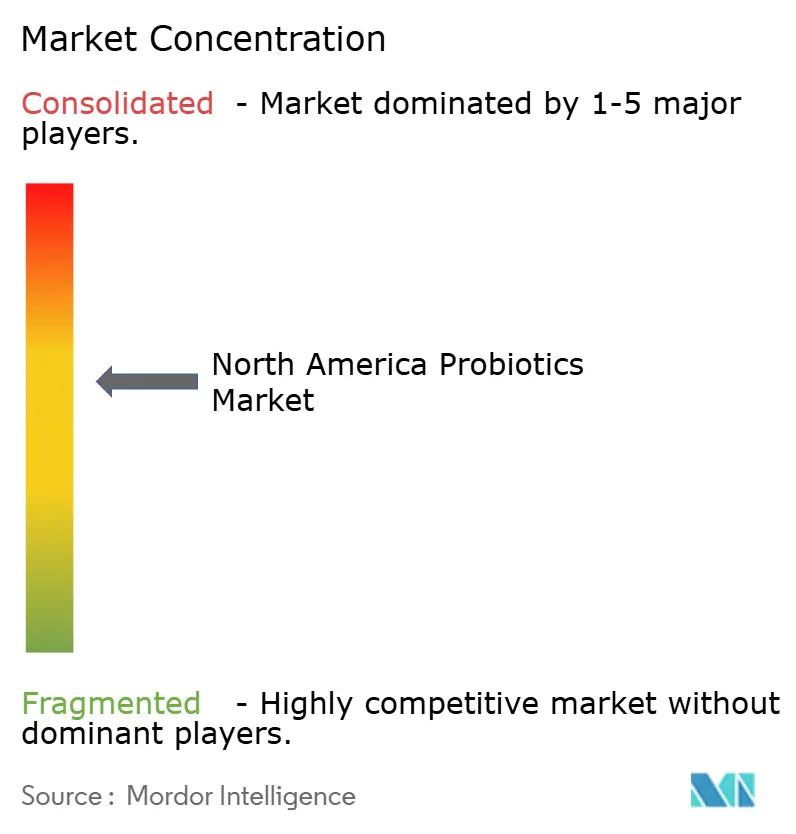

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Probiotics Market Analysis by Mordor Intelligence

The North America probiotics market was valued at USD 7.31 billion in 2025, and is estimated to grow from USD 7.84 billion in 2026 to reach USD 11.10 billion by 2031, growing at a CAGR of 7.20% during the forecast period. This is driven by heightened consumer awareness of the link between gut health and immune function, as well as the increasing role of digestive wellness in preventive healthcare strategies. Probiotics are widely recognized for their therapeutic and preventive benefits, including support for conditions such as lactose intolerance and inflammatory bowel disease. Market expansion is further supported by improved consumer education regarding probiotic efficacy and greater availability of probiotic supplements across retail channels. As preventive healthcare and digestive health remain key consumer priorities, the North American probiotics market is expected to sustain strong growth momentum. Product innovation has been a critical competitive lever, with manufacturers launching advanced formulations and diversified delivery formats to address evolving consumer preferences. In addition, the growing penetration of probiotic-fortified functional foods, beverages, dietary supplements, and pharmaceutical applications has broadened the market beyond traditional dairy-based products, creating new revenue opportunities across multiple segments.

Key Report Takeaways

- By product type, probiotic foods led with 61.08% of the North American probiotics market share in 2025, whereas probiotic drinks are set to expand at a 9.54% CAGR through 2031.

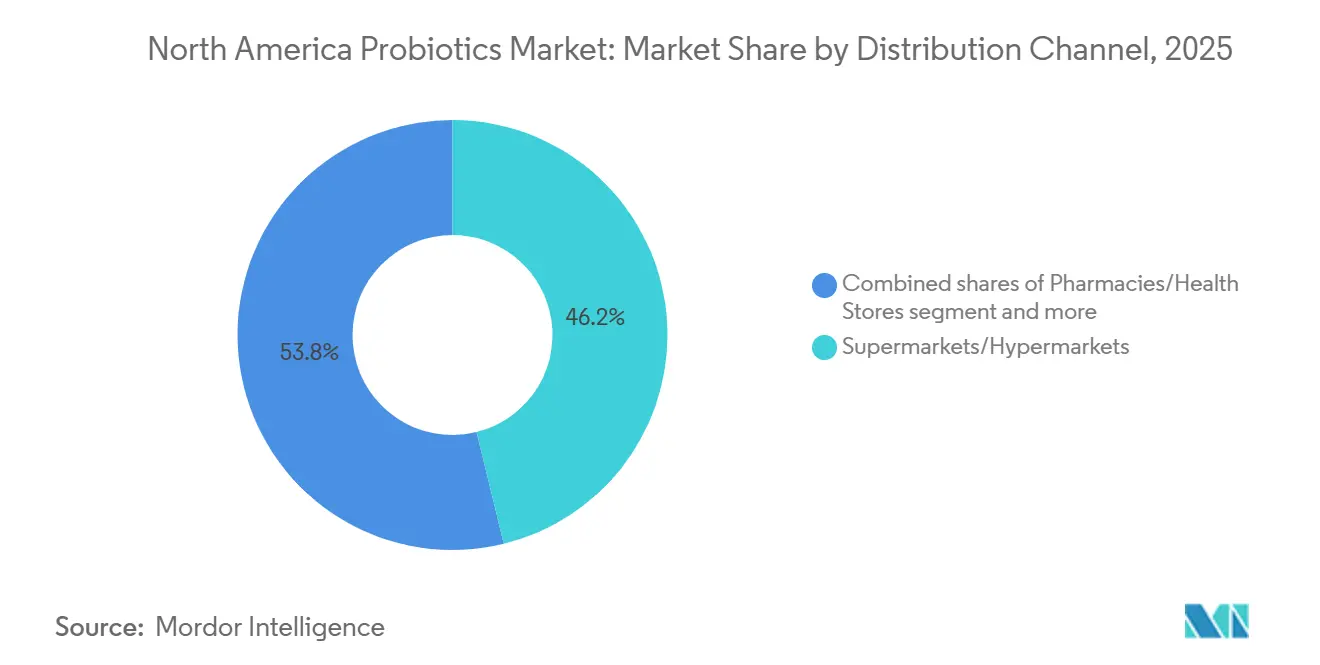

- By distribution channel, supermarkets and hypermarkets commanded 46.16% of the North American probiotics market size in 2025; online retail stores represent the fastest trajectory at a 9.21% CAGR to 2031.

- By geography, the United States held 79.50% of the North American probiotics market share in 2025, while Mexico is poised for the quickest rise with a 9.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing focus on digestive wellness demand | +1.5% | National, strongest in United States and Canada | Medium term (2-4 years) |

| Preventive healthcare drives everyday probiotic use | +1.3% | United States, Canada; early adoption in Mexico metropolitan areas | Long term (≥ 4 years) |

| Dairy-free and plant probiotics expand consumers | +1.2% | United States and Canada urban centres; niche in Mexico | Medium term (2-4 years) |

| E-commerce growth improves probiotic accessibility | +1.0% | United States and Canada; nascent in Mexico | Short term (≤ 2 years) |

| Recognition of immune benefits fuels market growth | +0.9% | United States and Canada; growing awareness in Mexico | Medium term (2-4 years) |

| Interest in functional and fermented foods rises | +0.8% | Urban North America, expanding to suburbs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing focus on digestive wellness demand

Digestive health has emerged as a high-growth opportunity, now ranking as the fourth most sought-after health benefit among U.S. consumers, with 36% actively seeking gut-health solutions across foods, beverages, and supplements[1]Source: International Food Information Council, "2024 IFIC Food & Health Survey," ific.org. Younger cohorts, particularly Gen Z and Millennials, are accelerating category momentum by linking digestive health with adjacent benefits such as energy, weight management, and overall performance. This enables brands to expand beyond traditional supplements into probiotic-enhanced snacks, beverages, and meal replacements with broader lifestyle positioning. The North American market has witnessed increased investment in research and development by major manufacturers to develop innovative probiotic formulations targeting specific health conditions, as exemplified by Danone's 2024 establishment of the Activia Gut Health Board, which aims to provide expert guidance and support for improving digestive health. From a regulatory perspective, the U.S. environment is supportive. The FDA’s structure/function claim framework permits digestive health messaging without premarket approval, lowering regulatory hurdles and accelerating SKU development and portfolio expansion. Together, these factors make digestive health a scalable platform for growth, differentiation, and cross-category innovation.

Dairy-free and plant probiotics expand consumers

Plant-based probiotic innovations are expanding market reach by addressing previously inaccessible consumer segments. These products address multiple consumer needs simultaneously, including lactose intolerance accommodation, environmental sustainability concerns, and protein diversification requirements. Additionally, the growing consumer awareness of gut health benefits, coupled with the rising adoption of plant-based diets and product launches such as Danone Canada's Silk, which in February 2024 launched a plant-based yogurt, has created a favorable environment for the expansion of plant-based probiotic products across the region. Plant-based probiotic products are able to sustain premium pricing by targeting higher-income consumers who prioritize perceived health value over price. IFIC data indicate that in households earning over USD 100,000 annually, healthfulness is a stronger purchase driver than cost, supporting margin expansion and premium portfolio strategies.

E-commerce growth improves probiotic accessibility

Online channels are transforming access to high-quality and premium probiotic products by enabling direct-to-consumer engagement, bypassing traditional retail markups, and delivering educational content that highlights product benefits. E-commerce growth has expanded consumer reach and made specialty formulations more widely available[2]Source: U.S. Census Bureau, "Monthly Retail Trade Report: E-commerce Retail Sales," census.gov. These platforms support personalized nutrition, including microbiome testing and custom probiotic blends, allowing smaller, premium-focused brands to compete effectively despite limited physical retail presence. Advanced analytics and AI tools further enhance the premium offering by enabling companies to track consumer preferences and purchasing patterns, optimize product development, and tailor marketing messaging to high-value segments. By removing distribution barriers and providing a direct line to discerning, health-conscious consumers, online channels facilitate broader adoption of premium probiotic solutions, while also fostering brand differentiation in an increasingly competitive market.

Increasing interest in functional foods and fermented products is boosting overall probiotic consumption

In North America, the growing adoption of functional foods and fermented products is a key driver of probiotic market expansion. Consumers are increasingly integrating probiotics into everyday diets via yogurt, kefir, kombucha, plant-based alternatives, and fortified snacks, moving the category beyond traditional supplements. This mainstreaming expands the consumer base, particularly among urban, health-conscious, and digitally engaged demographics who seek convenience, personalization, and wellness outcomes. Plant-based and allergen-friendly formulations are enabling probiotics to be incorporated into a wider range of fortified foods, attracting vegans, lactose-intolerant, and allergy-sensitive consumers and increasing overall market penetration. The combination of increased awareness, diverse product formats, and convenient access is translating into higher consumption frequency, repeat purchases, and overall market growth, positioning North America as a leading region for probiotic innovation and category expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for natural and fresh foods as substitutes | -0.6% | United States, Canada; less pronounced in Mexico | Medium term (2-4 years) |

| Lack of standardized labeling affects transparency and trust | -0.5% | United States and Canada regulatory jurisdictions | Long term (≥ 4 years) |

| Storage and formulation challenges reduce viability of probiotic strains | - 0.4% | National, particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Strict regulatory approvals delay product launches in several regions | - 0.3% | United States and Canada, varying by product category | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Natural and Fresh Foods as Substitutes

The North American probiotics market faces a strategic tension: while 36% of consumers actively seek digestive health benefits, 79% are concerned about food processing, and 63% sometimes avoid processed foods as per International Food Information Council Food & Health Survey, 2024. This challenge is particularly pronounced in the dietary supplements segment, where capsules and tablets carry a pharmaceutical perception that conflicts with the “food-as-medicine” ethos. Consumers increasingly prefer minimally processed, whole-food sources such as kefir, sauerkraut, and kimchi, while USDA guidance restricts “natural” claims to products without synthetic additives, forcing brands to choose between clinical (CFU and strain-specific) and natural positioning. Shelf-stable formats face perception and processing challenges, whereas fresh refrigerated products benefit from a health halo but are limited by distribution and spoilage risk.

Lack of Standardized Labeling Affects Transparency and Trust

Regulatory fragmentation in North America creates significant challenges for the probiotics market. Labeling and quality requirements vary widely across jurisdictions: Health Canada mandates a minimum of 10⁹ CFU at expiry and limits eligible strains to an approved list, the FDA allows structure/function claims without disclosing CFU or strain details, and Mexico’s NOM-051 focuses on sugar and sodium rather than probiotic potency (Health Canada, FDA, COFEPRIS). This patchwork generates inconsistent product standards, complicates cross-border trade, and allows some brands to overstate potency by 50–70% or omit strain-level disclosure, despite efficacy being strain-specific. This regulatory complexity raises compliance costs for manufacturers, hinders portfolio standardization across North America, and creates barriers to scaling high-quality, transparent probiotic offerings. Brands that can navigate this landscape through clear labeling, validated potency, and credible strain disclosure gain a competitive advantage in building consumer trust and differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foods Maintain Dominance While Drinks Accelerate

The North American probiotics market is led by probiotic foods, which accounted for 61.08% of market share in 2025, driven by the widespread presence of yogurt in refrigerated dairy aisles and the clinical validation of infant formulas for C-section and preterm infants. Yogurt remains the category workhorse, with advanced culture technologies enabling manufacturers to reduce dairy solids while delivering premium texture and digestive-health benefits through clinically studied strains. Infant formula is experiencing a post-pandemic resurgence, with formulations targeting microbiome diversity in C-section deliveries capturing a significant share of the premium segment. Beyond formula, baby food is also expanding as parents increasingly prioritize early gut-health interventions, although regulatory caution around infant dosing continues to constrain innovation. Probiotic drinks are the fastest-growing segment, with a projected CAGR of 9.54% through 2031, driven by demand for convenient, on-the-go formats and innovation in dairy-free options such as kombucha and fermented teas.

In parallel, dairy-based formats, including kefir and drinkable yogurts, are expanding beyond digestive health through protein fortification, enabling positioning around satiety, recovery, and daily performance and increasing consumption occasions. The dietary supplements segment, including capsules, tablets, powders, and gummies, exhibits bifurcated demand. Gummies are experiencing rapid growth, driven by convenience and consumer-friendly taste, while capsules maintain clinical credibility for precise therapeutic dosing. Premium multi-strain formulations can command high price points, reflecting consumer willingness to pay for perceived efficacy, quality, and trusted strains, positioning this segment as a high-margin opportunity within the broader probiotics market.

By Distribution Channel: Digital Transformation Reshapes Access

Supermarkets and hypermarkets accounted for 46.16% of distribution share in 2025, supported by impulse purchasing, promotional visibility, and strong consumer trust in refrigerated dairy sections as indicators of quality. These formats offer a broad assortment and temperature-controlled environments critical to probiotic stability. Pharmacies and health stores compete through health-focused positioning and staff expertise, leveraging professional recommendations to drive trial and premium purchases. Convenience stores, while benefiting from high foot traffic and daily purchase behavior, remain underpenetrated due to cold-chain constraints and lower health intent; however, shelf-stable formats such as gummies and stick packs present a viable entry point.

Online retail is the fastest-expanding channel, growing at a 9.21% CAGR, driven by direct-to-consumer subscriptions that bypass retailer margin stacking and increase lifetime customer value. In response, leading companies are adopting integrated omnichannel strategies, combining physical retail, e-commerce, and expanded cold-chain logistics to maximize reach while preserving product quality and freshness across channels. Other channels, including direct selling and practitioner dispensing, serve niche, premium segments seeking personalized guidance.

Geography Analysis

The United States accounted for 79.50% of the North American probiotics market in 2025, supported by a mature retail ecosystem, advanced cold-chain infrastructure, and long-standing consumer familiarity with probiotic claims. Market adoption has been reinforced by decades of mainstream exposure to digestive health messaging, while the FDA’s permissive structure/function claim framework enables brands to communicate digestive and immune benefits without premarket approval, accelerating SKU launches and innovation cycles.

Mexico represents the fastest-growing market in the region, with a projected CAGR of 9.03% through 2031. Growth is driven by a rising middle class, increasing urbanization, and highly effective alternative distribution models, including direct-to-home delivery networks. Expanding health and wellness retail formats and rising local manufacturing capacity are further supporting demand growth and improving market access. Canada’s probiotics market is shaped by stringent regulatory oversight, with Health Canada’s labeling and potency requirements reinforcing premium positioning and consumer trust. The market shows strong momentum in personalized and condition-specific probiotic formulations, creating opportunities for higher-value, differentiated products.

The rest of North American markets, including parts of the Caribbean and Central America, remain nascent but exhibit emerging potential driven by tourism exposure, improving distribution infrastructure, and growing awareness of digestive health. While regulatory frameworks in these markets are less developed, increasing consumer education and retail expansion are gradually supporting market entry and long-term growth opportunities.

Regulatory Landscape

In the United States, probiotics sold as dietary supplements generally operate under the DSHEA framework, where structure/function claims are used without premarket approval, but labeling and ingredient eligibility remain active topics for the category. On March 27, 2026, the US Food and Drug Administration (FDA) held a public meeting (Docket FDA-2026-N-2047) to discuss the scope of dietary supplement ingredients and how concepts such as "dietary substance" apply to innovations including probiotics, signaling ongoing scrutiny that can influence evidence standards, claims strategy, and pathways for novel strains.

Canada applies a more prescriptive route, regulating probiotics as Natural Health Products (NHPs) under the Natural Health Products Regulations (SOR/2003-196), which require product authorization and site licensing through Health Canada. New NHP labeling requirements came into force on June 21, 2025 (with a transition period for existing products until June 22, 2028), and Health Canada updated its Natural Health Product Probiotics Monograph on April 24, 2026, tightening expectations around stability, viability, and microbial purity testing. Across North America, this regulatory patchwork (FDA vs Health Canada, alongside Mexico oversight via COFEPRIS) keeps cross-border portfolio standardization and label harmonization as an operational constraint for multi-country brands.

Competitive Landscape

The North American probiotics market exhibits moderate consolidation, with major players like Nestlé S.A., Danone, BioGaia AB, Amway Corporation, and PepsiCo Inc. dominating the landscape. These established companies leverage their manufacturing capabilities and extensive distribution networks, while specialized probiotic manufacturers compete through innovation and premium product positioning. The market structure enables large companies to maintain significant market share through economies of scale and established brand recognition, while smaller players carve out niches through specialized offerings and targeted marketing strategies.

The market exhibits a dual competitive structure where volume-focused incumbents expand through retail partnerships, while innovation-driven entrants target specialized segments. Companies are launching innovative products, such as ZBiotics' development of a probiotic drink mix in September 2024 that converts sugar into fiber through genetic engineering, aiming to enhance digestion, nutrient absorption, and gut health. Upstream consolidation has further reshaped the competitive landscape. The merger of major probiotic ingredient suppliers has concentrated control over proprietary, clinically validated strains, increasing sourcing risk and input costs for smaller formulators while strengthening the position of multinationals with long-term supply agreements.

White-space opportunities are clustering around postbiotics that bypass cold-chain constraints, personalized formulations enabled by microbiome testing, and functional hybrids combining probiotics with collagen, adaptogens, or metabolic-support ingredients. Technology adoption is now a core competitive lever: advanced encapsulation and shelf-stabilization technologies are table stakes, while leaders are deploying AI to accelerate product development and digital platforms to maintain premium pricing.

North America Probiotics Industry Leaders

-

PepsiCo Inc.

-

BioGaia AB

-

Amway Corporation

-

Danone

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory definition and labeling clarity for live microbial supplements is an immediate whitespace area for companies that can document strain identity, viability through end of shelf life, and claim substantiation across borders. The FDA discussion on March 27, 2026 around the scope of dietary supplement ingredients (DSHEA) has pushed trade bodies and industry stakeholders to advocate for frameworks that accommodate novel strains and modern production methods, creating an opening for suppliers and finished-product brands that invest in traceability, validated CFU/viability labeling practices, and compliant, condition-specific positioning.

Manufacturing specialization and capacity additions are also creating concrete pathways to scale supplements and functional formats while managing strain integrity. In February 2026, Vitaquest opened a new probiotics manufacturing suite at its Parsippany, New Jersey site and cited a 100% increase in probiotic manufacturing capacity, while Vidya opened a 28,750-square-foot probiotic manufacturing facility in Bunnell, Florida in April 2026 with physically separated production lines for spore-forming and non-spore-forming strains. In parallel, Lifeway Foods has continued a multi-phase, USD 45 million expansion of its Waukesha, Wisconsin facility aimed at higher kefir output, reinforcing opportunity around cold-chain capable dairy and drinkable formats; these investments support broader SKU variety (including plant-based and shelf-stable adjacencies) and enable faster iteration in delivery forms such as gummies, drink mixes, and functional beverages distributed through online and mainstream retail.

Recent Industry Developments

- February 2026: PepsiCo launched Pepsi Prebiotic Cola nationwide in the United States across retail and online channels, offering Original Cola and Cherry Vanilla flavors with 3 grams of prebiotic fiber per serving. The move brings digestive-health adjacency into a legacy carbonated soft drink platform, using large-scale distribution to normalize functional positioning in mainstream beverage aisles.

- December 2025: BioGaia launched BioGaia Gastrus PURE ACTION, a condition-specific probiotic positioned for consumers with heightened digestive sensitivities. The product reinforces the category shift toward clinically validated, trust-led differentiation as brands compete on strain credibility and quality signaling rather than broad, generic digestive claims.

- November 2024: General Mills entered the shelf-stable probiotic snack segment with the launch of YoBark, a yogurt-coated granola bar formulated with probiotic cultures and supported by microencapsulation for viability through processing and shelf life. This expanded competitive intensity beyond refrigerated dairy into ambient snacking, widening consumption occasions for probiotic-enabled products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this market, we size the value of finished probiotic products sold across North America, where live microbial strains are present and marketed for health benefits in foods, beverages, and dietary supplements.

Scope exclusions: Bulk probiotic ingredients, animal feed probiotics, and internal transfer or captive use inside vertically integrated producers are excluded.

Segmentation Overview

-

By Product Type

-

Probiotic Foods

- Yogurt

- Bakery/Breakfast Cereals

- Baby Food and Infant Formula

- Other Probiotic Foods

-

Probiotic Drinks

- Dairy-based Drinks

- Fruit/Plant-based Drinks

- Others

-

Dietary Supplements

- Capsules

- Tablets

- Powders

- Gummies

- Others

-

Probiotic Foods

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Health Stores

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand picture and to keep assumptions realistic before we spoke to the market. We referenced public sources such as FDA and Health Canada updates, USDA food consumption signals, USITC trade statistics for relevant product categories, and Statistics Canada consumer and price series, along with peer reviewed nutrition and microbiome journals for usage patterns and strain related constraints.

On top of that, annual reports, investor presentations, retailer and distributor announcements, and reputable press were reviewed to understand product launches, pricing direction, and channel mix shifts. Where needed, a paid subscription for company financials and a patent database were used to cross-check revenue exposure and innovation activity tied to probiotic formats and strains. These sources are illustrative only, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, brand teams, ingredient specialists, distributors, and category managers who track probiotic foods, drinks, and supplements across the United States, Canada, Mexico, and the rest of North America. We used these discussions to confirm what is counted as a probiotic product at shelf, how pricing moves by format, and how demand changes with new claims, regulations, and consumer health priorities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | |

| Mid tier: 50% | Functional/Unit leaders: 42% | |

| Smaller Players: 17% | Managers: 43% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of the addressable spend, where country level consumption and category sales signals are mapped into probiotic foods, probiotic drinks, and dietary supplements, and then filtered using penetration and price checks discussed in expert calls. To keep the totals grounded, selective bottom-up approximations were also used, like sampling brand level pricing, checking channel mix, and rolling up a limited set of supplier and distributor indicators to see if the market total sits in a plausible range.

Inputs that shaped the model include probiotic product launch intensity, average selling price ranges by format (food, beverage, supplement), share movement across retail versus online channels, claim and labeling enforcement trends, and relative consumer health interest tied to digestive and immunity positioning. Forecasting was built using scenario analysis, where the main case is adjusted by expected pricing progression and adoption rates, and then stress-tested for faster or slower shifts in channel mix and supplement uptake. When bottom-up data was missing for smaller brands, gaps were handled using category averages and calibrated shares so the model still stays repeatable and auditable.

Data Validation & Update Cycle

Before finalizing, we triangulate the modeled totals against independent signals such as reported category growth, trade flows for relevant finished product groups, and observed price bands in major channels. Large variances are flagged, reviewed, and taken back into follow-up discussions when a key assumption seems off, which helps prevent single-source bias from shaping the outcome.

Each report goes through multiple analyst review steps, including logic checks at country level and a final pass for outliers in growth rates, pricing, and mix shifts. The report is refreshed annually, and interim updates are made when a material event changes demand, regulation, or pricing, followed by a final pre-delivery check so clients receive the latest view.

Mordor Intelligence's North America Probiotics Market Market Size Measured Against Other Published Estimates

Published market sizes for North America probiotics can look far apart because the word probiotics is applied differently across foods, drinks, supplements, and sometimes even adjacent animal or ingredient categories. Differences also come from how firms treat retail versus food-service value, and whether the estimate is anchored to consumption indicators or to broad revenue pools.

The largest gap drivers we see are scope choices and pricing logic. Some estimates fold in animal feed probiotics or bulk ingredient sales, while others use aggressive price growth assumptions without matching them to real shelf price bands or channel mix. In our sizing, only finished probiotic foods, beverages, and dietary supplements sold in the region are counted, with cross-checks against country level demand signals and retail pricing cadence, which is a key reason the base value lands lower in this study, and that scope choice is applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.31 B (2025) | |

| Global Consultancy A | USD 10.80 B (2025) | This figure appears to include animal feed probiotics and a wider definition of functional products, which expands the revenue pool beyond finished human foods, drinks, and supplements. |

| Industry Databook B | USD 30.77 B (2025) | This estimate uses a broad product scope that combines food and beverages, dietary supplements, and animal probiotics, which materially increases the total versus a finished human product-only view. |

Looking across the table, the spread is mainly explained by what gets included, not by small math differences. When scope is kept tight to finished human probiotic products and the pricing and channel mix assumptions are checked with real market inputs, the market total becomes easier to trace and to repeat year after year.

Key Questions Answered in the Report

What is the current value of the North American probiotic products market?

The market stands at USD 7.84 billion in 2026 and is projected to reach USD 11.10 billion by 2031.

Which product segment leads sales in the probiotic products market?

Probiotic foods dominate with a 61.08% share of 2025 revenue, anchored by yogurt and cultured-dairy lines.

Why are probiotic drinks growing faster than other formats?

Their 9.54% forecast CAGR reflects demand for portable, low-sugar beverages and innovation in dairy-free recipes that maintain live-culture viability.

Which North American country shows the highest growth potential for probiotics?

Mexico leads with a 9.03% CAGR to 2031 due to rising middle-class income, health-focused retail expansions, and mobile-commerce adoption.

Who are the key players in North America Probiotic Products Market?

Nestlé S.A., Danone, PepsiCo Inc., BioGaia AB, and Amway Corporation are the major companies operating in the North America Probiotics Market.

Page last updated on: