Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 25.67 Billion |

| Market Size (2026) | USD 27.03 Billion |

| Market Size (2031) | USD 35.07 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

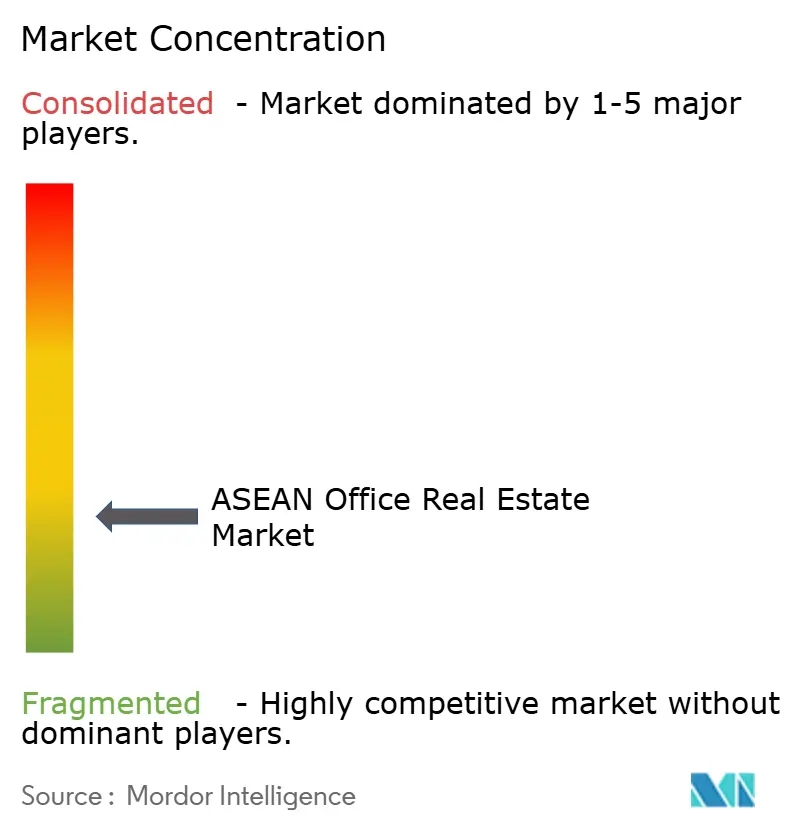

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Office Real Estate Market Analysis by Mordor Intelligence

The ASEAN office real estate market size was valued at USD 25.67 billion in 2025 and estimated to grow from USD 27.03 billion in 2026 to reach USD 35.07 billion by 2031, at a CAGR of 5.32% during the forecast period (2026-2031). Demand momentum is sustained by record foreign direct investment of USD 230 billion in 2023, which has tilted regional corporate footprints toward Southeast Asian capitals. Flight-to-quality preferences keep Grade A offices at the center of leasing strategies, while hybrid work policies push decision-makers to prioritize flexible layouts, digital infrastructure, and green certifications. Multinational tenants in banking, insurance, technology, and professional services continue to consolidate into a smaller number of premium addresses, reinforcing rent resilience in core districts. At the same time, limited prime supply pipelines in Singapore, Bangkok, and Jakarta restrain vacancy growth and support the ASEAN office real estate market’s medium-term pricing power. Government incentives that accelerate digital transformation and sustainability investment complement these trends by widening the tenant base and raising building specifications[1]Satvinder Singh, “ASEAN Investment Report 2024,” ASEAN Secretariat, asean.org.

Key Report Takeaways

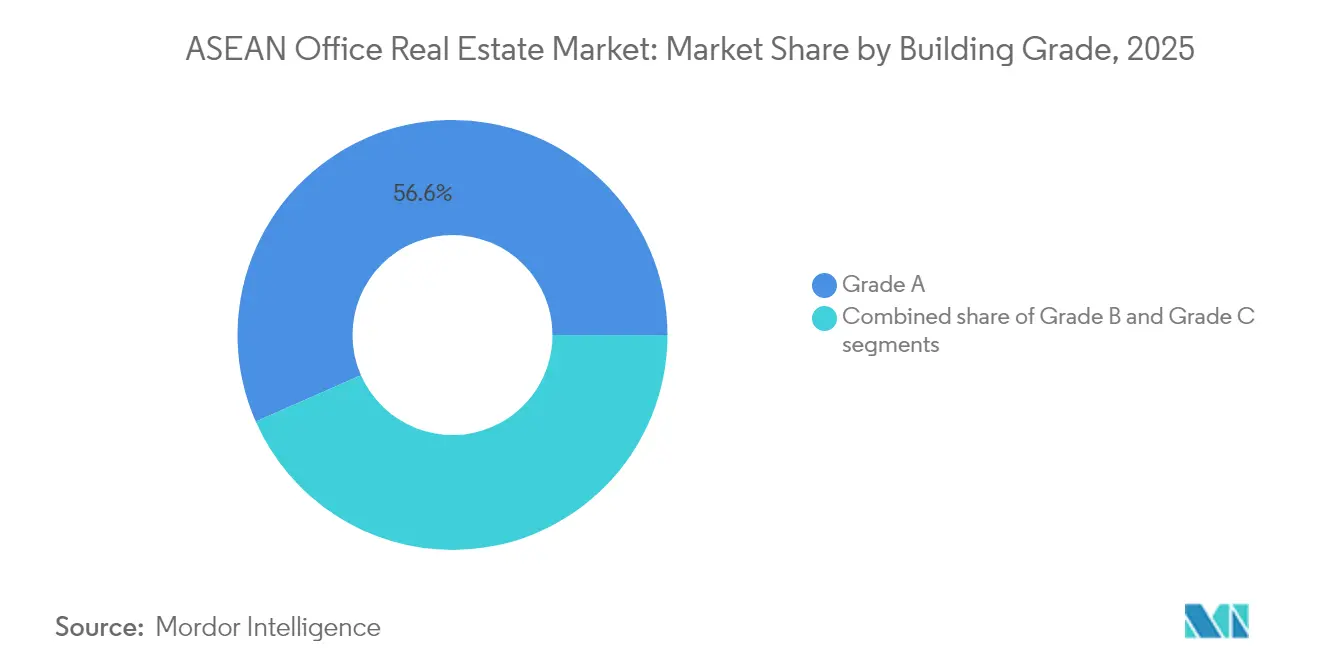

- By building grade, Grade A space led with 56.60% revenue share in 2025; it is projected to advance at a 6.05% CAGR through 2031.

- By transaction type, rentals commanded 69.70% of ASEAN office real estate market share in 2025, while sales are set to log the fastest 6.20% CAGR to 2031.

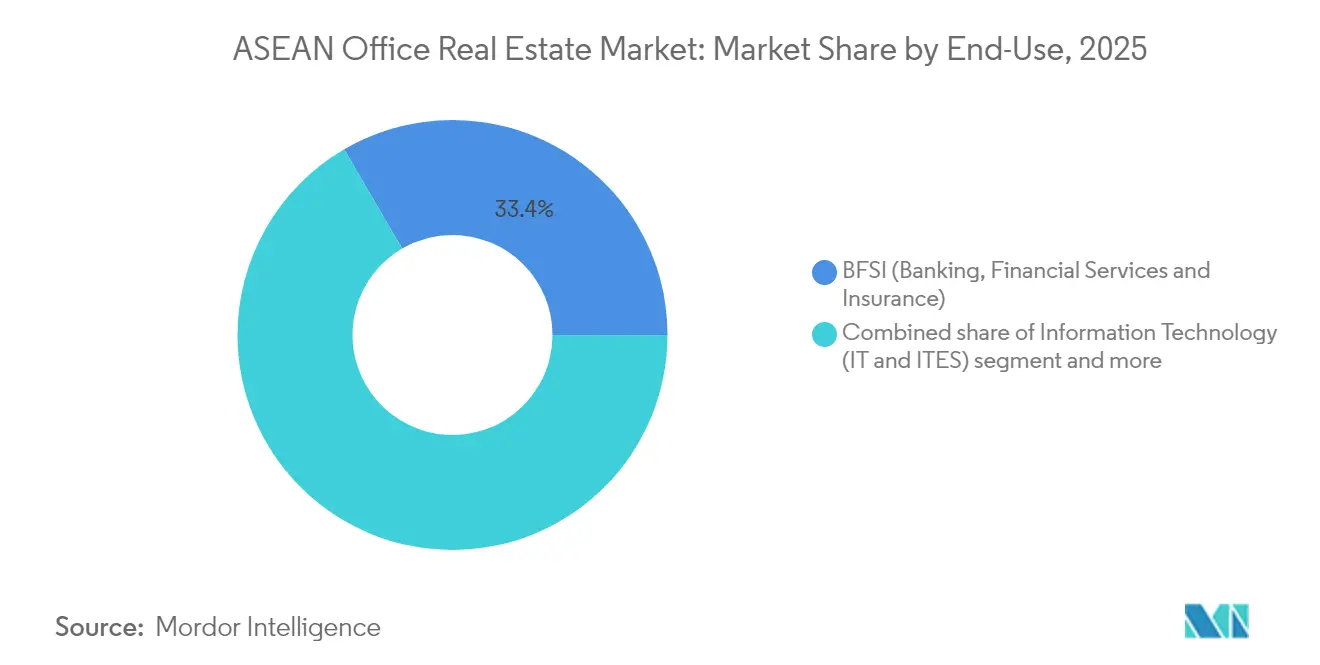

- By end use, BFSI occupiers held 33.40% of the 2025 ASEAN office real estate market size, whereas IT & ITeS segment revenues are forecast to rise at a 6.40% CAGR to 2031.

- By geography, Indonesia accounted for 47.40% of 2025 revenue, and Vietnam is expected to expand at a 6.72% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained foreign investment in Vietnam, Indonesia, and the Philippines driving office demand | +1.5% | Vietnam, Indonesia, Philippines | Long term (≥ 4 years) |

| Gradual economic recovery across Southeast Asia improving corporate leasing sentiment | +1.2% | Indonesia, Thailand, Malaysia, Philippines | Medium term (2-4 years) |

| Limited new prime office supply in city cores supporting rental stability | +0.9% | Singapore, Bangkok CBD, Jakarta CBD | Medium term (2-4 years) |

| Hybrid work adoption increasing demand for flexible, well-located Grade A office spaces | +0.8% | Singapore, Malaysia, Thailand, urban centers | Short term (≤ 2 years) |

| Sustainability and green leasing priorities influencing tenant preferences | +0.6% | Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Technology upgrades in commercial buildings enhancing operational efficiency | +0.4% | Global ASEAN markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained Foreign Investment in Vietnam, Indonesia and the Philippines Driving Office Demand

Vietnam captured 48.6% year-on-year FDI growth in January 2025, with processing and manufacturing projects taking 66.9% of inflows whitecase.com. Each new plant requires procurement, logistics and legal functions that gravitate to downtown Ho Chi Minh City towers, where Grade A vacancy dipped to 19.4% in 2024 cbrevietnam.com. Jakarta remains the natural hub for regional headquarters targeting ASEAN’s largest domestic market, while Metro Manila benefits from continued BPO contract wins. Foreign corporates attract a halo of auditors, consultants and IT vendors, reinforcing net absorption in the ASEAN office real estate market[2]Nguyen Chi Dung, “Foreign Investment Statistics January 2025,” Ministry of Planning and Investment (Vietnam), mpi.gov.vn.

Gradual Economic Recovery Across Southeast Asia Improving Corporate Leasing Sentiment

Southeast Asia’s GDP is projected to grow 4.5% in 2025, underpinned by consumer spending and public infrastructure programs. Lease tenures are lengthening as firms abandon the stop-gap strategies adopted during the pandemic and commit to larger footprints in Manila, Jakarta, and Kuala Lumpur. Tourism-led services rebound is adding professional services employment that depends on well-equipped offices. Banks and insurers are enlarging client-facing space to capture cross-border trade flows accelerated by supply-chain realignment. Stronger cash flows let companies secure premium floors early, fostering a ripple effect of occupancy gains across upper-tier buildings in the ASEAN office real estate market.

Limited New Prime Office Supply in City Cores Supporting Rental Stability

Developers, squeezed by higher borrowing costs, are rolling out fewer speculative CBD projects. Singapore’s pipeline below 2027 stands at less than 2 million sq ft, fueling landlord pricing confidence even after 12 successive quarters of rent growth. Bangkok and Jakarta witness similar constraints as zoning and land scarcity limit large-scale additions. The scarcity of fresh Grade A stock sustains occupancy above 90% in top-tier towers, buffers cash yields for REITs and positions the ASEAN office real estate market for steady landlord-favored negotiations through mid-decade.

Hybrid Work Adoption Increasing Demand for Flexible, Well-Located Grade A Office Spaces

Forty-three percent of Asia-Pacific employers hit peak utilization rates above 80% despite smaller average daily attendance, proving that when staff come in, they value superior locations and collaboration zones. Hybrid policies, hence, reward towers with campus-style amenities, touch-free access, smart ventilation, and wellness facilities. Rents in such properties trade at USD 8.8 per sq ft per month in Singapore’s CBD, a 12% premium over non-certified peers. The bifurcation pushes older inventory toward obsolescence, while the ASEAN office real estate market channels both capital expenditure and tenancy into trophy assets clustered around mass-transit nodes.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest rate pressures and funding constraints slowing new office project launches | -0.9% | Regional, particularly affecting development financing | Medium term (2-4 years) |

| High vacancy rates persist in older buildings due to occupier flight to quality | -0.7% | Singapore business parks, Jakarta non-CBD, older Bangkok developments | Short term (≤ 2 years) |

| Global economic uncertainty causing multinational firms to delay long-term leasing decisions | -0.5% | Singapore, Malaysia, Thailand (MNC-dependent markets) | Short term (≤ 2 years) |

| Regulatory inconsistency across ASEAN markets complicating regional expansion | -0.3% | Cross-border operations, particularly Vietnam, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interest Rate Pressures and Funding Constraints Slowing New Office Project Launches

Asia-Pacific real estate investment volumes shrank 27% in 2024 as financing costs jumped and lenders tightened underwriting standards. Developers now require higher pre-commit levels or joint-venture equity for greenfield projects, pushing delivery timelines beyond 2028. While constrained pipelines support rent stability, they also cap market expansion potential in second-tier cities. The capital crunch, therefore, moderates the ASEAN office real estate market’s attainable CAGR during the forecast window.

High Vacancy Rates Persist in Older Buildings Due to Occupier Flight to Quality

Vacancy at Singapore’s Changi Business Park approached 40% in 2024 after large occupiers shed surplus space, underlining the widening gap between premium and secondary stock. Similar patterns in Jakarta and Bangkok reveal that buildings without sustainability credentials or modern cooling systems struggle to attract tenants. Owners face steep retrofit costs that erode returns, prompting sales or conversion to alternative uses. Near-term oversupply in legacy towers keeps headline vacancy elevated, tempering headline growth in the broader ASEAN office real estate market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Capture Value

Grade A assets contributed 56.60% of 2025 revenue, reaffirming their status as the backbone of the ASEAN office real estate market. These towers cluster in CBD corridors with mass-transit access and advanced digital infrastructure that meet global tenant criteria. Higher air-quality systems, column-free floorplates, and extensive ESG disclosures keep occupancy near 90%. Investors gravitate toward this tier to secure stable cash flows and hedge regulatory risk. Upgrades such as on-site renewable generation and smart-glass facades further embed Grade A properties into corporate sustainability roadmaps, underpinning a 6.05% CAGR outlook that outpaces the overall industry.

Grade B supply sits under competitive stress as tenants migrate upward. Landlords are compelled to unlock capital for retrofits or accept lower rents, shrinking yield differentials with Grade A. Some Grade C buildings exit the leasing pool altogether through conversion into co-living, education or data-center use-cases. In markets like Singapore and Kuala Lumpur, government incentives for deep-retrofit programs offer a lifeline, yet only the most centrally located structures can justify the required capex. Consequently, revenue concentration in prime assets is expected to intensify, reinforcing a core-plus investment narrative within the ASEAN office real estate market.

By Transaction Type: Rental Flexibility Dominates

Rentals accounted for 69.70% of the ASEAN office real estate market size in 2025 as corporates demanded agility amid evolving hybrid policies. Shorter lease tenures and expansion-contraction clauses give CFOs the headroom to recalibrate footprints quickly without heavy upfront capital. Flexible-space providers partner with landlords to curate turnkey suites, boosting service revenues and amenity depth. This model supports high building utilization on collaboration days and maintains predictable cashflows for owners.

Sales transactions, although forming a smaller base, are projected to log the highest 6.20% CAGR as owner-occupiers and core funds pivot to long-run value capture. Supply-constrained CBDs encourage blue-chip tenants to lock in future premises, while inflation-hedging motives spur pension funds toward direct buys. The rental-to-ownership mix hence diversifies, but flexibility will still define most new leases signed across the ASEAN office real estate market through 2031.

By End Use: Financial Services Lead, Technology Accelerates

BFSI (Banking, Financial Services and Insurance) organizations held 33.40% ASEAN office real estate market share in 2025, anchored by Singapore’s global finance hub positioning and Malaysia’s Islamic finance depth. Banks prioritize power-redundant buildings with robust cybersecurity infrastructure to run trading floors and digital banking labs. Regional regulators demand strict data-residency compliance, steering lenders to grade-A towers equipped with dedicated server rooms and secure fiber links. These specifications keep BFSI demand sticky in prime quarters even as branch footprints shrink elsewhere.

Information Technology and IT-enabled Services will expand at a market-leading 6.40% CAGR, buoyed by USD 60 billion of data-center capital set to flow into Southeast Asia by decade-end. Global hyperscalers, platform firms, and AI developers require adjacent office clusters to host engineering, sales, and policy teams. Governments nurture the ecosystem through skills programs such as Microsoft’s plan to train 2.5 million citizens in AI by 2025, translating into a steady pipeline of tech-sector occupiers throughout the ASEAN office real estate market.

Geography Analysis

Indonesia retains leadership with 47.40% 2025 revenue, underpinned by its USD 1.4 trillion economy and policy continuity that anchors manufacturing expansion. Government transport megaprojects are knitting Greater Jakarta into a unified labor catchment, boosting demand for well-connected Grade A floors. CBD occupancy hovered near 70% through 2024 while net absorption improved as oil-and-gas, telecom, and e-commerce groups recommitted to in-office collaboration. The city’s tightening green-building code is expected to nudge owners toward retrofits, further consolidating value in the upper tier of the ASEAN office real estate market.

Vietnam, forecast to grow at 6.72% CAGR, benefits from rapid FDI acceleration that feeds office uptake far beyond headline manufacturing projects. Ho Chi Minh City’s vacancy compression to 19.4% illustrates how support functions for export plants turn quickly into inner-city space requirements. Favorable credit-growth ceilings and a young digital workforce intensify corporate interest, prompting developers to fast-track premium towers in Thu Thiem and District 7. Hanoi experiences a similar pivot as multinational R&D centers emerge around Diplomatic District clusters, signaling durable depth across the ASEAN office real estate market.

Singapore, Thailand, Malaysia and the Philippines collectively offer mature yet distinct stories. Singapore’s supply-tight CBD keeps rents at USD 8.8 per sq ft per month even as hybrid adoption stabilizes. Malaysia positions Kuala Lumpur and the Johor-Singapore Special Economic Zone for cross-border synergies that could add USD 26 billion output annually. Thailand courts automotive and chipmakers through reduced corporate taxes in Eastern Economic Corridor zones, while the Philippines leverages English-speaking talent to deepen BPO clusters in Metro Manila and Cebu. Together these geographies provide the stability and scale that global investors seek when allocating to the ASEAN office real estate market.

Competitive Landscape

The ASEAN Office Real Estate Market is moderately fragmented, with diversified conglomerates, listed REITs, and local champions each carving niches. CapitaLand Group, UOL Group, and City Developments draw on integrated development, asset management, and hospitality arms to recycle capital quickly and capture end-to-end value streams. Mid-tier developers specialize in single-city portfolios or mixed-use precincts, often partnering with pension funds that require operating expertise. Flexible-space operators such as IWG and WeWork collaborate with landlords to activate under-utilized floors, adding subscription revenue and enhancing building stickiness within the ASEAN office real estate market.

Strategic moves center on portfolio pruning and upgrade. CapitaLand Ascendas REIT deployed USD 543.6 million in May 2025 to acquire two prime assets, signaling confidence in core CBD rent trajectories. Developers offload non-performing assets to recycle proceeds into ESG-compliant towers, while institutional investors increase direct stakes to hedge inflation. Cross-border diversification is also visible; Mapletree Investments opened an Abu Dhabi office in 2024 to source Middle-East capital and co-investment deals, balancing exposure across economic cycles. As capital requirements scale, smaller players either form joint ventures or exit, intensifying consolidation.

Technology and sustainability are the next battlegrounds. Leading landlords roll out digital twins, tenant apps, and energy analytics across portfolios, reducing operating costs and elevating user experience. Portfolio-wide net-zero roadmaps enhance access to green loans and sustainability-linked bonds, cutting weighted average cost of capital by up to 30 basis points. Competitive differentiation will therefore hinge less on sheer floorplate supply and more on integrated service, data transparency, and carbon footprint in the ASEAN office real estate market.

ASEAN Office Real Estate Industry Leaders

CapitaLand

UOL Group Limited

City Developments Limited

Frasers Property Limited

Keppel Management Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CapitaLand Ascendas REIT acquired two prime buildings for USD 543.6 million, reinforcing its focus on core CBD assets.

- May 2025: Google’s Malaysian affiliate awarded a USD 237 million data-center contract to Gamuda Bhd and purchased land worth USD 108 million for the same project.

- March 2025: Arm Holdings Plc established a Malaysian base after discussions with government leaders, enlarging Southeast Asia’s semiconductor ecosystem.

- January 2025: Malaysia and Singapore signed the Johor-Singapore Special Economic Zone MoU, targeting 100,000 jobs and a USD 26 billion annual GDP lift.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the ASEAN office real estate market as the annual monetary value of income-producing, purpose-built office buildings, both newly completed and standing stock, traded, leased, or owner-occupied across Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam.

Scope exclusion: coworking franchises that operate under revenue-share agreements inside retail assets are not counted.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal)

- By Country

- Indonesia

- Vietnam

- Thailand

- Philippines

- Malaysia

- Singapore

- Rest of ASEAN

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regional developers, REIT managers, brokerage heads, and facilities directors in Jakarta, Singapore, and Ho Chi Minh City. These conversations clarified effective rents, typical capital values, and yield expectations, letting us reconcile desk findings with on-ground sentiment before locking our assumptions.

Desk Research

We began with macro data from sources such as the ASEAN Secretariat national accounts, central-bank policy releases, and ministries of public works, which outline GDP, construction permits, and foreign direct investment trends. Building completions and pipeline figures were pulled from city planning departments and apex realtor associations like REHDA Malaysia and REI Indonesia. Rental and vacancy benchmarks came from open quarterly bulletins issued by CBRE, JLL, and Cushman & Wakefield, while company financials were screened through D&B Hoovers and recent filings. Dow Jones Factiva supplied news on large asset trades. (The sources named illustrate the breadth; many other public records and press releases were also reviewed.)

Market-Sizing & Forecasting

A top-down stock-by-grade model converted city-level gross floor area into capital value using verified average selling prices, vacancy-adjusted rent rolls, and prevailing cap rates. Results were stress-tested through selective bottom-up checks on landmark transactions. Key variables include Grade A net absorption, pipeline completions, cross-border investment flows, prime rent growth, and government infrastructure spend. Five-year forecasts rely on multivariate regression linking rents and yields to GDP, office job creation, and policy rates, with scenario ranges vetted by our interview panel. Data gaps, for example, private treaty deal prices, were bridged via median-yield imputation from comparable assets.

Data Validation & Update Cycle

Outputs pass two analyst peer reviews, anomaly scans versus central-bank lending data, and variance flags against prior editions. Reports update yearly; mid-cycle revisions are triggered if vacancy swings beyond 150 bps or if a single deal skews market value above 5 %.

Why Mordor's ASEAN Office Real Estate Baseline Earns Dependability

Published estimates often diverge because firms mix construction cost, land value, or even wider commercial segments into their totals.

Key gap drivers in rival work stem from broader scope, including mixed-use towers, currency conversion at list-date instead of average-year rates, and infrequent refreshes that miss 2024's rate-driven repricing. Our disciplined definition, annual refresh, and dual-path validation keep our 2025 baseline at USD 25.67 B the most decision-ready figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.67 B (2025) | Mordor Intelligence | - |

| USD 100 B (2024) | Global Consultancy A | Includes owner-occupied HQ land and shell cost; uses 2022 exchange rates |

| USD 250 B (2023) | Industry Insights Firm B | Adds undeveloped land banks and corporate campus valuations; no vacancy discount applied |

These comparisons show how narrower, finance-ready scoping and yearly recalibration enable Mordor Intelligence to deliver a balanced and transparent anchor for strategic planning.

Key Questions Answered in the Report

What is the current size of the ASEAN office real estate market?

The market stands at USD 27.03 billion in 2026 and is forecast to reach USD 35.07 billion by 2031.

Which country holds the largest ASEAN office real estate market share?

Indonesia leads with 47.40% of 2025 revenue thanks to its large domestic economy and Jakarta’s dominant CBD.

Which segment is growing fastest in the ASEAN office real estate market?

IT & ITeS demand is projected to expand at a 6.40% CAGR through 2031 as global tech firms upscale Southeast Asian operations.

How is hybrid work influencing office demand?

Hybrid policies concentrate demand in flexible, well-amenitized Grade A towers, driving rent premiums of around 12% for certified buildings.

What is the outlook for office supply in core ASEAN CBDs?

Limited speculative pipelines in Singapore, Bangkok and Jakarta point to continued landlord pricing power over the next four years.

Why are sustainability features important for office assets?

Green-certified buildings attract higher rents, lower operating costs and enable tenants to meet corporate ESG commitments, enhancing long-term asset value.

Page last updated on: