Meat Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.57 Billion |

| Market Size (2031) | USD 14.65 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

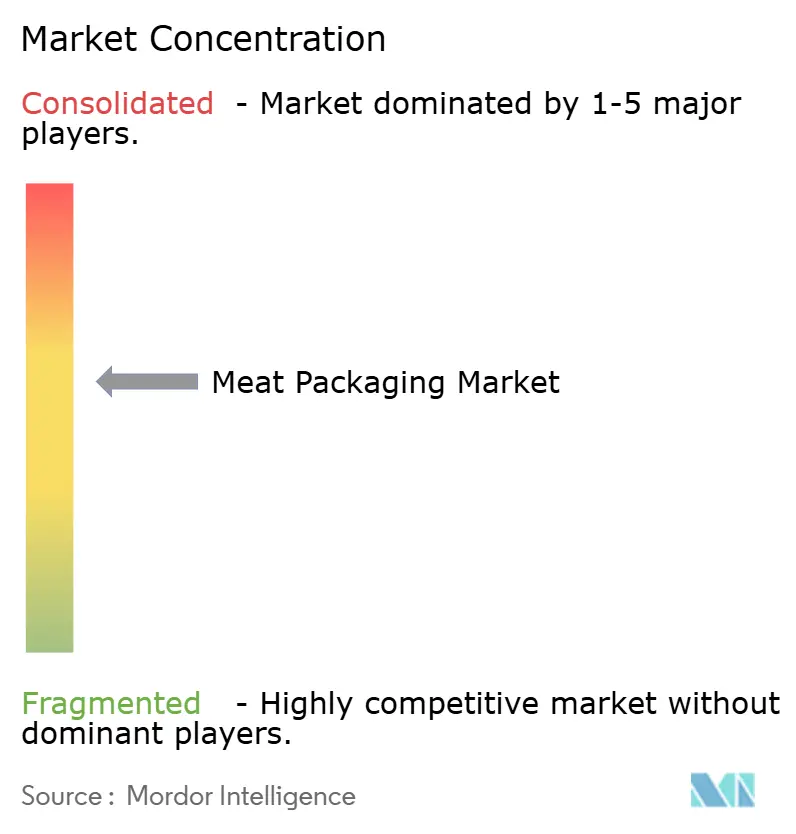

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meat Packaging Market Analysis by Mordor Intelligence

The meat packaging market size is projected to expand from USD 12.19 billion in 2025 and USD 12.57 billion in 2026 to USD 14.65 billion by 2031, registering a 3.11% CAGR between 2026 to 2031. This steady trajectory mirrors the sector’s efforts to extend shelf life, certify origin, and meet rising sustainability thresholds while absorbing volatile polymer costs and extended producer responsibility fees. Flex-format polyethylene pouches are capturing volume from legacy rigid trays because they deliver high oxygen barriers without sacrificing recyclability credit, a feature now written into most European grocery tenders. Retailers in North America are also pushing modified-atmosphere and vacuum-skin formats that carry real-time temperature logs, turning primary packs into data nodes that trim shrink and liability exposure. Meanwhile, cold-chain investments in China, India, and Brazil are unlocking chilled distribution, encouraging processors to trade up from wax-coated paper to multilayer film structures. Converter profitability, however, remains exposed to 30% swings in spot polyethylene prices and the European Union’s incoming levy on non-recycled resin, both of which are accelerating backward integration into resin compounding.

Key Report Takeaways

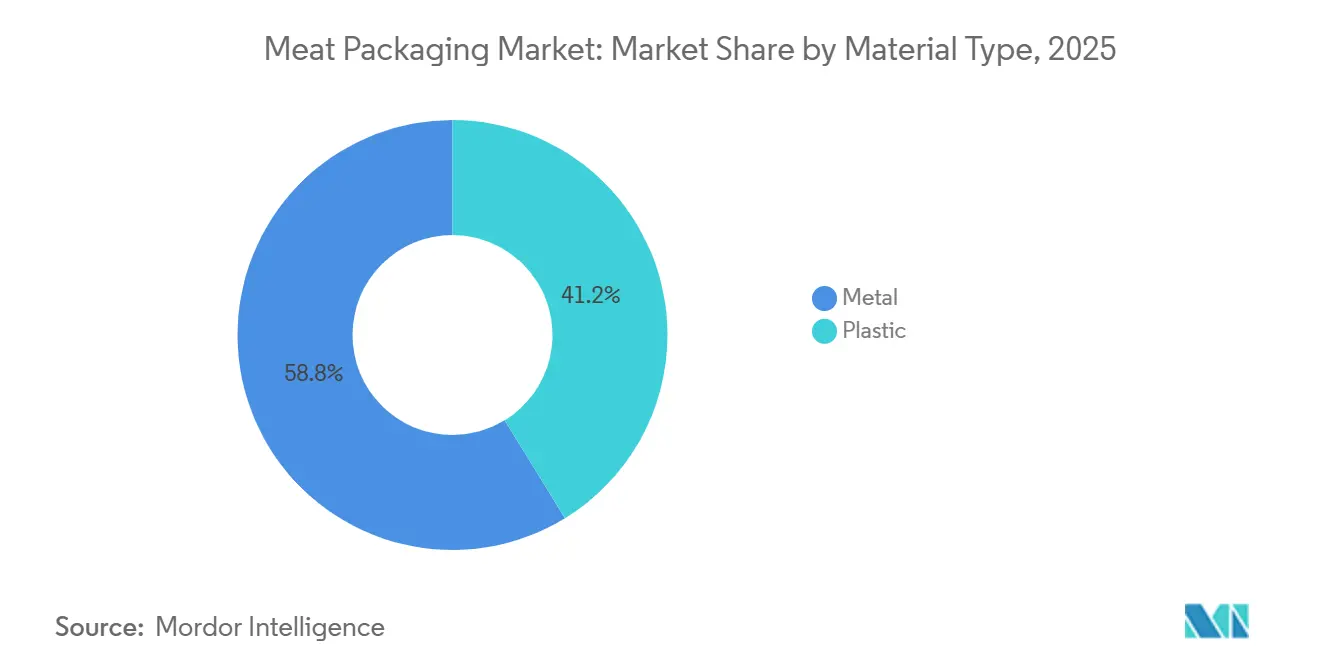

- By material type, plastic formats led with 41.23% revenue share in 2025, while flexible pouches within this cohort are projected to expand at a 3.56% CAGR through 2031.

- By meat type, fresh and frozen cuts accounted for 36.74% of the meat packaging market share in 2025, whereas ready-to-eat products are set to grow at a 3.74% CAGR to 2031.

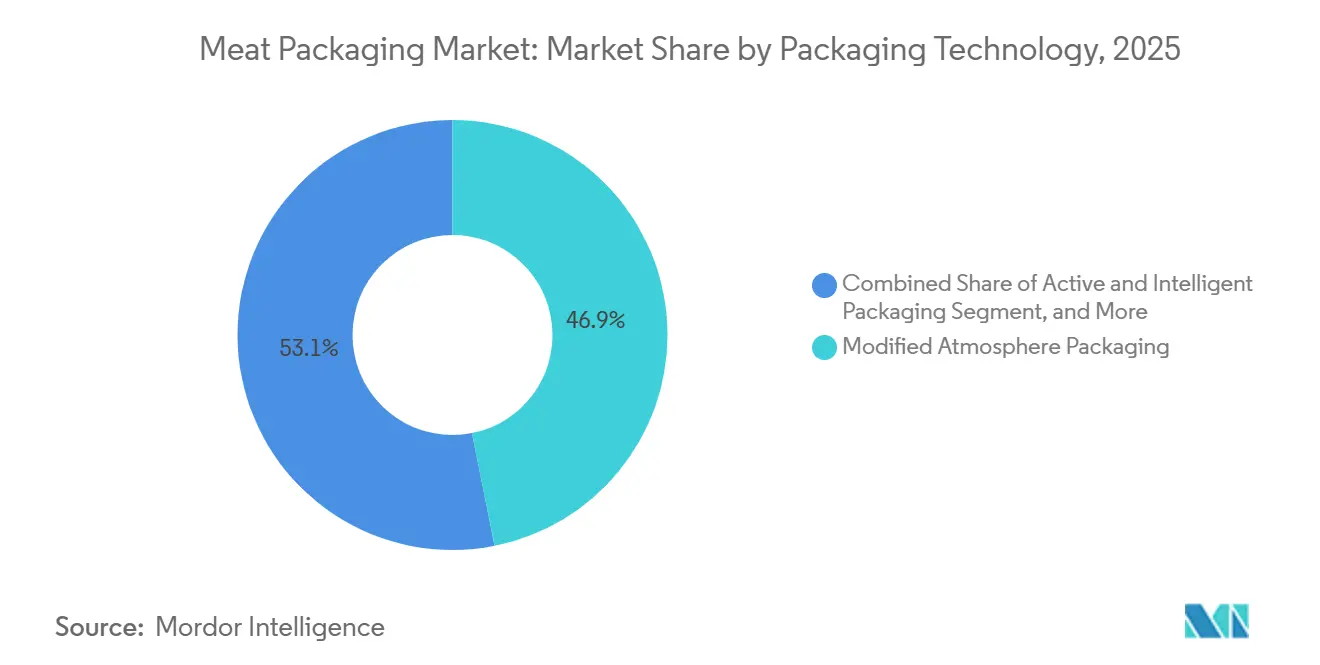

- By packaging technology, modified atmosphere packaging commanded 46.87% share in 2025, while active and intelligent formats are forecast to register a 3.91% CAGR over 2026-2031.

- By end-user channel, retail stores captured 52.42% of the meat packaging market share in 2025, but online grocery and meal-kit platforms are expected to achieve a 3.96% CAGR during the same period.

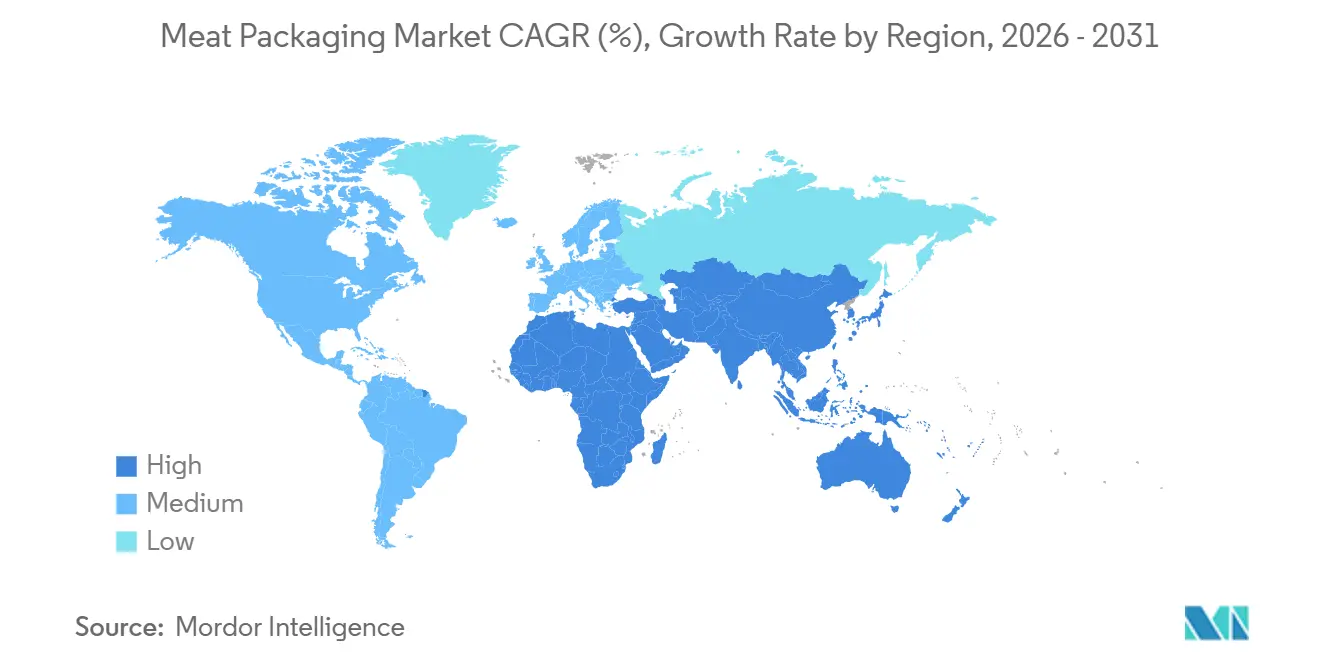

- By geography, North America accounted for 33.41% of the 2025 value, whereas Asia-Pacific is anticipated to post the fastest CAGR of 4.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meat Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenience and ready-to-eat meat products | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of organized retail and cold-chain logistics | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Shelf-life extension and food-safety regulations | +0.7% | Global, led by United States, European Union, China | Short term (≤ 2 years) |

| Sustainability-led shift to high-barrier mono-materials | +0.6% | Europe and North America, early adoption in Japan and South Korea | Medium term (2-4 years) |

| Adoption of antimicrobial and nanocomposite films | +0.4% | North America and Europe, pilots in Brazil and India | Long term (≥ 4 years) |

| Blockchain-enabled traceability and tamper-evident packs | +0.3% | North America and Europe, expanding to China and United Arab Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Convenience and Ready-to-Eat Meat Products

Ready-to-eat proteins posted an 8% year-on-year lift in 2025 across North America and Western Europe as dual-income households compressed meal-prep windows.[1]U.S. Department of Agriculture, “Consumer Trends in Convenience Foods,” usda.gov Microwaveable pulled pork, sous-vide poultry, and charcuterie kits now command 22% of refrigerated meat shelf space, up six percentage points in two years. To meet this demand, converters are engineering multilayer films that tolerate 121 °C retort cycles yet peel cleanly for single-serve access. Japan’s convenience stores introduced nitrogen-flushed bento boxes with integrated desiccant sachets in early 2025, taking chilled shelf life to 10 days and cutting spoilage by 18%. These shifts are raising margins on portion-control trays and resealable zippers, which earn converters about 15% more than commodity stretch film.

Expansion of Organized Retail and Cold-Chain Logistics

Asia-Pacific added 18 million m³ of refrigerated storage in 2025, with China responsible for 60% of capacity and India 25% under its Pradhan Mantri Kisan Sampada Yojana subsidy program. Modern trade penetration in India reached 15% of grocery turnover, enabling vacuum-skin and MAP formats previously impossible in warm, last-mile conditions. In sub-Saharan Africa, donor-funded solar cold rooms reduced meat spoilage by 30%, illustrating how infrastructure density correlates with premium-pack uptake.[2]World Bank, “Solar Cold Storage Projects in Africa,” worldbank.org Markets with cold storage per capita below 0.1 m³ remain dominated by canned meat, whereas those above 0.3 m³ rapidly shift to chilled MAP trays.

Shelf-Life Extension and Food-Safety Regulations

The United States required validated shelf-life studies for ready-to-eat meats from January 2025, pushing 40% of small processors toward antimicrobial dips and high-barrier films. Europe capped migration levels for nanoscale additives in mid-2025, compelling converters that use silver or zinc oxide particles to file new dossiers.[3]European Commission, “Packaging and Packaging Waste Regulation,” ec.europa.eu China’s traceability mandate now blocks non-QR-coded beef and pork from tier-one cities, further tightening compliance windows. Collectively, these rules have redirected capital toward co-extrusion lines capable of integrating barriers and variable-data printing in a single pass.

Sustainability-Led Shift to High-Barrier Mono-Materials

Europe’s packaging regulation, enforceable since January 2025, forbids non-recyclable multi-material laminates, igniting a race to polyethylene-only structures with oxygen transmission rates below 5 cc/m²/day. Amcor’s seven-layer AmPrima film delivers a 21-day chilled shelf life for ground beef and is already listed by Tesco and Carrefour. Japan layered a resource-circulation tax of JPY 50 (USD 0.34) per kilogram of virgin resin in April 2025, lifting recycled-content demand by 28% over six months. As a result, a two-tier market is emerging: premium mono-material packs for export lines and lower-cost legacy laminates for domestic outlets with looser mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-waste regulations and recyclability challenges | -0.5% | Europe, North America, Japan, South Korea | Short term (≤ 2 years) |

| Volatile polymer and metal input prices | -0.4% | Global, acute in South America and Middle East | Short term (≤ 2 years) |

| Single-use-packaging taxes and extended producer responsibility fees | -0.3% | Europe, Canada, emerging India and Brazil | Medium term (2-4 years) |

| Growth of alternative proteins reducing red-meat demand | -0.2% | North America and Europe, early signals in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Waste Regulations and Recyclability Challenges

California’s SB 54 will extract USD 500 million annually from packaging producers to bankroll municipal recycling, while Canada mandates 75% recyclability by 2030. Europe’s PPWR bans oxo-degradable plastics, and India insists on 30% recycled content in rigid packs by 2027, a target that exceeds current resin supply by 40%. The resulting compliance mosaic forces exporters to maintain triple packaging lines, diluting scale economies. Eastern European converters ship scrap west at EUR 200 per ton, eroding closed-loop economics, and chemical-recycling pilots still struggle with EUR 50 million capex hurdles and uncertain mass-balance acceptance.

Volatile Polymer and Metal Input Prices

Polyethylene swung 35% in 2025 on U.S. cracker outages, Chinese demand whiplash, and European gas price spikes, shaving 200 basis points off converter margins. Aluminum for semi-rigid trays rose 18% after Indonesian and Australian bauxite quotas, while Chinese dual-control energy caps cut smelter output by 1.2 million tons. Steel for aerosol and composite cans inflated 12% as Brazilian iron-ore expansions slipped. Berry Global and Sealed Air are therefore moving upstream into resin compounding to lock in formula pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Flexible Formats Drive Recyclability Gains

Plastic formats accounted for 41.23% of the meat packaging market share in 2025 and, on present trajectories, will deliver a 3.56% CAGR through 2031. Within that pool, flexible pouches capture 60% of volume thanks to a 40% weight edge over rigid trays, which lowers freight bills and carbon scores that retailers now audit. The meat packaging market for rigid trays is still expanding in warehouse clubs that need stackability, but overall growth is slower than for flexible lines. Metal formats, dominated by aluminum semi-rigid trays and foil lids, hold the balance: aluminum supplies 70% of metal tonnage because it pairs heat resistance with premium positioning for steak and seafood lines. Regulatory pressure is relentless. ISO 18604 recyclability norms adopted in 2025 disqualify metallized films that delaminate during wash cycles, pushing capital toward multilayer polyethylene that maintains barrier integrity while sorting cleanly.

Investment signals confirm the tilt. Amcor poured USD 120 million into an 11-layer line in Ghent to eliminate polyamide tie layers. Sealed Air’s new polyethylene vacuum-skin film extends beef shelf life to 18 days and still qualifies for mechanical recycling. Europe’s AGEC law slaps a EUR 0.10 fee on each aluminum tray, curbing food-service adoption, although oven-ready segments still pay the premium. The dual objective of keeping oxygen out and value in without complicated laminates is steering converter roadmaps for the next five years.

By Meat Type: Ready-To-Eat Lines Accelerate

Fresh and frozen cuts accounted for 36.74% of value in 2025, but ready-to-eat lines are on track for the fastest 3.74% CAGR through 2031 as consumers trade meal prep for microwavable convenience. The meat packaging market size captured by processed sausages, bacon, and deli slices is stable overall, yet fragments between artisanal, low-additive SKUs growing at mid-single digits in Western economies and shrinking commodity hot-dog lines. Ready-to-eat growth is catalyzing investment in retort-stable pouches and portion-control cups that reduce food waste. Japan’s nitrogen-flushed bento packs raised shelf life to 10 days and now guide similar initiatives in South Korea.

Fresh and frozen still provide the tonnage foundation, especially in inland China and rural South Asia, where cold-chain gaps enforce blast-freezing. New capacity of 18 million m³ in China for 2025 alone allows modified-atmosphere trays for chilled pork to appear in first-tier cities. Regulatory heat adds complexity: the U.S. FSIS now mandates 60-day shelf-life validation for ready-to-eat lines, prompting increased uptake of antimicrobial films. Converter portfolios must therefore straddle commodity vacuum film for high-throughput poultry and high-spec retort laminate for premium grab-and-go segments.

By Packaging Technology: Active Formats Win Retailer Buy-In

Modified atmosphere packaging retained 46.87% of revenue in 2025 because it carries chilled beef through a 14-day replenishment cycle, yet active and intelligent formats will capture the fastest 3.91% CAGR as retailers shift spoilage risk upstream. Iron-based oxygen scavengers are now standard in most premium ground-beef trays, reducing residual oxygen to below 0.5% and preventing browning. U.S. supermarkets doubled usage of time-temperature indicators to 8% of packs in two years. Vacuum-skin subformats additionally reduce void space, shaving freight costs by 25% for e-commerce boxes.

Edible coatings and biodegradable films still have penetration below 2% but attract grants and venture funding. Chitosan and cellulose solutions added 10 days of shelf life in controlled trials, yet require FDA GRAS clearance and continuous-film throughput before commercial launch. European rules capping nanoparticle migration at 0.05 mg/kg force converters to re-test silver-ion substrates, lengthening development timelines. Blockchain-enabled QR codes have scaled up after Walmart set a Q4 2026 deadline for beef and pork suppliers to join IBM Food Trust, a capability that mid-tier converters without digital printing lines struggle to achieve.

By End-User Channel: E-Commerce Reshapes Format Demands

Retail still accounted for 52.42% of 2025 revenue, but online grocery and meal-kit operators will log the fastest 3.96% CAGR as direct-to-consumer cold chains mature. U.S. e-commerce accounted for 12% of meat spend in 2025, up from 8% two years earlier, driven by Amazon Fresh and subscription models that ship vacuum-packed cuts in insulated cartons. These logistics chains need puncture-resistant, tamper-evident film and dimensionally efficient shapes to dodge volumetric shipping fees. Food-service regained volume as dining rebounded, yet kitchen labor gaps nudged operators toward pre-portioned sous-vide proteins that cut back-of-house prep by 40%.

Processors are hedging supply risk by insourcing packaging. JBS installed thermoforming lines across its U.S. beef plants in 2025, reducing lead time from 6 weeks to 10 days. Tyson is working with Sealed Air on antimicrobial films that extend the shelf life of ready-to-eat chicken to 75 days. California’s AB 1200 will outlaw polystyrene foam trays in restaurants from January 2026, forcing HORECA suppliers to adopt molded fiber or polyethylene trays that cost 20% more but meet compostability mandates.

Geography Analysis

North America generated 33.41% of global revenue in 2025, propelled by 28 kg per capita red meat intake and strict FSIS labeling that rewards high-barrier, tamper-evident packs. Canada’s 75% recyclability rule is already steering converters toward mono-material polyethylene, while Mexico’s shift from paraffin-coated paper to vacuum-skin packs is unlocking chilled exports that command 25% price premiums. Plant-based proteins now absorb 8% of refrigerated meat shelf space, introducing a mild volume drag that converters counterbalance with value-added formats. The FDA’s Q2 2025 guidance on antimicrobial packaging tightened silver-ion migration limits, delaying several new product launches and lengthening qualification cycles.

Asia-Pacific will record the quickest 4.19% CAGR, underpinned by China’s cold-chain surge and India’s climb to 15% modern-trade share of grocery spend. China’s QR-code mandate for imported beef and pork fences out non-traceable products, leveling the playing field for domestic chilled lines that meet the spec. India’s 2025 subsidy pool of INR 45 billion (USD 540 million) fast-tracked cold storage, enabling vacuum-skin mutton packs for urban supermarkets. Japan and South Korea copied nitrogen-flush convenience packs pioneered by 7-Eleven, pulling active and intelligent films deeper into mainstream retail. In contrast, cold-chain deficits keep inland China and rural South Asia reliant on frozen or canned meat.

Europe’s directive requiring 65% of plastic to be recyclable by 2030 is the global benchmark, propelling investment in mechanical recycling hubs clustered in Germany, the Netherlands, and Italy. Eastern European converters face EUR 200-per-ton freight to move scrap west, eroding margins and accelerating consolidation. The United Kingdom’s GBP 200 per-ton plastic packaging tax, levied on packs with under 30% recycled resin, spurred a 22% jump in demand for mechanically recycled polyethylene in 2025. France’s EUR 0.10 levy on aluminum trays is spurring a shift to molded-fiber alternatives in hospitality. South America rides beef export growth to China and the Middle East, adopting blockchain-stamped trays to clear customs hurdles, while donor-funded cold rooms in sub-Saharan Africa are trimming poultry spoilage by 30%. Middle East importers, led by the United Arab Emirates, buy European-spec MAP trays for halal beef, balancing premium quality against shipping costs.

Competitive Landscape

The meat packaging sector shows moderate concentration, with the top five converters holding roughly 35% of global revenue. Amcor, Sealed Air, Berry Global, Mondi, and Crown Holdings set technology baselines that regional specialists follow. Their combined scale secures resin at formula pricing and funds multilayer co-extrusion lines that smaller rivals cannot match. Yet more than 600 local converters remain active, supplying niche vacuum-skin films and molded-fiber trays to nearby processors. This long tail keeps price competition lively in emerging markets and prevents any single firm from dictating specifications.

Strategic moves in 2025 emphasized backward integration and circular-economy positioning. Amcor bought Moda for USD 195 million, gaining recycled-content extrusion capacity and strengthening European mono-material credentials. Sealed Air filed 12 patents covering the integration of oxygen scavengers into vacuum-skin film, extending chilled beef shelf life to 21 days. Berry Global acquired a 60% stake in a Brazilian flex-pack producer, adding 12,000 tons of meat-pack capacity and a deeper South American reach. Mondi partnered with a German processor to co-develop a paper-based modified-atmosphere tray that cuts plastic content by 40%.

Technology adoption now separates the premium and commodity tiers more than geography does. Converters that invested in digital printing and blockchain-ready serial coding capture retailer programs that demand pack-level traceability. Firms locked into commodity stretch film face margin pressure from Asian imports and tightening recyclability rules. The competitive field, therefore, rewards companies that pair polymer science with data systems, while leaving room for agile specialists to serve regional tastes.

Meat Packaging Industry Leaders

Amcor plc

Sealed Air Corporation

Berry Global Group Inc.

Mondi plc

Crown Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Amcor plc committed USD 150 million to expand recycled-content polyethylene at its Oshkosh, Wisconsin plant, targeting 50,000 tons of annual mono-material capacity by Q4 2027.

- January 2026: Sealed Air launched Cryovac Darfresh Infinity, a polyethylene-only vacuum-skin line achieving a 21-day beef shelf life and winning early listings at Tesco and Carrefour.

- December 2025: Berry Global bought a 60% stake in a Brazilian flexible converter for USD 85 million, adding 12,000 tons of meat-pack capacity.

- November 2025: Mondi partnered with a German processor to create a paper-based MAP tray that trims plastic by 40% yet secures a 14-day ground-pork shelf life.

Global Meat Packaging Market Report Scope

The Meat Packaging Market Report is Segmented by Material Type (Plastic, and Metal), Meat Type (Fresh and Frozen, Processed, Ready-to-Eat), Packaging Technology (Modified Atmosphere Packaging, Vacuum Skin Packaging, Active and Intelligent Packaging, Edible and Biodegradable Films), End-User Channel (Retail, Food-Service/HORECA, Online Grocery and Meal-Kit, Meat Processors/Packers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Plastic | Flexible Pouches |

| Rigid Trays and Containers | |

| Metal | Aluminium |

| Steel | |

| Other Metals |

| Fresh and Frozen |

| Processed |

| Ready-to-Eat |

| Modified Atmosphere Packaging |

| Vacuum Skin Packaging |

| Active and Intelligent Packaging |

| Edible and Biodegradable Films |

| Retail |

| Food-Service / HORECA |

| Online Grocery and Meal-Kit |

| Meat Processors / Packers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Plastic | Flexible Pouches | |

| Rigid Trays and Containers | |||

| Metal | Aluminium | ||

| Steel | |||

| Other Metals | |||

| By Meat Type | Fresh and Frozen | ||

| Processed | |||

| Ready-to-Eat | |||

| By Packaging Technology | Modified Atmosphere Packaging | ||

| Vacuum Skin Packaging | |||

| Active and Intelligent Packaging | |||

| Edible and Biodegradable Films | |||

| By End-User Channel | Retail | ||

| Food-Service / HORECA | |||

| Online Grocery and Meal-Kit | |||

| Meat Processors / Packers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the meat packaging market today?

The meat packaging market size reached USD 12.57 billion in 2026 and is on track to hit USD 14.65 billion by 2031.

Which packaging technology is growing the quickest?

Active and intelligent formats, including oxygen scavengers and time-temperature indicators, are projected to grow at a 3.91% CAGR through 2031.

What drives demand for ready-to-eat meat packaging?

Dual-income households and shrinking meal-prep windows are boosting ready-to-eat lines, which are advancing at a 3.74% CAGR over 2026-2031.

How will EU recyclability rules affect materials used?

The EU requirement that 65% of plastic packs be recyclable by 2030 is shifting investment toward polyethylene-only mono-materials that qualify for mechanical recycling.

Which region offers the fastest growth opportunity?

Asia-Pacific leads with a 4.19% CAGR, fueled by massive cold-chain expansion in China and India’s rising organized retail share.

How concentrated is supplier power in this space?

The top five converters hold around one-third of revenue, giving the market a moderate concentration profile with room for regional specialists.

Page last updated on: