Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

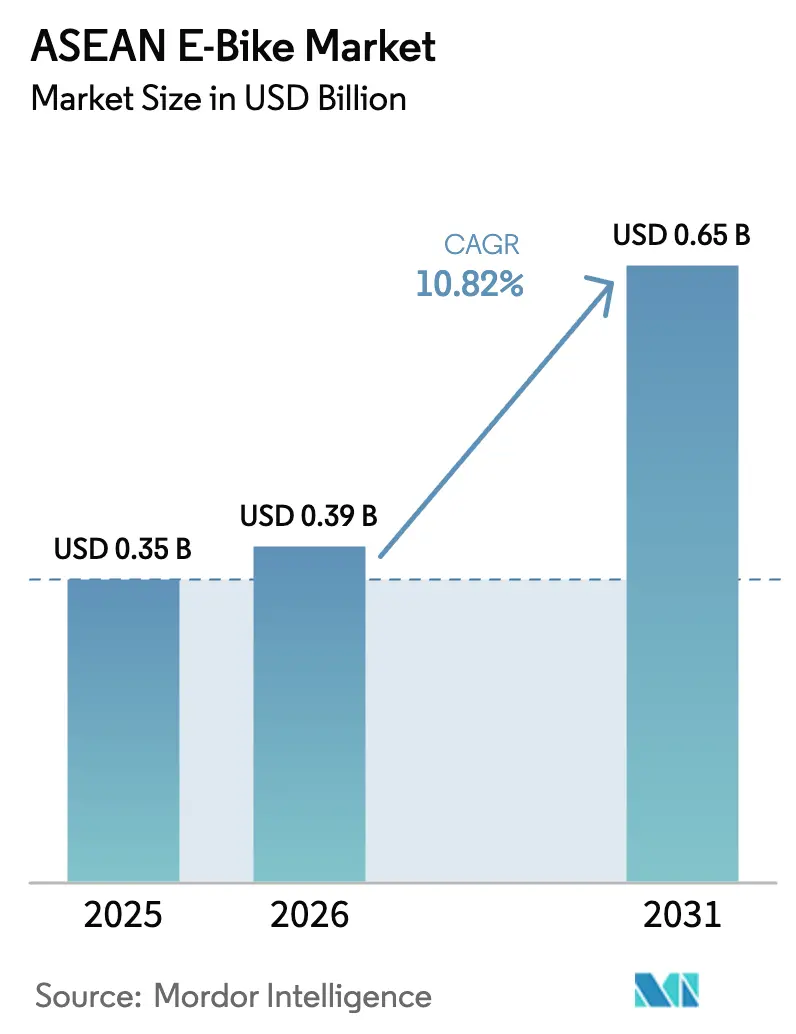

| Base Year Market Size (2025) | USD 0.35 Billion |

| Market Size (2026) | USD 0.39 Billion |

| Market Size (2031) | USD 0.65 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

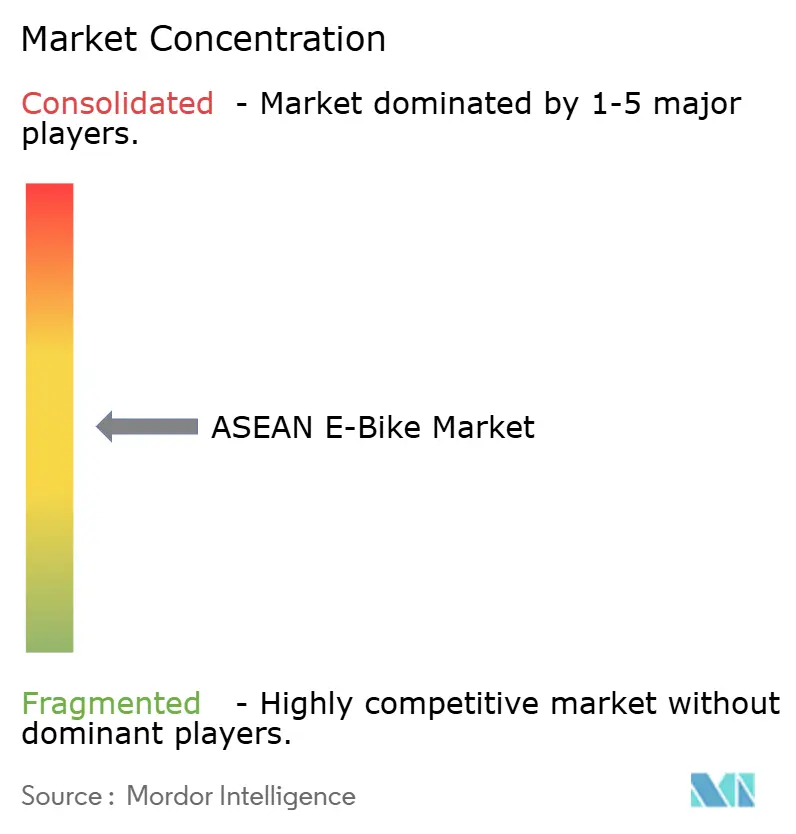

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN E-Bike Market Analysis by Mordor Intelligence

Asean e-bike market size in 2026 is estimated at USD 0.39 billion, growing from 2025 value of USD 0.35 billion with 2031 projections showing USD 0.65 billion, growing at 10.82% CAGR over 2026-2031. Rapid switching from internal-combustion two-wheelers to battery power is accelerating as urban policies tighten emissions, consumer awareness of operating costs improves, and local supply chains scale up. Subsidy programs in Vietnam, Indonesia, and Thailand are anchoring early adoption, while corporate fleet electrification and higher battery energy density further reinforce demand. Competition remains dispersed because legacy bicycle brands, pure-play electric start-ups, and motorcycle OEMs all vie for share, yet the growing availability of under-USD 1,000 models keeps volumes rising in price-sensitive cities. Infrastructure gaps still temper progress, but pilot solar-powered swap stations and informal charging points are reducing range anxiety and widening the Asean e-bike market’s addressable base.

Key Report Takeaways

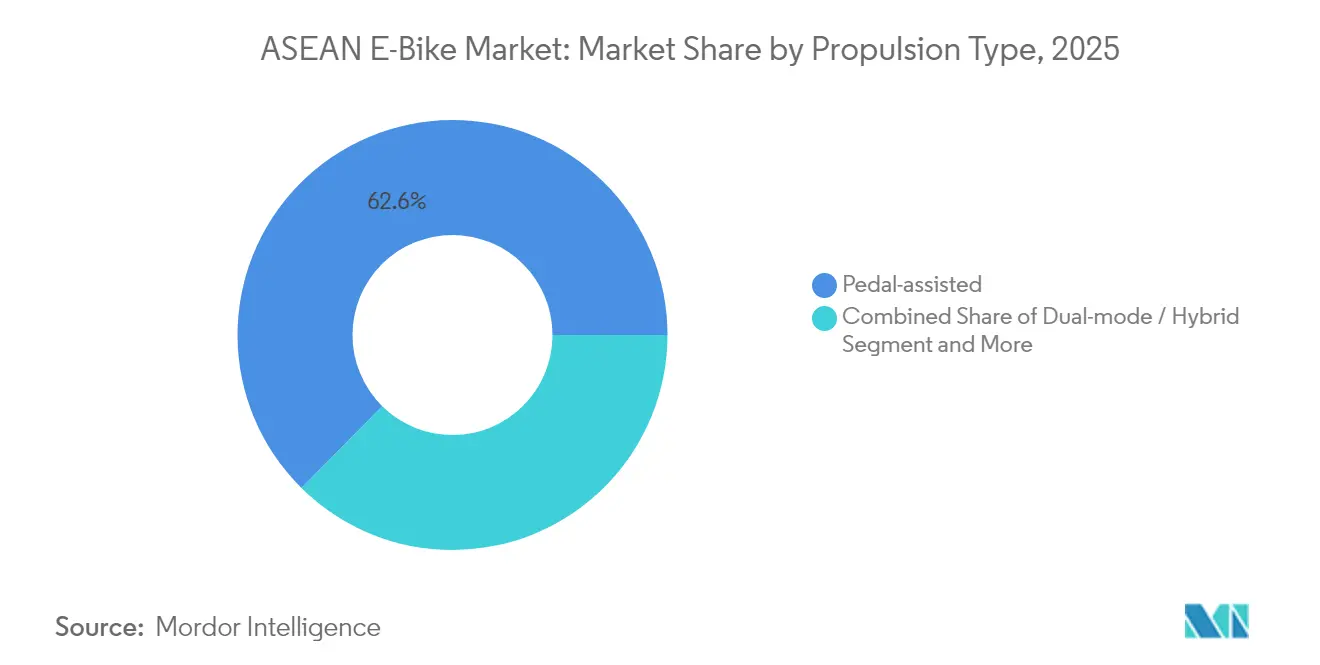

- By propulsion type, pedal-assisted models held 62.60% of the ASEAN e-bike market share in 2025, whereas dual-mode hybrids are forecast to post a 12.20% CAGR through 2031.

- By motor type, hub drives commanded an 81.90% of the ASEAN e-bike market share in 2025, while mid-drive systems are set to climb at a 12.60% CAGR to 2031.

- By battery chemistry, lithium-ion captured 90.10% of the ASEAN e-bike market share in 2025, and is projected to grow fastest at an 11.20% CAGR during 2026-2031.

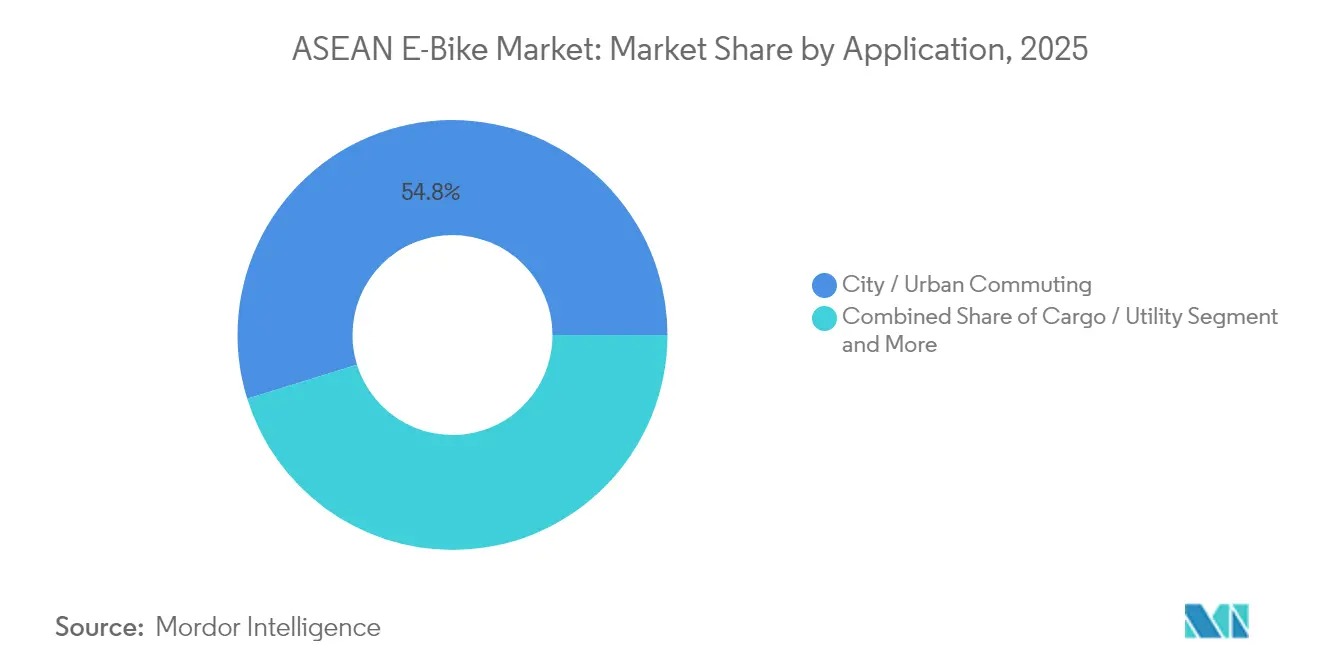

- By application, city commuting captured 54.80% of the ASEAN e-bike market share in 2025, and fleet delivery is projected to grow at a 12.90% CAGR during 2026-2031.

- By price band, models below USD 1,000 accounted for 65.70% of the ASEAN e-bike market share in 2025, and the USD 1,000-2,000 tier should rise at 11.40% CAGR to 2031.

- By country, Vietnam controlled 28.70% of the ASEAN e-bike market share in 2025, whereas the Philippines is anticipated to expand at a 11.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN E-Bike Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government E-Mobility Incentives | +2.8% | Vietnam, Indonesia, Thailand core; expanding to Malaysia and the Philippines | Short term (≤ 2 years) |

| Corporate E-Bike Fleet Expansion | +2.1% | Urban centers in Vietnam, Indonesia, Thailand, Singapore | Medium term (2-4 years) |

| Urban Congestion and Vehicle Restrictions | +1.9% | Jakarta, Bangkok, Manila, Hanoi, Ho Chi Minh City | Medium term (2-4 years) |

| Rising Battery Energy Density | +1.7% | Strongest in Vietnam, Thailand | Long term (≥ 4 years) |

| Tourism Micro-Mobility Schemes | +1.2% | Bali, Phuket, Langkawi, Boracay | Short term (≤ 2 years) |

| Solar-Powered Swap Station Pilots | +0.8% | Secondary urban centers, pilots in Vietnam and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government E-Mobility Incentives and Purchase Subsidies

Fiscal support is accelerating shifts from gasoline motorcycles to electric options. Vietnam’s 0% registration tax and public-charger rollout underpinned notable sales in H1 2025, ranking the country third worldwide [1]Tuấn Lê, “Việt Nam tiêu thụ xe máy điện nhiều thứ ba thế giới,” CafeF, cafef.vn. Indonesia moved from a significant cash grant to a VAT discount in 2025, yet still lifted subsidized volumes in 2024. Thailand’s BEV 3.5 plan combines duty relief and local-content bonuses, and Malaysia plus the Philippines are drafting parallel packages. These converging measures send reliable demand signals that justify tooling investments and raise the Asean e-bike market’s medium-term visibility.

Expansion of Corporate E-Bike Fleets for Last-Mile Logistics

B2B buyers are electrifying two-wheeler fleets to cut fuel costs and comply with low-emission-zone rules. Vietnam’s ride-hailing decree obliges 400,000 motorcycles to switch by 2029. Indonesian couriers in Jakarta and Surabaya report significant operating cost savings after adopting e-bikes, prompting multi-year procurement contracts. Fleet operators value battery-swap compatibility, heavy-duty frames, and extended warranties, creating design niches that favor commercial-grade platforms and lock in repeat orders for the Asean e-bike market.

Urban Congestion Pricing and ICE-Vehicle Restrictions

City authorities are converting policy intent into enforceable bans. Hanoi will exclude gasoline motorcycles inside Ring Road 1 from July 2026 and expand coverage to Rings 2 and 3 by 2030. Ho Chi Minh City blocks new gasoline motorcycles for ride-hailing from 2026, instantly diverting demand toward compliant e-bikes [2]Sultan Abdurrahman, “Outlook 2025: Menanti Perkembangan Infrastruktur Kendaraan Listrik,” Tempo.co, tempo.co. Jakarta’s odd-even plate limits and Bangkok’s congestion-pricing draft underline a Southeast-Asian shift in which electric propulsion becomes a prerequisite for inner-city access, reinforcing the uptake curve of the Asean e-bike market.

Rising Battery Energy Density Lowering Total Cost of Ownership

Higher-density lithium-ion packs extend range yet trim weight, boosting user acceptance in stop-and-go traffic. Vertically integrated Chinese majors supply lower-cost modules while unveiling sodium-ion prototypes that resist tropical heat and charge faster. Declining battery prices tilt five-year total-cost-of-ownership models in favor of electric, especially where gasoline tops USD 1.10 per liter, sustaining long-run gains for the Asean e-bike market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Charging and Swapping Infrastructure | −1.8% | Rural and secondary urban areas across ASEAN | Medium term (2-4 years) |

| Popularity of Low-Priced ICE Scooters | −1.4% | Indonesia, Philippines, Vietnam rural areas | Short term (≤ 2 years) |

| Fragmented Homologation Standards in ASEAN | −0.9% | All member states | Long term (≥ 4 years) |

| Lithium-Ion Cell Import Tariffs | −0.7% | Thailand, Malaysia, Singapore, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Public Charging/Swapping Infrastructure

Indonesia fielded only 3,772 public charging points as of March 2025, a notable share of its 2030 target [3]Anh Vũ, “Hãng xe máy điện Trung Quốc tự sản xuất pin, động cơ, mỗi năm bán 9 triệu xe,” Cafebiz, cafebiz.vn. Rural riders lack home garages, so range anxiety dampens uptake. Private investors hesitate until traffic justifies payback, prolonging the chicken-and-egg cycle that restricts rural penetration of the Asean e-bike market.

Popularity of Low-Priced ICE Scooters

Honda’s gasoline scooters still outsell electrics because extensive dealer networks reassure buyers. In Thailand, a Honda automatic costs more than a Yadea RS20 yet commands loyalty through perceived reliability. Until subsidies bridge purchase-price gaps, many first-time owners in Indonesia and the Philippines stay with fuel models, diluting total addressable volumes for the Asean e-bike market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Pedal-Assisted Models Drive Mainstream Adoption

The pedal-assist category represented 62.60% of the ASEAN e-bike market share in 2025 as consumers valued hybrid exercise and electric thrust. Dual-mode hybrids should log the top-line 12.20% CAGR through 2031, widening the ASEAN e-bike market by attracting riders who want throttle freedom on hills yet license-free status on cycle lanes. Regulatory flexibility, especially where pedal-assists qualify as bicycles, supports broad commuter acceptance.

Continuation of the same sub-heading adds that throttle-only variants hold niches in delivery services requiring constant stop-start bursts, while regulators in Vietnam may demand mirrors and turn signals for higher-speed classes. As model choice diversifies, manufacturers integrate smart controllers that toggle between human-power bias and full motor drive, increasing perceived value in the ASEAN e-bike market.

By Motor Type: Hub Dominance Confronted by Rising Mid-Drive Appeal

Hub motors owned 81.90% of the ASEAN e-bike market share in 2025 because they are cheap to produce, sealed against tropical rain, and simple to service. Yet the mid-drive slice is expanding at 12.60% CAGR as sport commuters and cargo couriers appreciate balanced weight and torque multiplication. Brands now market removable mid-drive powertrains that simplify fleet maintenance, hinting at a gradual technological pivot within the ASEAN e-bike market.

At the same time, friction-drive kits survive in retrofit circles where riders wish to electrify existing bicycles for under USD 300. Although marginal in volume, such kits introduce new users who could migrate to factory e-bikes, feeding future replacement cycles in the ASEAN e-bike market.

By Battery Chemistry: Lithium-Ion Retains Overwhelming Lead

Lithium-ion packs covered 90.10% of the ASEAN e-bike market share in 2025 and are tracking an 11.20% CAGR. Higher watt-hour density extends per-charge range to 120 km on 1 kWh packs, sufficient for daily city trips. Sodium-ion prototypes may appear in 2027 models, promising better heat resilience and materially hedging lithium price swings, which could unlock fresh cost tiers for the ASEAN e-bike market.

Lead-acid options persist in cost-constrained rural districts but lose share as second-hand lithium units enter the resale channel. Improved recycling networks further tip buyer sentiment toward modern chemistries, cementing lithium-ion’s supremacy in the ASEAN e-bike market.

By Application: Commuting Dominates While Fleet Delivery Surges

Urban commuting soaked up 54.80% of the ASEAN e-bike market share in 2025 after cities launched low-emission corridors and secure parking hubs. Delivery and fleets, however, drive the fastest-growing tranche at 12.90% CAGR because riders cover 100-150 km daily and redeem cost savings within 18 months. Fleet feedback loops push suppliers to enlarge battery-swap compatibility, hastening iteration cycles in the ASEAN e-bike market.

Outdoor trekking and e-mountain segments revolve around Thailand’s Chiang Mai trail tourism and Vietnam’s Sơn La circuits, where mid-drives rule. Compact folding e-bikes facilitate first-mile transit to metro stations in Singapore, proving the modal versatility that broadens the user base and stabilizes unit demand for the ASEAN e-bike market.

By Price Band: Sub-USD 1,000 Tier Anchors Volume, Mid-Tier Climbs

Models under USD 1,000 formed 65.70% of the ASEAN e-bike market share in 2025 as household incomes in Indonesia, Vietnam, and the Philippines guided budgets. Dealers bundle free helmets and first-year maintenance to attract first-time buyers, sustaining checkout momentum in the ASEAN e-bike market.

Mid-tier offerings between USD 1,000-2,000 are recording an 11.40% CAGR on the back of larger batteries, smartphone connectivity, and disc brakes. Premium units above USD 2,000 stay niche but spotlight innovation that eventually trickles down, reinforcing aspirational marketing within the ASEAN e-bike market.

Geography Analysis

Vietnam’s 28.70% of the ASEAN e-bike market share in 2025 rested on coordinated incentives and burgeoning domestic output. Progressive exclusion of gasoline motorcycles inside Hanoi’s Ring Road 1 from 2026 and ride-hailing electrification in Ho Chi Minh City ensure sustained demand within the Asean e-bike market.

Indonesia sits on the region’s deepest two-wheeler base. Subsidized electric purchases grew after the VAT-discount schema replaced cash grants. Jakarta’s aim 4.5 million by 2035 charts a towering runway, although charger deployment must accelerate to unlock the full promise for the Asean e-bike market.

The Philippines advances fastest at 11.80% CAGR due to Urban Green Mobility guidelines that earmark e-bike lanes across Metro Manila. Thailand’s Samut Prakan plant started shipping in May 2025, targeting significant cumulative units within three years under BEV 3.5 support, while Malaysia and Singapore focus on high-spec categories with smart telematics, offering margin-rich niches that round out regional demand in the Asean e-bike market.

Competitive Landscape

Moderate fragmentation prevails as no single brand exceeds a major region-wide volume. VinFast enjoys local dominance in Vietnam, but Chinese powerhouses Yadea and Tailg leverage a significant global scale to price aggressively in Indonesia and Thailand. Japanese motorcycle majors explore hybrid e-scooter launches, signaling next-wave rivalry inside the Asean e-bike market.

Localization strategies intensify: Yadea's commitment to a Vietnam plant and another line in Thailand to skirt tariffs and meet local-content rules. Dat Bike raises domestic supplier ratios for its Weaver++ model, trimming lead times and fortifying supply resilience. Battery-swap network specialists Mercu and Oyika form cross-country joint ventures that could morph into platform gatekeepers, shaping aftermarket economics across the Asean e-bike market.

Competitive advantages coalesce around vertically integrated battery packs, cybersecurity compliance, and telematics ecosystems that feed predictive maintenance. With UN R155 and R156 cybersecurity rules looming, manufacturers able to certify over-the-air update security may seize institutional fleet tenders, inching market concentration upward in the Asean e-bike market.

ASEAN E-Bike Industry Leaders

Yadea Technology Group Co. Ltd

Giant Manufacturing Co. Ltd

Yamaha Motor Co. Ltd

Trek Bicycle Corporation

Merida Industry Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: JiBike confirmed a January launch of Vietnam’s first electric-bicycle sharing service in Hue with an initial 280-bike fleet.

- February 2024: G-Bike and Hue Monuments Conservation Center agreed to pilot shared electric bicycles at tourist sites, including the Imperial Palace, to advance sustainable tourism.

ASEAN E-Bike Market Report Scope

An e-bike, short for electric bicycle, is a type of bicycle equipped with an electric motor that provides propulsion assistance to the rider. E-bikes typically feature a rechargeable battery that powers the motor, which can be activated through pedaling (pedal-assist) or by using a throttle. This electric assistance enables riders to travel longer distances, tackle hills more easily, and ride at higher speeds with less effort compared to traditional bicycles. E-bikes offer a convenient and eco-friendly mode of transportation, making them increasingly popular for commuting, leisure cycling, and recreational activities.

The ASEAN e-bike market report covers a detailed study of the latest trends and innovations. The report also covers segmentation based on propulsion type, application type, battery type, power type, and country. By propulsion type, the market is segmented into pedal-assisted and throttle-assisted (power-on-demand). By application, the market is segmented into city/urban, trekking (e-mountain bikes/E-MTB), and cargo. By battery type, the market is segmented into lithium-ion and lead-acid batteries. By country, the market is segmented into Vietnam, Indonesia, Malaysia, Thailand, Singapore, and the Rest of Southeast Asia. The report also provides market sizing and forecasts for all the segments mentioned above in USD.

By Propulsion Type

| Pedal-assisted |

| Throttle-assisted (Power-on-demand) |

| Dual-mode / Hybrid |

By Motor Type

| Hub-motor |

| Mid-drive |

| Other motors (e.g., friction) |

By Battery Chemistry

| Lithium-ion |

| Lead-acid |

By Application

| City / Urban Commuting |

| Trekking / E-MTB |

| Cargo / Utility |

| Delivery and Fleet (Last-mile) |

| Folding / Compact |

By Price Band

| Below USD 1,000 |

| USD 1,000 -2,000 |

| Above USD 2,000 |

By Country

| Vietnam |

| Indonesia |

| Malaysia |

| Thailand |

| Singapore |

| Philippines |

| Rest of ASEAN |

| By Propulsion Type | Pedal-assisted |

| Throttle-assisted (Power-on-demand) | |

| Dual-mode / Hybrid | |

| By Motor Type | Hub-motor |

| Mid-drive | |

| Other motors (e.g., friction) | |

| By Battery Chemistry | Lithium-ion |

| Lead-acid | |

| By Application | City / Urban Commuting |

| Trekking / E-MTB | |

| Cargo / Utility | |

| Delivery and Fleet (Last-mile) | |

| Folding / Compact | |

| By Price Band | Below USD 1,000 |

| USD 1,000 -2,000 | |

| Above USD 2,000 | |

| By Country | Vietnam |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Singapore | |

| Philippines | |

| Rest of ASEAN |

Key Questions Answered in the Report

How large will the Asean E-Bike sector be by 2031?

The Asean E-Bike market size is projected to reach USD 0.65 billion by 2031, rising from USD 0.35 billion in 2025 at an 10.82% CAGR.

Which propulsion format leads sales today?

Pedal-assisted e-bikes held 62.60% of 2025 shipments, well ahead of throttle-only and hybrid variants.

Which country currently buys the most electric bicycles in Southeast Asia?

Vietnam commanded 28.70% share in 2025, supported by zero-tax incentives and domestic production.

Where is demand growing fastest in the region?

The Philippines shows the quickest expansion, forecast at a 11.80% CAGR through 2031 as Metro Manila pursues green-mobility lanes.

Page last updated on: