AI In Food And Beverages Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.34 Billion |

| Market Size (2031) | USD 88.37 Billion |

| Growth Rate (2026 - 2031) | 36.96% CAGR |

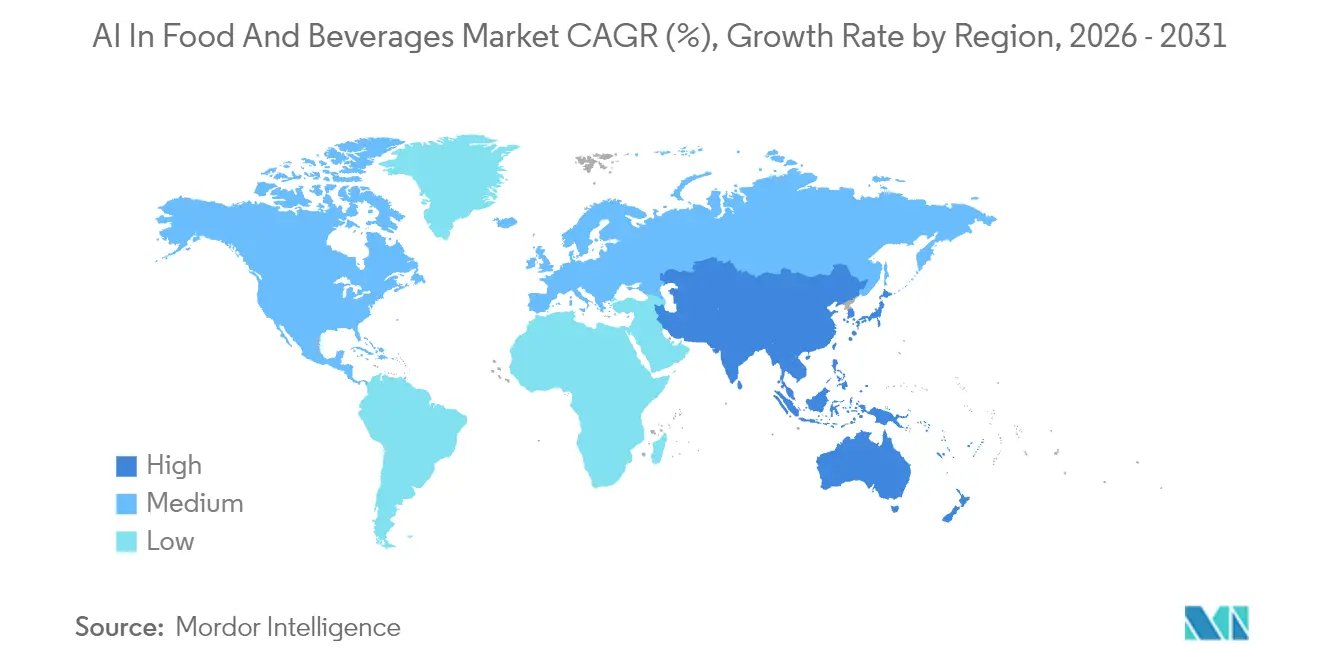

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

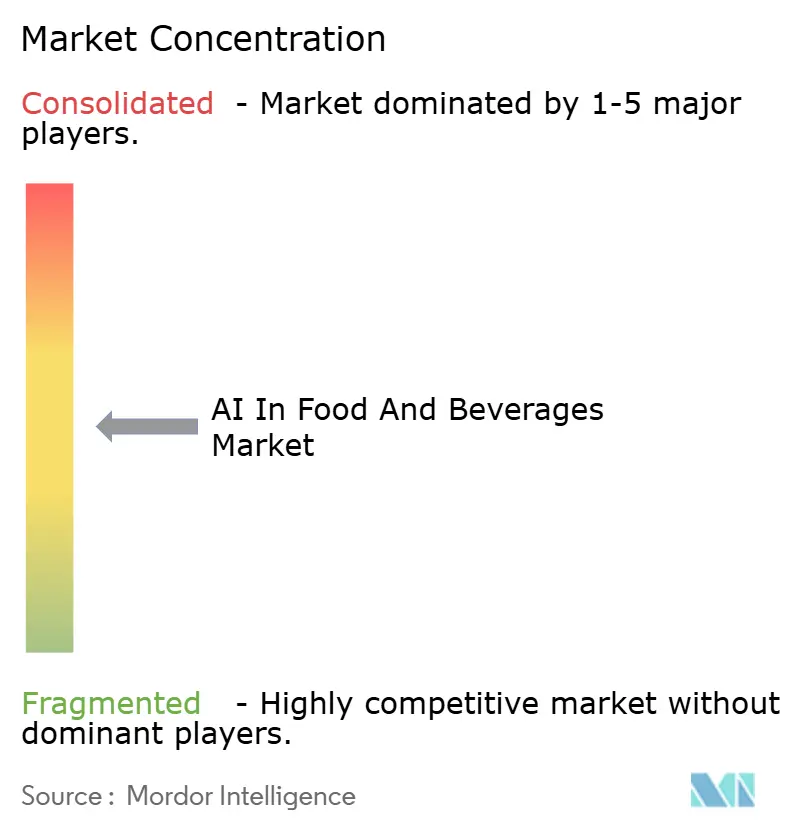

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Food And Beverages Market Analysis by Mordor Intelligence

The AI In Food And Beverages market size is expected to grow from USD 13.39 billion in 2025 to USD 18.34 billion in 2026 and is forecast to reach USD 88.37 billion by 2031 at 36.96% CAGR over 2026-2031.

Surging investments in computer vision, robotics, and predictive analytics help processors offset labor shortages, comply with strict safety norms, and cut waste, while large restaurant chains deploy personalization engines that lift ticket values and customer retention. Market momentum is amplified by government funding for smart-factory projects, cloud providers embedding turnkey AI modules into existing MES platforms, and global retailers tightening sustainability scorecard requirements for suppliers. Heightened competition is shifting emphasis from isolated pilots to enterprise-wide rollouts, with early adopters already reporting 8-12% overall-equipment-effectiveness gains and 10-15% inventory-spoilage cuts. Successful deployments now hinge on access to skilled process engineers who can align algorithm outputs with daily production constraints, making service partnerships a strategic imperative for manufacturers and food-service operators.

Key Report Takeaways

- By component, software solutions led with 47.35% revenue share in 2025, while services are projected to expand at a 40.8% CAGR through 2031.

- By technology, computer vision captured 41.95% of the AI in food & beverages market share in 2025; robotics and automation record the fastest growth at 41.15% CAGR to 2031.

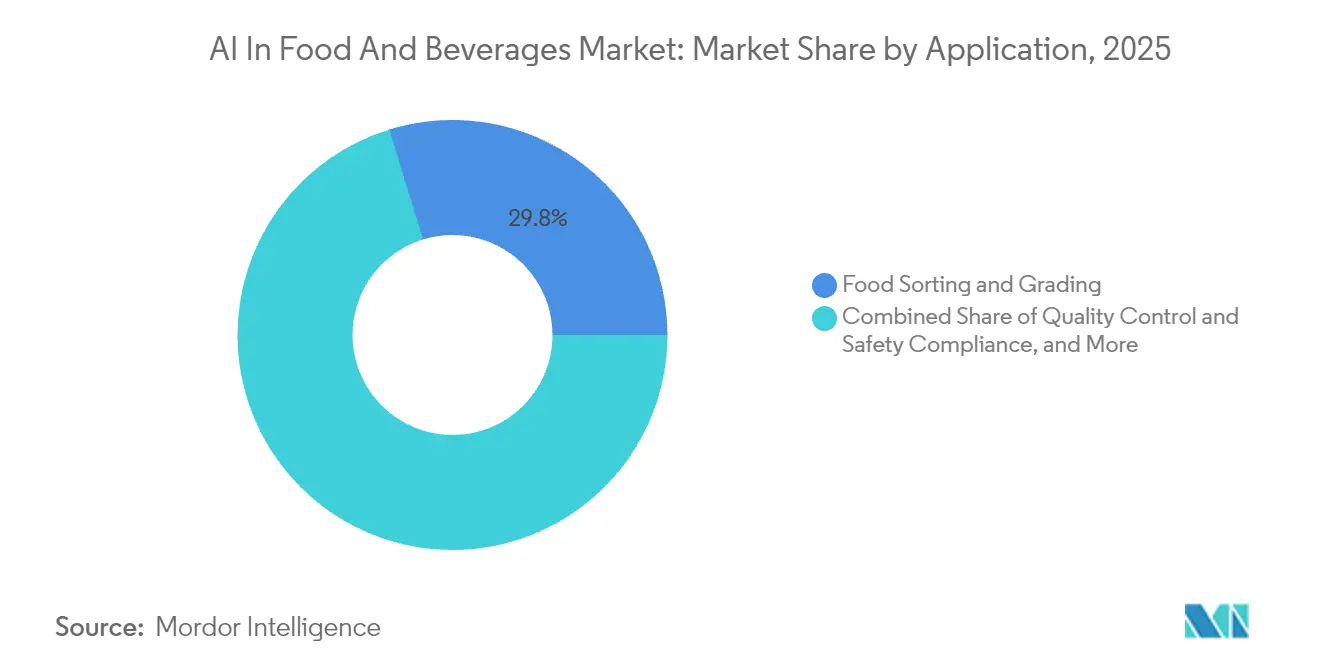

- By application, food sorting and grading accounted for a 29.75% share of the AI in food & beverages market size in 2025, whereas predictive maintenance is advancing at a 41.05% CAGR through 2031.

- By end user, food-processing manufacturers held a 37.10% share in 2025; quick-service and cloud kitchens post the highest projected growth at 38.95% CAGR to 2031.

- By geography, Asia Pacific led with 33.70% revenue share in 2025 and is forecast to grow at 40.25% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-powered computer-vision systems slash defect rates >25% in meat, produce and bakery lines | +8.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Predictive-maintenance algorithms curb unplanned downtime and raise OEE by 8-12% | +7.5% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Personalised menu and promo engines lift average ticket size 15-20% for QSRs and cafés | +6.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Gen-AI accelerates recipe reformulation cycles from months to days, boosting NPD velocity | +5.9% | Global, led by multinational F&B companies | Long term (≥ 4 years) |

| Carbon-traceable AI platforms unlock 5-10% "green-premium" pricing in export markets | +4.1% | EU regulatory markets, expanding globally | Long term (≥ 4 years) |

| End-to-end predictive analytics cut inventory spoilage 10-15%, saving ~USD 30 billion globally | +6.7% | Global, with highest impact in perishables-heavy regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Computer-Vision Systems Slash Defect Rates More than 25% in Meat, Produce, and Bakery Lines

Real-time machine vision now detects microscopic blemishes that manual inspectors miss, lifting first-pass yield and cutting scrap. Accuracy levels exceed 95%, enabling plants to drive defect rates below 2% within half a year. Processors gain further upside by linking vision outputs to line-speed and cutting-parameter adjustments that optimize recovery. Chick-fil-A’s lemon-squeezing robots, for instance, saved 10,000 labor hours in 2024 while standardizing quality[1]Kelly Gilblom, “Chick-fil-A Turns to Robots for Lemon Prep,” Bloomberg, bloomberg.com. These benefits resonate most in high-throughput operations where minor quality gains translate into significant margin protection.

Predictive-Maintenance Algorithms Curb Unplanned Downtime and Raise OEE by 8-12%

AI models analyze vibration and acoustic signatures, giving maintenance teams 2-4 weeks’ lead time to plan interventions and avoiding USD 50,000 per hour losses tied to emergency stoppages. Dairy plants adopting sensor-driven digital twins report 10% capacity upticks and 65% variability reductions. As inflation raises part and labor costs, the value of avoided downtime grows, moving predictive maintenance from optional to mandatory in capital-intensive lines.

Personalised Menu and Promo Engines Lift Average Ticket Size 15-20% for QSRs and Cafes

Natural-language models parse historical orders and real-time inventory to present tailored upsell suggestions during ordering. PepsiCo’s Smart Cans pilot demonstrated the appeal of AI-guided customization. Chains rolling out these engines enjoy higher basket values and reduced menu complexity without sacrificing throughput during peaks, supporting top-line growth even as ingredient prices fluctuate.

Gen-AI Accelerates Recipe Reformulation Cycles from Months to Days, Boosting NPD Velocity

Generative algorithms simulate thousands of formulations, forecasting sensory acceptance before costly pilot trials. Coca-Cola leveraged the approach to design “Y3000 Zero Sugar,” collapsing development timelines and cutting iteration costs by 40%. The methodology particularly benefits brands targeting reduced-sugar, plant-based, or allergen-free niches, where traditional R&D processes struggle to keep pace with shifting consumer preferences.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Full-stack AI roll-outs can exceed USD 5 million per plant, limiting adoption by SMEs | -4.8% | Global, with highest impact in developing markets | Short term (≤ 2 years) |

| Data-ownership and cybersecurity risks deter cloud-based deployments | -3.2% | EU & North America regulatory markets | Medium term (2-4 years) |

| Seasonal ingredient variability causes model-drift, inflating re-training costs | -2.7% | Agricultural-dependent regions globally | Long term (≥ 4 years) |

| Acute shortage of AI-savvy process engineers in F&B plants delays scaling efforts | -5.1% | Global, with severe shortages in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Full-Stack AI Roll-Outs Can Exceed USD 5 Million Per Plant, Limiting Adoption by SMEs

High capital outlays for edge hardware, cloud licences, and systems integration restrain smaller firms, with 79% of processors delaying AI initiatives in 2025 due to cost uncertainty[2]Food Processing Editorial Team, “2025 Manufacturing Outlook Survey,” foodprocessing.com. Modular and subscription models reduce entry hurdles, yet ROI proofs remain essential for board approval in cash-constrained settings.

Data Ownership and Cybersecurity Risks Deter Cloud-Based Deployments

Processors handling sensitive formulations and consumer data fear IP theft, ransomware, and regulatory penalties. Compliance with the EU AI Act 2024/1689 adds documentation burdens that lengthen implementation cycles. Vendors now promote zero-trust architectures and sovereign-cloud options to win cautious clients.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Implementation Services Gain Speed as Software Leads Functional Depth

Software still anchors the AI in the food & beverages market, commanding 47.35% revenue in 2025, thanks to modular platforms that interface easily with legacy MES and PLC layers. Continuous over-the-air updates allow producers to refine algorithms without shutting lines, preserving uptime and lowering the total cost of ownership. Services, however, grow faster at 40.8% CAGR because value shifts to domain experts who can translate generic AI models into plant-specific workflows, calibrate sensors, and train staff on exception handling. Many processors now structure contracts around performance-linked fees, rewarding integrators for measurable yield or energy gains.

Ongoing skills shortages reinforce demand for third-party expertise, and major integrators bundle change-management programs with cloud subscriptions to shorten payback periods. As a result, services are expected to narrow the revenue gap with software by 2031, reflecting a broader sector view that execution quality outweighs tool selection. This convergence pushes vendors toward outcome-as-a-service deals that align incentives and open recurring revenue streams within the AI in food & beverages market.

By Technology: Vision Systems Dominate Today, while Robotics Delivers Future Scale

Computer-vision suites captured the largest share at 41.95% because cameras and high-speed GPUs plug into existing conveyors with minimal disruption. Real-time image analytics automates defect detection, grading, and pack validation, delivering visible ROI within a single budget cycle. Conversely, robotics and automation post a 41.15% CAGR as processors confront labor scarcity and rising hygiene standards. Collaborative robots now portion dough, garnish bowls, and execute clean-in-place tasks, expanding the automation addressable market beyond palletizing and pick-and-place operations.

Integrating vision-guided arms with smart grippers supports gentle handling of fragile items such as pastries or fresh berries, broadening use cases in premium product lines. Government incentives, Japan’s USD 7.8 million culinary-robot grant among them, accelerate capex plans. Over the forecast horizon, hybrid cells that meld robotics, vision, and AI scheduling engines are expected to redefine factory layout economics across the AI in food & beverages market.

By Application: Sorting Leads Revenues, Predictive Maintenance Captures Momentum

Food-sorting and grading accounted for 29.75% of 2025 spending in the AI in food & beverages market, leveraging proven capabilities to detect foreign objects, color deviations, and size inconsistencies at high line speeds. Automated ejection reduces recalls and boosts brand trust, making sorting a staple investment in protein, produce, and bakery segments. Predictive maintenance, though smaller, expands fastest at 41.05% CAGR because every unplanned hour of downtime can erase a week’s profit in thin-margin plants.

Machine-learning models ingest multivariate sensor feeds and historical work-order data to advise maintenance crews on part replacements, thereby lifting OEE by 8-12%. Cloud dashboards share insights across multi-plant networks, letting corporate engineers benchmark asset health and schedule mobile technician teams efficiently. As integrated asset-performance systems mature, predictive maintenance is projected to command a greater slice of the AI in the food & beverages market size by 2031.

By End User: Processors Hold Scale Advantage, QSRs Lead Customer-Facing Innovation

Food-processing manufacturers represented 37.10% of expenditure in 2025, driven by complex batch and continuous operations where minor efficiency gains multiply across high volumes. These firms already run extensive SCADA layers, making them natural candidates for advanced analytics that refine set-points and balance line speeds. Quick-service restaurants and cloud kitchens, however, demonstrate the strongest growth at 38.95% CAGR. They leverage recommendation engines, kitchen-display predictions, and autonomous fryers to enhance guest experience and control labor cost volatility.

Large QSR groups partner with hyperscale clouds to pilot generative voice ordering and AI-driven crew scheduling, compressing wait times and standardizing output quality across thousands of outlets. Positive early metrics encourage franchisees to adopt centralized data platforms, cementing QSRs as pivotal demand drivers within the AI in food & beverages market.

Geography Analysis

Asia Pacific leads the AI in food & beverages market with 33.70% share in 2025 and is expanding at 40.25% CAGR as governments champion smart-manufacturing roadmaps and wage inflation undercuts manual processes. China’s multibillion-dollar AI infrastructure subsidies enable domestic OEMs to offer low-cost vision modules, while India’s food-processing incentives favour startups integrating crop-to-fork data for traceability. Regional pilots show tangible impact: Taiwan’s tea processors lifted capacity 75% and halved labor through AI-enabled lines, illustrating the pragmatic uptake pace.

North America maintains heavyweight status through enterprise alliances, typified by Coca-Cola’s USD 1.1 billion Microsoft agreement that equips plants with predictive quality, demand sensing, and generative marketing tools. Regulatory bodies reinforce adoption; the FDA’s Elsa platform applies machine learning to speed risk-based inspection scheduling, signaling policy support for AI in compliance workflows. Capital budgets remain disciplined, yet boardrooms prioritize proven AI modules that bolster resilience against supply shocks and wage pressure.

Europe balances ambition and caution under the EU AI Act framework, requiring rigorous transparency and human oversight. Producers view compliance as a license-to-operate cost and selectively pilot AI for carbon-footprint reporting, allergen tracking, and yield optimization. Carbon-traceable products command 5-10% premiums in northern supermarkets, motivating exporters to integrate accredited AI systems. While South America and MEA markets trail in absolute spend, infrastructure programs and knowledge-transfer partnerships are laying the groundwork for faster adoption in grains, cocoa, and protein subsectors, ensuring the AI in food & beverages market ultimately scales worldwide.

Competitive Landscape

Competition blends industrial-automation majors, vertical AI specialists, and cloud hyperscalers, fostering a dynamic battlefield where service integration often trumps proprietary algorithms. ABB, Honeywell, and Siemens embed edge AI chips into legacy PLC portfolios, promising seamless migrations for brownfield sites. Startups focus on niche pain points, e-nose freshness sensing or allergen detection, then license APIs to platform players, accelerating feature rollouts.

Strategic alliances are reshaping power balances: Coca-Cola’s long-term cloud deal secures preferential access to Microsoft’s multimodal models, compelling rival beverage groups to negotiate similar partnerships. Patent filings highlight convergence trends; Meta’s work on ultrawide-band food-consumption tracking could interface with retailer loyalty data to personalize nutrition advice, while Coca-Cola’s remote micro-ingredient storage patent signals plans for on-premises flavor customization.

Barriers to entry include domain expertise, validated training datasets, and global service footprints. Integrators able to bundle change management, cybersecurity, and regulatory documentation capture premium fees and consolidate shares. As the leading five suppliers account for roughly 45% of global revenues, the AI in food & beverages market remains moderately concentrated, leaving room for disruptors that can prove ROI in underserved applications such as fermentation monitoring or allergen-free batch scheduling.

AI In Food And Beverages Industry Leaders

TOMRA Sorting Solutions AS

Rockwell Automation Inc.

ABB Ltd

Honeywell International Inc.

Key Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Fresh Blends launched a cloud platform with AI-driven analytics modules DataStudio and Dynamic Pivot.

- April 2025: GrubMarket acquired Delta Fresh Produce, extending its AI-powered supply-chain platform into Mexico.

- June 2025: Tate & Lyle completed its USD 1.8 billion acquisition of CP Kelco, targeting sweetening and fortification synergies.

- April 2024: Level Equity acquired Upshop, an AI retail-software provider.

Global AI In Food And Beverages Market Report Scope

Artificial Intelligence (AI) is a process of making intelligent machines that work and react like humans. The aim is to teach machines to think intelligently, as humans do. The machines have been doing what they were told to do till today. But with AI, machines will think and behave like human beings. The food processing industry is leveraging AI to enhance various offerings, optimize operations, and deliver better customer experience.

The artificial intelligence (AI) in the food and beverage market is segmented by application (food sorting, consumer engagement, quality control, and safety compliance, production and packaging, maintenance, and other applications), end user (hotels and restaurants, the food processing industry, and other end users), and geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa).

The market sizes and forecasts are in terms of value in USD for all the above segments.

| Hardware |

| Software |

| Services |

| Machine Learning |

| Computer Vision |

| Natural Language Processing |

| Robotics and Automation |

| Food Sorting and Grading |

| Quality Control and Safety Compliance |

| Production and Packaging Optimisation |

| Predictive Maintenance |

| Consumer Engagement and Personalisation |

| Quick-service and Cloud Kitchens |

| Inventory and Supply-Chain Planning |

| Other Niche Applications |

| Food Processing Manufacturers |

| Beverage Manufacturers |

| Hotels and Full-service Restaurants |

| Quick-service and Cloud Kitchens |

| Retailers and E-commerce Grocers |

| Others (Catering, Institutional FandB) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Technology | Machine Learning | ||

| Computer Vision | |||

| Natural Language Processing | |||

| Robotics and Automation | |||

| By Application | Food Sorting and Grading | ||

| Quality Control and Safety Compliance | |||

| Production and Packaging Optimisation | |||

| Predictive Maintenance | |||

| Consumer Engagement and Personalisation | |||

| Quick-service and Cloud Kitchens | |||

| Inventory and Supply-Chain Planning | |||

| Other Niche Applications | |||

| By End User | Food Processing Manufacturers | ||

| Beverage Manufacturers | |||

| Hotels and Full-service Restaurants | |||

| Quick-service and Cloud Kitchens | |||

| Retailers and E-commerce Grocers | |||

| Others (Catering, Institutional FandB) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the AI in the food & beverages market?

The market is valued at USD 18.34 billion in 2026 and is projected to reach USD 88.37 billion by 2031, reflecting a 36.96% CAGR.

Which component segment is growing fastest?

Implementation services register the highest growth at a 40.8% CAGR because processors need domain expertise to customize AI models for plant-specific workflows.

Why is predictive maintenance gaining momentum?

Unplanned downtime costs can exceed USD 50,000 per hour; AI-driven predictive maintenance lifts overall equipment effectiveness by 8-12%, delivering quick ROI.

Which region leads adoption?

Asia Pacific holds 33.70% market share and is expanding at 40.25% CAGR, supported by government smart-factory incentives and persistent labor pressures.

How are quick-service restaurants using AI?

QSRs deploy personalization engines that raise average ticket value by 15-20% and autonomous kitchen systems that curb labor costs, driving a 38.95% CAGR in the segment.

What are the main barriers to wider AI adoption in food processing?

High upfront costs, data-ownership concerns, seasonal model drift, and a shortage of AI-literate process engineers remain the principal challenges.

Page last updated on: