Adhesion Promoters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

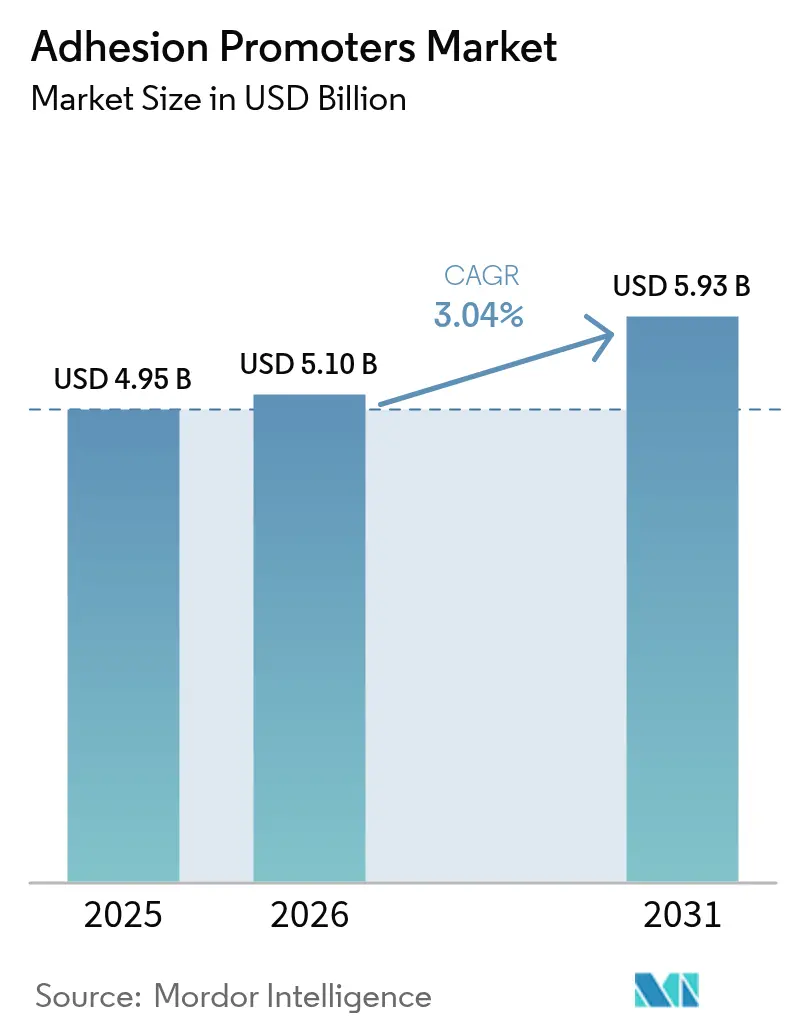

| Market Size (2026) | USD 5.1 Billion |

| Market Size (2031) | USD 5.93 Billion |

| Growth Rate (2026 - 2031) | 3.04% CAGR |

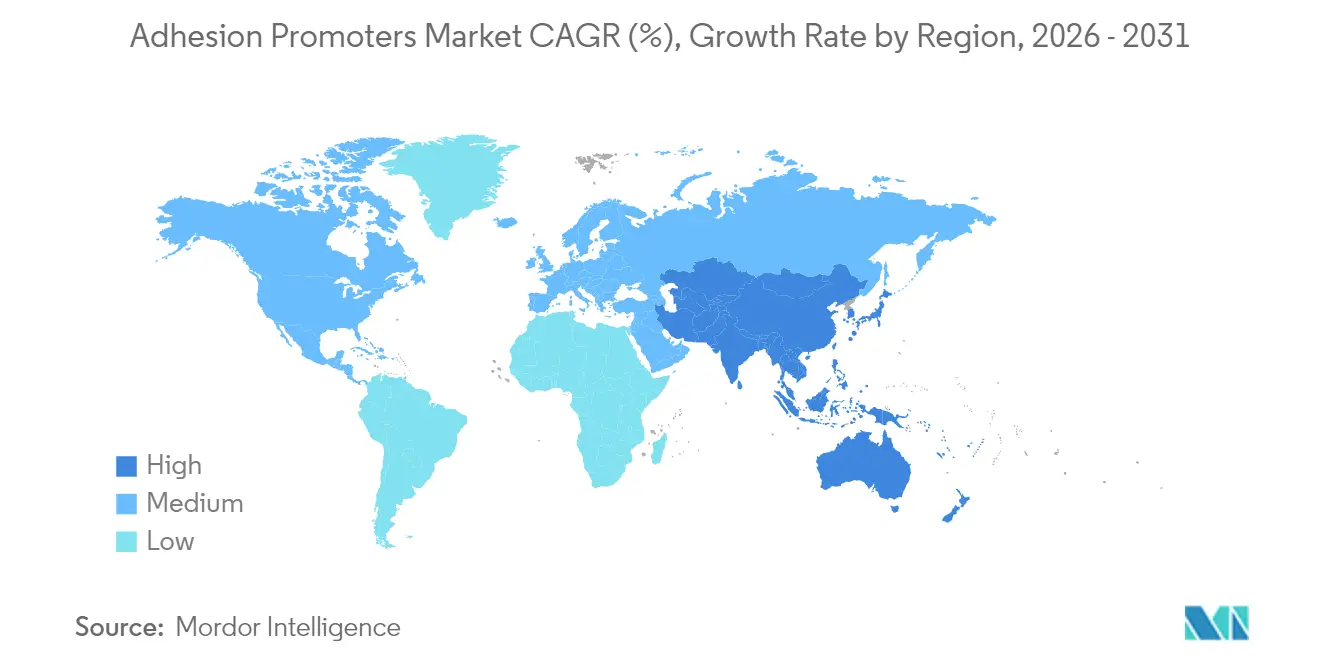

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

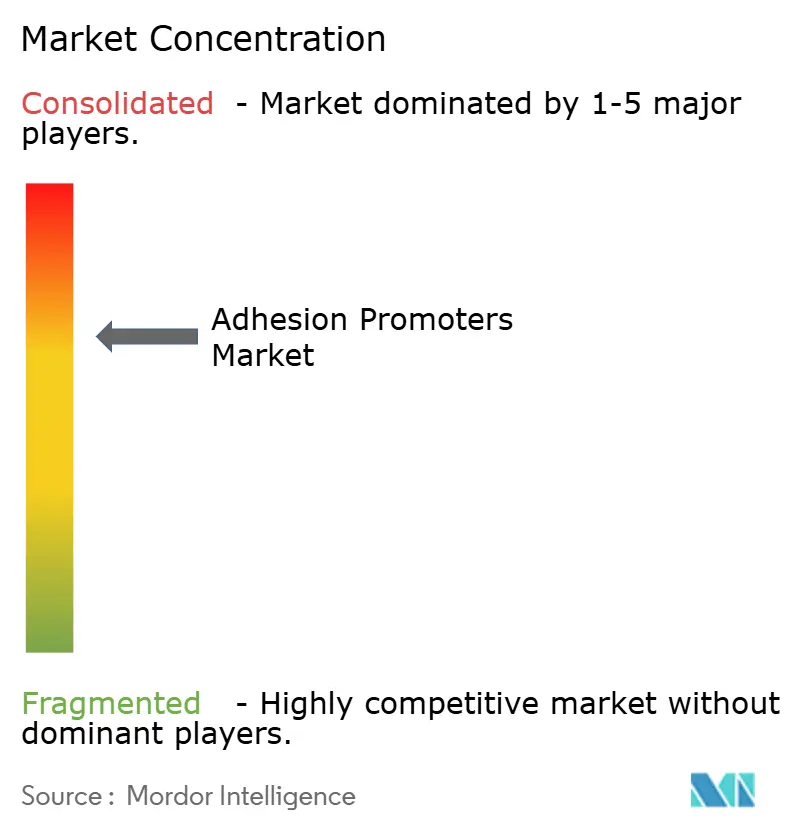

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adhesion Promoters Market Analysis by Mordor Intelligence

The Adhesion Promoters Market size was valued at USD 4.95 billion in 2025 and estimated to grow from USD 5.1 billion in 2026 to reach USD 5.93 billion by 2031, at a CAGR of 3.04% during the forecast period (2026-2031). Moderate expansion reflects a sector moving from rapid adoption to steady replacement demand as regulations tighten and sustainable chemistry gains ground. Investment in automotive lightweighting, relentless electronics miniaturization, and Asia-Pacific’s flourishing flexible-packaging sector continue to anchor revenue. Suppliers with vertically integrated silane capacity are insulated from feedstock swings, positioning them to capture downstream value as electric vehicles multiply. Meanwhile, formulators that can align with stricter VOC thresholds without sacrificing bond strength are securing long-term contracts, particularly in construction and consumer goods. The adhesion promoters market therefore rewards players that pair molecular design expertise with localized production footprints in growth regions.

Key Report Takeaways

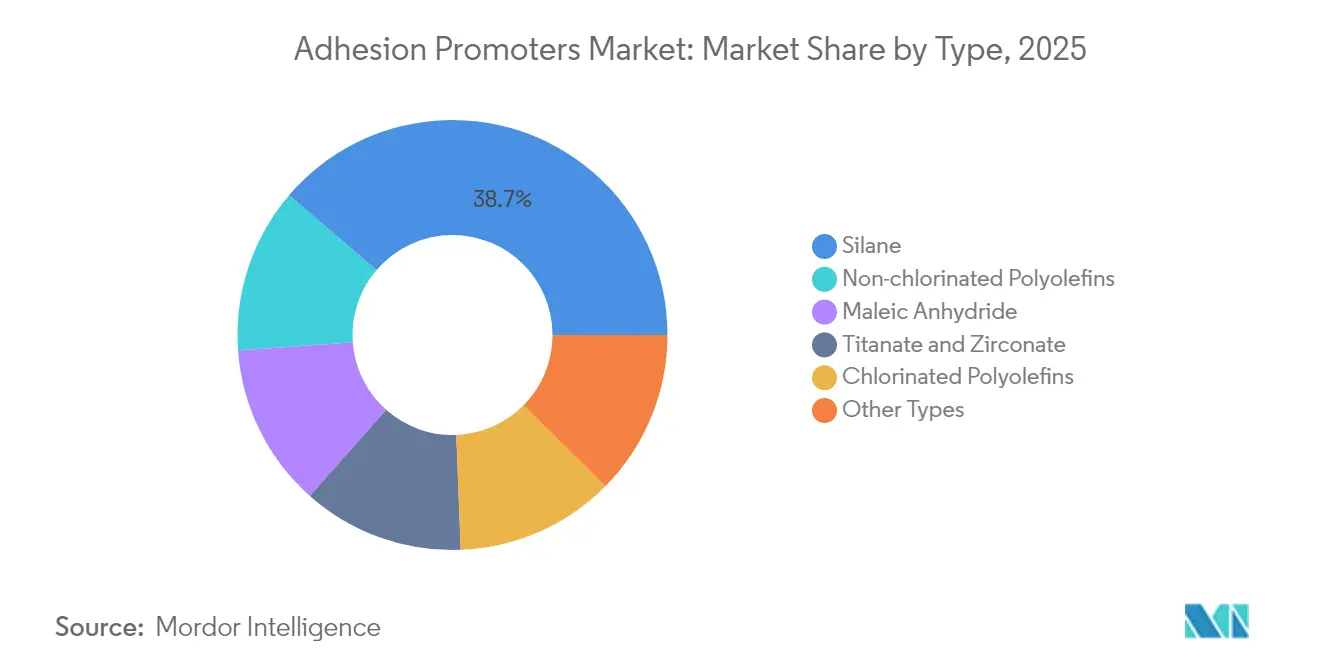

- By type, silane-based variants led with 38.74% revenue share in 2025 and are forecast to advance at a 5.72% CAGR through 2031, reflecting their versatility across organic–inorganic interfaces.

- By application, adhesives are projected to record the fastest 5.28% CAGR through 2031, while paints and coatings retained leadership with 31.52% of adhesion promoters market share in 2025.

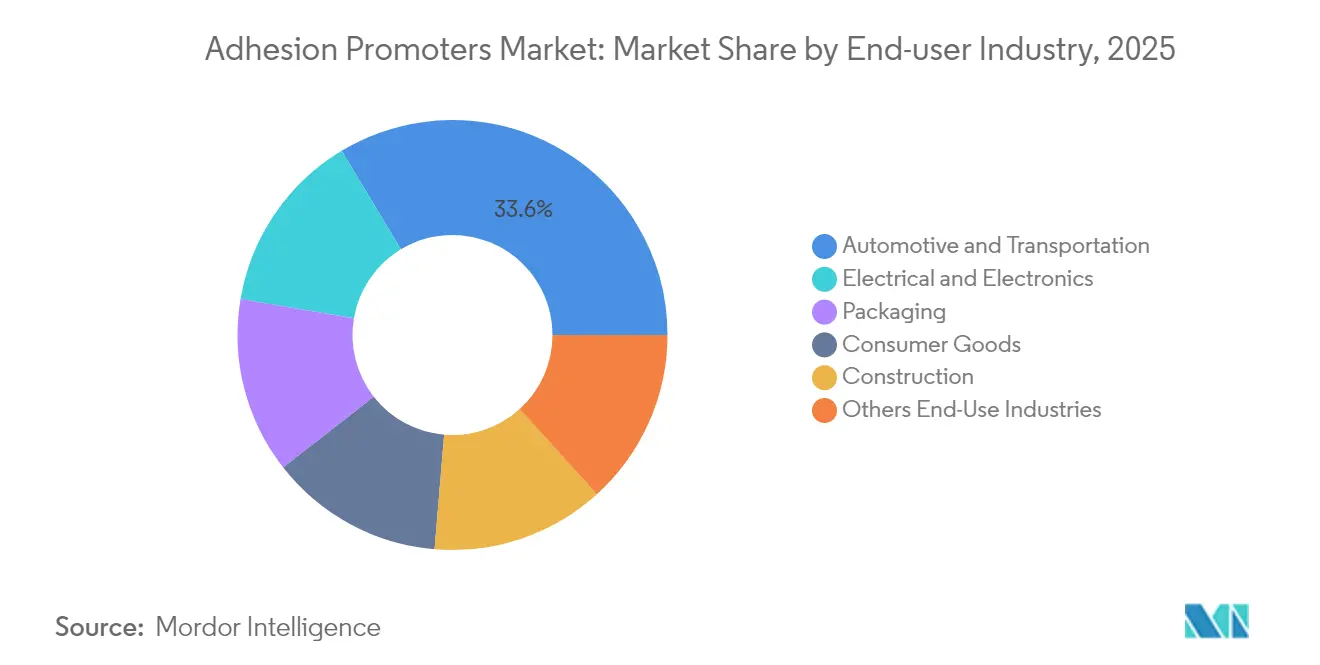

- By end-use industry, automotive and transportation dominated with 33.62% share in 2025; electrical and electronics is poised for the highest 4.54% CAGR to 2031 as battery and semiconductor packaging scale.

- By geography, Asia-Pacific accounted for 46.92% of 2025 revenue and is set to expand at a 4.63% CAGR up to 2031 on the back of packaging converter upgrades and infrastructure build-out.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adhesion Promoters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight automotive plastics & composites | +1.2% | North America, EU, APAC assembly hubs | Medium term (2-4 years) |

| Electronics miniaturization & EV batteries | +0.8% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Expansion of flexible-packaging converters | +0.6% | APAC, rising in Middle East & Africa | Medium term (2-4 years) |

| Shift to silane-based green-tire systems | +0.4% | EU-led global rollout | Long term (≥ 4 years) |

| Climb in electrical & electronics usage | +0.7% | APAC manufacturing corridors, global diffusion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for lightweight automotive plastics and composites

Global vehicle platforms are migrating toward multi-material architectures that combine carbon fiber, glass fiber, aluminum, and high-strength steel. Covalent bonding across such dissimilar substrates hinges on silane, titanate, and zirconate promoters that tolerate thermal cycling beyond 150 °C while curbing galvanic corrosion[1]Sika Automotive, “Lightweight Bonding in Multi-Material Vehicles,” sika.com. Latest formulations enable a 15% curb-weight reduction without compromising crash metrics, directly supporting electric-vehicle range goals. As OEMs localize battery-pack lines, regional sourcing of adhesion promoters becomes a competitive differentiator, particularly in North America where compliance with Inflation Reduction Act content rules shapes supplier selection. The adhesion promoters market therefore embeds itself deeper into the automotive value chain each model year.

Electronics miniaturization and EV battery packaging needs

Foldable displays, camera lens stacks, and system-in-package boards call for ultra-thin adhesive layers able to flex thousands of times while remaining optically clear. Promoters engineered with low glass-transition monomers preserve transparency and suppress yellowing, enabling bezel-free smartphone designs. In parallel, cell-to-pack EV architectures eliminate conventional module walls; specialized promoters now link cells to cooling plates, withstanding −40 °C to 85 °C swings and inhibiting thermal-runaway propagation. These dual pressures speed adoption of thermally conductive, electrically insulating promoter chemistries, expanding the adhesion promoters market across consumer and mobility electronics.

Expansion of flexible packaging converters in Asia

Regional converters have invested in solvent-free laminators and electron-beam curing, both of which demand promoters that create reliable bonds at lower coat weights and cure speeds. Phosphate-ester systems meet tightening migration limits for food contact while maintaining seal integrity in retort pouches[2]Arkema, “Phosphate Ester Promoters for Food Contact,” arkema.com. Higher-barrier structures reduce material thickness by 12%, aligning with e-commerce sustainability targets. Although bio-based promoters still command a 20% premium, brand-owner commitments to recycled content are accelerating pilot runs, broadening the adhesion promoters market footprint among large fast-moving consumer-goods accounts.

Shift to silane-based green-tire formulations

European tire makers are phasing in silane coupling agents that boost silica–rubber affinity, lowering rolling resistance by up to 12% and lifting wet grip scores. Mainstream adoption is underway as capacity from Evonik and Momentive comes online, and similar mandates emerge in Brazil and South Korea. However, smaller regional tire plants lack the specialized mixers needed for precise silane dosing, so promoters packaged as masterbatches are gaining favor. The long-term pull keeps R&D dollars flowing into low-VOC, low-fume silane grades, reinforcing growth prospects for the adhesion promoters market well beyond 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silane & maleic-anhydride prices | -0.9% | Global, acute in APAC sourcing hubs | Short term (≤ 2 years) |

| VOC & halogenated CPO regulatory pressure | -0.6% | North America & EU, expanding into APAC | Medium term (2-4 years) |

| Cost-performance gap in bio-based promoters | -0.3% | Premium markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile silane and maleic-anhydride feedstock prices

Spot silane quotes swung 25% during 2024-2025 as energy-linked inputs and logistical bottlenecks rippled through Chinese producers. Maleic anhydride followed benzene and butane volatility, forcing formulators to renegotiate quarterly contracts. While tier-one suppliers accelerate backward integration, mid-size blenders pass surcharges downstream, eroding adhesive makers’ margins. These dynamics shave nearly 1 percentage point from the adhesion promoters market CAGR until fresh capacity stabilizes supply late in the forecast window.

VOC and halogenated CPO regulatory pressure

California’s 75% VOC cap for aerosolized sealants sparked a wave of reformulation, mirrored by Canadian and Mexican provinces within a year[3]California Air Resources Board, “VOC Regulations for Adhesives and Sealants,” arb.ca.gov. In parallel, EU REACH annex updates flagged certain chlorinated polyolefins, prompting 3M to suspend shipments into Europe. Water-borne promoters and non-halogenated polyolefin analogs answer compliance but suffer moisture sensitivity and slower cure kinetics at high humidity. Dual lines are therefore common: one for legacy markets, another for advanced regulation zones, complicating inventories and lengthening qualification cycles across the adhesion promoters market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silane Dominance Drives Innovation

Silane-based products captured 38.74% of the adhesion promoters market size in 2025 and their 5.72% CAGR through 2031 underscores continued diversification into automotive, tire, and electronics substrates. Hydrolyzable alkoxy groups secure bonds to glass, metal oxides, and silica, while functional organics co-polymerize with epoxies, polyesters, or urethanes. This dual reactivity shortens assembly time and reduces the need for mechanical pretreatment. Next-generation silanes graft pendant imide or epoxy rings, enhancing high-temperature tolerance for battery pack and aerospace components. Maleic-anhydride grafted polyolefins remain indispensable in polypropylene surface modification but grow only where lower cost outweighs chlorinated alternatives. Titanate and zirconate promoters, though niche, win contracts in under-hood applications exceeding 200 °C and in composites cured by autoclave cycles.

Competition now hinges on supply security; Evonik consolidated its silica and silane operations into the Smart Effects business line to synchronize upstream intermediates with customer-specific coupling agents. Smaller formulators are licensing these silanes to develop pre-condensed blends that cut user mixing errors. Environmental scrutiny is steering demand from chlorinated polyolefins toward non-halogenated grades compliant with emerging PFAS limits. As a result, dynamic rebalancing among chemistries will shape the adhesion promoters market across the decade.

By Application: Paints and Coatings Lead Market Penetration

Direct-to-metal coatings rely on adhesion promoters to remove primer steps, saving applicators 20-25% in labor and material costs while elevating salt-spray resistance. The segment held 31.52% revenue in 2025, anchored by architectural projects and automotive refinishing volumes. Bio-derived acrylic monomers introduced by BASF retain cross-link density yet trim fossil-carbon input by 40 %. Packaging coatings, especially for metal cans, integrate promoters that sustain adhesion during 125 °C retort yet withstand caustic recycling washes, a fit demanding phosphate-ester molecules.

Adhesives represent the fastest-rising niche, reaching a 5.28% CAGR as OEMs displace rivets and welds with structural bonding. Here, promoters provide wet-out on oily metal sheets and boost durability under saltwater exposure for marine craft. The adhesion promoters market size for automotive structural adhesives is projected to grow USD 433 million from 2026-2031, supported by platform redesigns toward gigacasting. Rubber-processing promoters linked to silica fillers underpin green-tire output; their penetration promises ancillary demand across footwear and conveyor belting where energy efficiency gains mirror tire benefits.

By End-Use Industry: Automotive Sector Drives Transformation

The automotive and transportation segment accounted for 33.62% share in 2025 and remains pivotal as battery-electric models proliferate. Silane and titanate promoters in crash-resistant structural adhesives align aluminum and carbon-fiber parts that cannot be spot-welded. Battery enclosures require promoters that dissipate heat yet maintain dielectric strength, a specialty now commercialized by global resin majors. Advanced driver-assistance systems also lean on low-shrink optical adhesives whose promoters inhibit delamination of LiDAR windows under UV and thermal cycling.

Electronics manufacturing follows close behind, driven by semiconductor wafer-level packaging that demands copper–polyimide adhesion without surface roughening. Consumer device makers pivot to antimicrobial coatings with built-in promoters that bond to plastic housings, widening the adhesion promoters industry’s scope. In packaging, Asia-Pacific converters’ switch to solvent-free laminates places promoters at the lamination interface to ensure seal integrity after retort sterilization. Construction spending on energy-efficient façades integrates promoters into silicone sealants that tolerate ±50% joint movement while adhering to coated glass, aluminum composite panels, and stone substrates.

Geography Analysis

Asia-Pacific dominated the adhesion promoters market with 46.92% revenue in 2025, propelled by automotive assembly clusters, electronics export bases, and swift urban infrastructure rollout. The region’s flexible-packaging converters are racing to adopt electron-beam curing, a shift that requires promoters with rapid surface migration yet low odor Adhesives Magazine. Government incentives for light-duty EVs in China, India, and Indonesia add further pull, and domestic silane output shields regional buyers from exchange-rate shocks.

North America represents a mature but innovation-heavy arena where regulatory compliance shapes demand. California’s VOC limits accelerated adoption of water-borne promoter systems, and the United States-Mexico-Canada Agreement favors localized chemical supply chains. Electric-pickup launches in Michigan and Texas validate promoters that survive winter freeze-thaw and hot-soak extremes, expanding contract volumes for specialty silicone-modified coupling agents. The adhesion promoters market therefore evolves here through specification upgrades rather than unit-growth spurts.

Europe remains tightly governed by environmental legislation, steering formulators to non-halogenated and bio-based promoters. Automotive green-tire mandates make silane suppliers strategic partners for OEMs chasing CO₂ fleet targets. Retrofit programs under the Renovation Wave initiative further lift consumption in building sealants that embed phosphate-ester promoters for adhesion to new-generation façade claddings. Despite modest GDP growth, the region’s rigorous standards create premium pricing corridors that lift the adhesion promoters market size in revenue terms.

Regulatory Landscape

Regulation for adhesion promoters is shaped primarily by chemical-restriction frameworks and regional air-emissions rules that affect solvents, plasticizers, and halogenated components used in promoter-containing coatings, primers, and adhesive systems. In the European Union, REACH (Regulation (EC) No 1907/2006) and its Annex XVII restrictions, including controls relevant to raw materials used in adhesive and coating formulations such as diisocyanates and certain phthalates, drive reformulation toward lower-hazard and lower-VOC options while increasing documentation requirements for market access.

In the United States, TSCA oversight has tightened for new-chemical submissions, and EPA actions such as the January 2025 final risk evaluation for diisononyl phthalate (DINP) have increased worker-exposure scrutiny for adhesive and sealant spraying scenarios. Air-quality rules in California also anchor compliance priorities: SCAQMD amended Rule 1151 in November 2024 with phased VOC limits and full implementation by January 1, 2028, and it moved toward reactivity-based pathways (PW-MIR), including a March 2026 amendment to Rule 1124 covering aerospace adhesion promoter limits. Together, these developments accelerate adoption of water-borne and non-halogenated promoter technologies while extending qualification and labeling-review cycles across end-use industries.

Value Chain Analysis

The value chain begins with upstream feedstocks and intermediates used to manufacture promoter chemistries, including silane precursors and inputs for maleic-anhydride grafted polymers, titanate/zirconate systems, and chlorinated or non-chlorinated polyolefins. Specialty chemical producers, including global suppliers such as Evonik and Eastman, synthesize neat coupling agents or formulate ready-to-use promoter packages, then supply them directly to large OEM-focused formulators or through distributors into coatings, adhesives, inks, plastics compounding, and rubber processing.

Midstream value is created through application engineering and regulatory support, where suppliers provide formulation guidance, compatibility testing, and compliance documentation for VOC and chemical-management requirements. Downstream, adhesion promoters are incorporated into paints and coatings, structural and assembly adhesives, printing inks, and surface-treatment systems used by automotive and transportation, electrical and electronics, packaging, and construction customers. Recent product activity shows how innovation moves through the chain, including the use of supplier-developed water-based promoters for polyolefins that support TPO/PP coating and ink adhesion, and UV-ink adhesion promoter introductions for metal and composite substrates. Technical service, qualification support, and regional availability therefore remain central to winning specifications.

Competitive Landscape

The adhesion promoters market is moderately consolidated, with top chemical players holding global reach while regional formulators target niche substrates. Evonik's "Smart Effects" integrates silica and silane assets, streamlining filler treatment and coupling chemistry. BASF's acquisition of DOMO Chemicals' adipic-acid assets secures nylon intermediates for high-temperature polyamide bonding. Hybrid organophosphonate promoters dominate technology advancements, offering superior aluminum-bond performance, as reflected in rising patent activity. Companies have been focusing on bio-based tackifiers, reducing adhesive carbon footprints by 25% to align with consumer-packaged-goods brand goals. Smaller innovators leverage nano-silica-functionalized promoters to expand bonded areas without altering viscosity, gaining traction in electronics assembly. Customers increasingly value suppliers combining local technical expertise with global logistics, emphasizing the need for fast service and advanced chemical solutions.

Adhesion Promoters Industry Leaders

Momentive

Evonik Industries AG

DOW

BASF

Wacker Chemie AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is emerging around compliance-driven substitution, where end users replace higher-VOC and halogenated approaches with water-borne and non-chlorinated alternatives while maintaining adhesion on low-surface-energy plastics and performance under humidity and temperature cycling. This can be seen in the continued push toward district-level VOC compliance structures in the United States, including SCAQMD phased VOC limits under Rule 1151 through full implementation by January 1, 2028, and the growing use of reactivity-based PW-MIR pathways, alongside EU REACH-driven pressure on formulations that rely on restricted classes of substances. For suppliers, the clearest path to specification wins is offering drop-in promoter systems supported by documentation and testing for coatings, primers, and adhesive applications being reformulated to meet these rule sets.

Capacity expansion and localization in adjacent bonding-material value pools also create pull-through opportunities for adhesion promoters, particularly as structural adhesives and polyurethane-derived systems scale. In July 2026, Syensqo broke ground on a manufacturing expansion at Havre de Grace, Maryland, to increase capacity for high-performance structural adhesives and surfacing products, and in July 2026 Covestro completed acquisitions of former Vencorex sites in Rayong, Thailand, and Freeport, Texas, to expand HDI-derivatives capacity for adhesives and coatings. These actions add regional formulation and manufacturing activity in systems where adhesion promotion is performance-critical, while increasing expectations around consistent, compliant promoter supply and technical qualification support across North America and Asia-Pacific production corridors.

Recent Industry Developments

- April 2026: Evonik Industries AG launched Ancamine 2875, a modified polyamine epoxy curing agent positioned for ultrafast cure and moisture vapor barrier performance with adhesion to cold and damp concrete. The product targets faster installation and more robust bonding in construction and flooring chemistries where surface conditions often undermine adhesion, reinforcing Evoniks portfolio depth in adhesion-relevant additives.

- March 2025: Evonik Industries AG launched ORTEGOL AP 100, an adhesion promoter for 2K polyurethane systems aimed at improving adhesion to metal and plastics in EV battery potting. By supporting performance in both foamed and compact PU systems, it strengthens supplier positioning in battery-pack encapsulation and related electronics protection applications.

- August 2024: Interface Polymers Ltd expanded its global reach for Polarfin adhesion promoters. The move broadens availability of promoter technology used to improve bonding between dissimilar polymers and other substrates, supporting adoption in packaging and durable goods where multi-material constructions are increasing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers adhesion promoters that are added or applied to help two materials stick better, especially when surfaces are hard to bond. Value is counted as the sales of these promoter chemistries used across industrial and consumer manufacturing.

Scope exclusions: We exclude the value of the main adhesive, coating, or resin system itself unless the promoter is sold and priced as a distinct additive or primer component.

Segmentation Overview

- By Type

- Silane

- Maleic Anhydride

- Titanate and Zirconate

- Chlorinated Polyolefins

- Non-chlorinated Polyolefins

- Other Types

- By Application

- Plastics and Composites

- Paints and Coatings

- Rubber

- Adhesives

- Metal Substrates

- Other Applications

- By End-Use Industry

- Automotive and Transportation

- Electrical and Electronics

- Packaging

- Consumer Goods

- Construction

- Others End-Use Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the adhesion-promoter chemistry and where it is consumed, then matching that usage to measurable industry outputs. We rely on public references such as USGS materials statistics, US International Trade Commission trade data, Eurostat industrial production series, UN Comtrade customs data, and EPA or ECHA regulatory notes for chemical use and restrictions.

To link these signals back to revenue, we also review annual reports, investor presentations, product technical data sheets, and association publications tied to coatings, plastics, composites, and rubber processing. In a few cases, paid subscriptions for company financials and a shipment-level import/export database are used to sanity-check producer presence and trade flows. These sources are not exhaustive, and we also used other public documents for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to confirm what is actually purchased as an adhesion promoter, what is bundled into broader formulations, and how pricing moves with feedstock and performance requirements. We conduct interviews with formulators, raw material suppliers, distributors, and downstream users across APAC, EMEA, and the Americas, then reconcile differences in use rates by end application through follow-up questions when inputs do not align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 26% | EMEA: 29% |

| Smaller Players: 16% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where coatings, plastics and composites, rubber, and metal-treatment activity is reconstructed by region from production and trade indicators, then converted into promoter demand using typical treat rates and application mix. After forming the demand pool, pricing is applied using a practical range of average selling prices that reflects resin type, performance grade, and regional mix, and then totals are rolled up to the global number.

To keep the result grounded, we also run selective bottom-up checks using supplier revenue disclosures where available, channel feedback on volume movements, and sampled price points for common promoter chemistries. Where country visibility is weak, assumptions are bridged from a close proxy market using industrial output and import dependence, then adjusted after interview feedback. For forecasting, we use scenario analysis so growth tracks a small set of observable drivers, such as vehicle production and lightweighting intensity, coatings output, plastic and composite consumption, electronics manufacturing trends, and shifts toward low-VOC and more sustainable formulations.

Data Validation & Update Cycle

Outputs are checked against independent signals such as regional manufacturing indices, trade flows for key precursor families, and visible capacity additions, and then reviewed for outliers that do not match known demand patterns. If a large variance is found, the assumption behind it is revisited and, when needed, respondents are re-contacted to confirm whether the shift is real or a definition mismatch.

Before sign-off, the model goes through a multi-step analyst review so arithmetic, currency conversion timing, and year alignment are consistent across regions. The report is refreshed annually, and interim updates are triggered by material events such as major plant expansions, regulatory changes, or sharp feedstock swings. Right before delivery, we do a last pass to ensure the numbers reflect the latest public data and validated market signals.

Mordor Intelligence's Adhesion Promoters Market Size Compared Against Other Published Estimates

Published market values for adhesion promoters can differ more than buyers expect, even when the topic name looks identical. The main reasons are how each source decides what counts as an adhesion promoter, which year is treated as the base, and how pricing is converted and carried forward.

Some estimates expand the scope to include broader surface-treatment packages or adjacent additives that improve bonding as part of a formulation. In the Mordor Intelligence model, the value is limited to products sold and priced as adhesion promoters or promoter-like primers, and bundled additive value inside a main adhesive or coating is not separately counted unless it is explicitly itemized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.10 B (2026) | |

| Global Consultancy A | USD 5.21 B (2024) | Uses a different base year and applies a faster growth path, and its category discussion leans heavily toward composites and plastics pull-through, which can lift implied penetration and pricing assumptions versus a broader end-use mix. |

| Industry Publisher B | USD 4.44 B (2025) | Starts from a different year and may apply tighter pricing progression across types and forms, and it can also vary by whether promoter demand is counted only as standalone products or partially bundled within application segments. |

Taken together, the spread is mainly explained by year selection, what gets counted as a distinct promoter sale, and how ASP ranges are advanced over time. By tying the model to observable manufacturing outputs and then pressure-testing treat rates and pricing through interviews, we end up with a practical number that can be traced back to clear demand drivers.

Key Questions Answered in the Report

What is the current size of the adhesion promoters market?

The market is valued at USD 5.1 billion in 2026, with expectations to reach USD 5.93 billion by 2031 at a 3.04% CAGR.

Which adhesion promoter chemistry leads global demand?

Silane-based products hold 38.74% of 2025 revenue due to their ability to bond organic polymers to inorganic surfaces.

Why is Asia-Pacific the largest regional market?

High concentrations of electronics manufacturing, automotive assembly, and flexible-packaging conversion give Asia-Pacific 46.92% of global revenue in 2025, with growth supported by infrastructure spending and government incentives.

How are regulations affecting product development?

Stricter VOC limits and halogenated compound restrictions in the United States and European Union are accelerating the shift to water-borne and non-halogenated promoter chemistries.

Which application segment is growing fastest?

Adhesives register the highest projected CAGR at 5.28% through 2031 as industries replace mechanical fasteners with structural bonding solutions that rely on promoters.

Page last updated on: