Flame Retardants For Aerospace Plastics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

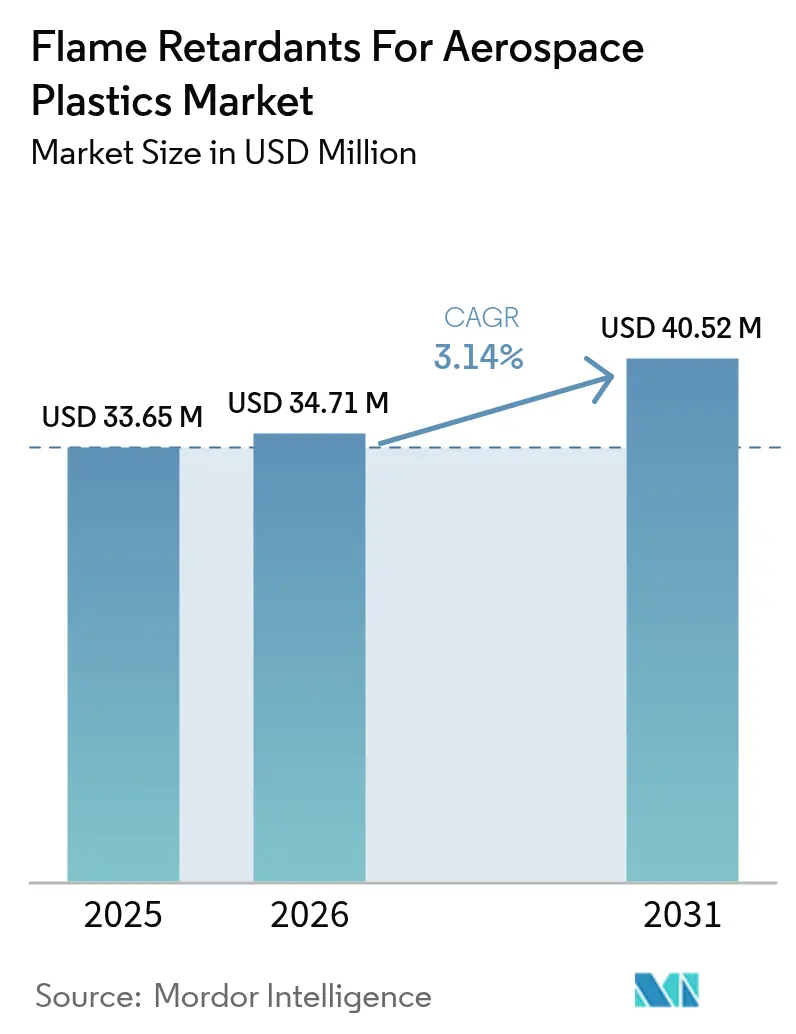

| Market Size (2026) | USD 34.71 Million |

| Market Size (2031) | USD 40.52 Million |

| Growth Rate (2026 - 2031) | 3.14% CAGR |

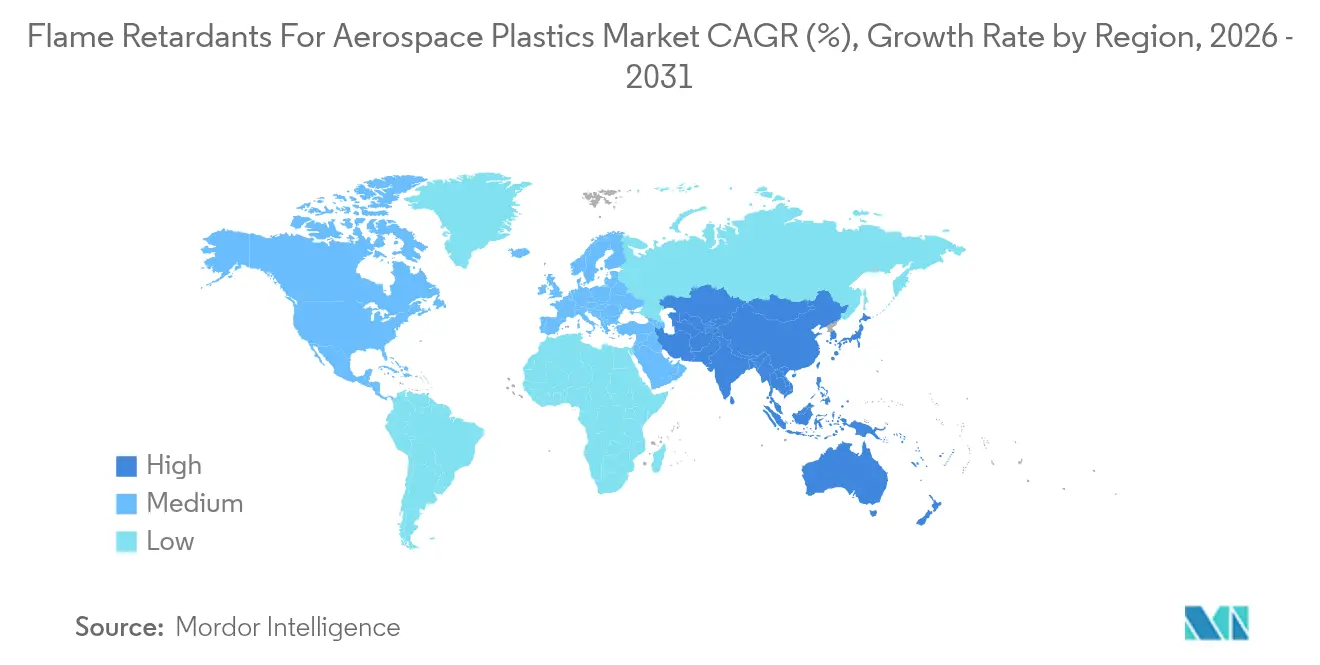

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flame Retardants For Aerospace Plastics Market Analysis by Mordor Intelligence

The Flame Retardants For Aerospace Plastics Market size was valued at USD 33.65 million in 2025 and estimated to grow from USD 34.71 million in 2026 to reach USD 40.52 million by 2031, at a CAGR of 3.14% during the forecast period (2026-2031). Rising aircraft build rates, the phase-out of halogenated systems, and the shift toward lightweight composite airframes underpin demand, yet each new formulation must clear 2–3-year qualification hurdles that moderate near-term volume growth. China’s September 2024 export curbs on antimony trioxide have reset raw-material risk calculations for OEMs, accelerating the search for aluminum trihydrate and phosphorus alternatives even as Boeing lifts 737 output to 38 units per month and stabilizes 787 deliveries at 5 per month. Supply-chain disruption is therefore unfolding simultaneously with production recovery, creating a delicate balance between availability and compliance for the flame retardants for aerospace plastics market. Competitive focus has moved sharply toward halogen-free innovation, with suppliers emphasizing PFAS-free portfolios and closed-loop recycling solutions rather than price concessions.

Key Report Takeaways

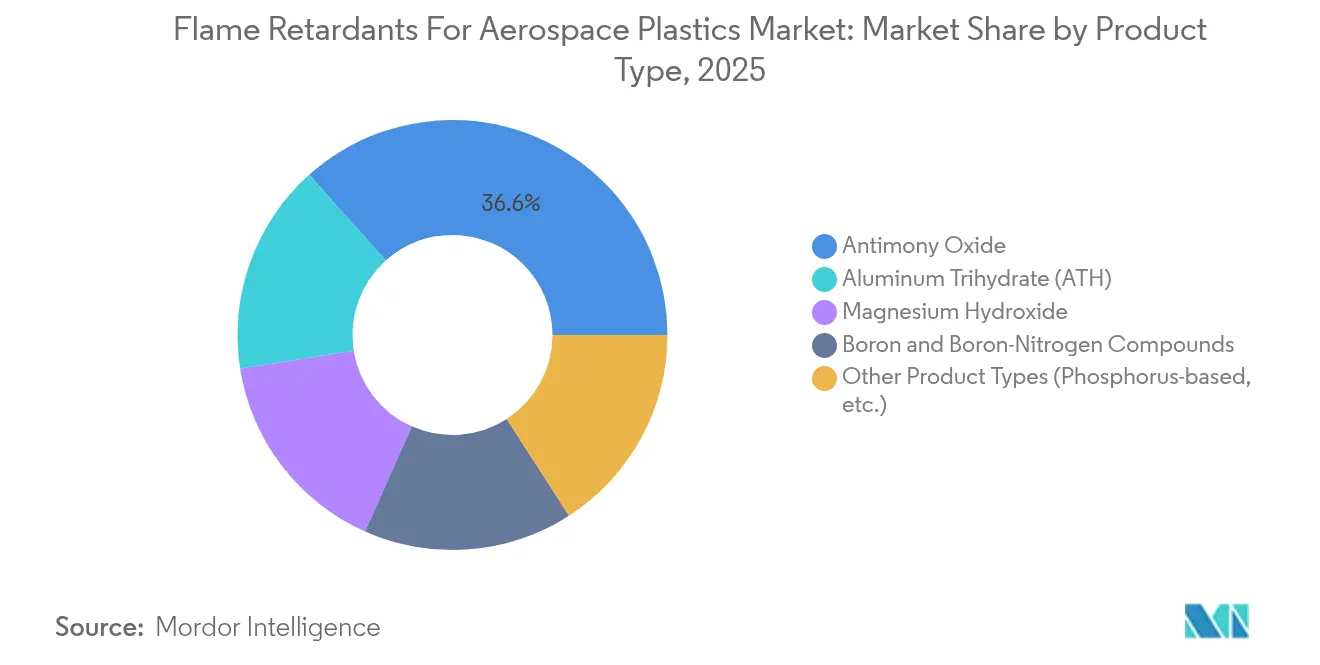

- By product type, antimony oxide led with 36.62% of flame retardants for aerospace plastics market share in 2025, while “other product types,” headed by phosphorus chemistries, are projected to post the fastest 3.99% CAGR to 2031.

- By polymer type, carbon-fiber-reinforced polymer accounted for 40.92% share of the flame retardants for aerospace plastics market size in 2025 and polyether-ether-ketone is advancing at a 4.08% CAGR through 2031.

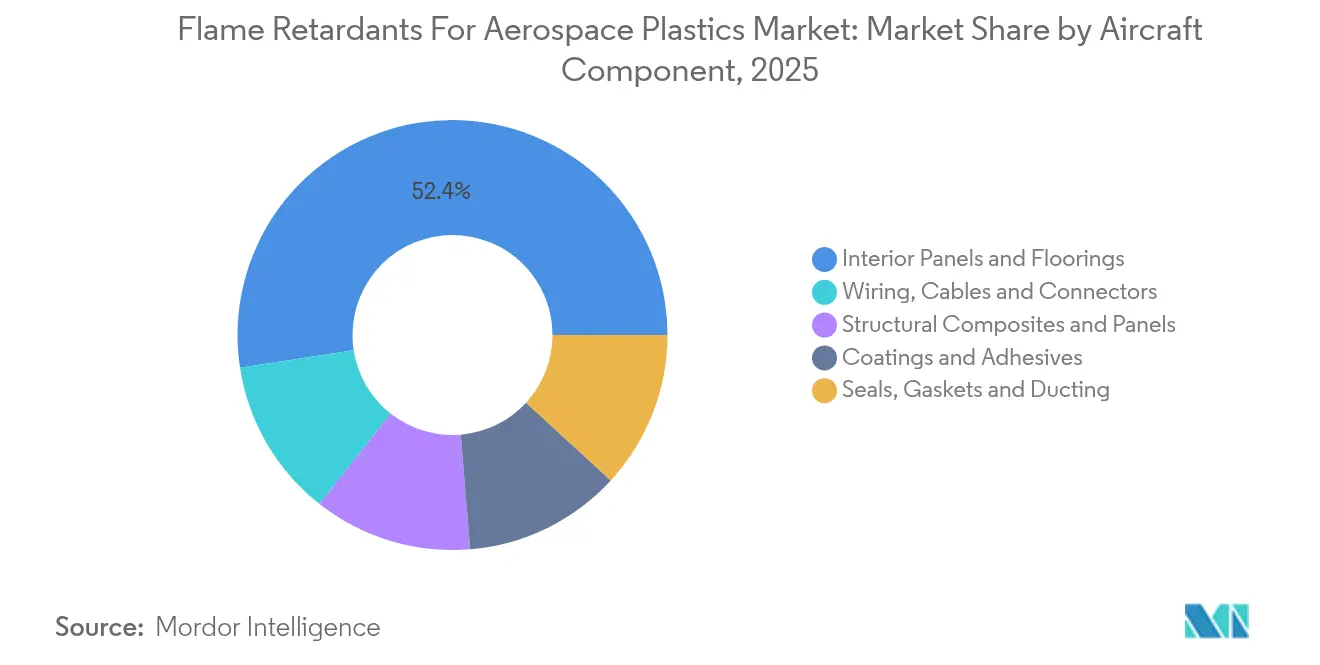

- By aircraft component, interior panels and floorings captured 52.43% of the flame retardants for the aerospace plastics market size in 2025; structural composites and panels are forecast to grow at a 4.44% CAGR to 2031.

- By geography, North America held a 35.28% share of the flame retardants for the aerospace plastics market in 2025, whereas Asia-Pacific records the highest regional CAGR at 3.94% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flame Retardants For Aerospace Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fire-safety regulations for cabin and structural plastics | +0.80% | Global | Long term (≥ 4 years) |

| Rising aircraft production and fleet renewal programmes | +0.70% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Shift toward lightweight non-metallic airframes | +0.50% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Transition to halogen-free flame retardant chemistries | +0.40% | EU & North America core, expanding to APAC | Medium term (2-4 years) |

| Expanded Use of 3D-Printed Aerospace Parts requiring flame retardants | +0.30% | North America & EU early adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Fire-Safety Regulations for Cabin and Structural Plastics

Aviation authorities have tightened material-level tests beyond FAR 25.853. In 2024, the FAA introduced more rigorous heat-release criteria for transport-category aircraft with over 20 seats, while EASA’s 2025 halon-replacement guide requires extinguisher conversion by December 2025, indirectly raising barriers for interior plastics[1]Federal Aviation Administration, “Advisory Circular on Heat Release Rate Testing,” faa.gov . OEMs now design to the most demanding global rule set because regional arbitrage is vanishing. Special conditions tied to novel fuel-tank layouts on aircraft such as the A321neo XLR highlight how new designs can trigger fresh fire-protection clauses. Retrofit mandates on in-service fleets combine with forward-fit requirements, ensuring that the flame retardants for the aerospace plastics market remain buoyed by both legacy and next-generation programs.

Rising Aircraft Production and Fleet Renewal Programmes

Boeing’s backlog of more than 5,600 jets underpins a multi-year production climb, and its Q1 2025 guidance confirms 38 monthly 737 builds while projecting a step-up in 787 output to 7 per month[2]Boeing, “Boeing Reports First Quarter Results 2025,” boeing.com . Each incremental aircraft contains more composite content than the platform it replaces, so flame-retardant consumption grows faster than airframe counts. Fleet-renewal imperatives aimed at fuel savings advance orders for high-composite narrow-body variants, and defense modernisation programs borrow identical chemistries, further expanding addressable volumes. This production-driven pull offsets the certification drag embedded in the flame retardants for the aerospace plastics market.

Shift Toward Lightweight Non-Metallic Airframes

Composite fuselage sections offer 20–30% weight savings versus aluminum, yet demand sophisticated fire performance to maintain cabin survivability. Tests on the 787 show composite skins can limit burn-through without triggering higher toxicity, validating phosphorus-enhanced epoxy matrices that char on exposure. Growth is no longer confined to primary structures; cabin brackets, ducts, and even seat frames are migrating to thermoplastic composites that must still pass vertical Bunsen and smoke density criteria. Suppliers able to embed flame-retardant functionality directly into the polymer backbone enjoy an adoption premium because they avoid post-processing compromises.

Transition to Halogen-Free Flame-Retardant Chemistries

Environmental scrutiny of brominated additives has accelerated EU and US market exits, pushing OEMs toward phosphorus, nitrogen, and metal-hydrate solutions. Clariant completed its PFAS-free portfolio in December 2023, illustrating the commercial value of proactive reformulation. While higher loading levels can downgrade mechanical properties, newer intumescent packages pair ammonium polyphosphate with melamine to match V-0 ratings without halogens. California’s unfolding PFAS bans in consumer markets serve as leading indicators for aerospace, prompting OEMs to lock in future-proof chemistries well ahead of regulation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile antimony-oxide pricing and supply concentration in China | -0.60% | Global, acute impact in North America & EU | Short term (≤ 2 years) |

| Toxicological scrutiny of legacy brominated systems | -0.40% | EU & North America core, expanding globally | Medium term (2-4 years) |

| Avaiability of alternatives like phenolic composites | -0.20% | Global, concentrated in mass transit crossover applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Antimony-Oxide Pricing and Supply Concentration in China

With China supplying around two-thirds of global capacity, the September 2024 export control shattered the security of supply for antimony trioxide, the single largest product segment at 37.28% share. U.S. import dependence exceeds 60%, and replacement sources in Tajikistan or Australia face 18–24-month aerospace qualification windows. Spot prices have jumped 100–200%, compelling OEMs to fast-track aluminum trihydrate and phosphorus systems despite the exhaustive test matrix each new additive must clear. Near-term volatility therefore drags on the flame retardants for the aerospace plastics market until alternative chemistries gain full certification.

Toxicological Scrutiny of Legacy Brominated Systems

Voluntary removal of Deca BDE from North American supply chains signalled the shifting regulatory tide, and REACH continues to re-classify brominated agents as substances of very high concern. As recycling mandates loom, OEMs weigh end-of-life costs alongside fire performance, nudging them toward chemistries with cleaner toxicity profiles. Yet halogen-free packages often demand higher dosage, pressing engineers to safeguard strength-to-weight targets. The uncertain regulatory horizon can pause specification finalisation, slowing immediate uptake in the flame retardants for aerospace plastics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Antimony Oxide Dominance Under Supply Pressure

Antimony oxide commands the largest slice of the flame retardants for the aerospace plastics market at 36.62% in 2025. However, China’s export restrictions have made this leadership fragile, sparking 2-year price swings and spurring OEMs to certify aluminum trihydrate and magnesium hydroxide blends that release water endothermically and promote char at lower smoke toxicity. Other product types, which encapsulate these alternatives plus next-generation phosphorus compounds, are expected to clock a 3.99% CAGR through 2031-the fastest among all categories. Suppliers with broad portfolios capable of bridging the qualification gap are positioned to absorb share as antimony-centric lines confront scarcity. Notably, some organophosphorus compounds that graft onto polymer chains are being adopted because they curb additive migration and therefore prolong in-service fire performance.

The substitution race reshapes procurement hierarchies as OEMs seek single-source partners that can deliver multi-chemistry coverage. Start-ups advancing boron-nitrogen hybrids aim to combine flame suppression with smoke reduction, but certification inertia means incumbent suppliers with aerospace pedigrees still own the buying centre. Consequently, the flame retardants for aerospace plastics market remains an incumbent’s game for now, albeit with clear incentive for diversification.

By Polymer Type: CFRP Leadership Drives Advanced Formulations

Carbon-fiber-reinforced polymers sit atop polymer demand with a 40.92% share, mirroring the aerospace imperative to maximise strength-to-weight ratios. Epoxy matrices in CFRP respond well to phosphorus additives that foster insulating char without degrading interfacial bonding. Polyether-ether-ketone, while smaller in volume, is on track for the highest 4.08% CAGR due to its ability to handle 300 °C service conditions in engine nacelles and hot doors. This thermoplastic shift also dovetails with recyclability targets, prompting suppliers to create flame-retardant packages that survive multiple melt cycles.

Polycarbonate and thermoset polyimide niches keep their foothold through optics and high-temperature resistance, respectively, and each demands custom additive tuning. Because processing temperatures vary from under 200 °C in polycarbonate to more than 400 °C in some high-performance thermoplastics, universal solutions remain elusive, reinforcing the bespoke orientation of the flame retardants for aerospace plastics market.

By Aircraft Component: Interior Applications Lead Structural Growth

Cabin panels and floorings accounted for 52.43% of the 2025 volume, reflecting strict smoke density and toxicity limits in enclosed passenger spaces. Designers now favour halogen-free intumescent coatings that swell under heat, protecting underlying composite laminates while limiting harmful gas evolution. Conversely, structural composites and wing-box panels will post the swiftest 4.44% CAGR as next-gen medium-haul platforms incorporate larger monolithic barrels.

Meanwhile, wiring harnesses, seals, and ducts continue to demand low-corrosivity additives that maintain flexibility. Additive manufacturing opens fresh component classes such as custom air-diffuser grills, all of which must clear vertical flammability and smoke tests. Diversity of applications therefore propels specialist formulating skills, cushioning the flame retardants for aerospace plastics market from commoditisation.

Geography Analysis

North America dominates with a 35.28% 2025 share, anchored by Boeing’s Washington and South Carolina clusters and a robust supplier ecosystem capable of rapid material qualification. FAA advisory circulars offer transparent certification pathways, fostering early adoption of novel additives. Defense budgets layer incremental demand on top of commercial projects, further buttressing regional volumes. The flame retardants for the aerospace plastics market thus enjoy a dual-channel lift across civil and military build rates in the United States.

Asia-Pacific, though smaller, is the quickest-rising at 3.94% CAGR out to 2031. Chinese, Indian, and Japanese OEM programs are localising material supply, incentivising Western suppliers to form joint ventures that meet identical quality thresholds at a lower cost base. Government incentives-from China’s commercial aviation development plan to India’s production-linked schemes-make the region a magnet for new flame retardant manufacturing footprints. End-market growth also stems from regional carriers expanding narrow-body fleets, which translates into higher composite content per airframe and therefore higher additive intensity.

Europe brings environmental stringency to the fore. REACH registration and EASA halon-replacement deadlines are pushing OEMs toward halogen-free and even bio-based solutions, permitting suppliers to price at a premium for compliance assurance. Circular-economy pilots, especially around composite recycling, mean that any new flame retardant package must enable-not obstruct-material recovery. Consequently, European demand skews toward high-value additive systems, providing margin uplift within the global flame retardants for aerospace plastics market.

Competitive Landscape

The field is moderately fragmented yet technologically intensive. BASF, Clariant, and SABIC each lever diversified chemistries and in-house test centres that shorten OEM qualification cycles. Clariant’s PFAS-free rollout in 2023 typifies proactive compliance positioning, gaining favour among European and North American customers wary of future bans. BASF is pushing organophosphorus innovations that covalently bond to polymer matrices to curb out-gassing, while SABIC capitalises on integrated upstream resin production to ensure additive compatibility throughout the supply chain.

Chinese export controls on antimony are triggering strategic partnerships between aircraft OEMs and chemical majors to co-develop hydrates and phosphorus blends. New entrants are exploring bio-based feedstocks, but the mandatory fire, smoke, and toxicity (FST) test matrix creates an entry moat. Additive-manufacturing-compatible powders are emerging as a white-space niche; Evonik’s PA12 launch in November 2024 underscores this direction as 3D-printed air-ducts move from prototype to cabin installation. Price remains a secondary lever because flame retardant cost is marginal relative to total airframe value, leaving technical performance and regulatory assurance as primary differentiators across the flame retardants for aerospace plastics market.

Flame Retardants For Aerospace Plastics Industry Leaders

BASF SE

Clariant

HUBER CORPORATION

LANXESS

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Evonik introduced flame-retardant PA12 and carbon black-infused powders for 3D printing at a Frankfurt trade show. The carbon black powder is an excellent material for manufacturing 3D-printed products intended for outdoor use, particularly suitable for aerospace applications, where resistance to elevated heat and light exposure is essential.

- October 2023: Clariant has officially opened a new facility for its Exolit OP flame retardants in Daya Bay. These flame retardants are instrumental in supporting the rapid growth of engineering plastics applications, particularly in the e-mobility and electrical segments within the transportation industry.

Global Flame Retardants For Aerospace Plastics Market Report Scope

The flame retardants for aerospace plastics market report includes:

| Antimony Oxide |

| Aluminum Trihydrate (ATH) |

| Magnesium Hydroxide |

| Boron and Boron-Nitrogen Compounds |

| Other Product Types (Phosphorus-based, etc.) |

| Carbon-Fibre-Reinforced Polymer (CFRP) |

| Polycarbonate |

| Thermoset Polyimides |

| Polyether-ether-ketone (PEEK) |

| Other Polymer Type (Polyether-ketone-ketone (PEKK), etc.) |

| Interior Panels and Floorings |

| Wiring, Cables and Connectors |

| Structural Composites and Panels |

| Seals, Gaskets and Ducting |

| Coatings and Adhesives |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Antimony Oxide | |

| Aluminum Trihydrate (ATH) | ||

| Magnesium Hydroxide | ||

| Boron and Boron-Nitrogen Compounds | ||

| Other Product Types (Phosphorus-based, etc.) | ||

| By Polymer Type | Carbon-Fibre-Reinforced Polymer (CFRP) | |

| Polycarbonate | ||

| Thermoset Polyimides | ||

| Polyether-ether-ketone (PEEK) | ||

| Other Polymer Type (Polyether-ketone-ketone (PEKK), etc.) | ||

| By Aircraft Component | Interior Panels and Floorings | |

| Wiring, Cables and Connectors | ||

| Structural Composites and Panels | ||

| Seals, Gaskets and Ducting | ||

| Coatings and Adhesives | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the flame retardants for aerospace plastics market?

The market is valued at USD 34.71 million in 2026 and is projected to reach USD 40.52 million by 2031.

Which product type dominates demand?

Antimony oxide leads with 36.62% share, though its future is clouded by Chinese export controls.

Which geographic region is growing fastest?

Asia-Pacific registers the highest 3.94% CAGR through 2031 as China, India, and Japan ramp up aerospace manufacturing.

Why are halogen-free formulations gaining ground?

Stricter environmental rules, especially in Europe and North America, are phasing out brominated additives in favour of phosphorus-, nitrogen-, and metal-hydrate-based solutions.

How will 3D printing affect the flame retardants for aerospace plastics market?

Adoption of additive manufacturing for cabin and replacement parts is opening a niche for specialty flame-retardant powders, expanding demand beyond traditional injection-moulding applications.

What impact do antimony export restrictions have on the market?

China’s controls have doubled spot prices and triggered urgent qualification of aluminum trihydrate and phosphorus alternatives, injecting short-term volatility into supply and pricing.

Page last updated on: