Data Center Generator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.88 Billion |

| Market Size (2031) | USD 9.84 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

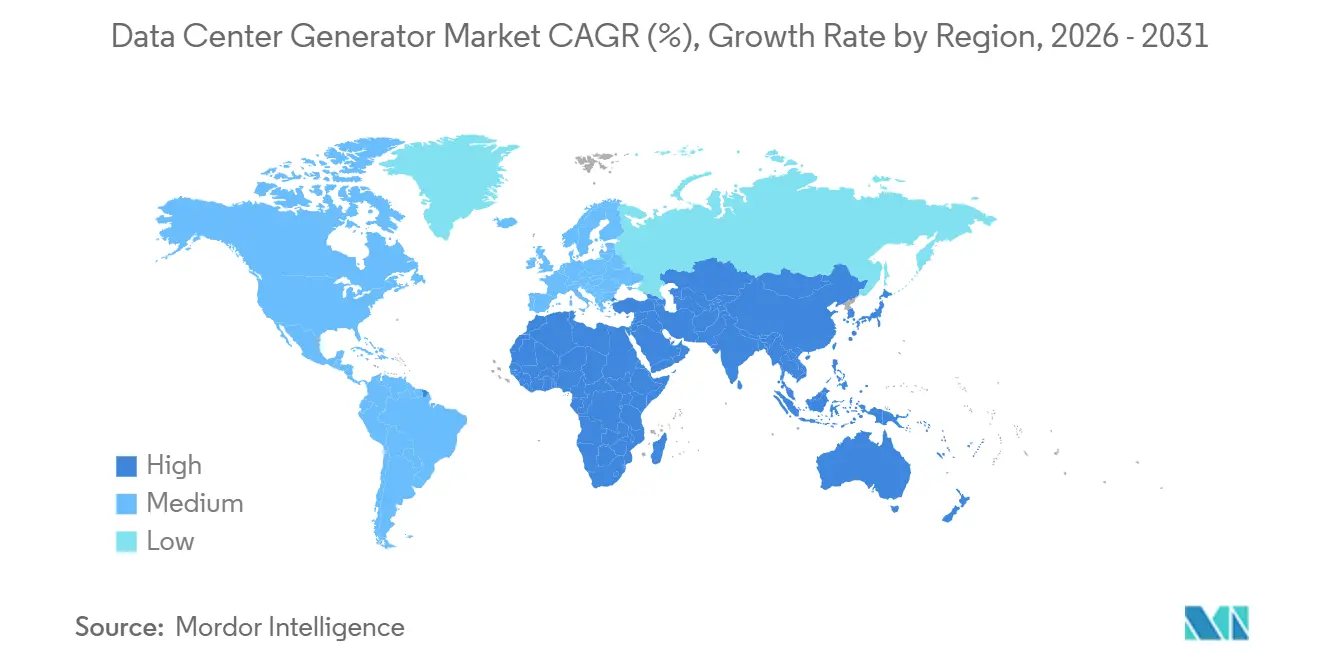

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

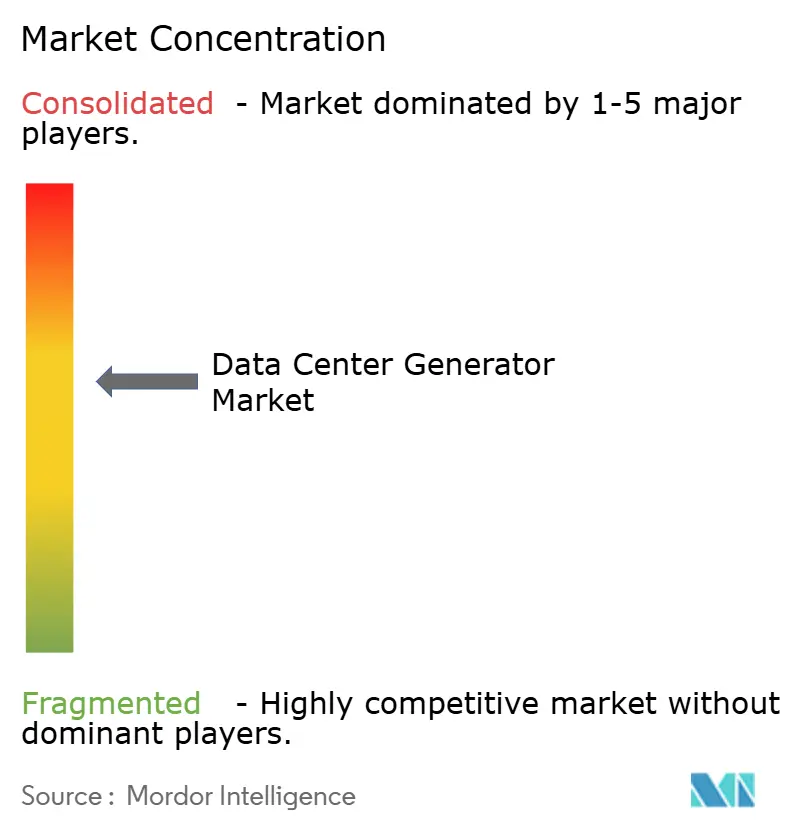

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Center Generator Market Analysis by Mordor Intelligence

The data center generator market size is projected to be USD 7.57 billion in 2025, USD 7.88 billion in 2026, and reach USD 9.84 billion by 2031, growing at a CAGR of 4.55% from 2026 to 2031. Operators are spending on generators not merely to add capacity but to redesign backup-power architecture for AI clusters that can draw up to 100 kilowatts per rack. Fuel flexibility is becoming a core specification as hyperscalers test natural-gas, hydrogen and hydrotreated vegetable-oil blends that satisfy Scope 1 targets without compromising N+1 or 2N redundancy. Edge deployments in emerging markets are favoring factory-integrated diesel blocks that can be staged within nine months, while mature markets are retrofitting legacy fleets with dual-fuel kits to hedge against carbon taxes.

Key Report Takeaways

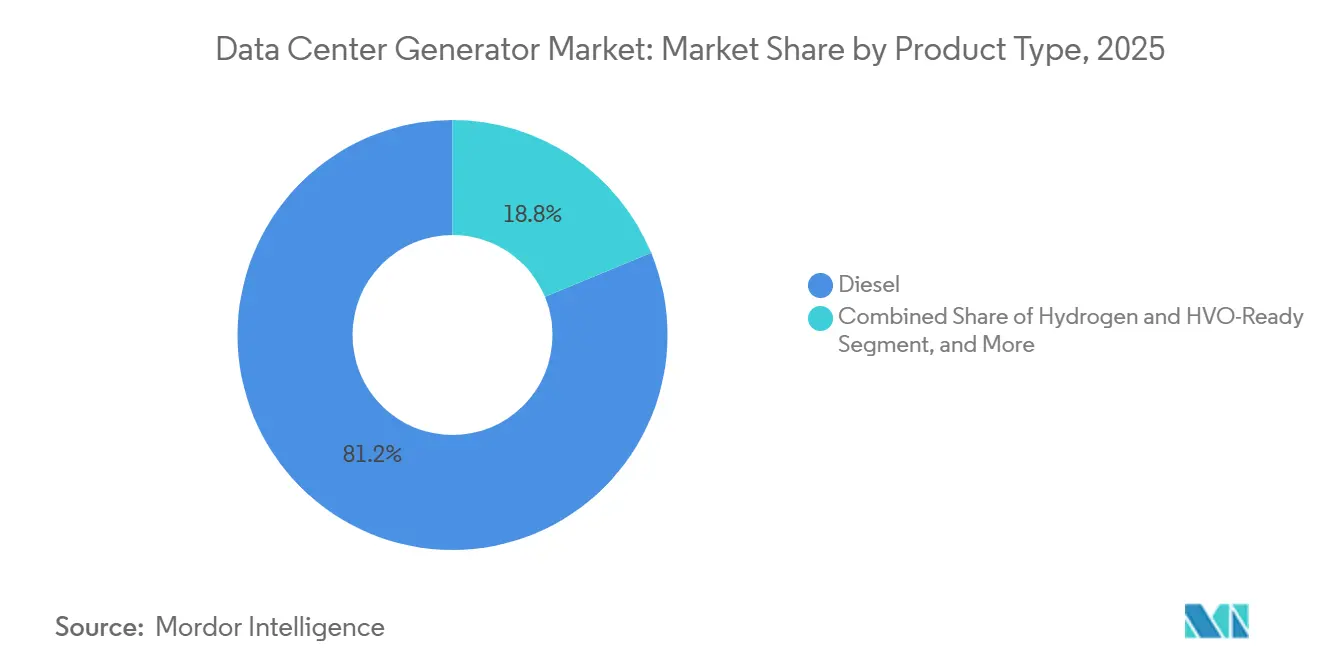

- By product type, diesel gensets led with 81.24% market share in 2025, while the hydrogen- and HVO-ready units segment is projected to post the fastest growth at a 5.22% CAGR through 2031.

- By capacity, sub-1 megawatt generators captured 45.79% of the data center generator market size in 2025, whereas the units above 2 megawatt segment is forecast to expand at a 5.61% CAGR to 2031.

- By tier, tier 3 facilities accounted for 52.86% of market share in 2025, while the tier 4 installations segment is expected to grow at a 5.71% CAGR during the same period.

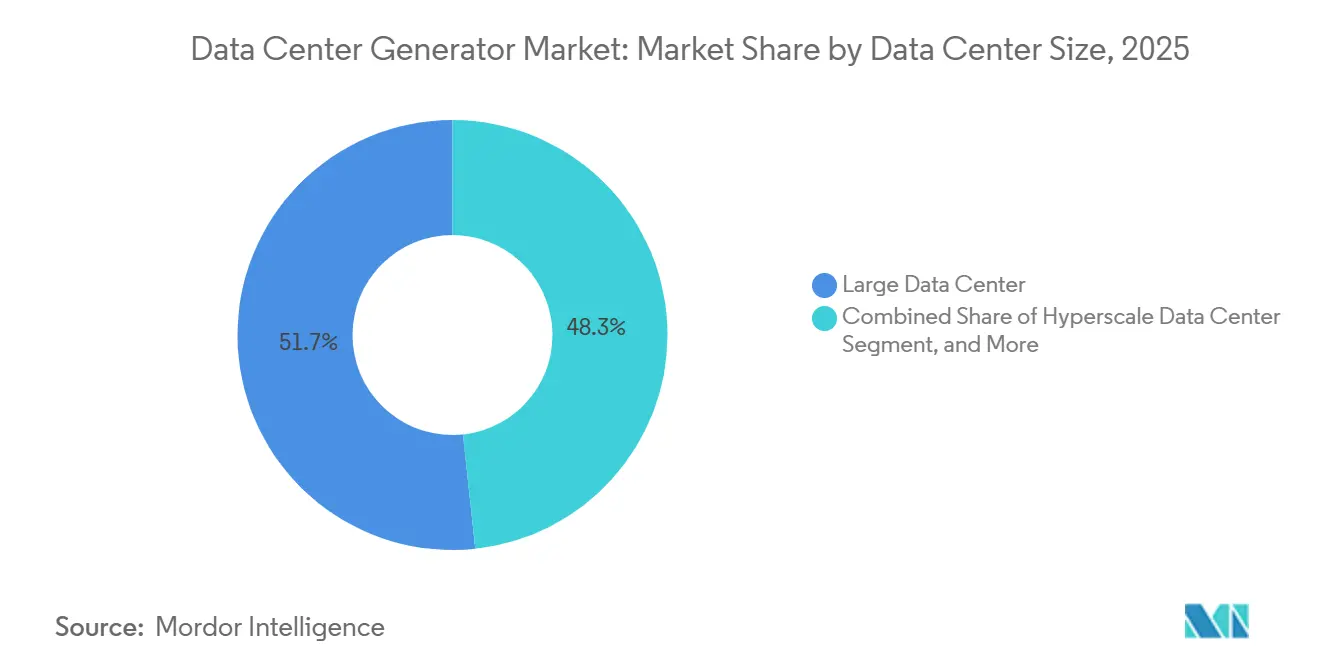

- By data center size, the large data center segment accounted for 51.68% of the market in 2025, yet the hyperscale data center segment is advancing at a 5.46% CAGR through 2031.

- By data-center type, colocation providers held 53.14% of the market share in 2025, whereas the hyperscaler segment is set to climb at a 5.87% CAGR to 2031.

- By geography, North America generated 40.34% of the market share in 2025, but Asia-Pacific is on course for the strongest regional growth with a 6.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Hyperscale and Colocation Build-Out | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Rack-Power Densities from AI Workloads | +1.1% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Expansion of Edge Data Centers in Emerging Markets | +0.9% | Asia-Pacific, Middle East and South America | Long term (≥ 4 years) |

| Transition to Natural-Gas and HVO Gensets for Sustainability | +0.8% | Europe, North America and Middle East | Medium term (2-4 years) |

| Deployment of Trailer-Mounted Temporary Generation Fleets | +0.5% | Global, emphasis on colocation and hyperscale staging | Short term (≤ 2 years) |

| Adoption of Modular Micro-Grid-Ready Generator Blocks | +0.6% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Hyperscale and Colocation Build-Out

Hyperscale operators and colocation providers added more than 2 gigawatts of IT load during 2025, a build-out that translated into multi-megawatt generator procurements across Virginia, Texas and Jakarta. Average lifecycles have stretched from ten to fifteen years, so buyers now demand firmware-upgradable platforms rather than single-fuel machines, allowing them to pivot quickly if carbon pricing changes. Colocation firms are specifying N+2 redundancy, which means three generators per site, a choice that inflates capital outlays by roughly 30% yet lowers insurance premiums. In outage-prone grids such as California, operators earn demand-response income by exporting spare standby capacity during peak events, turning generators into revenue assets. Suppliers that embed microgrid controllers and grid-parallel certifications in the base design capture disproportionate win rates because they shorten commissioning by several weeks.

Rising Rack-Power Densities from AI Workloads

NVIDIA H-series GPUs push rack loads beyond 80 kilowatts, forcing a jump from 208-volt to 480-volt power distribution and raising starting-current requirements for backup sets. A 10-megawatt AI pod now calls for at least 12 megawatts of standby power plus headroom for future nodes, a specification that propels demand for 3-megawatt to 4-megawatt machines. Cummins noted a 23% year-over-year surge in orders above 2 megawatts, with AI campuses absorbing most of the incremental volume.[1]Cummins Inc., "Form 10-K Annual Report 2025," cummins.com/investors Manufacturers are migrating to modular engine blocks that scale from 2 to 4 megawatts, reducing engineering time and spare-parts complexity. This trend also reshapes rental markets as hyperscalers lease temporary 3-megawatt sets during commissioning before permanent power is online.

Expansion of Edge Data Centers in Emerging Markets

Governments in India, Indonesia, and Vietnam subsidize edge facilities sized between 500 kilowatts and 2 megawatts to localize content and support 5G latency targets. These sites rely on diesel generators because pipeline gas infrastructure is sparse, and batteries alone cannot cover hours-long blackouts. Containerized power modules that combine genset, switchgear, and UPS reduce deployment time from six months to six weeks, a critical advantage where real estate leases are short. Rental specialists like Aggreko offer three-year contracts that convert capex into opex, a structure favored by cash-constrained mobile operators. Remote monitoring with satellite backhaul minimizes truck rolls and ensures compliance with warranty terms even in regions lacking skilled technicians.[2]Aggreko Ltd., "Press Releases and Annual Reports," aggreko.com

Transition to Natural-Gas and HVO Gensets for Sustainability

The European Corporate Sustainability Reporting Directive compels disclosure of Scope 1 emissions, accelerating retrofits from diesel to natural-gas or HVO-capable platforms.[3]European Commission, "Corporate Sustainability Reporting Directive," ec.europa.eu Natural-gas sets emit roughly 25% less CO₂ per kilowatt-hour and virtually eliminate particulate matter, easing urban permitting in Frankfurt and London. HVO provides up to 90% lifecycle carbon savings while enabling operators to retain existing diesel infrastructure; its adoption is highest in Scandinavia where supply chains convert waste fats into renewable diesel. Rolls-Royce mtu posted an 18% jump in natural-gas orders during 2025 and now bundles fuel hedging with equipment to lock in total energy cost. As corporate power-purchase agreements add carbon clauses, fuel-flexible gensets become a requirement even for wholesale colocation bids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-Emission Regulations Targeting Diesel Gensets | -0.7% | Europe, North America, Asia-Pacific developed markets | Medium term (2-4 years) |

| Shift Toward Battery and Fuel-Cell Alternatives | -0.6% | Europe, North America | Long term (≥ 4 years) |

| High-Horsepower Engine Supply-Chain Bottlenecks | -0.4% | Global | Short term (≤ 2 years) |

| Urban Permitting Hurdles on Noise and Air Quality | -0.3% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Carbon-Emission Regulations Targeting Diesel Gensets

Tier 4 regulations in the United States and runtime caps in the European Union now add USD 50,000 to USD 100,000 of after-treatment hardware to units above 750 kilowatts. Compliance complexity raises maintenance labor and forces operators to install continuous-emissions monitors, stretching project timelines. Some buyers delay procurement, hoping hydrogen-blended engines will secure future approvals, yet commercial availability is unlikely before 2027. Suppliers must stock multiple exhaust packages per model to address varying local codes, inflating inventory. The uncertainty slows replacement cycles in mature markets and diverts spending toward alternative technologies.

Shift Toward Battery and Fuel-Cell Alternatives

Lithium-ion battery systems now cost near USD 300 per kilowatt-hour installed, making them competitive for Tier 4 sites requiring only minutes of autonomy. They deliver instantaneous power and eliminate the 10-second transfer delay of diesel sets, an advantage for latency-sensitive workloads. Microsoft’s Dublin campus piloted a 3-megawatt fuel-cell array that can run 48 hours on green hydrogen, signaling growing confidence in zero-emission standby solutions. Yet fuel-cell capex remains around USD 1,500 per kilowatt and onsite hydrogen storage complicates safety reviews, so deployment is still selective. Over the next five years, hybrid topologies that pair batteries for ride-through with smaller gensets for extended outages are expected to cannibalize some diesel volume, especially in dense European metros.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fuel Diversification Redefines Performance Economics

Diesel platforms retained 81.24% of the market share in 2025 because operators trust their field-proven performance and global fuel logistics, anchoring the data center generator market even as sustainability targets tighten. Natural-gas sets flourish where pipeline connectivity exists, allowing owners to tap lower fuel costs that run 30% to 40% under diesel equivalents. The hydrogen and HVO-capable machines segment is expanding at a 5.22% CAGR as suppliers release dual-fuel engines that toggle between diesel, gas, and renewable blends without mechanical changes, a design that lowers stranded-asset risk. Kohler’s KD-Series, introduced in late 2025, can operate on pure HVO, a capability aimed at northern Europe, where renewable diesel supplies are robust. Operators increasingly buy platforms that accept multiple fuels because they provide a hedge against future carbon taxes and supply disruptions, even at a 10% to 15% price premium over single-fuel sets.

Regional adoption is uneven. North America and Europe dominate natural-gas orders due to extensive pipeline grids and stringent particulate limits. Asia-Pacific and the Middle East continue to depend on diesel, given limited gas distribution and lower fuel substitution incentives, yet pilot projects using local biofuels signal a gradual change. Manufacturers now couple each sale with software that optimizes blend ratios in real time, integrating emissions targets, spot fuel pricing and grid carbon intensity. Generac’s GridLink controller, launched in 2026, retrofits legacy fleets, extending asset life and reducing capex pressure. As a result, fuel flexibility rather than engine displacement is fast becoming the primary purchase criterion in the data center generator market.

By Capacity: Demand Polarizes Between Sub-1-Megawatt and Multi-Megawatt Classes

Sub-1 megawatt machines captured 45.79% of the market share in 2025, catering to edge, enterprise and branch-office sites that rarely exceed 500 kilowatts. Their compact footprint allows indoor placement in urban buildings where external yards are costly or impossible. Mid-range 1 to 2 megawatt sets remain a staple for regional colocation halls that need N+1 redundancy without the structural reinforcements large units require. Meanwhile, the generators above 2 megawatt segment is growing at a 5.61% CAGR because hyperscalers are consolidating vast AI workloads into fewer locations, prompting orders for 3-megawatt to 4-megawatt models that minimize cabling loss and switchgear cost.

Regulatory thresholds also influence sizing. Many jurisdictions impose stricter environmental impact reviews on units above 2 megawatts, so owners sometimes parallel multiple smaller machines to dodge lengthy permitting. Yet AI workloads are reversing that logic; fewer, larger engines simplify paralleling logic, reduce inrush current coordination challenges, and optimize cooling airflows. Cummins’ QSK95, a 3.5 megawatt flagship, doubled its share of the data center generator market size for capacities over 2 megawatts within one year. Rental fleets mirror the trend, with Aggreko adding 150 trailer-mounted units between 1 and 3 megawatts in 2025 to serve campus-scale construction phases.

By Tier Type: Elevated Redundancy Expectations Lift Tier 4 Adoptions

Tier 3 sites retained 52.86% of share in 2025 because they balance 99.982% uptime with tolerable capex profiles, suiting retail colocation clientele. Operators typically deploy two independent gensets, each capable of the full IT load, enabling maintenance without shutdown. The tier 4 facilities segment is expanding at a 5.71% CAGR because banks, healthcare networks, and AI cloud operators now require 99.995% uptime, compelling 2N or 2(N+1) architectures that double generator count. Insurance premiums for non-redundant sites are rising, so even mid-market colocation firms upgrade to Tier 4 to capture higher rack rates and avoid liability.

Moving from Tier 3 to Tier 4 also reshapes service models. Predictive analytics platforms continuously watch bearing vibration, exhaust temperature, and fuel quality to catch failures before they break redundant boundaries. Rolls-Royce’s flywheel-integrated Kinetic PowerPack eliminates transfer delay, appealing to high-frequency trading halls that cannot accept even a short-term UPS ride. Tier 1 and Tier 2 sites, limited to development labs and disaster-recovery bunkers, now account for a shrinking portion of the data center generator market, reflecting the accelerating migration of casual workloads to public cloud.

By Data Center Size: Hyperscale Campuses Command Incremental Capital

Large facilities captured 51.68% of the market share in 2025 because they serve a mixed customer base of enterprise, SaaS, and content players. Small facilities under 5 megawatts still populate dense metro cores where land and transmission capacity are scarce, but their share is slipping as cloud migration consolidates spend. The hyperscale data center segment is advancing at a 5.46% CAGR as Meta, AWS, and Google roll out 100-megawatt-plus buildings in Vienna, Osaka, and Manassas. Such sites require entire generator villages, sometimes exceeding 150 units, and therefore draw suppliers into multiyear framework agreements.

Clustered development in Loudoun County and Phoenix spurs community backlash over noise and air quality, prompting owners to specify silencers and catalyst systems from day one. Hyperscale operators also negotiate wholesale gas contracts or build on-site LNG storage to cap fuel volatility. In Brazil and Saudi Arabia, sovereign funds co-finance hyperscale parks, bundling renewable energy plants that lower effective carbon intensity. That collaboration accelerates generator procurement by enabling public entities to fast-track permitting, compressing timelines that would otherwise stretch over 18 months.

By Data Center Type: Colocation Incumbents Face Hyperscaler Competition

Colocation facilities held 53.14% of the market share in 2025 because multi-tenant halls rely on backup power to honor service-level agreements and retain customers. Equinix and Digital Realty operate hundreds of sites, each requiring standardized generator specs to simplify spares and training. Hyperscalers and cloud-service segment is growing at a 5.87% CAGR because vertical integration lets them optimize fuel, cooling, and microgrid export in ways multi-tenant operators cannot match. Google's Council Bluffs campus captures waste heat from natural-gas gensets for office heating, cutting overall energy use by 12%. Enterprise and edge data centers, serving single tenants or local workloads, round out the segment with smaller average capacity and higher price sensitivity.

Colocation providers are adopting hyperscaler practices by signing long-term service contracts that bundle preventive maintenance, fuel hedging, and emissions offsets. That bundling reduces operational risk and aligns with customer ESG reporting needs. Hyperscalers specify custom configurations, including remote-start controllers and grid-export inverters, which differentiate their offerings from retail colocation. As a result, the data center generator industry is bifurcating into standardized multi-tenant products and bespoke hyperscale platforms, each with distinct supply chains and margin profiles.

Geography Analysis

North America accounted for 40.34% of the market share in 2025, driven by Virginia, Texas and Oregon, where hyperscale operators and colocation providers benefit from low power costs and streamlined interconnection rules. AWS disclosed a CAD 4.5 billion (USD 3.3 billion) expansion in Calgary, including 45 megawatts of backup generation, signaling Canada's emergence as a diversification hub. Mexico is attracting nearshoring-linked data-center projects, though grid reliability gaps and limited pipeline gas slow adoption of natural-gas gensets. The region's mature colocation base and aggressive AI build-out sustain robust demand, yet urban noise ordinances in Los Angeles and New York are pushing operators toward battery hybrids and enclosed acoustic sets.

Asia-Pacific is forecast to advance at a 6.09% CAGR through 2031 as India, Indonesia, Vietnam and the Philippines offer tax holidays and expedited environmental approvals for digital infrastructure. India's Ministry of Electronics and Information Technology granted data centers critical-infrastructure status, unlocking priority power allocations and accelerating permitting. China's state-owned cloud providers deploy thousands of megawatts annually, yet foreign suppliers face local-content mandates that favor domestic engine manufacturers. Japan and South Korea, with high electricity prices and strict emissions codes, favor natural-gas and battery systems over diesel. Australia's Sydney and Melbourne markets grow steadily, though renewable-energy targets are encouraging solar-plus-battery configurations that reduce reliance on combustion backup.

Europe's data center generator market size is fragmented across national jurisdictions, each imposing distinct noise limits, runtime caps and fuel standards. The United Kingdom, Germany, France and the Netherlands anchor demand, with London and Frankfurt serving as financial-services hubs that require Tier 4 uptime. The Industrial Emissions Directive restricts urban diesel runtime to 50 hours annually unless continuous monitors are installed, a rule that accelerates natural-gas and HVO adoption. Italy and Spain offer lower power costs and renewable incentives, yet permitting delays and grid congestion constrain growth. The Middle East is witnessing sovereign investment in hyperscale campuses; Saudi Arabia's Public Investment Fund committed USD 6.4 billion to three facilities in Riyadh, Jeddah and Dammam, each needing 40 to 80 megawatts of standby power. Africa remains nascent, with South Africa leading installed capacity, while Nigeria, Kenya and Egypt deploy edge sites to support mobile broadband. South America concentrates in Brazil, where Ascenty and Odata expand colocation to serve local enterprises and hyperscalers navigating data-residency laws; Chile and Colombia are emerging as secondary markets, offering stable politics and renewable resources, though seismic risk and fiber scarcity pose challenges.

Competitive Landscape

The market is moderately concentrated with suppliers such as Caterpillar, Cummins, Generac, Rolls-Royce mtu, Kohler, and others, leaving regional specialists and rental providers ample room to capture niche segments such as trailer-mounted fleets and micro-grid-ready modules. Competition centers on fuel flexibility, lead-time compression, and total cost of ownership rather than upfront price, because operators now model 15-year fuel spend, carbon pricing, and grid export revenue. Caterpillar and Cummins dominate the high-horsepower segment above 2 megawatts by cross-selling from mining, marine, and industrial applications, while Generac and Kohler focus on sub-1-megawatt units serving enterprise and edge deployments. Rolls-Royce MTU has carved a premium position with flywheel-battery hybrids that eliminate transfer delays, appealing to Tier 4 operators unwilling to deploy full 2N generator redundancy.

White-space opportunities are emerging in pre-integrated modular systems that combine generation, switchgear and cooling in ISO containers, microgrid controllers enabling island-mode or grid-export operation, and predictive-maintenance platforms using machine learning to forecast component failures. Atlas Copco filed a patent in 2024 for a containerized genset with integrated thermal storage that captures waste heat during testing and discharges it during outages, extending runtime without extra fuel. Fuel-cell suppliers like Bloom Energy and battery integrators like Fluence position their products as drop-in replacements for diesel sets in applications requiring under four hours of runtime. Software-defined power management is creating opportunities for Schneider Electric and Eaton, which offer cloud platforms that aggregate telemetry from gensets, UPS and grid interconnections, enabling real-time fuel and emissions optimization.

Cummins announced a USD 150 million expansion of its Fridley, Minnesota, facility in February 2026 to boost QSK95 output by 30%, addressing 18-month lead times for high-horsepower units. Rolls-Royce mtu secured a 72-megawatt natural-gas contract for a Frankfurt hyperscale campus in January 2026, integrating microgrid control that exports power during peak demand. Generac launched its EcoGen HVO series in December 2025, targeting European colocation providers seeking Scope 1 reductions. Caterpillar completed an USD 85 million acquisition of Weichai Baudouin's European distribution network in November 2025, expanding service reach in France, Germany and the United Kingdom. These moves illustrate how incumbents are investing in localized production, fuel-flexible platforms and service density to defend share against emerging disruptors.

Data Center Generator Industry Leaders

-

Caterpillar Inc.

-

Atlas Copco AB

-

Cummins Inc.

-

Himoinsa SL

-

HITEC Power Protection BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cummins confirmed a USD 150 million capacity expansion at its Minnesota plant to boost production of 3 MW–4 MW QSK95 gensets.

- January 2026: Rolls-Royce mtu won a 72 MW natural-gas genset order for a hyperscale campus in Frankfurt, integrating a microgrid controller for grid-export capability.

- December 2025: Generac launched its EcoGen HVO series (500 kW–2 MW) that operates on 100% hydrotreated vegetable oil without engine modifications.

- December 2025: Caterpillar acquired Weichai Baudouin’s European distribution network for USD 85 million, adding 12 service centers focused on data-center power.

Global Data Center Generator Market Report Scope

DC Generators are the backup power supply reservoirs for the data centers during a power break. A total power cut-off from a data center may need a complete restart for the system. This may lead to system downtime, start-up issues, and current/ongoing information damage. Thus, the generators constantly support data centers with a backup power supply to evade such irregularities and failures.

The Data Center Generator Market Report is Segmented by Product Type (Diesel, Natural Gas, Hydrogen and HVO-Ready, and Other Product Types), Capacity (Less than 1 MW, 1-2 MW, and Greater than 2 MW), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Diesel |

| Natural Gas |

| Hydrogen and HVO-Ready |

| Other Product Types |

| Less than 1 MW |

| 1 - 2 MW |

| Greater than 2 MW |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Diesel | ||

| Natural Gas | |||

| Hydrogen and HVO-Ready | |||

| Other Product Types | |||

| By Capacity | Less than 1 MW | ||

| 1 - 2 MW | |||

| Greater than 2 MW | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Size | Small Data Center | ||

| Medium Data Center | |||

| Large Data Center | |||

| Hyperscale Data Center | |||

| By Data Center Type | Colocation Data Center | ||

| Hyperscalers Data Center/CSPs | |||

| Enterprise and Edge Data Center | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of this market by 2031?

The market is expected to reach USD 9.84 billion by 2031, expanding at a 4.55% CAGR from 2026 to 2031, driven by hyperscale AI clusters and edge proliferation.

Which fuel type holds the largest share?

Diesel gensets commanded 81.24% of the market share in 2025, yet hydrogen and HVO-ready units segment is growing fastest at 5.22% annually as operators seek Scope 1 emission reductions.

How are AI workloads influencing generator specifications?

AI training clusters can draw 100 kilowatts per rack, requiring gensets above 2 megawatts to handle inrush current and provide expansion headroom, accelerating demand for multi-megawatt platforms.

Why are Tier 4 facilities expanding faster than Tier 3?

Tier 4 sites demand 2N redundancy for 99.995% uptime, appealing to financial-services and cloud operators that cannot tolerate brief outages, and they command rental premiums of 20% to 30%.

Which region is growing most rapidly?

Asia-Pacific is forecast to expand at 6.09% through 2031 as India, Indonesia and Vietnam offer tax incentives and fast-track permitting for digital infrastructure.

What alternatives are challenging diesel gensets?

Lithium-ion batteries now cost near USD 300 per kilowatt-hour and deliver instantaneous power, while fuel cells offer zero local emissions, both appealing in urban markets with strict runtime caps.

Page last updated on: