Oman Aquaculture Market Analysis by Mordor Intelligence

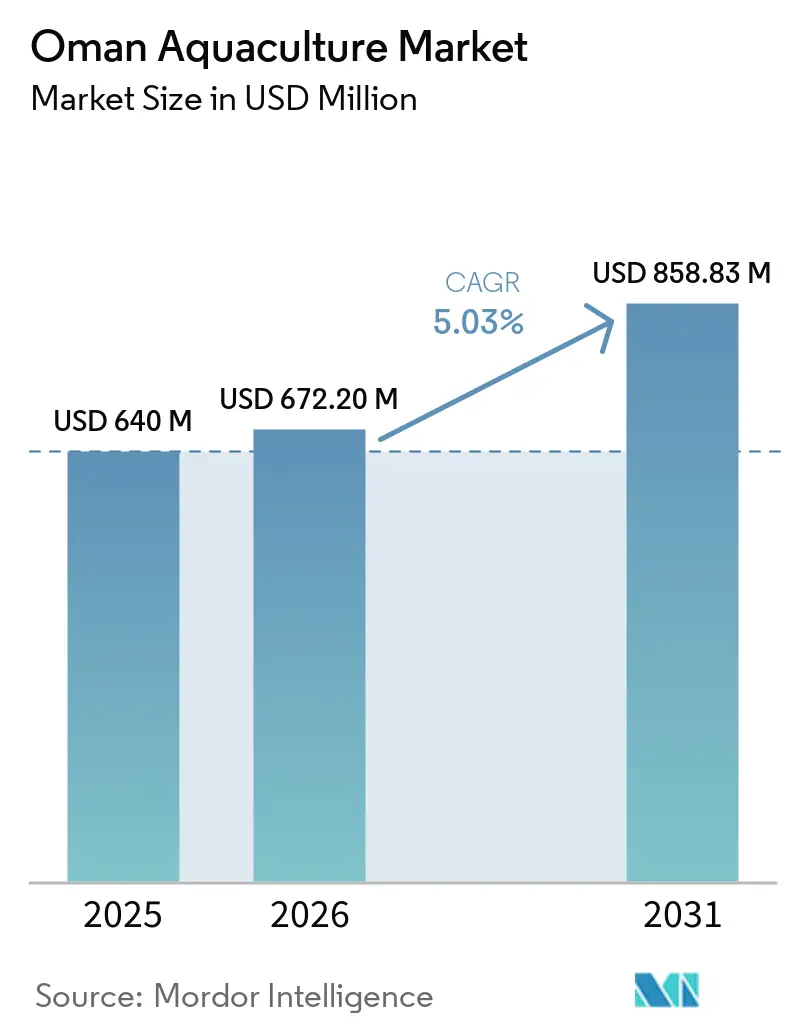

The Oman aquaculture market size is projected to expand from USD 640.0 million in 2025 and USD 672.2 million in 2026 to USD 858.8 million by 2031, registering a CAGR of 5.03% between 2026 and 2031. The Oman aquaculture market is advancing on the back of policy-led expansion, with food security, export diversification, and project facilitation now closely tied to national development priorities under Vision 2040. This policy support is being reinforced by structured investor outreach, long-tenure industrial incentives in Duqm, and financing channels that lower the entry barrier for new farms and processing assets. The Oman aquaculture market is also driven from a stronger export profile, as producers align with certification, traceability, and processing standards required in the European Union, China, the Republic of Korea, and other premium destinations. Competition remains moderate, but scale is shifting toward operators that can combine farming, hatchery control, feed access, and downstream processing into a single operating model. At the same time, disease exposure, imported input dependence, and climate-linked coastal risks continue to shape the pace and quality of expansion across the Oman aquaculture market.

Key Report Takeaways

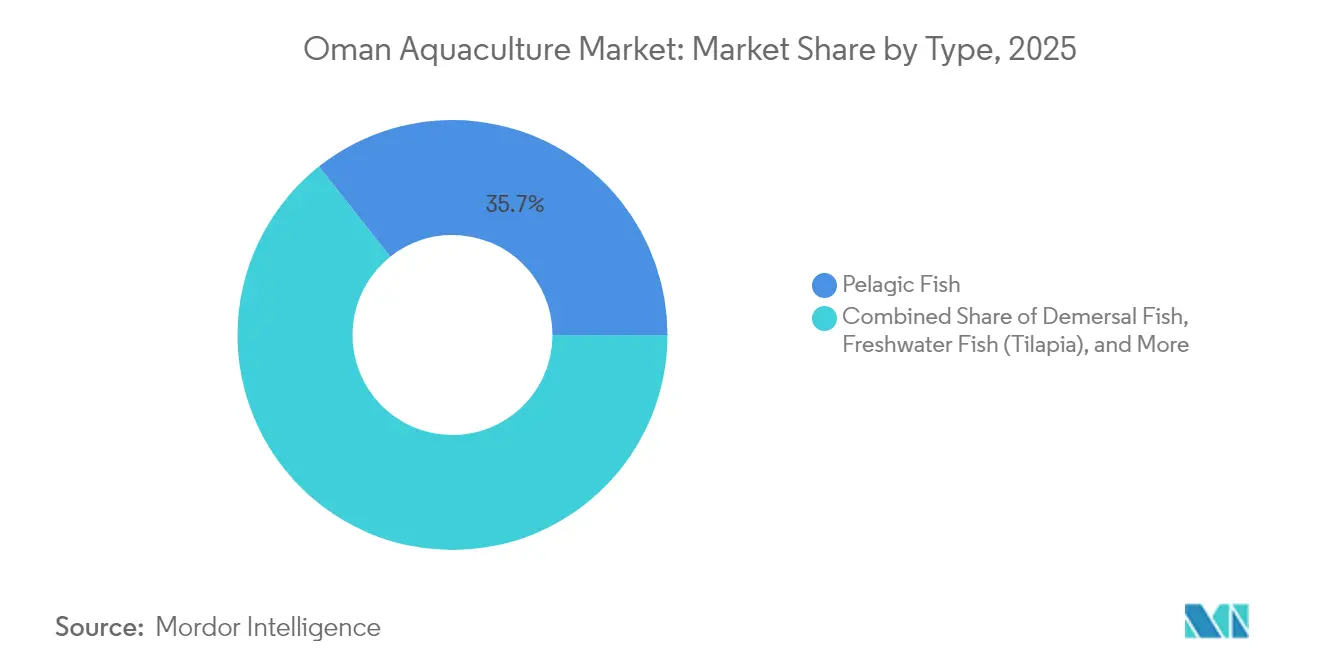

- By type, pelagic fish held 35.7% of the Oman aquaculture market share in 2025, while shrimp is forecast to grow at a 5.42% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Aquaculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 funding and project pipeline | +1.2% | National, with early gains in South Al Sharqiyah, Muscat, and North Al Batinah | Medium term (2-4 years) |

| Export demand from Gulf Cooperation Council and East Asia for premium seafood | +1.0% | National, with spillover to GCC and East Asian export corridors | Medium term (2-4 years) |

| Shrimp and sea bream capacity additions in South Al Sharqiyah and Muscat | +0.8% | South Al Sharqiyah and Muscat Governorates | Short term (≤ 2 years) |

| Financing support and investor facilitation for aquaculture projects | +0.6% | National, with early gains in North Al Batinah and South Al Sharqiyah | Short term (≤ 2 years) |

| Oyster and abalone diversification improves species mix | +0.5% | Dhofar, Masirah Island, and Musandam | Long term (≥ 4 years) |

| Certification-led premiumization and export access | +0.4% | Global, including the EU, China, Korea, and Russia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2040 Funding and Project Pipeline

The Oman aquaculture market is benefiting from a clear policy push that places aquaculture within the wider food security agenda under Vision 2040. The 2026 investment portfolio showed that aquaculture remains a priority channel for new project development and capital deployment in the country. Financing support is also significant, as the Agricultural and Fisheries Development Fund has been positioned to cover up to 80% of project costs through linked institutions, reducing the equity burden for smaller and mid-sized operators. This support appears more durable than a one-cycle spending push, as Tanfeedh has established a formal pipeline process to identify, package, and promote viable projects rather than relying on ad hoc approvals. The incentive framework in the Duqm Fisheries Industrial Zone, including long tax relief and customs waivers, adds a downstream pull that supports processing, logistics, and export-oriented investment across the Oman aquaculture market.

Export Demand from Gulf Cooperation Council and East Asia for Premium Seafood

The Oman aquaculture market is aligning with export demand, as seafood buyers are placing greater emphasis on certification, traceability, and quality consistency. Farmed Omani seafood is already reaching the European Union, China, the Republic of Korea, and Russia, indicating that the market is moving beyond domestic absorption and into premium trade lanes. This matters because export compliance not only widens market access but also pushes farms to operate with tighter water management, disease monitoring, and handling standards. The move toward processed formats such as canned products, fillets, and individually quick-frozen products at Duqm raises the revenue base beyond what raw volume growth can deliver on its own. As a result, the Oman aquaculture market is benefiting not only from increased production capacity but also from higher realizations per kilogram in export channels.

Shrimp and Sea Bream Capacity Additions in South Al Sharqiyah and Muscat

Capacity expansion is becoming more visible in the Oman aquaculture market, driven by project additions in shrimp and marine finfish. In South Al Sharqiyah, saline coastal land and shallow water tables continue to support large pond-based shrimp projects at lower site-preparation intensity than in many alternative locations. The April 2026 agreements for 2 shrimp projects in the governorate, with a combined investment of RO 41.3 million (USD 107.41 million) and output of 11,000 metric tons a year, show how quickly this project base is scaling. In June 2024, in Muscat, the seabass and sea bream project pipeline highlights the simultaneous development of premium finfish initiatives, including the Seeb floating-cage project, which is planned to achieve a full-scale production capacity of 10,000 metric tons per year. These additions are creating two specialized production corridors, one centered on shrimp and one centered on marine finfish, which reduces direct overlap inside the Oman aquaculture market.

Financing Support and Investor Facilitation for Aquaculture Projects

Investor facilitation in the Oman aquaculture market is now moving beyond promotion and into packaged execution support. The 2026 food security investment package brought projects to market through technical studies, economic assessments, identified sites, and clearer delivery structures, reducing pre-development uncertainty for investors. This approach matters because earlier project cycles in smaller Gulf markets were often slowed by land, licensing, or feasibility gaps rather than by a lack of investor interest. In October 2024, Fisheries Development Oman (FDO) signed an advisory contract with Malta-based AquaBioTech Group to support strategic development within the Sultanate's aquaculture sector. Backed by a USD 1.2 billion investment, the partnership aims to accelerate sustainable projects to drive economic diversification under Oman Vision 2040[1]Source: AquaBioTech Group, Daniel. "Fisheries Development Oman (FDO) signs advisory contract with AquaBioTech Group." aquabt.com. The current model shortens the path from concept to operating farm and also makes Oman more accessible to specialized aquaculture firms that prefer de-risked entry routes. The result is a stronger pipeline of near-term buildouts in farms, hatcheries, and linked processing assets across the Oman aquaculture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disease and biosecurity risk in shrimp and finfish farms | -0.6% | South Al Sharqiyah and North Al Batinah, especially shrimp hubs | Short term (≤ 2 years) |

| Dependence on imported seed and aquafeed inputs | -0.5% | National | Medium term (2-4 years) |

| Harmful algal blooms, monsoon hypoxia, and cyclone exposure | -0.4% | Sea of Oman and Arabian Sea coastal zones | Short term (≤ 2 years) |

| Coastal siting friction, environmental approvals, and competing shoreline uses | -0.3% | Muscat, Dhofar, and Musandam coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Disease and Biosecurity Risk in Shrimp and Finfish Farms

Disease remains the most immediate biological threat to the Oman aquaculture market, especially in intensive shrimp systems. White Spot Syndrome Virus and Acute Hepatopancreatic Necrosis Disease remain relevant concerns because Oman still relies on imported broodstock and post-larvae channels linked to regions where these risks are well known. A 2024 survey from Sultan Qaboos University found that 50.72% of imported fish samples carried 1 or more ectoparasites, underscoring the broader vulnerability posed by live-animal imports. Blue Aqua International is on track to have its Semi-Recirculating Aquaculture System farm, along with a hatchery and broodstock center in Shinas, fully operational by February 2026. With a planned capacity of 1,800 metric tons, the Shinas facility is being designed as a state-of-the-art, technology-driven farm that emphasizes biosecurity, efficiency, and environmental responsibility[2]Source: Mendoza, Jomar. "Shinas shrimp farm nears completion." omanobserver.om. Even so, uneven infrastructure across operators means a serious disease event in a dense shrimp cluster could quickly affect production, investor confidence, and restocking decisions across the Oman aquaculture market.

Dependence on Imported Seed and Aquafeed Inputs

Input dependence still limits the operating resilience of the Oman aquaculture market. Specific-pathogen-free shrimp seed and much of the high-protein aquafeed continue to come from abroad, leaving farms exposed to freight delays, trade restrictions, and supplier disruptions. This dependence matters most during stocking cycles because delayed seed or feed availability can affect pond utilization, growth planning, and cash conversion at the farm level. The Oman Bio-Products Factory, inaugurated in the Khazaen Economic Zone in December 2025, with a Phase 1 capacity of 15,000 metric tons of aquatic feed per year, demonstrates that localization of this supply layer has become a policy priority. Until domestic feed and seed capacity deepens further, volatility in imported inputs will continue to weigh on margins and operating predictability across the Oman aquaculture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrimp Ascendancy Reshapes a Pelagic-Led Market

Pelagic fish accounted for 35.7% of the market in 2025, keeping this category at the forefront of the Oman aquaculture market by value. Sardines and mackerel supported this position through their direct consumption and their role in fishmeal and oil production, linking aquaculture activity with the wider seafood processing chain. Tuna and barracuda added a premium layer to the pelagic segment, and the tuna fattening project in Quriyat showed that Oman is also testing ways to capture more high-value processing and finishing activity domestically. Demersal fish such as grouper, trevally, emperor, and pomfret served smaller but attractive demand pockets tied to premium domestic and regional consumption. Freshwater tilapia remained a smaller category, yet it continued to hold strategic relevance for inland operators because it offers a more accessible route into the Oman aquaculture industry than many marine species.

Shrimp is projected to record a 5.42% CAGR through 2026 to 2031, making it the fastest-growing segment of the Oman aquaculture market. Vannamei and Indian White shrimp are driving this rise, supported by South Al Sharqiyah’s saline soils and shallow coastal gradients that allow large pond footprints at lower civil construction intensity than many competing sites. Scallop and lobster remain limited in current scale, but they still have development potential, provided operators are willing to invest in seed production and aquaculture-assisted stock programs. Abalone and caviar stay small in volume terms, though the unit-value premium in abalone is among the strongest in the entire species mix because the native Omani product faces less direct price pressure in premium import channels.

Geography Analysis

South Al Sharqiyah acts as the center of gravity for the Oman aquaculture market because it hosts the deepest concentration of shrimp projects and some of the most favorable saline coastal land in the country. North Al Batinah is emerging as the second main shrimp corridor, helped by the Phoenix National project in Shinas and the start of operations at Blue Aqua International’s integrated shrimp, hatchery, and broodstock facility in the same area. Together, these 2 governorates account for most of the near-term incremental farm capacity now moving through the Oman aquaculture market.

Muscat carries the strongest concentration of premium marine finfish activity in the Oman aquaculture market. Projects in Quriyat and Seeb are aimed at export-oriented species such as European seabass and sea bream, which gives Muscat a different role from the shrimp-heavy eastern coast. Al Wusta, centered on Duqm, is becoming the main downstream integration zone rather than a pure farming hub. The Sea Pride Integrated Fisheries Company (SIFCO) complex in Duqm, with IQF freezing, automated shrimp lines, and tuna canning capabilities, provides producers across multiple regions with a stronger route to export processing and cold chain support. When combined with tax relief, customs waivers, and long land-use windows, Al Wusta becomes one of the most important enabling geographies in the Oman aquaculture market, even when farm output is produced elsewhere.

Dhofar plays a distinct role because it holds the Omani abalone resource and remains the core location for premium abalone development in the Omani aquaculture market. The addition of a new Sharabithat abalone project to the 2026 investment pipeline shows that Dhofar’s role is expanding from wild-capture heritage into structured commercial farming. Musandam, despite its physical distance from mainland production zones, moved closer to full commercial participation when Musandam Aquaculture Company began trial harvests from its sea bream cages near Khasab in February 2025[3]Source: Prabhu, Conrad. "Musandam's first aquaculture project begins trial harvest." omanobserver.om. Masirah Island adds another niche layer through rock oyster activity, showing that remote coastal locations can still support viable shellfish production when species choice matches local conditions.

Competitive Landscape

The Oman aquaculture market follows a dual-track structure in which state-backed platforms and private operators are both active, but they compete with different tools and at different scales. Fisheries Development Oman remains central because it links strategic public backing with large-scale project ambition across marine finfish, shrimp, and the downstream value chain. This has kept concentration moderate rather than low, since a limited number of well-supported entities hold much of the visible large-scale pipeline, while smaller firms are still building project depth. Sea Pride’s shrimp farm in Awrab and its link to the processing platform in Duqm demonstrate how vertical integration is becoming a practical competitive model in the Oman aquaculture market. Blue Aqua’s integrated Shinas site provides a second example, as it combines farm production, hatchery functions, broodstock control, and enhanced biosecurity in a single asset base.

Technology is becoming one of the clearest dividing lines inside the Oman aquaculture market. Semi-recirculating and full recirculating systems offer tighter water control, lower disease exposure, and greater consistency than conventional open systems, especially under high environmental stress. The Ministry-backed Al Musannah marine RAS pilot also matters because it supports local operator training and gives the market a domestic reference point for controlled-environment production. Tuna fattening in Quriyat adds another strategic example, as it shows leading players are not only scaling conventional categories but are also testing premium species pathways that can improve export value realization.

White-space opportunities remain open in shellfish, algae, premium niche species, and land-based controlled systems, indicating the Oman aquaculture market is not yet locked into a mature competitive landscape. Smaller names such as Arabian Sea Fisheries Co (SFZ) LLC and Masirah Sea Fish Products LLC are positioned to defend narrower coastal niches rather than compete directly with the largest shrimp and finfish projects. Formal food-safety systems, traceability, and export compliance are raising the operating threshold, favoring organized firms with stronger process discipline and greater capital access.

Recent Industry Developments

- April 2026: The Sultanate of Oman and the Food and Agriculture Organization of the United Nations, through the Oman Ministry of Agriculture, Fisheries, and Water Resources, have signed four aquaculture investment agreements worth over RO 51 million (USD 132 million). These include shrimp farming projects in South Al Sharqiyah and Al Wusta, and a finfish project in Quriyat, Muscat. The agreements, the largest single-tranche aquaculture investment in Oman's history, support the Ministry's 252,000 metric tons output target for 2030.

- February 2026: Phoenix National Company has started construction on its RO 23.5 million (USD 61.1 million) white-leg shrimp aquaculture project in Shinas, North Al Batinah. Spanning 15 hectares, it targets an annual output of 7,500 metric tons and features modern pond technology, biosecurity-controlled hatcheries, and advanced water management. Progress is tracked under the Ministry's investor-facilitation framework.

- June 2025: The Sultanate of Oman and the Food and Agriculture Organization of the United Nations (FAO) signed a Host Country Agreement to establish FAO's permanent representation in Oman. This agreement aims to enhance food security cooperation in the region through sustainable fisheries management, technical support, and projects in aquaculture and climate resilience.

Oman Aquaculture Market Report Scope

Aquaculture is the practice of farming aquatic organisms, including fish, mollusks, and crustaceans. The commercial production of aquatic species, namely, fish (pelagic fish types, demersal fish types, freshwater fish types, caviar, and salmon) and other edible aquatic species (scallops, shrimp, lobsters, and other species) produced through the country's fisheries and aquaculture sector have been considered for the market study. The Omani fisheries and aquaculture market is segmented by type (pelagic fish, demersal fish, freshwater fish, scallops, shrimp, lobsters, caviar, and other types). The report offers the market size and forecasts in terms of volume (metric tons) and value (USD) for all the above segments.

By Species

| Pelagic Fish | Sardines |

| Mackerel | |

| Tuna | |

| Barracuda | |

| Demersal Fish | Grouper |

| Trevally | |

| Emperor | |

| Pomfret | |

| Freshwater Fish | Tilapia |

| Carp | |

| Crustaceans | Whiteleg Shrimp |

| Indian White Shrimp | |

| Lobster | |

| Mollusks and Other Aquatic Species | Abalone |

| Oyster | |

| Scallop | |

| Seaweed and Algae | |

| Other Marine Finfish | Sea Bream |

| Sea Bass | |

| Cobia | |

| Barramundi |

By Geography

| Production Analysis (Volume) | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destination Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistic and Infrastructure | ||

| Seasonality Analysis | ||

| By Species | Pelagic Fish | Sardines | |

| Mackerel | |||

| Tuna | |||

| Barracuda | |||

| Demersal Fish | Grouper | ||

| Trevally | |||

| Emperor | |||

| Pomfret | |||

| Freshwater Fish | Tilapia | ||

| Carp | |||

| Crustaceans | Whiteleg Shrimp | ||

| Indian White Shrimp | |||

| Lobster | |||

| Mollusks and Other Aquatic Species | Abalone | ||

| Oyster | |||

| Scallop | |||

| Seaweed and Algae | |||

| Other Marine Finfish | Sea Bream | ||

| Sea Bass | |||

| Cobia | |||

| Barramundi | |||

| By Geography | Production Analysis (Volume) | ||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the projected value of Oman aquaculture by 2031?

The Oman aquaculture market is forecast to reach USD 858.8 million by 2031, up from USD 672.2 million in 2026, at a 5.03% CAGR over 2026 to 2031.

Which species category leads aquaculture revenue in Oman?

Pelagic fish led in 2025 with 35.7% of revenue, supported by strong domestic consumption and links to fish meal and oil processing.

Which category is growing the fastest in Oman aquaculture?

Shrimp is projected to be the fastest-growing type, with a 5.42% CAGR from 2026 to 2031, supported by large pond projects in South Al Sharqiyah and North Al Batinah.

Which governorates matter most for aquaculture expansion in Oman?

South Al Sharqiyah and North Al Batinah are central for shrimp capacity, while Muscat leads in premium marine finfish and Al Wusta supports processing and export logistics through Duqm.

What are the main risks facing seafood farming operations in Oman?

The main risks are disease in shrimp and finfish farms, imported seed and feed dependence, harmful algal blooms, cyclone-linked marine disruption, and slower coastal approvals.

Page last updated on: