Application Gateway Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

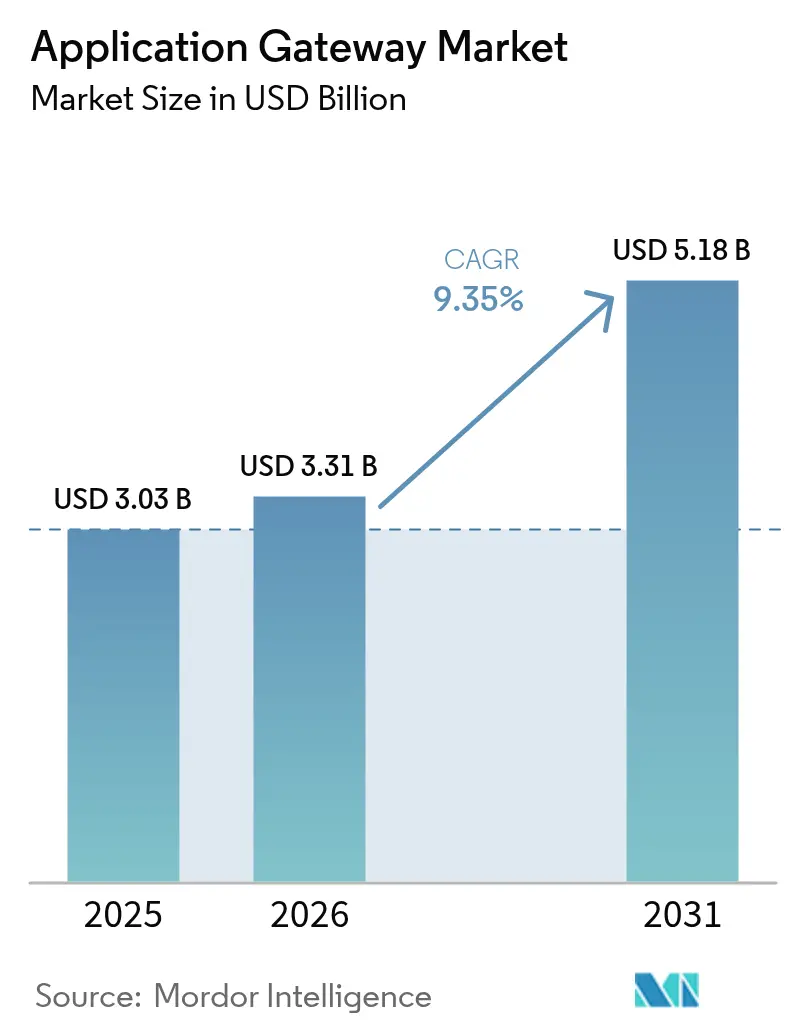

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 5.18 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Gateway Market Analysis by Mordor Intelligence

Application Gateway Market size market size in 2026 is estimated at USD 3.31 billion, growing from 2025 value of USD 3.03 billion with 2031 projections showing USD 5.18 billion, growing at 9.35% CAGR over 2026-2031. The upward trajectory is propelled by a sharp rise in automated Layer-7 DDoS attacks, wider deployment of Zero-Trust and SASE architectures, and accelerated cloud-native application rollouts. Enterprises seek low-latency, policy-driven traffic management for hybrid multicloud environments, placing application gateways at the center of security and performance strategies. Growing investment in edge computing and quantum-resistant encryption further enlarges the addressable opportunity, while managed service models help enterprises overcome skills shortages.

Key Report Takeaways

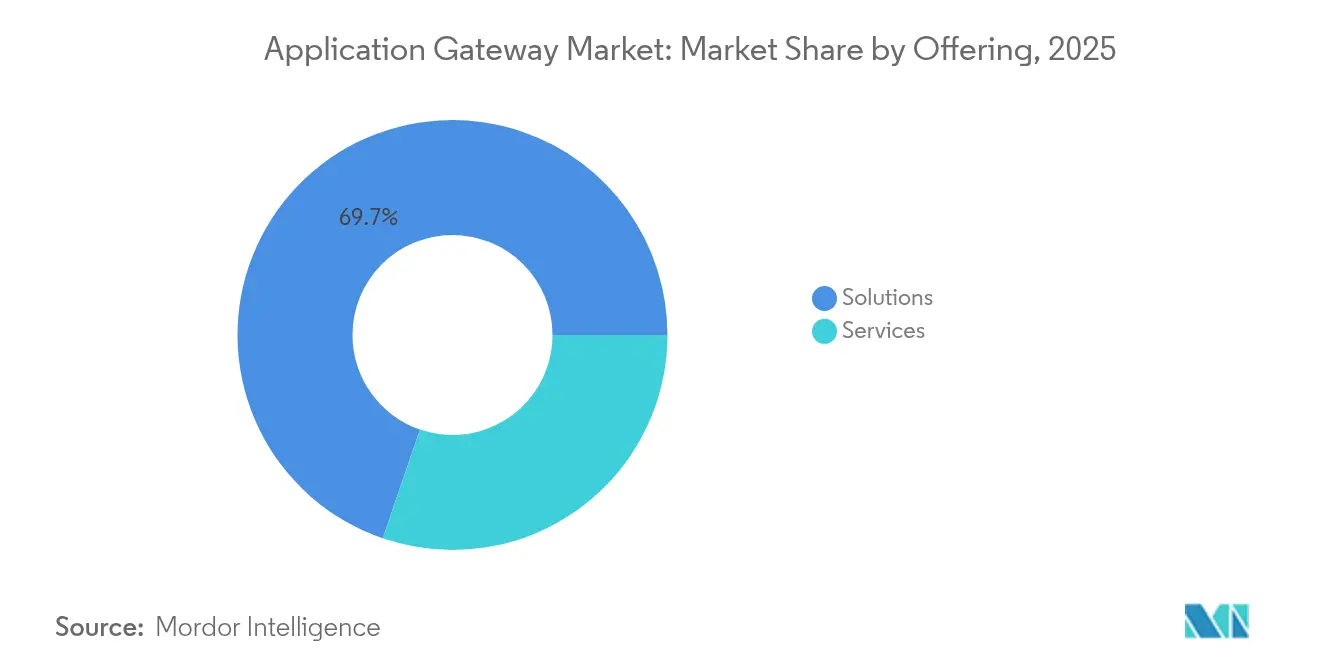

- By offering, solutions retained 69.74% revenue share of the application gateway market in 2025, whereas services are on course for the fastest 12.11% CAGR through 2031.

- By deployment mode, cloud implementations held 58.10% of the application gateway market share in 2025; hybrid deployments are projected to register an 10.84% CAGR by 2031.

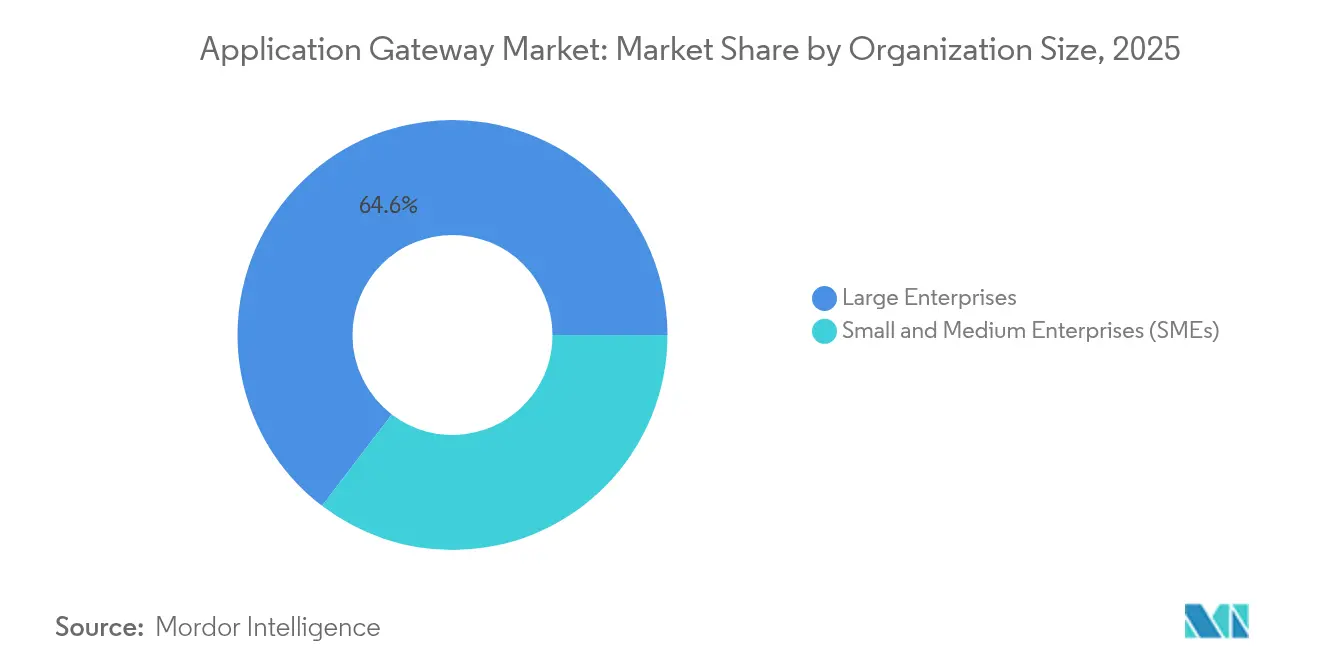

- By organization size, large enterprises commanded 64.62% of the application gateway market size in 2025, while the SME segment is expanding at a 12.29% CAGR.

- By end-user industry, IT and telecommunications generated 27.85% revenue in 2025; retail and e-commerce is forecast to accelerate at an 11.12% CAGR to 2031.

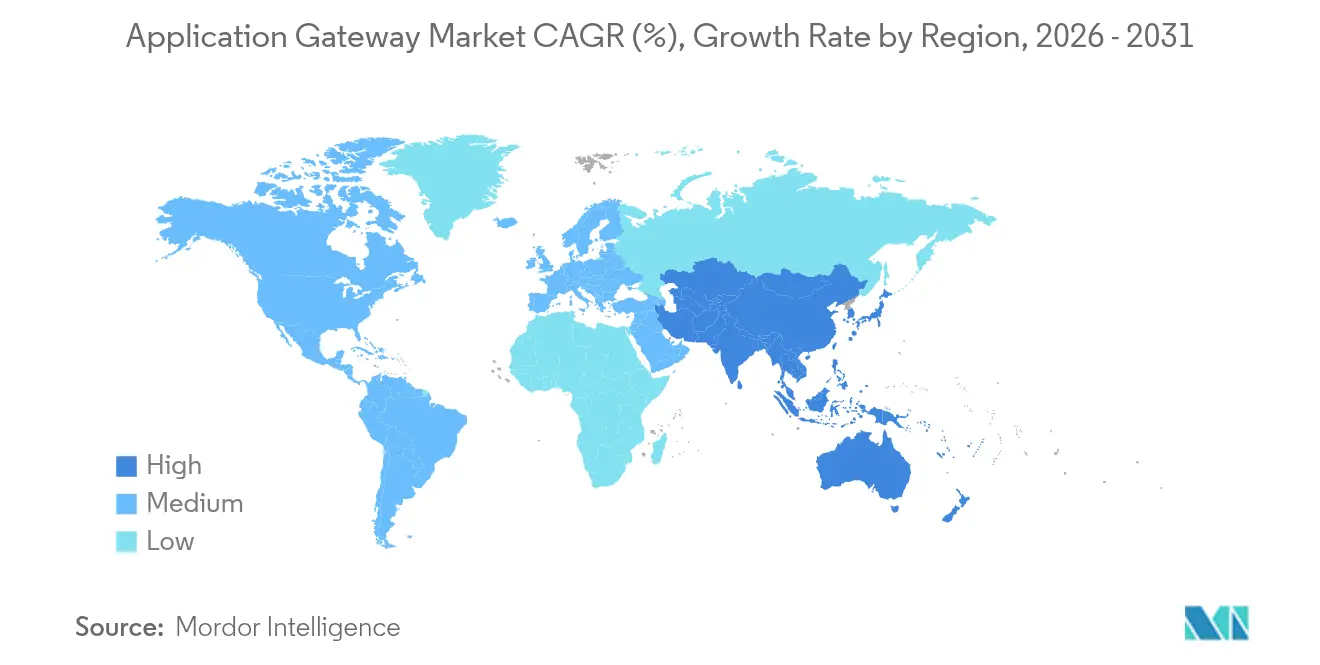

- By geography, North America contributed 37.74% of 2025 revenue, whereas Asia-Pacific is predicted to advance at a 11.93% CAGR through 2031.

- F5, Cloudflare, and Akamai collectively accounted for slightly above 40% of 2024 revenue, indicating a moderately consolidated environment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in automated Layer-7 DDoS and bot attacks | +2.1% | Global, peak in North America and Europe | Short term (≤ 2 years) |

| API-centric digital transformation | +1.8% | Global, led by North America and APAC | Medium term (2-4 years) |

| Shift toward Zero-Trust and SASE | +1.5% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Cloud-native application explosion | +1.4% | Global, highest adoption in APAC | Long term (≥ 4 years) |

| Edge computing demand | +1.2% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Quantum-resistant encryption R&D | +0.8% | North America and Europe, selective APAC uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in automated Layer-7 DDoS and bot attacks

Daily Layer-7 DDoS volumes reached 4,500 attempts in 2024, according to Microsoft threat intelligence. Attackers now mimic legitimate traffic, rendering traditional WAF signatures ineffective. Vendors respond with machine-learning-driven mitigation such as Akamai’s Behavioral DDoS Engine, which distinguishes abnormal patterns in real time. Financial services and e-commerce platforms feel the sharpest revenue impact, prompting urgent procurement of integrated application gateway platforms that combine behavioral analytics, rate-limiting, and API threat detection.[1]Microsoft Corp., “Understanding the Evolving Threat of DDoS Attacks in 2024,” techcommunity.microsoft.com

API-centric digital transformation among enterprises

By 2026, 40% of financial transactions are projected to flow through non-bank channels, underscoring the centrality of API-first development. Multicloud API gateways, illustrated by Kong’s deployment at First Abu Dhabi Bank, unify microservices and security policies across AWS and GCP, cutting operational complexity. As API endpoints multiply, demand consolidates around Web Application and API Protection (WAAP), where a single gateway enforces traffic inspection, authentication, and observability.[2]Kong Inc., “Deploying a Multi-Cloud API Gateway on AWS and GCP,” konghq.com

Rapid shift toward Zero-Trust and SASE architectures

Enterprises move away from perimeter defense, folding networking and security into cloud-delivered SASE stacks. Palo Alto Networks now supports RFC 9242 and RFC 9370 for quantum-safe VPNs, future-proofing encrypted tunnels. Case studies such as Westfield demonstrate 60% network cost savings via Prisma SASE, elevating application gateways to identity-aware enforcement points that authenticate users, devices, and context on every request.[3]Palo Alto Networks, “The Quantum Countdown: How Hybrid Encryption Is Quietly Fortifying Your Web Browsing and Applications,” live.paloaltonetworks.com

Cloud-native application explosion

Kubernetes and serverless adoption intensify the need for gateways capable of automatic service discovery, policy-as-code, and scale-out capacity. F5 Distributed Cloud App Stack integrates SaaS-delivered load balancing and WAAP with GitOps workflows, enabling consistent configuration across multicloud clusters. Ephemeral workloads drive interest in API-driven gateways that spin up and retire alongside containers without manual intervention.[4]F5 Inc., “Distributed Cloud App Stack,” docs.cloud.f5.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills gap in full-stack security operations | -1.3% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Interoperability issues in multicloud setups | -0.9% | Global, high impact on large enterprises | Medium term (2-4 years) |

| Budget compression in SMBs | -0.7% | Global, varies by economic cycles | Short term (≤ 2 years) |

| Emerging privacy regulations | -0.5% | Europe and APAC, selective in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skills gap in full-stack application security operations

The UK recorded a 3,500-person annual deficit of qualified cyber professionals in 2024. Talent with combined networking, API security, and Zero-Trust expertise remains scarce, delaying complex gateway deployments. Vendors increasingly bundle managed services and low-code policy builders, but recruitment challenges persist.

Interoperability issues across multicloud and hybrid environments

Nine in ten enterprises cite difficulties orchestrating disparate vendor-specific gateway services. Divergent APIs complicate uniform policy enforcement and raise the specter of vendor lock-in. Platform-agnostic management layers from providers such as F5 address part of the problem, yet comprehensive standardization remains elusive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Surge Despite Solutions Dominance

Solutions generated 69.74% of 2025 revenue as enterprises implemented Web Application Firewalls, API gateways, and load balancers to counter escalating Layer-7 threats. The application gateway market size tied to services is projected to climb at a 12.11% CAGR, outpacing product growth as organizations outsource complex multicloud configurations. Managed services covering threat analytics and policy tuning attract firms grappling with lean internal teams. Cardinal Health leveraged professional services around F5 Advanced WAF to cut malicious traffic by 40% while enhancing visibility.

Enterprises increasingly buy outcomes such as risk reduction and SLA uptime rather than discrete features, prompting vendors to wrap consulting, deployment, and ongoing SOC support within subscription plans. Consumption-based billing aligns spend with usage, lowering barriers for SME entry and unlocking cross-sell opportunities into Zero-Trust and SASE bundles.

By Deployment Mode: Hybrid Gains Momentum Amid Cloud Leadership

Cloud deployment held 58.10% of 2025 revenue, favored for its elastic scale and native integration. Microsoft Azure Application Gateway achieved a 99.95% SLA, making platform services attractive for greenfield applications. The hybrid segment, however, is forecast for the highest 10.84% CAGR as enterprises retain sensitive workloads on-premises. The application gateway market share for hybrid models climbs as firms seek uniform policy orchestration from edge to core while avoiding wholesale re-platforming.

Partnerships such as F5–NetApp–Red Hat simplify overlay networks that span data centers and multiple clouds. Enterprises rely on policy-driven traffic steering to balance latency, compliance, and cost, cementing gateways as the connective tissue in distributed architectures.

By Organization Size: SME Acceleration Challenges Enterprise Dominance

Large enterprises represented 64.62% of the application gateway market in 2025, thanks to complex portfolio needs and regulatory mandates. The application gateway market size attributable to SMEs, though smaller, is poised for a 12.29% CAGR as affordable SaaS gateways remove hefty capital outlays. VMware’s SD-WAN-as-a-service illustrates tailored bundles delivering bandwidth optimization and built-in security for resource-constrained firms.

SMEs nevertheless face budget headwinds and limited staff; 71% already host workloads in public clouds yet lack comprehensive gateway governance, underscoring a growing managed-service opportunity.

By End-user Industry: Retail E-commerce Drives Digital Commerce Security

IT and telecommunications drove 27.85% of 2025 spend, benefiting from inherent demand for carrier-grade application delivery. Retail and e-commerce is projected for the fastest 11.12% CAGR as omnichannel platforms expose extensive APIs that require granular security. BFSI maintains robust adoption because transaction integrity is critical and regulatory audits are stringent. Healthcare providers accelerate investment in response to FDA guidance on medical device cybersecurity; Medcrypt’s Guardian integrates with RTI Connext to protect authentication and data integrity across hospital networks.

Industrial verticals—manufacturing and energy—expand uptake to safeguard OT networks merging with IT systems under Industry 4.0 initiatives. Government agencies invoke Zero-Trust mandates, making gateways essential for user-centric access to citizen services.

Geography Analysis

North America sustained 37.74% revenue leadership in 2025, underpinned by expansive enterprise IT footprints and regulatory frameworks that favor rapid security refresh cycles. Federal directives on Zero-Trust and quantum-ready encryption accelerate purchase orders, while high breach costs sharpen C-suite focus on Layer-7 protections. The region contends with the deepest cyber-talent shortage, nudging buyers toward managed service models to close operational gaps.

Asia-Pacific represents the fastest expanding block with a 11.93% CAGR to 2031. Nations such as India, China, and Japan launch substantial public–private cloud and data-center investments that spur adoption of advanced traffic-management and security stacks. An AI language-model uptake of 60% across enterprises intensifies bandwidth demand, increasing reliance on gateways that optimize east-west and north-south traffic while enforcing API governance. Fragmented regulatory landscapes across APAC necessitate flexible policy engines that segment data residency and privacy requirements on a per-country basis, favoring vendors capable of granular, rule-based routing.

Europe follows with steady growth tied to GDPR compliance and data-sovereignty mandates. Application gateways that offer built-in geo-fencing and granular cross-border controls gain preference among enterprises coping with divergent interpretations of privacy law after Brexit. Industrial economies in Germany and France integrate gateways into OT networks to protect connected machinery, while Nordic countries add quantum-safe encryption to critical-infrastructure rollouts. Edge data centers proliferate, prompting demand for distributed policy enforcement to keep latency below 20 ms for real-time analytics.

Latin America and the Middle East & Africa remain nascent but strategic. Digital-first banks in Brazil and Saudi Arabia adopt cloud-native gateways to secure open-banking APIs, while 5G build-outs create fertile ground for telecom-centric gateway services. Limited cyber-talent pools and economic volatility suppress immediate scale, yet managed-security models lower upfront spending hurdles. As local compliance regimes mature, vendors that bundle advisory and implementation services position themselves for accelerated uptake beyond 2027.

Competitive Landscape

Established vendors pursue platform consolidation to integrate load balancing, WAAP, and observability in a single control plane. F5 posted USD 731 million revenue in Q2 2025, with systems revenue up 27%, reflecting success in hybrid multicloud orchestration. Cloudflare pairs its global network with Kyndryl’s managed-services expertise to win transformation deals that embed Zero-Trust policies across multi-cloud estates.

Akamai deepens cloud-infrastructure capabilities after acquiring Linode and select Edgio assets, adding 4,200 points of presence to support AI inference workloads at 3× throughput with 60% lower latency. Concurrently, the firm exited China CDN operations, opening whitespace for regional providers to capture local-compliance-focused clients. Strategic moves highlight how regional regulation shapes go-to-market tactics.

Disruptive entrants bet on API-first and edge-native architectures. Start-ups emphasize developer-friendly policy-as-code and AI-driven anomaly detection. Patent filings reveal innovation in low-latency path failover and offloaded AI/ML traffic steering, aiming to differentiate on performance and resilience. Competitive intensity intensifies as hyperscale clouds expand proprietary gateway services with bundled economics, pressuring independent suppliers to focus on open standards, deep observability, and value-added managed offerings.

Application Gateway Industry Leaders

Akamai Technologies Inc.

Amazon Web Services Inc.

A10 Networks Inc.

Barracuda Networks LLC

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Akamai launched an industry-first DNS posture-management service with agentless detection and 24/7 managed SOC support, targeting enterprises seeking integrated prevention and compliance.

- March 2025: Akamai introduced Cloud Inference, leveraging 4,200 PoPs to deliver 3× higher throughput and 60% lower latency for AI workloads.

- March 2025: Honeywell partnered with Verizon to embed 5G in smart meters, adding real-time grid telemetry protected by gateway-driven encryption.

- February 2025: Akamai signed a USD 100 million multi-year cloud-computing contract with a global technology company that includes managed Kubernetes and application-gateway security.

- January 2025: Akamai discontinued CDN services in China, shifting its regional focus to edge security portfolios.

- December 2024: Akamai acquired select Edgio customer contracts and patents, expecting USD 80–100 million in additional 2025 revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the application gateway market as all software or appliance-based layer-7 traffic managers that consolidate web application firewall (WAF), API gateway/WAAP, load-balancer/ADC, and SASE gateway functions, delivered on-premise, in the cloud, or through hybrid deployments. These platforms inspect, protect, and optimize HTTP/S and API traffic for enterprises of every size, spanning verticals from BFSI to manufacturing, and are valued here only at the point of vendor sale or subscription renewal according to Mordor Intelligence.

Scope Exclusions: Legacy layer-4 load balancers, pure CDN services, and standalone VPN concentrators lie outside this coverage.

Segmentation Overview

- By Offering

- Solutions

- Web Application Firewall (WAF)

- API Gateway / WAAP

- Load Balancer / ADC

- Secure Access Service Edge (SASE) Gateway

- Services

- Solutions

- By Deployment Mode

- On-Premise

- Cloud

- Hybrid

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Industry

- BFSI

- IT and Telecommunications

- Retail and E-commerce

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing

- Energy and Utilities

- Education

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed gateway product managers, MSSP architects, and CISOs across North America, Europe, and Asia-Pacific to validate deployment counts, cloud transition timelines, and price erosion curves. We then surveyed mid-market IT directors to test assumed penetration rates within SMEs. These voices closed data gaps and anchored key scenario assumptions before final triangulation.

Desk Research

Our analysts began by mining tier-1 public sources such as US-CERT cyber incident advisories, the European Union Agency for Cybersecurity (ENISA) breach database, NIST's National Vulnerability Database, OWASP Top-10 reports, and regional telecom regulator filings to size the threat surface and deployment base. Trade associations like the Cloud Security Alliance and OASIS provided adoption benchmarks for Zero-Trust and API-first architectures, while company 10-Ks, investor decks, and select filings downloaded via Dow Jones Factiva and D&B Hoovers yielded revenue splits and average selling prices.

Complementary inputs were gathered from customs shipment summaries, Questel's patent families on WAAP algorithms, and import/export alerts that track physical ADC appliances. The sources listed here illustrate the breadth of desk work; many additional publications, datasets, and statistical yearbooks also informed data collection, cross-checks, and contextual framing.

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the global addressable demand pool from the number of internet-facing web and API endpoints, average gateway penetration per 100 endpoints, and prevailing subscription or appliance ASPs. These results are stress-tested with selective bottom-up roll-ups of leading suppliers' reported revenues and channel checks. Input variables include: (1) annual Layer-7 DDoS incident counts, (2) share of workloads migrated to public cloud, (3) mean API traffic growth, (4) SME cloud-security budget index, and (5) regional currency shifts. A multivariate regression links these drivers to historical spend and projects forward. Scenario analysis adjusts for fast-rising SASE bundles.

Data Validation & Update Cycle

Outputs undergo anomaly scans, peer review, and variance checks versus independent indicators (e.g., CDN egress growth, SSL certificate issuances). Reports refresh every year, and material events trigger rapid re-validation so clients receive the most current baseline.

Why Mordor's Application Gateway Baseline Is Widely Trusted

Published estimates often diverge because firms choose different component mixes, pricing benches, and refresh cadences. Our disciplined scope alignment, driver selection, and annual update rhythm temper such swings.

Key gap drivers versus other publishers include: some count only ADC appliances, others fold API-only gateways or CDN security add-ons; several apply flat ASP progressions, while we adjust for SaaS price compression; and a few still use 2019 currency bases, whereas we translate revenues at rolling average rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.03 B (2025) | Mordor Intelligence | - |

| USD 2.53 B (2024) | Global Consultancy A | Excludes managed WAAP services; uses 2022 ASPs |

| USD 2.78 B (2025) | Industry Association B | Counts hardware only; limited SME sampling |

The comparison shows that Mordor's blended software-plus-service scope, rolling currency conversion, and dual validation steps deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and reproducible logic.

Key Questions Answered in the Report

What is the current application gateway market size?

The application gateway market size stands at USD 3.31 billion in 2026, with a projected rise to USD 5.18 billion by 2031.

Which segment is growing fastest in the application gateway market?

Services, encompassing professional and managed offerings, exhibit the highest 12.11% CAGR through 2031.

Why are hybrid deployments gaining traction?

Enterprises balance cloud scalability with on-premises compliance, driving an 10.84% CAGR for hybrid models that maintain uniform security controls across environments.

What is the main driver behind increased application gateway adoption?

Surging automated Layer-7 DDoS and bot attacks require advanced gateways that combine behavioral analytics and API security at scale.

Which region leads growth in the application gateway market?

Asia-Pacific is forecast for the fastest 11.93% CAGR, propelled by large-scale digital-infrastructure investments and rising AI traffic demands.

How consolidated is the competitive landscape?

The top five vendors control a bit more than 60% of global revenue, reflecting moderate consolidation and ample space for niche innovators.

Page last updated on: