Antidote Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

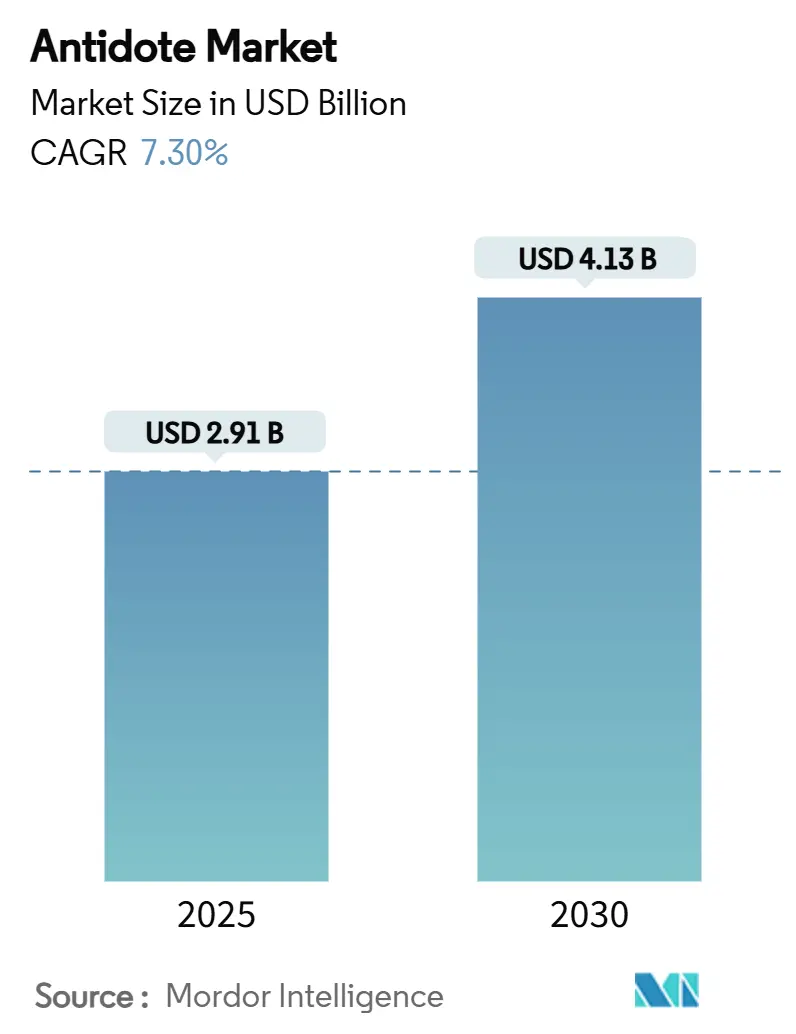

| Market Size (2025) | USD 2.91 Billion |

| Market Size (2030) | USD 4.13 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antidote Market Analysis by Mordor Intelligence

The antidote market size reached USD 2.91 billion in 2025 and is forecast to advance at a 7.3% CAGR to USD 4.13 billion by 2030. Robust expansion reflects three converging forces: mounting opioid-overdose emergencies, accelerating incidence of DOAC-related bleeding, and sustained military funding for chemical-warfare countermeasures. North America dominates current demand thanks to over-the-counter (OTC) naloxone access, while Asia Pacific is posting the quickest gains as governments invest in emergency medical capacity. Acute price pressures on novel biologic reversal agents and unresolved cold-chain gaps in low- and middle-income countries still temper momentum. Yet, technological advances in AI-driven discovery and widening retail distribution channels continue to unlock new addressable volumes. Competitive intensity remains moderate because incumbent pharmaceutical majors, specialty antivenom laboratories, and early-stage biotechnology entrants focus on distinct toxin classes rather than directly overlapping portfolios.

Key Report Takeaways

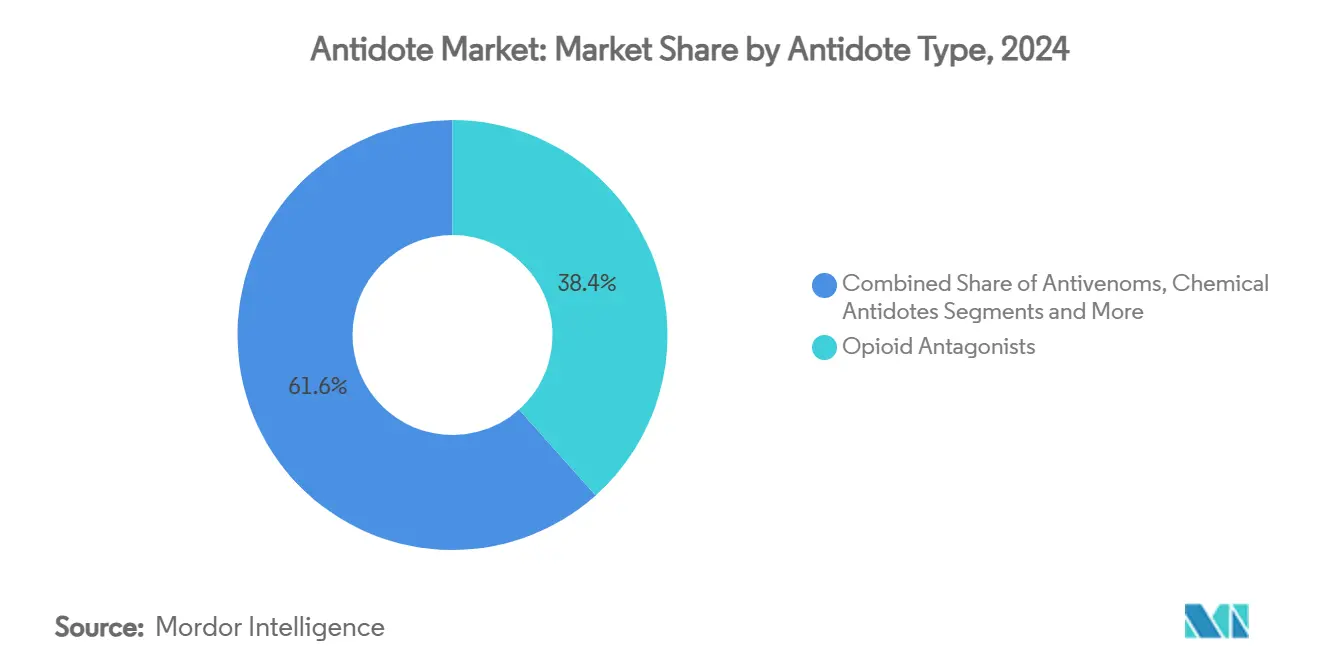

- By antidote type, opioid antagonists accounted for 38.4% of the antidote market share in 2024, while anticoagulant reversal agents are projected to expand at 12.3% CAGR through 2030.

- By indication, opioid overdose captured a 42.1% share of the antidote market size in 2024; anticoagulant-associated bleeding is advancing at a 12.2% CAGR to 2030.

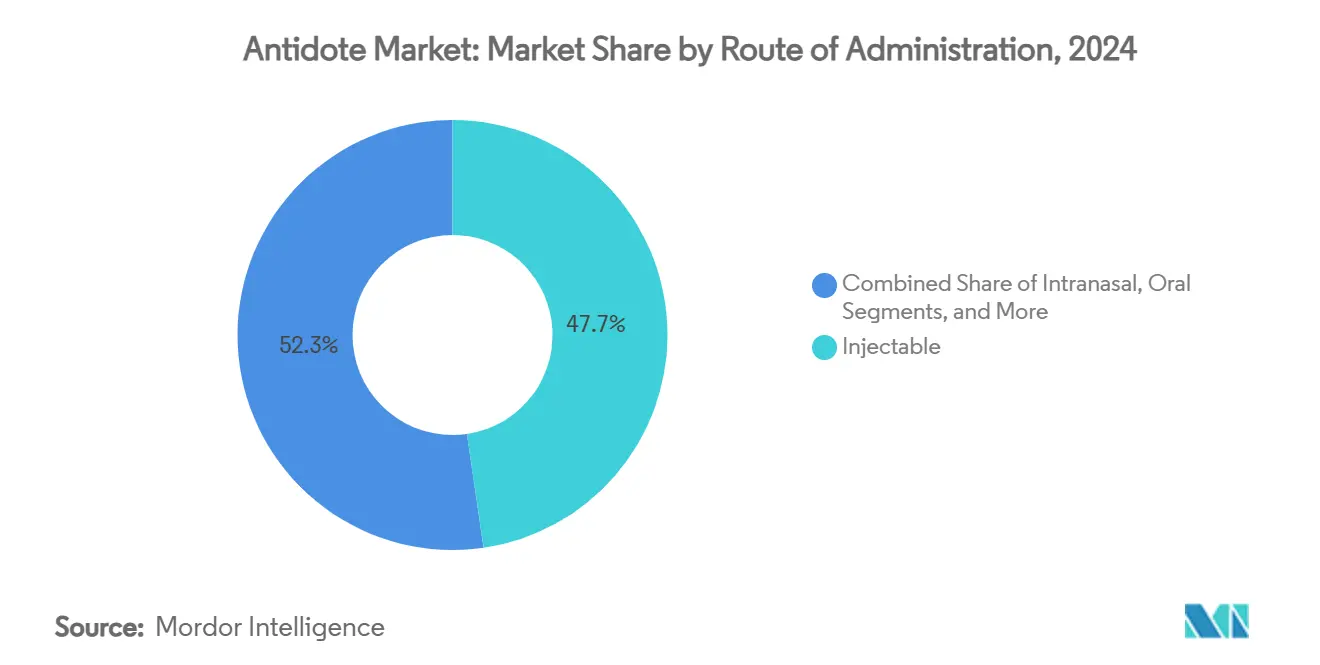

- By route of administration, injectable products led with 47.7% revenue share in 2024, whereas intranasal formulations are forecast to rise at a 12.0% CAGR over 2025-2030.

- By end user, hospitals and trauma centers held 49.8% of the antidote market share in 2024; military and defense organizations recorded the fastest CAGR at 11.5% to 2030.

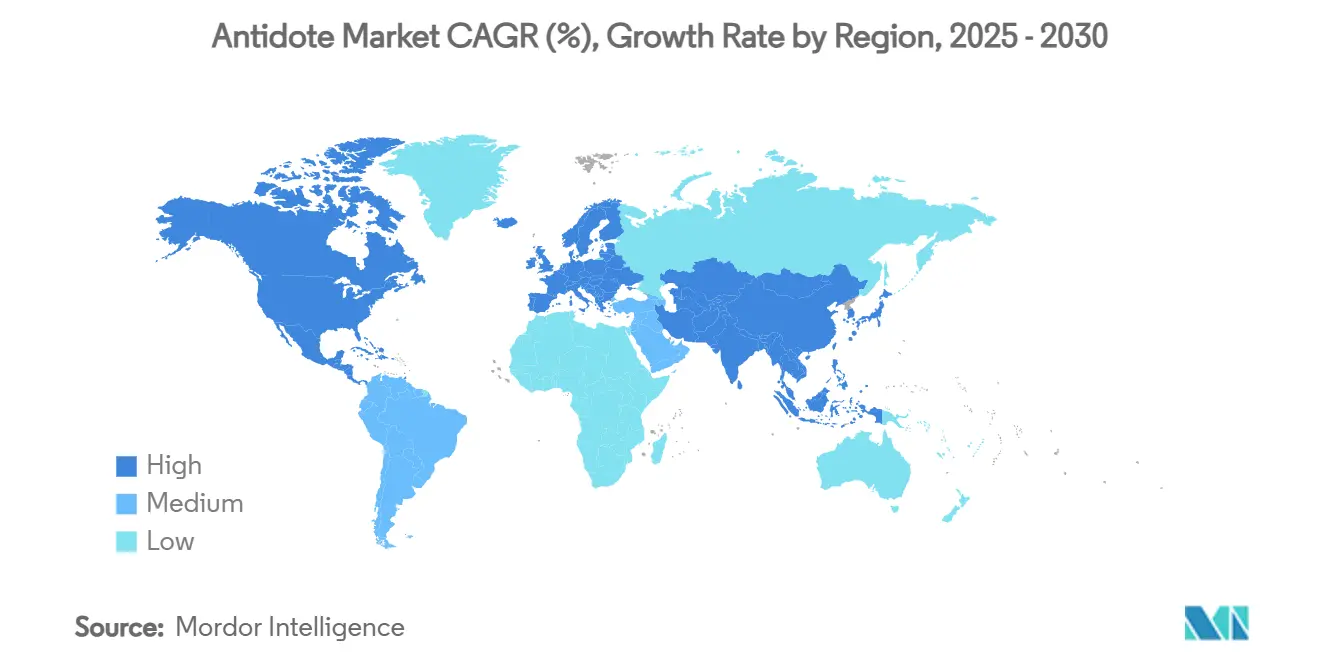

- By geography, North America led with 41.5% of the antidote market in 2024, while Asia Pacific is poised to climb at a 9.3% CAGR throughout the forecast horizon.

Global Antidote Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Opioid-Overdose Prevalence | +1.50% | North America & Europe, spillover to APAC | Short term (≤ 2 years) |

| Rising Use Of DOACs Driving Demand For Specific Reversal Agents | +1.80% | Global, concentrated in developed markets | Medium term (2-4 years) |

| WHO-Led Anti-Venom Access Programmes In Africa & Asia | +1.20% | Sub-Saharan Africa & APAC core | Long term (≥ 4 years) |

| OTC Switch Of Naloxone In US & Europe Broadening Retail Channels | +0.90% | North America & Europe | Short term (≤ 2 years) |

| Military Funding For Novel Chemical-Warfare Antidotes | +0.80% | Global, led by US, NATO countries | Medium term (2-4 years) |

| AI-Enabled Rapid Antidote Discovery Platforms | +0.10% | Global, R&D centers in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Opioid-Overdose Prevalence

More than 83,000 opioid-overdose deaths were reported in the United States during 2022, sustaining heavy demand for rapid-acting antagonists. First-response agencies now carry multi-dose naloxone kits, while clinical data show intranasal nalmefene reduces cardiac-arrest risk to 2.2% versus 19.2% for naloxone in fentanyl cases.[1]Celine M. Laffont et al., “Comparison of Intranasal Naloxone and Nalmefene,” Frontiers in Psychiatry, frontiersin.orgThe US Department of Defense is fielding high-dose autoinjectors for weaponized fentanyl exposure, signaling tactical demand beyond civilian overdose scenarios. Combined, these trends reinforce volume growth across emergency channels, cementing opioids as the cornerstone of the antidote market.

Rising Use of DOACs Driving Demand for Specific Reversal Agents

Andexanet alfa commands a list price above USD 10,000 per treatment episode but maintains brisk uptake because factor Xa inhibitor-related bleeds require immediate reversal. Streamlined regulatory reviews, exemplified by Health Canada’s fast-track approval pathway, shorten time-to-market and encourage manufacturers to build companion antidotes into every new anticoagulant programme. Hospitals are revising emergency algorithms to ensure on-hand inventory despite budgetary strain, pushing anticoagulant reversal products to the fastest-growing segment of the antidote market.

WHO-Led Anti-Venom Access Programmes in Africa & Asia

The World Health Organization targets a 50% reduction in snakebite mortality by 2030 through standardized antivenom guidelines.[2]World Health Organization, “Target Product Profiles for Animal Plasma-Derived Antivenoms,” who.intNew target product profiles cover broad-spectrum and syndromic formulations, helping public laboratories—now 46 worldwide—focus on region-wide applicability rather than localized batches. Harmonised quality benchmarks should curb substandard imports and bolster trust among healthcare providers, ultimately expanding the antidote market in previously underserved rural districts.

OTC Switch of Naloxone Broadening Retail Channels

The US FDA authorized OTC naloxone in March 2023 under its Additional Conditions for Nonprescription Use framework. Large chains quickly priced two-spray units below USD 35, yet only 53% of pharmacies stocked the product in early 2024 due to supply-chain and liability concerns. State bulk-purchase consortia now aggregate orders to minimise unit costs, thereby widening household-level penetration and lifting baseline volumes within the antidote market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High Cost Of Novel Reversal Biologics | -0.80% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Cold-Chain & Serum-Shortage Issues In LMIC Hospitals | -0.60% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Low Stocking Rates Of Critical Antidotes In Community Hospitals | -0.40% | Global, concentrated in rural and resource-limited settings | Short term (≤ 2 years) |

| Regulatory Fragmentation For Cross-Border Antivenom Trade | -0.30% | ASEAN, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-High Cost of Novel Reversal Biologics

Price tags above USD 10,000 for single-episode treatments force hospitals to ration andexanet alfa through tight utilization protocols, delaying time-critical administration. Budget stress in emerging markets magnifies inequities, as reimbursement schemes rarely cover premium biologics, crimping near-term expansion of the antidote market.

Cold-Chain & Serum-Shortage Issues in LMIC Hospitals

Antivenoms require 2-8 °C storage; yet power outages and inadequate transport expose vials to heat degradation, producing ineffective stock and elevating mortality from snakebites.[3]Chanthawat Patikorn, “Situation of Snakebite and Antivenom Access in ASEAN,” ncbi.nlm.nih.gov Supply gaps are deepest in rural clinics, constraining the antidote market where need is highest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Antidote Type: Opioid Antagonists Hold Command While Reversal Agents Surge

Opioid blockers captured 38.4% of 2024 revenue as synthetic fentanyl variants kept emergency demand elevated, anchoring the antidote market. Naloxone innovation moved toward needle-free spray devices, yet product development now emphasizes higher-potency molecules like nalmefene to address fentanyl analogs.

Anticoagulant reversal agents lead growth at 12.3% CAGR thanks to the clinical imperative for rapid DOAC neutralisation, lifting their share of the antidote market size to an expected 22% by 2030. Suppliers are aligning launch strategies with companion anticoagulant rollouts, cementing co-dependent revenue streams.

By Indication: Overdose Management Dominates but Bleeding Complications Accelerate

Opioid overdose represented 42.1% of the antidote market demand in 2024 as first-responder protocols standardized multi-dose carry requirements. The syndromic approach favors stocking broad-spectrum antagonists where precise toxin identification is delayed.

Bleeding linked to factor Xa inhibitors is expanding at 12.2% CAGR, adding USD 620 million to the antidote market size by 2030. Uptake of idarucizumab and andexanet alfa reshapes emergency department formularies that formerly relied on non-specific hemostatic agents.

By Route of Administration: Injectable Reliability Meets Nasal Speed

Injectables retained a 47.7% share in 2024 because intravenous push ensures rapid systemic exposure in critical care scenarios. Their dominance keeps manufacturing capacity centred on sterile liquid fill-finish plants, which is crucial to sustaining the antidote market.

The intranasal segment is on track for 12.0% CAGR, propelled by 6-9-minute therapeutic onset and 47-51% bioavailability that allow non-clinicians to intervene early. Multiple pipeline products apply permeation enhancers to extend nasal delivery beyond opioids toward cyanide and nerve-agent indications.

By End User: Hospital Command Faces Tactical Uplift

Hospitals and trauma centres accounted for 49.8% of the antidote market share in 2024, reflecting centralized formulary management and cold-chain capacity. Expansion efforts revolve around onsite toxicology support and AI decision-support tools for dose optimization.

Military and defence buyers will grow at 11.5% CAGR through 2030, underpinned by pre-deployment stockpiles and facility hardening measures against nerve agents. Government tenders typically lock in multi-year supply volumes, offering predictability that stabilizes the broader antidote market.

Geography Analysis

North America’s 41.5% antidote market leadership stems from robust opioid mitigation programmes, federal CHEMPACK caches, and rapid adoption of DOAC reversal biologics. Yet access gaps persist, particularly in rural areas where only 53% of retail pharmacies stock OTC naloxone. State-level bulk purchasing and pharmacist-prescribing authority are closing those disparities, underpinning mid-single-digit regional growth.

Asia Pacific’s antidote market is advancing at 9.3% CAGR as China’s healthcare expenditure targets RMB 205 trillion by 2030 and India implements a National Action Plan for snakebite management. Investments in rural trauma centres and domestic antivenom facilities enlarge baseline volumes. Regulatory harmonisation remains a hurdle: ASEAN’s divergent labelling rules slow cross-border supply, extending lead times and driving localised production clustering.

Europe presents a mature but steady landscape. EMA’s centralised approvals speed adoption of new reversal agents, and universal health coverage reimburses premium biologics, sustaining predictable outlays. Workplace safety directives maintain consistent demand for heavy-metal chelators. However, modest population growth and prevailing price controls cap CAGR in the low single digits.

Competitive Landscape

Market structure remains moderately fragmented because few suppliers span every toxin class. Pfizer and Emergent BioSolutions dominate opioid antagonists, while AstraZeneca and CSL leverage biologics expertise to control anticoagulant reversal niches. Antivenom production is spread across more than 40 laboratories, many publicly funded, diluting individual shares but safeguarding supply continuity.

Commercial rivalry intensifies as OTC naloxone erodes prescription brand premiums, igniting a race to undercut unit prices without sacrificing margin. Simultaneously, defence contracts offer high-volume certainty, encouraging specialised lines for autoinjectors and inhalational antidotes. Early-stage biotech entrants wield monoclonal antibody platforms that promise longer half-lives and higher specificity, threatening older plasma-derived products within the antidote industry.

Strategic moves include AstraZeneca’s plan to elevate total revenue to USD 80 billion by 2030 with larger rare-disease franchises that feature DOAC reversals. Meanwhile, generic manufacturers pursue supply-chain efficiencies and low-cost nasal sprays for community programmes, broadening the antidote market yet compressing pricing power across established brands.

Antidote Industry Leaders

Emergent BioSolutions

AstraZeneca

Pfizer Inc.

SERB Pharmaceuticals

CSL Seqirus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AstraZeneca outlined 21 late-stage New Molecular Entities at the JP Morgan Healthcare Conference, reinforcing its commitment to critical-care pipelines that include antidotes.

- January 2025: Skadden analysed the FDA’s ACNU framework, detailing commercial opportunities for OTC drugs with specific conditions, pertinent to next-generation antidote launches.

- July 2024: AstraZeneca projected low-double-digit revenue growth for H1 2024, buoyed by manufacturing expansions that support its Andexxa franchise.

Global Antidote Market Report Scope

| Opioid Antagonists (Naloxone, Nalmefene) |

| Anticoagulant Reversal Agents (Andexanet alfa, Idarucizumab) |

| Antivenoms (Snake, Scorpion, Spider) |

| Chemical & Nerve-agent Antidotes (Atropine, Pralidoxime, Cobinamide) |

| Heavy-Metal Chelators (Dimercaprol, DMSA, EDTA) |

| Opioid Overdose |

| Envenomation & Venomous Bites |

| Anticoagulant-Associated Bleeding |

| Chemical & Industrial Poisoning |

| Heavy-Metal Toxicity |

| Injectable |

| Intranasal |

| Oral |

| Topical/Local |

| Inhalational |

| Hospitals & Trauma Centres |

| Emergency Medical Services |

| Military & Defence Organisations |

| Ambulatory Surgical Centres |

| Retail & Community Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Antidote Type | Opioid Antagonists (Naloxone, Nalmefene) | |

| Anticoagulant Reversal Agents (Andexanet alfa, Idarucizumab) | ||

| Antivenoms (Snake, Scorpion, Spider) | ||

| Chemical & Nerve-agent Antidotes (Atropine, Pralidoxime, Cobinamide) | ||

| Heavy-Metal Chelators (Dimercaprol, DMSA, EDTA) | ||

| By Indication | Opioid Overdose | |

| Envenomation & Venomous Bites | ||

| Anticoagulant-Associated Bleeding | ||

| Chemical & Industrial Poisoning | ||

| Heavy-Metal Toxicity | ||

| By Route of Administration | Injectable | |

| Intranasal | ||

| Oral | ||

| Topical/Local | ||

| Inhalational | ||

| By End User | Hospitals & Trauma Centres | |

| Emergency Medical Services | ||

| Military & Defence Organisations | ||

| Ambulatory Surgical Centres | ||

| Retail & Community Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antidote market in 2025?

The antidote market size stood at USD 2.91 billion in 2025 and is projected to reach USD 4.13 billion by 2030 at a 7.3% CAGR.

Which therapeutic segment is expanding the fastest?

Anticoagulant reversal agents lead growth with a 12.3% CAGR through 2030 as hospitals adopt factor Xa inhibitor antidotes for DOAC-related bleeding.

Why is Asia Pacific showing the highest growth rate?

Accelerating healthcare investment, WHO-supported antivenom programmes, and rising poisoning incidence are driving a 9.3% CAGR across Asia Pacific.

What delivery route is gaining share most rapidly?

Intranasal formulations, prized for needle-free administration and 6-9-minute onset, are advancing at a 12.0% CAGR within overall antidote sales.

Which end-user segment will see the strongest uptake?

Military and defence organisations are projected to grow at 11.5% CAGR due to strategic stockpiling of chemical-warfare countermeasures.

What remains the biggest restraint on market expansion?

Ultra-high prices of novel biologic reversal agents continue to limit adoption, especially in budget-constrained healthcare systems.

Page last updated on: