Anticoagulant Reversal Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

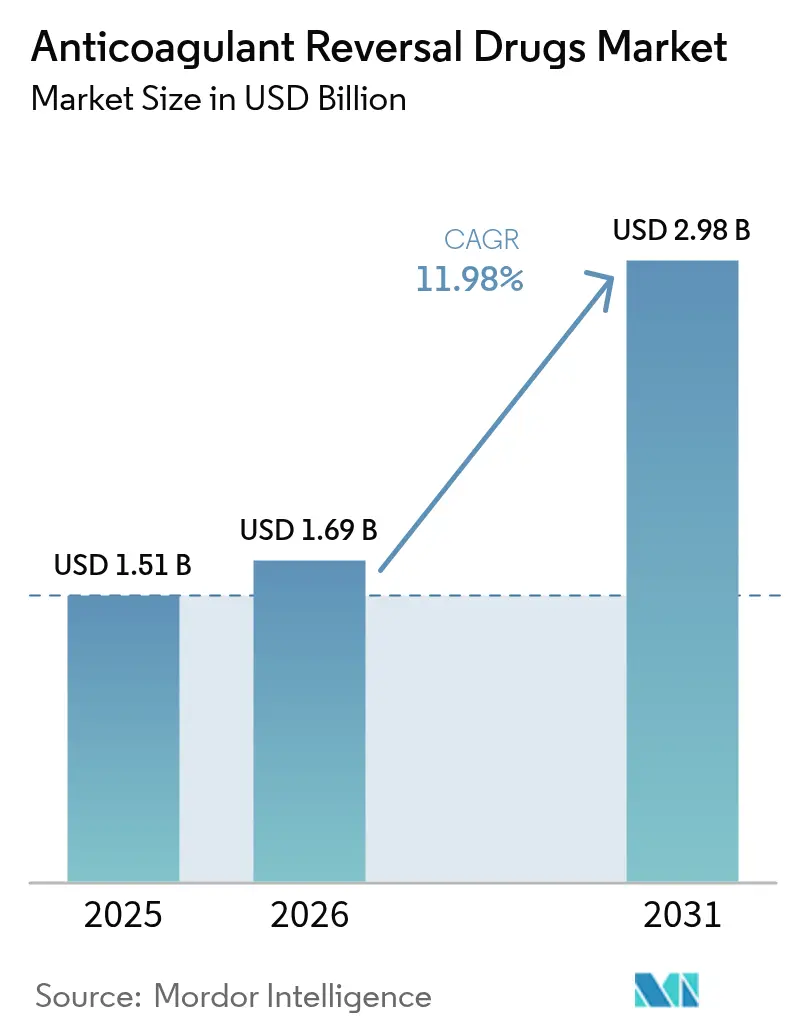

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 11.98% CAGR |

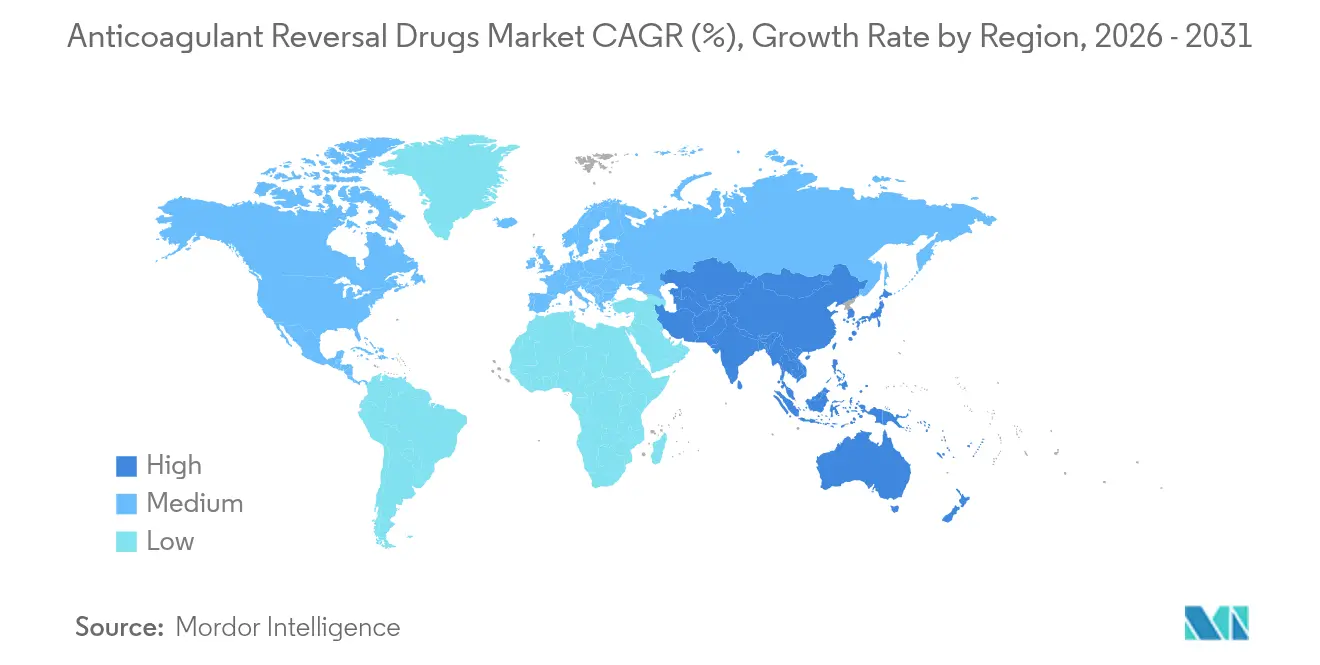

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anticoagulant Reversal Drugs Market Analysis by Mordor Intelligence

anticoagulant reversal drugs market size in 2026 is estimated at USD 1.69 billion, growing from 2025 value of USD 1.51 billion with 2031 projections showing USD 2.98 billion, growing at 11.98% CAGR over 2026-2031. Growth stems from greater adoption of direct oral anticoagulants (DOACs), an expanding elderly population, and faster regulatory approvals that shorten time-to-market for new reversal agents. Hospitals are widening DOAC-first protocols, which in turn heighten demand for rapid, specific reversal solutions. Rising use of AI-driven coagulation diagnostics is improving bleed detection and guiding earlier intervention, while on-shored plasma collection strengthens prothrombin complex concentrate (PCC) supply resilience. Competitive momentum intensified after Novartis secured abelacimab, a Factor XI inhibitor linked to 67% bleeding reduction compared with rivaroxaban, signalling a shift toward next-generation agents that could further reposition the anticoagulant reversal drugs market.

Key Report Takeaways

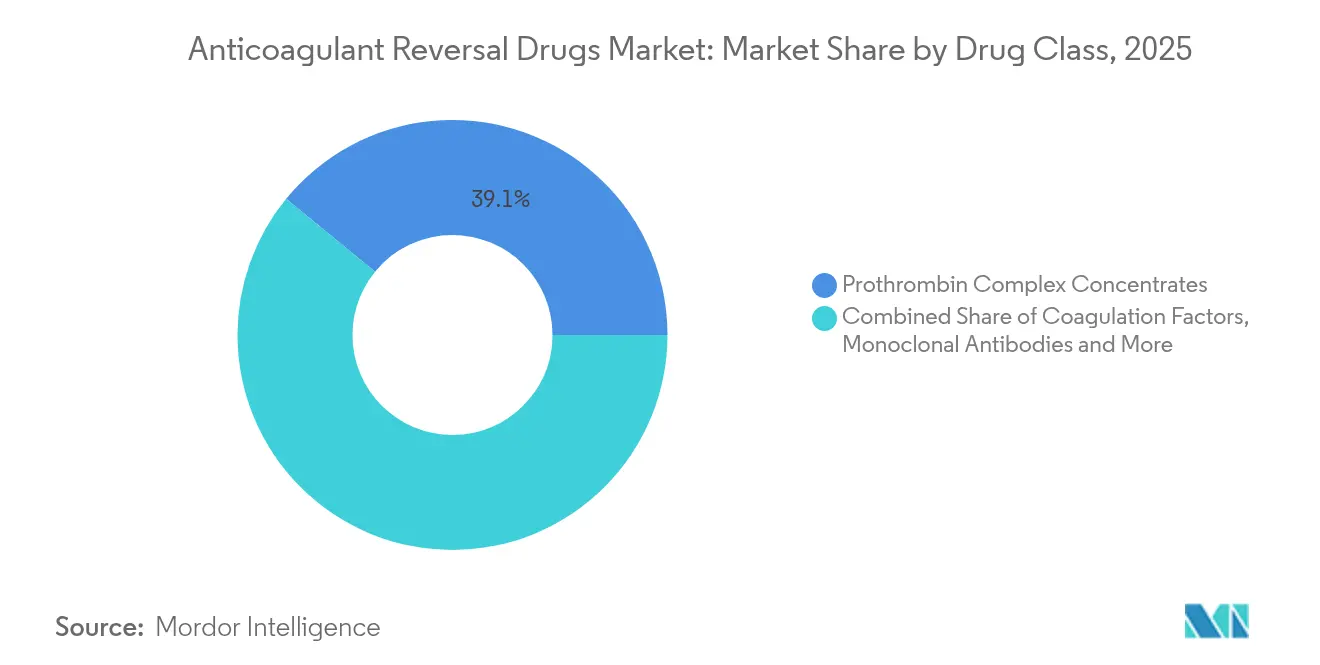

- By drug class, prothrombin complex concentrates led with 39.08% of anticoagulant reversal drugs market share in 2025, whereas recombinant decoy proteins are projected to expand at a 14.07% CAGR through 2031.

- By indication, life-threatening bleeding accounted for 46.93% of the anticoagulant reversal drugs market size in 2025, while elective surgery is advancing at a 13.61% CAGR toward 2031.

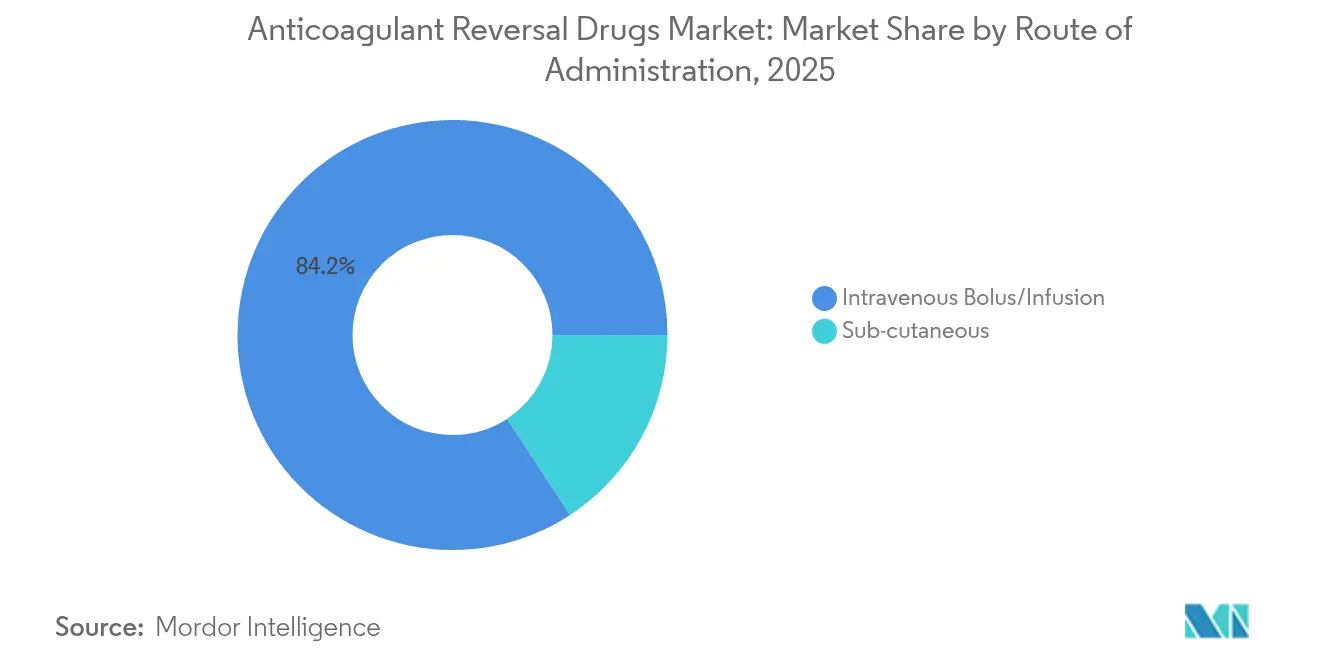

- By route of administration, intravenous products commanded 84.22% revenue in 2025; subcutaneous formulations record the highest 19.02% CAGR forecast.

- By end user, hospital pharmacies held 62.02% share in 2025, yet ambulatory surgery centers exhibit a 12.97% CAGR to 2031.

- By geography, North America captured 41.32% revenue in 2025; Asia-Pacific is the fastest-growing region at 14.24% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anticoagulant Reversal Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & rising blood-borne disorders | +2.8% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Accelerated US FDA/EMA fast-track approvals | +1.9% | North America & Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Hospital adoption of DOAC-first protocols | +2.1% | Global, led by developed markets | Medium term (2-4 years) |

| AI-driven coagulation diagnostics | +1.4% | Initially North America & Europe, expanding worldwide | Long term (≥ 4 years) |

| Supply-chain on-shoring of plasma-derived PCCs | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Rising Prevalence of Blood-Borne Disorders

Growing life expectancy pushes atrial fibrillation prevalence to 9% among those over 80 years, increasing chronic exposure to anticoagulants and heightening reversal needs. Hospitals now embed geriatric-specific anticoagulation pathways that guarantee availability of multiple reversal options for elderly patients who often cycle through varied regimens. This demographic shift elevates the strategic value of stocking both broad-spectrum PCCs and targeted agents for DOAC-associated bleeds.

Accelerated US FDA/EMA Fast-Track Approvals

Regulators prioritize unmet urgency over traditional timelines; andexanet alfa advanced under accelerated approval, while MK-2060 gained Fast Track status in 2025, cutting typical development windows from 8–12 years to roughly 5–7 years. The European Medicines Agency now accepts surrogate endpoints and real-world evidence for life-saving reversal therapies, allowing firms with robust data packages to capture early-mover advantage.

Hospital Adoption of DOAC-First Protocols Driving Demand for Reversal Agents

Emergency departments report DOAC-related bleeds comprising 35–40% of anticoagulant hemorrhages, up from 15–20% five years earlier. As hospitals pivot to DOACs for predictable kinetics, formularies accept premium-priced antidotes such as andexanet alfa and idarucizumab despite cost gaps versus PCCs, especially in Level 1 trauma centers where rapid reversal affects outcomes.

AI-Driven Coagulation Diagnostics Enabling Earlier Reversal Intervention

Machine-learning models integrating anti-Factor Xa, thrombin generation, and platelet metrics now surpass conventional tools in detecting patients needing reversal, facilitating proactive antidote ordering directly from electronic health records. Such systems minimize treatment delays and guide dose accuracy, reducing wastage of high-priced agents while improving bleed control[1]Abdulrahman Al Raizah, “Artificial intelligence in thrombosis: transformative potential and emerging challenges,” Thrombosis Journal, doi.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel agents | -2.3% | Global; pronounced in emerging markets | Medium term (2-4 years) |

| Thrombo-embolic risk & black-box warnings | -1.6% | Global; regulatory focus in North America & Europe | Long term (≥ 4 years) |

| Competition from point-of-care devices | -0.9% | Developed markets first, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel Agents

Andexanet alfa costs USD 25,000–50,000 per treatment, a 10–25 fold premium over PCCs, prompting insurers to impose prior-authorization hurdles and emerging-market hospitals to restrict use. Economic models still debate net savings relative to reduced ICU stays, slowing adoption despite proven anti-Factor Xa reversal efficacy.

Thrombo-Embolic Risk & Black-Box Warnings

A 10.3% post-treatment thrombosis rate with andexanet alfa versus 5.6% in usual care underscores the therapeutic dilemma of trading bleed control for clot risk. Guidelines require intensive monitoring and may further narrow indications if future surveillance echoes early safety concerns[2]Stuart J. Connolly, “Andexanet for Factor Xa Inhibitor–Associated Acute Intracerebral Hemorrhage,” New England Journal of Medicine, nejm.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: PCCs Anchor the Market While Decoy Proteins Accelerate

Prothrombin complex concentrates generated the largest revenue in 2025, holding 39.08% of anticoagulant reversal drugs market share, buoyed by decades of clinical familiarity and recent approval of Balfaxar that ensures diversified domestic supply. Hospitals value PCC versatility across warfarin and certain off-label DOAC emergencies, cementing a stable baseline within the anticoagulant reversal drugs market.

Recombinant decoy proteins such as andexanet alfa headline the fastest-growing cohort with a projected 14.07% CAGR through 2031. Their precise neutralization of Factor Xa inhibitors positions them as the contemporary standard for specific DOAC reversal, albeit at a high cost. Monoclonal antibodies could follow a similar trajectory once abelacimab concludes late-stage trials, potentially reshaping competitive hierarchies inside the anticoagulant reversal drugs market.

By Indication: Life-Threatening Bleeds Dominate, Elective Surgery Gains Traction

Life-threatening hemorrhage accounted for 46.93% of the anticoagulant reversal drugs market size in 2025, as rapid antidote access remains vital for intracranial, gastrointestinal, and trauma-related bleeds. Emergency clinicians prioritize agents with short onset and proven hemostatic efficacy, sustaining robust utilization across stroke centers and trauma networks.

Elective surgery posts the highest 13.61% CAGR, reflecting wider adoption of prophylactic reversal in planned cardiac or neurological procedures where anticoagulant continuation elevates bleed risk. Protocolized peri-operative management increases predictable demand and encourages manufacturers to explore longer-acting formulations suitable for scheduled care, thereby adding depth to the anticoagulant reversal drugs market.

By Route of Administration: Intravenous Prevails, Subcutaneous Innovation Emerges

Intravenous delivery remained dominant at 84.22% revenue in 2025, offering immediate bioavailability necessary for emergency scenarios. Combined with rapid coagulation assays, IV agents align with critical-care workflows, reinforcing market longevity of current formulations.

Subcutaneous routes, though nascent, are advancing at a 19.02% CAGR. Autoinjector designs and depot technologies aim to decentralize reversal into outpatient settings, supporting chronic anticoagulation management where delayed yet sustained reversal may suffice. These innovations could unlock new patient segments and diversify revenue streams inside the anticoagulant reversal drugs market.

By End User: Hospital Pharmacies Steer Procurement, Ambulatory Centers Rise

Hospital pharmacies held 62.02% share in 2025, orchestrating formulary reviews, bulk contracting, and emergency distribution. Their central role in stewardship decisions makes them pivotal gatekeepers for any entrant aspiring to scale within the anticoagulant reversal drugs market.

Ambulatory surgery centers record a 12.97% CAGR, mirroring the shift toward outpatient orthopedics, cardiovascular implants, and minimally invasive procedures. As these facilities take on higher-acuity cases, they adopt reversal agents to mitigate peri-operative bleeds, gradually broadening the anticoagulant reversal drugs market beyond tertiary hospitals.

Geography Analysis

North America delivered 41.32% of global revenue in 2025, supported by FDA-guided protocols that favor specific reversal agents and strong reimbursement for premium-priced products. Level 1 trauma systems and comprehensive stroke networks uphold steady consumption, while Health Canada’s 2024 clearance of Ondexxya widened continental access.

Asia-Pacific is projected to outpace all regions at 14.24% CAGR. Japan’s approval of Ondexxya, rising DOAC usage in China and India, and cardiovascular disease prevalence across urbanizing economies are converging forces expanding the anticoagulant reversal drugs market. National databases such as South Korea’s highlight major bleeding incidence that reinforces policy mandates for antidote availability.

Europe remains stable with coordinated EMA guidance and mature plasma supply chains backing PCC production. Germany, the United Kingdom, and France adopt cost-effectiveness metrics, compelling manufacturers to pair clinical evidence with economic value propositions. Middle East & Africa trail but represent white-space potential as tertiary-care capacity grows, albeit tempered by pricing constraints that currently limit widespread penetration of next-generation agents.

Competitive Landscape

The anticoagulant reversal drugs market shows moderate concentration, with established firms—CSL Behring, Pfizer, and others—leveraging scale and regulatory acumen to protect PCC and decoy protein franchises. The February 2025 acquisition of Anthos Therapeutics by Novartis for USD 925 million marked a decisive entry into Factor XI inhibitor territory, reinforcing strategic emphasis on therapies that reduce bleeding risk and, by extension, reshape reversal demand curves.

Competitive advantage increasingly depends on mechanism specificity, safety differentiation, and real-world evidence that supports payer adoption. Andexanet alfa sustains share despite premium pricing because its targeted action on Factor Xa inhibitors aligns with hospital quality benchmarks. Meanwhile, PCC suppliers invest in supply-chain resilience and pricing flexibility to preserve incumbency against novel entrants.

Emerging battlegrounds include pediatric labeling, integrated diagnostic-therapeutic platforms, and combination agents capable of neutralizing multiple anticoagulant classes simultaneously. Partnerships with AI analytics firms aim to embed dosing algorithms into electronic records, transforming standalone products into service-oriented solutions that deepen clinical integration within the anticoagulant reversal drugs market.

Anticoagulant Reversal Drugs Industry Leaders

Pfizer Inc

Octapharma AG

CSL Behring Limited

Boehringer Ingelheim Pharma GmbH

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Octapharma USA launched Balfaxar, a non-activated four-factor PCC approved for urgent reversal of vitamin K antagonist–induced deficiencies.

- August 2024: SFJ Pharmaceuticals announced FDA priority review of bentracimab BLA, a monoclonal antibody fragment targeting ticagrelor reversal.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the anticoagulant reversal drugs market as every branded or generic agent that quickly neutralizes oral or injectable anticoagulants during major bleeds or before unplanned surgery. Counted products are prothrombin complex concentrates, vitamin K, protamine, idarucizumab, andexanet alfa, and emerging recombinant decoy proteins dispensed through hospital, retail, and online pharmacies.

Scope exclusion: mechanical hemostatic devices and routine blood transfusions.

Segmentation Overview

- By Drug Class

- Prothrombin Complex Concentrates

- Coagulation Factors

- Monoclonal Antibodies

- Recombinant Decoy Proteins

- Phytonadione

- Other Classes

- By Indication

- Life-threatening Bleeding

- Emergency Surgery

- Elective Surgery

- By Route of Administration

- Intravenous Bolus/Infusion

- Sub-cutaneous

- By End User

- Hospital Pharmacies

- Emergency Departments/Trauma Centers

- Retail Pharmacies

- Ambulatory Surgery Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews with hospital pharmacists, trauma physicians, and payer formulary managers across North America, Europe, and Asia-Pacific tested dose norms, price bands, and uptake triggers, letting us ground secondary findings in bedside reality.

Desk Research

We, the Mordor analyst team, sized the treated-bleed pool using WHO mortality tables, CDC emergency-visit logs, and Eurostat discharges. FDA and EMA approval files dated launches, while company 10-Ks, investor decks, and D&B Hoovers snapshots signaled revenue. ClinicalTrials.gov listings and International Society on Thrombosis and Haemostasis papers mapped pipeline pace and guideline shifts. These references are illustrative; many other open sources aided validation.

Market-Sizing & Forecasting

Our top-down model multiplies the global anticoagulated population, the annual major-bleed rate, and the share treated with a reversal drug, then applies a weighted average selling price. Supplier roll-ups and sampled hospital invoices give bottom-up guardrails. Five-year projections employ multivariate regression that flexes direct oral anticoagulant penetration, growth of citizens over 65, elective-surgery backlog, emergency-bleed visits, and new approvals, with scenarios vetted by our primary experts.

Data Validation & Update Cycle

Outputs clear variance flags, peer review, and senior sign-off. Reports refresh annually, with interim updates after label changes, safety recalls, or large mergers.

Why Mordor's Anticoagulant Reversal Drugs Baseline Commands Reliability

Published values differ because other firms narrow product baskets, freeze older base years, or skip currency rebasing.

By refreshing 2025 data against clinical incidence and supplier revenue, Mordor Intelligence provides a balanced baseline that decision-makers trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.51 B, 2025 | Mordor Intelligence | - |

| USD 1.38 B, 2024 | Global Consultancy A | Leaves out protamine and retail sales |

| USD 1.30 B, 2024 | Industry Journal B | Uses 2023 FX and lacks Asia-Pacific hospitals |

These contrasts show that by tying every assumption to traceable variables and updating promptly, we deliver the surest baseline for strategy.

Key Questions Answered in the Report

What is the current size of the anticoagulant reversal drugs market?

The anticoagulant reversal drugs market size stood at USD 1.69 billion in 2026 and is projected to reach USD 2.98 billion by 2031.

Which drug class leads global revenue?

Prothrombin complex concentrates held 39.08% of global revenue in 2025, making them the dominant drug class.

Which region is growing the fastest?

Asia-Pacific is forecast to grow at a 14.24% CAGR between 2026 and 2031, the quickest pace among all regions.

Why are costs a major restraint?

Novel agents such as andexanet alfa cost USD 25,000–50,000 per episode—up to 25 times more than PCCs—triggering strict payer controls and slowing adoption.

What impact did Novartis’ acquisition of Anthos Therapeutics have?

The USD 925 million purchase secured abelacimab, a Factor XI inhibitor that reduces bleeding by 67%, signalling a strategic pivot toward next-generation agents and intensifying competition.

Page last updated on: