PARP Inhibitor Biomarkers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

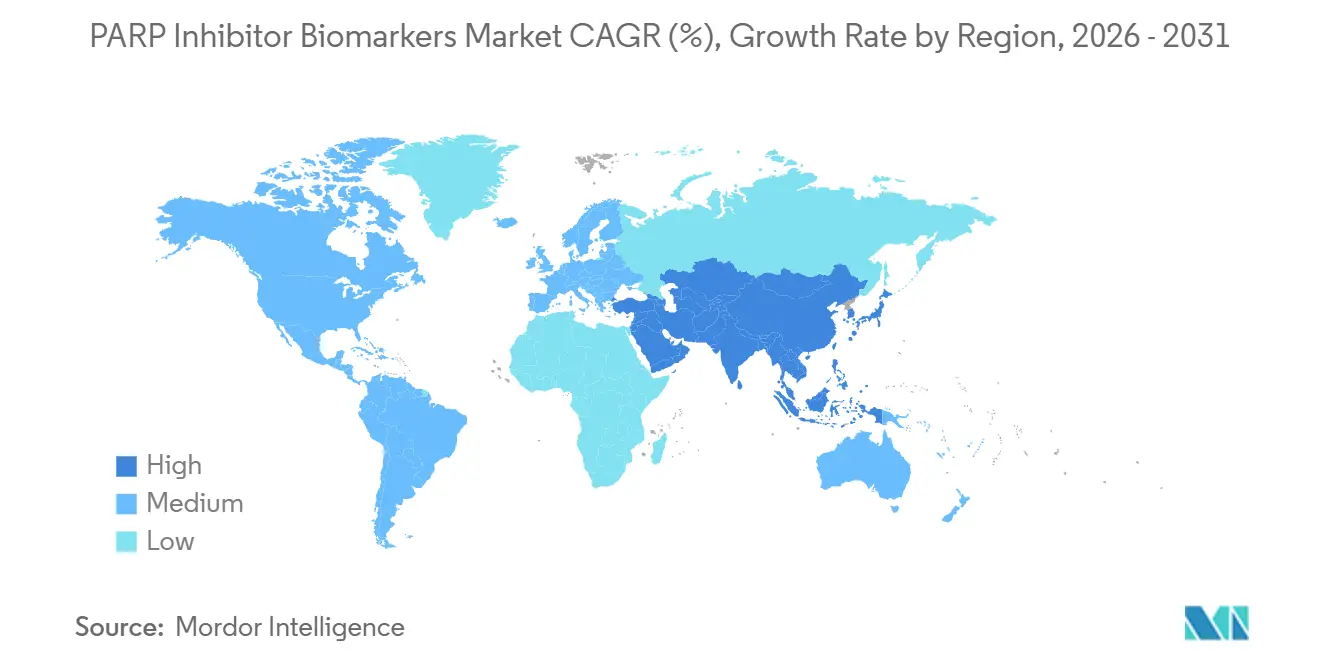

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PARP Inhibitor Biomarkers Market Analysis by Mordor Intelligence

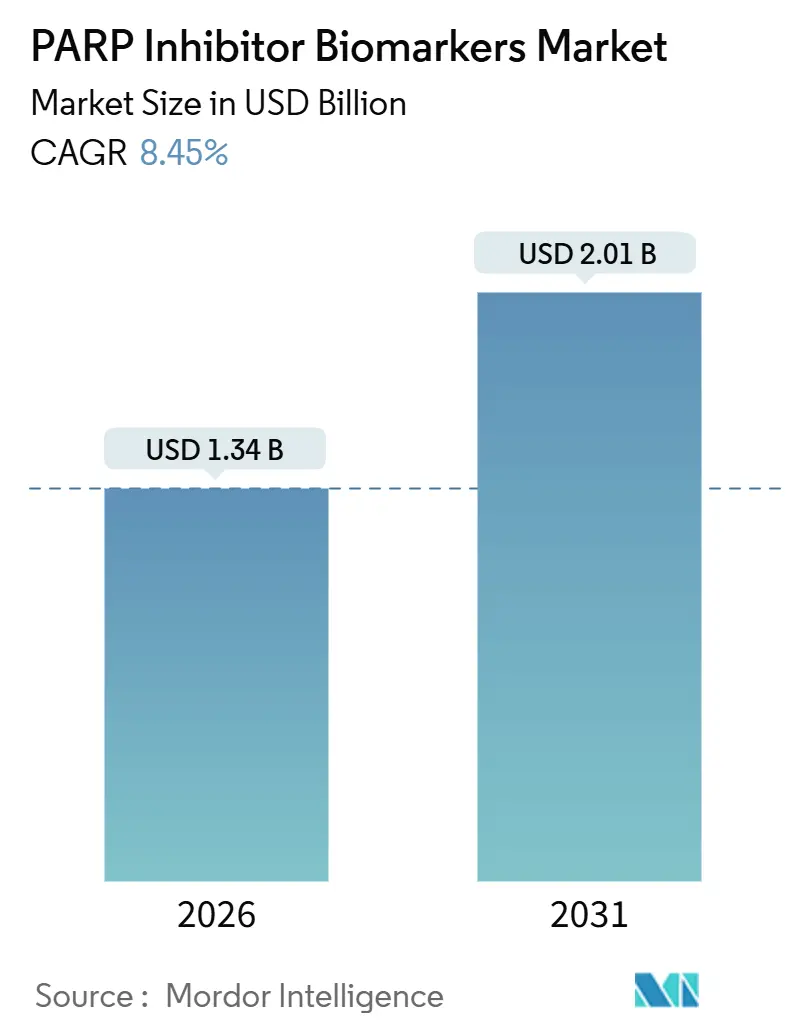

The PARP Inhibitor Biomarkers Market size is estimated at USD 1.34 billion in 2026, and is expected to reach USD 2.01 billion by 2031, at a CAGR of 8.45% during the forecast period (2026-2031).

Steady regulatory tailwinds, payer support for precision-oncology workflows, and rapid clinical adoption of liquid biopsy solutions continue to underpin this expansion. The November 2025 FDA proposal to move oncology NGS tests from Class III to Class II is shortening launch timelines, letting smaller laboratories compete head-to-head with entrenched reference centers. At the same time, FoundationOne Liquid CDx’s clearance for BRCA testing in metastatic prostate cancer has validated ctDNA assays across new tumor types, boosting demand for serial testing models. Falling sequencing costs, exemplified by USD 200 whole genomes on NovaSeq X Plus, are helping community hospitals internalize testing and retain interpretation revenue.[1]Illumina, “NovaSeq X Plus Sequencing Platform,” illumina.com Finally, global payer policies that link reimbursement to actionable genomic results are cementing BRCA/HRD testing as a routine element of PARP inhibitor prescribing decisions.[2]Centers for Medicare & Medicaid Services, “National Coverage Determination for NGS,” cms.gov

Key Report Takeaways

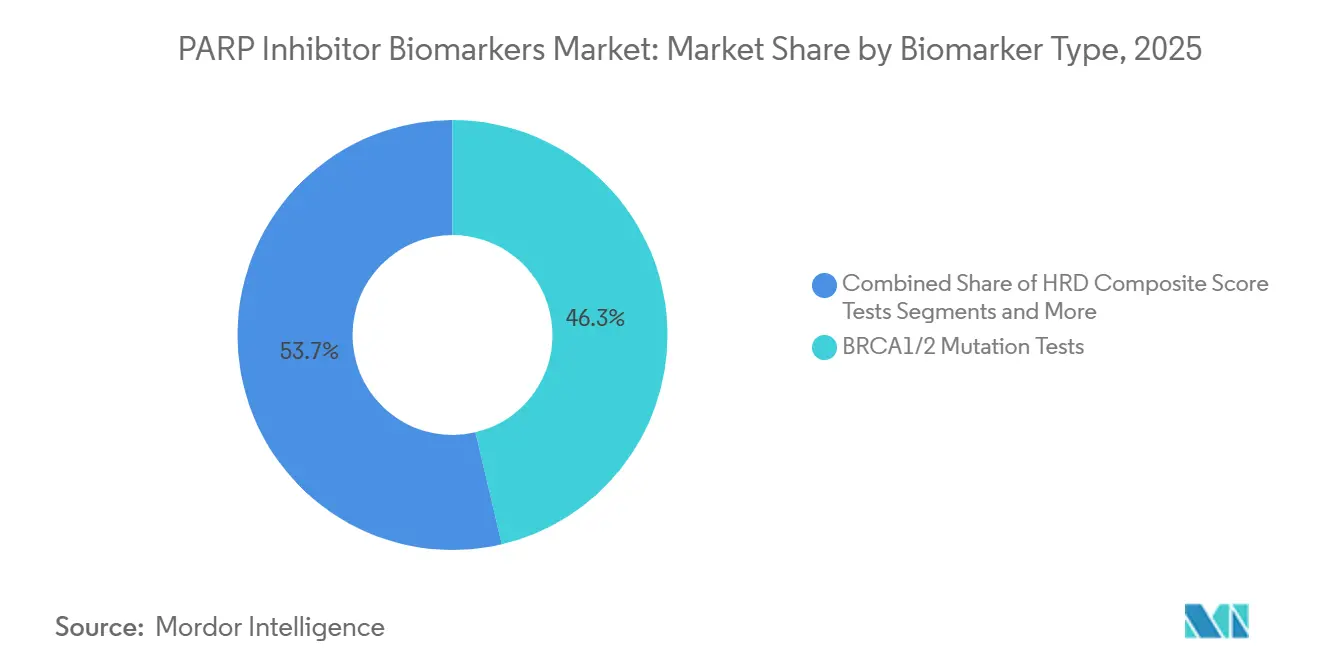

- By biomarker type, BRCA1/2 mutation tests held 46.32% of the PARP inhibitor biomarkers market share in 2025; ctDNA-based BRCA/HRD assays are projected to expand at an 11.34% CAGR through 2031.

- By technology platform, NGS commanded 59.44% revenue share in 2025, while digital PCR is poised to post the fastest 12.55% CAGR to 2031.

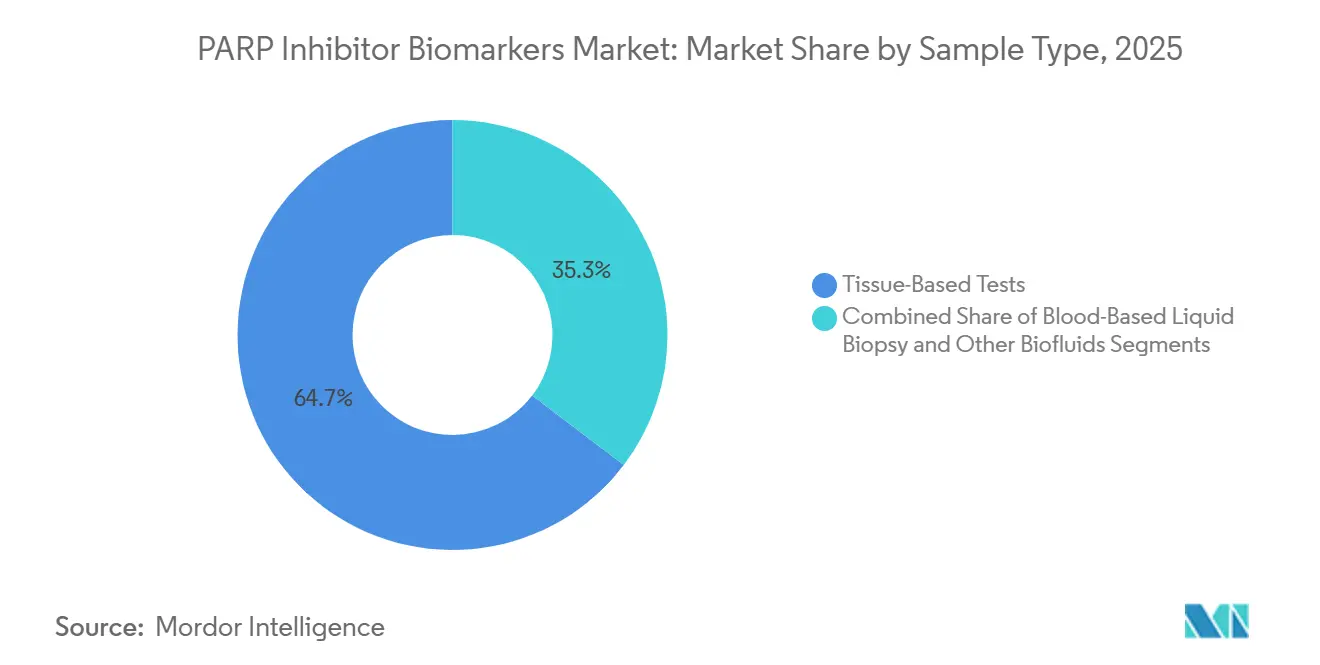

- By sample, tissue-based assays contributed 64.66% of the PARP inhibitor biomarkers market size in 2025; blood-based liquid biopsy is forecast to grow at 11.45% CAGR.

- By cancer type, ovarian testing represented 36.36% revenue in 2025, whereas prostate cancer is anticipated to grow at a 10.63% CAGR.

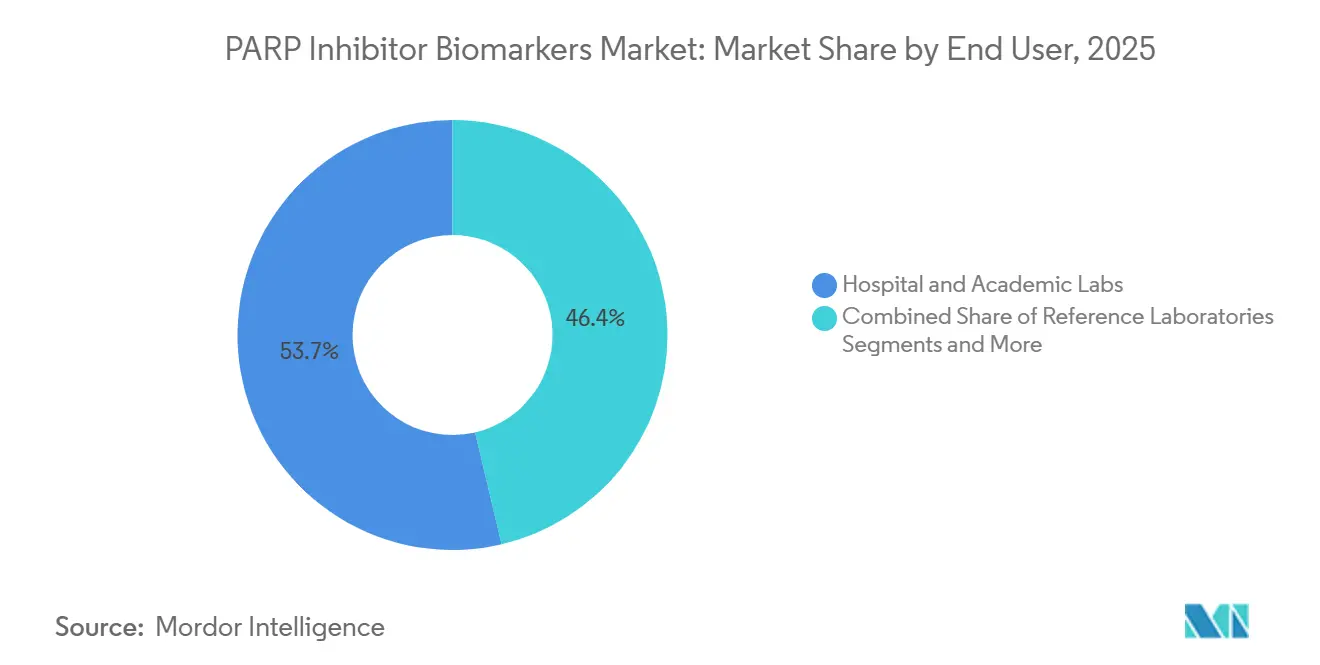

- By end user, hospital and academic labs controlled 53.65% share of the PARP inhibitor biomarkers market size in 2025; point-of-care settings will log an 11.41% CAGR through 2031.

- North America captured 44.64% of revenue in 2025 while Asia is set to deliver the quickest 10.76% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PARP Inhibitor Biomarkers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory approvals of PARP-linked CDx | +1.8% | North America and Europe | Medium term (2-4 years) |

| Expanding BRCA/HRD testing volumes | +1.5% | Global, with fast uptake in Asia-Pacific | Long term (≥ 4 years) |

| Declining NGS costs & wider lab adoption | +1.2% | Global, concentrated in high-volume reference centers | Short term (≤ 2 years) |

| FDA “class-label” guidance on multi-drug CDx | +0.9% | North America with spillover to EU and APAC | Medium term (2-4 years) |

| Liquid-biopsy repeat-testing revenues | +1.1% | North America and Europe, emerging in Asia | Medium term (2-4 years) |

| Payer acceptance of precision-oncology value | +0.8% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Approvals Of PARP-Linked Companion Diagnostics

Continuous FDA and EMA endorsements are accelerating commercial timelines. The August 2024 clearance of FoundationOne Liquid CDx for BRCA testing in metastatic prostate cancer opened a fresh revenue stream outside ovarian and breast settings. Europe followed with niraparib plus myChoice CDx in February 2025, ensuring trans-Atlantic alignment.[3]European Medicines Agency, “Niraparib with myChoice CDx Endorsed,” ema.europa.eu November 2025 draft rules to down-classify oncology NGS devices promise six-month 510(k) reviews, enlarging the field of eligible developers. The cumulative uplift is visible in the 1.8-percentage-point addition to growth, especially in the United States where clear pathways de-risk investment.

Rising BRCA/HRD Testing Volumes As PARP Labels Expand

NCCN’s universal BRCA testing recommendation for metastatic prostate cancer doubled the addressable testing pool in 2024. NICE’s green light for adjuvant olaparib in early-stage breast cancer extended genomic profiling into a curative setting. China’s late-2024 requirement that hospitals run companion diagnostics before reimbursing olaparib further widened uptake. Together, these changes add 1.5 percentage points to the forecast CAGR.

Declining NGS Costs & Lab Adoption

The NovaSeq X Plus has halved per-genome costs to USD 200, enabling regional hospitals to bring sequencing in-house. Ultima Genomics’ USD 100 target and Element Biosciences’ budget-friendly AVITI system are fuelling price competition.. Laboratories can now expand panel content without raising list prices, lifting test uptake in cost-sensitive payor environments. This price deflation contributes 1.2 percentage points to growth.

FDA “Class-Label” Guidance Enabling Multi-Drug CDx

April 2020 guidance endorsed single panels tied to several therapies, letting FoundationOne CDx claim 19 drug labels and lowering co-development spend by around 40%. Guardant360 CDx has since multiplied its gene-drug pairings five-fold without fresh pivotal trials. The approach adds 0.9 percentage points to expansion, mainly over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High test cost & uneven reimbursement | -0.7% | Global, acute in emerging and rural markets | Short term (≤ 2 years) |

| Assay standardization gaps for HRD scoring | -0.5% | North America and EU | Medium term (2-4 years) |

| Scarcity of genomics-literate workforce | -0.4% | Global, severe in APAC and Latin America | Long term (≥ 4 years) |

| Cyber-security barriers to genomic data flows | -0.3% | EU, China, and jurisdictions with strict localization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Test Cost & Uneven Reimbursement

Panels priced at USD 3,000–6,000 remain unaffordable for under-insured patients, and Medicaid often limits coverage to single-gene assays. Emerging economies face sharper disparities, with India reimbursing only USD 180 against reagent costs that exceed this figure many-fold. Prior authorization delays further erode timely access, contributing a -0.7 point drag.

Assay Standardization Gaps For HRD Scoring

Discordance of up to 20% between myChoice CDx and FoundationFocus thresholds undermines payer confidence and complicates trial enrollment. Lack of FDA-mandated reference standards holds back harmonization, shaving 0.5 percentage points from projected gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Biomarker Type: Liquid Biopsy Drives Serial Monitoring

BRCA1/2 mutation assays delivered 46.32% revenue in 2025, reflecting their mature clinical utility and multiple drug labels, while ctDNA-based BRCA/HRD panels are expected to climb at an 11.34% CAGR. HRD composite scoring added nearly 28% share thanks to its ability to capture non-BRCA homologous-repair defects. RAD51 functional testing and emerging markers such as SLFN11 stay niche but remain strategic for next-generation trials aimed at broadening the PARP inhibitor biomarkers market. Growing adoption of tumor-agnostic NGS panels that read hundreds of genes in one run aligns with payer interest in maximizing therapeutic matches from a single specimen.

Follow-up liquid biopsy every three months creates an annuity-like revenue stream and helps clinicians catch BRCA reversion mutations tied to treatment resistance. This repeat-testing proposition gives blood-based assays a structural growth advantage that will keep expanding the PARP inhibitor biomarkers market size through the decade.

By Technology Platform: Digital PCR Challenges NGS Turnaround

NGS retained a 59.44% share in 2025 on the strength of broad content and falling per-sample costs, but digital PCR is projected to log the quickest 12.55% CAGR as clinicians demand sub-0.1% allele-frequency sensitivity for minimal-residual-disease use cases. PCR’s 24-hour reporting cycle now supports same-day therapy initiation in newly diagnosed metastatic disease. Laboratories increasingly pair rapid PCR hotspot screens with reflex NGS for HRD scoring in negative cases, marrying speed with depth—an approach that keeps both modalities central to the PARP inhibitor biomarkers market.

By Sample Type: Blood Collection Expands Access

Tissue remained the dominant 64.66% sample in 2025, yet blood-based testing should carve out double-digit growth thanks to FDA draft guidance that formalized ctDNA’s role in curative-intent monitoring. The convenience of peripheral draws, ubiquity of phlebotomy services, and ability to track tumor evolution longitudinally are converting oncologists and payers alike. Urine and other fluids are emerging but still represent under 2% of the PARP inhibitor biomarkers market.

By Cancer Type: Prostate Leads Growth Curve

Ovarian cancer still contributed 36.36% of 2025 revenue, although prostate testing is charging ahead at a 10.63% CAGR following the FDA’s extension of BRCA liquid biopsy labeling to mCRPC. Breast cancer continues to expand into the adjuvant setting, and pancreatic testing is gaining momentum as maintenance strategies mature. New tumor-agnostic approvals could further diversify revenue streams and lift the overall PARP inhibitor biomarkers market.

By End User: Point-of-Care Models Gain Steam

Hospital and academic centers generated most 2025 sales, but point-of-care platforms able to return BRCA hotspot calls inside two hours are set to post an 11.41% CAGR. Community oncology clinics prefer in-office solutions that eliminate the seven-day wait tied to send-out NGS, an evolution that supports broader penetration of the PARP inhibitor biomarkers market.

Geography Analysis

North America retained 44.64% of 2025 turnover as CMS coverage, community-practice drug uptake, and the FDA’s class-label clarity kept the United States the launch pad for new assays. Canada is harmonizing reimbursement, though provincial disparities linger, while Mexico’s formulary addition of olaparib is seeding test demand despite laboratory capacity gaps.

Europe's EMA coordinated approval of niraparib plus myChoice CDx and NICE’s early-stage breast cancer endorsement are pushing test volumes, yet divergent reimbursement—Germany funds EUR 5,000 panels while Spain caps single-gene tests at EUR 300—creates an uneven growth map.

Asia-Pacific is the fastest riser with a 10.76% CAGR to 2031. China’s compulsory CDx reimbursement rule tied to olaparib and Japan’s JPY 560,000 national fee for genomic profiling are catalyzing investment. India and parts of Southeast Asia remain constrained by low public-insurance outlays, although private labs continue to import small but growing volumes of NGS reagents.

The Middle East, Africa, and South America collectively remain low of revenue. Saudi Arabia’s Vision 2030 initiative earmarks USD 1.2 billion for genomics; Brazil is close to finalizing CDx reimbursement for olaparib, and the UAE is positioning itself as a regional testing hub, steps that could lift future contributions.

Competitive Landscape

Foundation Medicine, Myriad Genetics, and Guardant Health controlled a high share of 2025 revenue, leveraging multi-drug CDx labels, exclusive pharma contracts, and nationwide payer deals. Guardant’s seven-day ctDNA turnaround is eroding tissue NGS share, while Myriad’s value-based contract with payers illustrates new risk-sharing economics. Tempus Labs and Caris Life Sciences use AI to shorten curation, with 98% concordance to expert pathologists achieved in 2024. Burning Rock’s aggressive USD 1,100 comprehensive panel pricing helped it seize 8% of China’s market in 2024, marking a potential blueprint for other regional entrants.

Pharma is pivoting toward vertical integration: AstraZeneca inked a 2024 deal with Illumina to embed CDx development within its clinical programs, threatening to disintermediate independent labs. Meanwhile, Roche’s December 2025 FDA win for rucaparib-nivolumab set the stage for combination regimens that could multiply test volumes as clinicians verify dual-mechanism eligibility.

Emerging white spaces include point-of-care BRCA assays delivering results in under four hours, CRISPR-based detection kits now flush with USD 50 million in VC backing, and novel biomarkers such as SLFN11 that promise to pull additional patients into the PARP inhibitor biomarkers market.

PARP Inhibitor Biomarkers Industry Leaders

Myriad Genetics

Foundation Medicine

F. Hoffmann-La Roche AG

NeoGenomics

Invitae

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Roche secured FDA approval for rucaparib plus nivolumab in BRCA-mutated metastatic prostate cancer, expanding FoundationOne CDx labels.

- December 2025: FDA proposed reclassifying oncology NGS tests to Class II, cutting review times to six months

- August 2025: GSK launched Zejula in India as first-line monotherapy for ovarian cancer irrespective of biomarker status.

- June 2025: Johnson & Johnson reported Phase 3 AMPLITUDE data showing niraparib plus abiraterone benefits in mCSPC with HRR alterations.

Global PARP Inhibitor Biomarkers Market Report Scope

PARP (Poly [ADP-ribose] polymerase) inhibitor biomarkers are biological indicators used to predict, monitor, or measure a patient's response to PARP inhibitor therapy, a targeted cancer treatment.

The PARP Inhibitor Biomarkers Market Report is segmented by Biomarker Type, Technology Platform, Sample Type, Cancer Type, End User, and Geography. By Biomarker Type, the market is segmented into BRCA1/2 Mutation Tests, HRD Composite Score Tests, RAD51 Functional Assays, ctDNA‑based BRCA/HRD Tests, and Emerging Markers. By Technology Platform, the market is segmented into Next-Generation Sequencing, PCR, Immunohistochemistry, In Situ Hybridisation, and Others. By Sample Type, the market is segmented into Tissue-Based Tests, Blood-Based Liquid Biopsy, and Other Biofluids. By Cancer Type, the market is segmented into Ovarian, Breast, Prostate, Pancreatic, and Others. By End User, the market is segmented into Hospital & Academic Labs, Reference Laboratories, Cancer Research Institutes, and Point-of-Care Settings. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| BRCA1/2 Mutation Tests |

| HRD Composite Score Tests |

| RAD51 Functional Assays |

| ctDNA-based BRCA/HRD Tests |

| Emerging Markers (SLFN11 etc.) |

| Next-Generation Sequencing |

| PCR (qPCR/dPCR) |

| Immunohistochemistry |

| In Situ Hybridisation |

| Others (CRISPR-based etc.) |

| Tissue-Based Tests |

| Blood-Based Liquid Biopsy |

| Other Biofluids |

| Ovarian Cancer |

| Breast Cancer |

| Prostate Cancer |

| Pancreatic Cancer |

| Others |

| Hospital & Academic Labs |

| Reference Laboratories |

| Cancer Research Institutes |

| Point-of-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Biomarker Type | BRCA1/2 Mutation Tests | |

| HRD Composite Score Tests | ||

| RAD51 Functional Assays | ||

| ctDNA-based BRCA/HRD Tests | ||

| Emerging Markers (SLFN11 etc.) | ||

| By Technology Platform | Next-Generation Sequencing | |

| PCR (qPCR/dPCR) | ||

| Immunohistochemistry | ||

| In Situ Hybridisation | ||

| Others (CRISPR-based etc.) | ||

| By Sample Type | Tissue-Based Tests | |

| Blood-Based Liquid Biopsy | ||

| Other Biofluids | ||

| By Cancer Type | Ovarian Cancer | |

| Breast Cancer | ||

| Prostate Cancer | ||

| Pancreatic Cancer | ||

| Others | ||

| By End User | Hospital & Academic Labs | |

| Reference Laboratories | ||

| Cancer Research Institutes | ||

| Point-of-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the PARP inhibitor biomarkers market in 2031?

The market is expected to reach USD 2.01 billion by 2031.

Which biomarker type holds the largest revenue share today?

BRCA1/2 mutation assays commanded 46.32% of 2025 sales.

Which region is growing fastest for PARP inhibitor biomarker testing?

Asia-Pacific is forecast to register a 10.76% CAGR through 2031.

How does liquid biopsy influence repeat-testing revenue?

Quarterly ctDNA monitoring can generate eight billable tests over two years, quadrupling revenue relative to a single tissue assay.

What regulatory change could most impact new assay launches?

FDA’s proposal to shift oncology NGS tests to the Class II 510(k) pathway is set to cut review times from 18 months to six.

Page last updated on: