Global Animal Biotechnology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

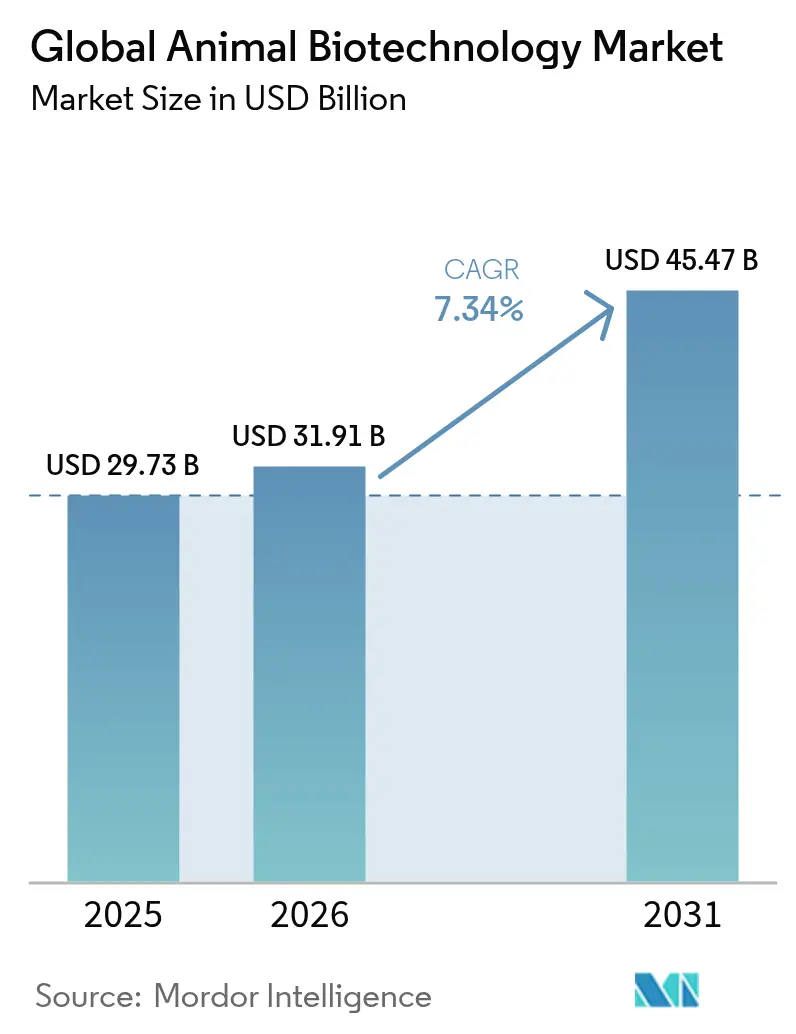

| Market Size (2026) | USD 31.91 Billion |

| Market Size (2031) | USD 45.47 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Animal Biotechnology Market Analysis by Mordor Intelligence

The animal biotechnology market size is expected to grow from USD 29.73 billion in 2025 to USD 31.91 billion in 2026 and is forecast to reach USD 45.47 billion by 2031 at 7.34% CAGR over 2026-2031. Demand originates from precision gene-editing breakthroughs, AI-guided breeding programs, and rapid in-clinic molecular tests that shorten disease-response times. Regulatory green lights, typified by the FDA’s first approval of PRRS-resistant pigs, validate commercial paths for engineered livestock while cutting avoidable swine losses valued at USD 1.2 billion. North America’s clear rules and deep R&D capacity keep the region in front, yet Asia-Pacific, propelled by China’s brisk vaccine expansion, is closing the gap fastest. Competitive intensity is moving from traditional drugs toward platform technologies that merge diagnostics, vaccines, and data analytics, giving scale players new tools and start-ups novel entry points.

Key Report Takeaways

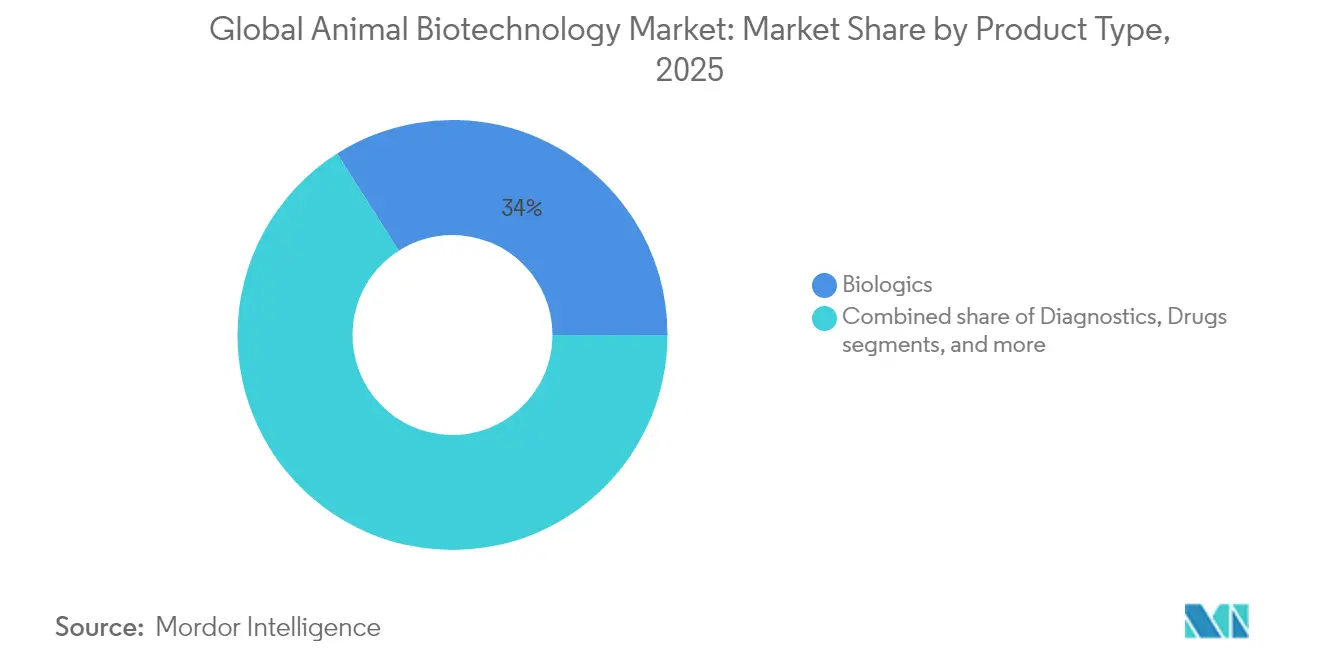

- By product type, biologics led with 34.02% of the animal biotechnology market revenue share in 2025, whereas reproductive and genetic technologies are expanding at a 8.78% CAGR to 2031.

- By application, preventive care and treatment held 73.85% of the animal biotechnology market size in 2025; disease diagnosis is advancing at a 7.62% CAGR through 2031.

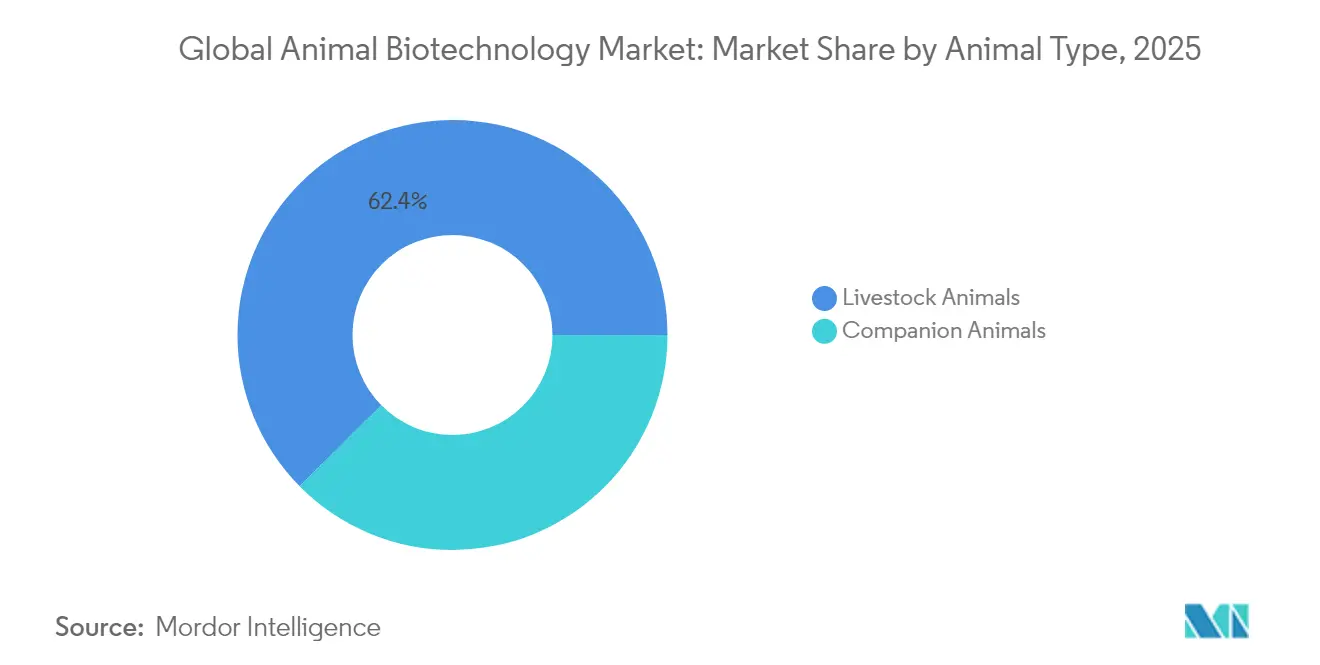

- By animal type, livestock accounted for 62.41% share of the animal biotechnology market size in 2025, while companion animals record the highest projected CAGR at 7.74% through 2031.

- By end-user, laboratories retained 35.74% share in 2025; point-of-care testing is growing at a 7.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animal Biotechnology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in CRISPR/Cas-Based Gene-Edited Livestock Programs | +1.8% | North America & EU leading, APAC emerging | Long term (≥ 4 years) |

| Expansion of AI-Enabled Precision-Breeding Platforms | +1.3% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Rising R&D Spending by Tier-1 Animal-Health Companies | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Growth in Point-of-Care Molecular Diagnostics for Zoonoses | +1.1% | Global, with accelerated adoption in APAC | Short term (≤ 2 years) |

| Demand for Thermostable Synthetic-Biology Vaccines | +0.9% | Global, particularly emerging markets | Medium term (2-4 years) |

| Regulatory Fast-Track Incentives for Antibiotic Alternatives | +0.8% | North America & EU, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in CRISPR/Cas-Based Gene-Edited Livestock Programs

The FDA’s 2025 clearance for PRRS-resistant pigs[1]PIC, “FDA Approves First Gene-Edited Pigs Resistant to PRRS,” pic.com cemented CRISPR’s shift from lab to farm, carving a proof-of-concept path that cuts recurring swine disease losses and trims antibiotic use by 5%. Expanded interest spans biopharma protein production via transgenic cattle[2]International Service for the Acquisition of Agri-biotech Applications, “Brazilian Cow Produces Human Insulin in Milk,” isaaa.org that secrete human insulin. Gene-edited organs for xenotransplant trials further blur the lines between animal health and human medicine. Regional rules differ, but scale developers with compliance budgets secure first-mover advantages that reinforce the animal biotechnology market.

Expansion of AI-Enabled Precision-Breeding Platforms

Genomic algorithms now guide embryo selection, milk-yield optimization, and climate-resilience traits in dairy and beef herds. Proprietary databases widen predictive gaps between incumbents and entrants. When coupled with gene-editing toolkits, artificial intelligence (AI) reorients breeding from iterative selection toward engineered outcomes. Data access hurdles may entrench existing breeders, yet cross-border data alliances are forming to level input depth, sustaining growth in the animal biotechnology market.

Rising R&D Spending by Tier-1 Animal-Health Companies

Zoetis raised R&D outlays while delivering USD 9.3 billion revenue in 2024, aligning budgets toward genomic and precision-medicine programs. Merck Animal Health’s SEQUIVITY RNA particle system[3]Merck Animal Health, “SEQUIVITY RNA Particle Platform,” merck-animal-health-usa.com exemplifies platform thinking that can pivot across pathogens within months. Larger coffers, plus regulatory and distribution expertise, set formidable barriers yet accelerate field innovation.

Growth in Point-of-Care Molecular Diagnostics for Zoonoses

Portable PCR and isothermal kits bring lab-grade detection into clinics, aligning with National Veterinary Associates’ 1,000-plus sites that feed real-time disease alerts into a shared platform. Fast confirmation enabled quick H5N1 vaccine rollouts after 973 dairy cattle herds were hit, supported by the Elanco-Medgene[4]PR Newswire, “Elanco and Medgene to Commercialize H5N1 Vaccine,” prnewswire.com partnership. The outcome is tighter biosecurity, lower outbreak losses, and wider uptake of biotechnology tools across the animal biotechnology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Public Opposition to Gene-Edited Food Animals | -1.4% | Global, particularly strong in EU | Long term (≥ 4 years) |

| Complex, Fragmented Global Approval Pathways | -1.1% | Global, varying by jurisdiction | Medium term (2-4 years) |

| High Bioreactor CAPEX in Emerging Markets | -0.7% | Emerging markets, APAC & MEA | Medium term (2-4 years) |

| Insurance Liability Risks for Transgenic Animal Leaks | -0.5% | Global, with varying frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Public Opposition to Gene-Edited Food Animals

Consumer sentiment skews cautious, more so in Europe. Retail bans arrive faster than formal regulations. Surveys show higher acceptance when edits cut antibiotic reliance or boost welfare, yet distrust lingers. Industry transparency campaigns aim to rebuild confidence and thus protect the animal biotechnology market.

Complex, Fragmented Global Approval Pathways

US processes revolve around molecular risk assessments whereas the EU leans on the precautionary principle. Emerging economies often lack defined statutes, extending timelines. Multinational firms absorb these costs; smaller innovators postpone launches, dampening momentum in parts of the animal biotechnology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologics Leadership Challenged by Genetic Innovation

Biologics held 34.02% of the animal biotechnology market share in 2025. Investor attention is shifting to reproductive and genetic technologies, the fastest-rising group at a 8.78% CAGR. Their surge reflects gene-editing platforms that compress development cycles and lift return profiles beyond vaccine economics. Diagnostics lines profit from clinic-based molecular tools, whereas conventional drugs face pressure from tighter antimicrobial rules. Hybrid offerings, such as SEQUIVITY’s RNA particle-plus-adjuvant combo, blur historical product labels and elevate platform depth as the new competitive yardstick.

Second-order effects include rising feed-additive ventures exploring synthetic biology proteins. Agency approvals for plant-expressed porcine enzymes spark curiosity from feed majors that seek cost-competitive nutrition gains. Expect biologics to retain top-line heft, yet genetic solutions will account for an outsized slice of incremental animal biotechnology market revenue.

By Application: Preventive Care Dominance Faces Diagnostic Disruption

Preventive programs anchored 73.85% of the animal biotechnology market revenue share in 2025, a testament to vaccine efficacy and producer economics that prefer prevention to cure. Disease diagnosis, however, records a brisk 7.62% CAGR and chips into traditional revenue mixes. Point-of-care devices close testing loops, making early detection financially rational for mid-size farms. R&D applications benefit when gene-editing advances shorten product timelines. The animal biotechnology market size attributable to research clients could climb further as public-private consortia back translational studies.

Uptake of cloud-linked diagnostic platforms creates network effects. Data improves model accuracy, which then refines vaccine strain matching, underscoring a virtuous circle between detection and prevention that strengthens overall animal biotechnology market resilience.

By Animal Type: Livestock Scale Versus Companion Premiumization

Livestock represented 62.41% of the animal biotechnology market size in 2025. Gains stem from herd-level genetic programs aimed at disease resistance and feed efficiency. Companion animals push a quicker growth path at 7.74% CAGR, thanks to owner willingness to finance advanced treatments. Products like Loyal’s lifespan-extending tablet for senior dogs signal a premium trajectory potentially transferable to equine or exotic species niches.

Producers of gene-edited pigs, disease-resistant poultry, and high-yield cattle continue to dominate volume. Yet margin dynamics increasingly favor companion therapeutics where single-patient pricing is higher, enabling a balance that stabilizes the wider animal biotechnology market.

By End-User: Laboratory Infrastructure Versus Point-of-Care Democratization

Laboratories accounted for 35.74% of the animal biotechnology market revenue share in 2025, reflecting their historic centrality in testing and R&D. Point-of-care sites clock the highest CAGR at 7.55% as vets adopt compact analyzers. Chain clinics roll out unified platforms that enhance data pooling. This switch supports a more distributed model that lowers sample transport expenses while broadening the reach of biotech innovations. Integration with supply-chain portals lets farmers order vaccines triggered by field test results, further embedding biotechnology into daily practice and reinforcing adoption across the animal biotechnology market.

Geography Analysis

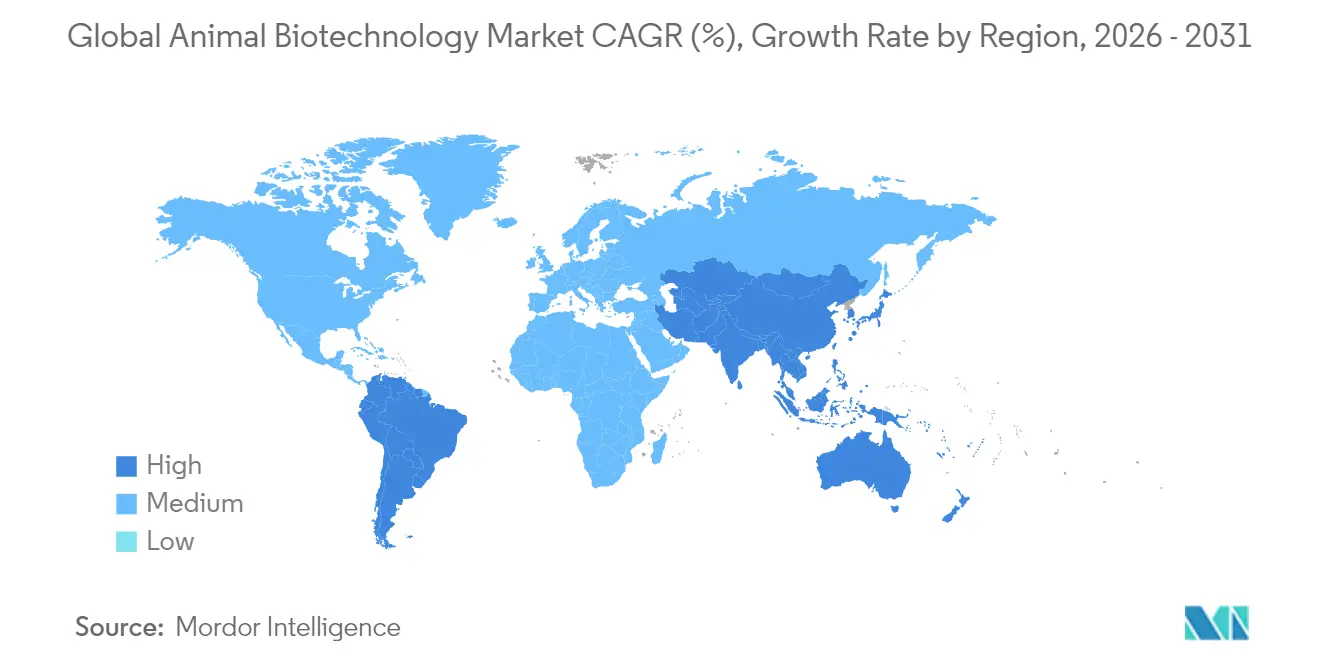

North America retained 37.10% share of the animal biotechnology market in 2025 and is growing at 6.82% CAGR. A science-focused regulator, deep venture funding, and consolidated vet networks create smooth tech diffusion. FDA nods for gene-edited pigs and early xenotransplant trials set policy precedents. U.S. veterinary service outlays reached USD 66 billion and are on pace for USD 70 billion by 2029, widening the spending base for biotech upgrades.

Asia-Pacific logs the fastest 7.92% CAGR and enlarges its slice of the animal biotechnology market on the back of soaring protein demand, burgeoning pet ownership, and aggressive vaccine rollouts. China’s animal-vaccine sales rose 26% annually as producers chase herd-health coverage. Regulatory maturity is uneven, but manufacturing capacity and cost advantages foster an emerging production hub, provided patent safeguards keep pace.

Europe appears steady with a 7.05% CAGR, yet wrestles with public skepticism toward genetic edits. Strong biologics pipelines and research clusters from Denmark to Germany keep the region relevant. However, precautionary rules could push breakthrough launches to North America first, delaying European benefit capture from the animal biotechnology market.

South America and Middle East & Africa remain niche but show consistent adoption where export-oriented livestock sectors modernize. Brazil’s experiments with insulin-producing cows highlight regional innovation potential, while Gulf states fund camel health programs amid rising dairy diversification. These pockets add incremental depth to the global animal biotechnology market without yet altering leadership ranks.

Competitive Landscape

Competition sits at a moderate level yet is quickening as data and platform models supplant standalone products. Top players hold overlapping pipelines in vaccines, diagnostics, and genetics. Zoetis lifted 2024 sales by 11.02%, inching its slice of the animal biotechnology market to 9.48%. Merck, Elanco, and Boehringer Ingelheim strengthen through platform and partner plays.

Consolidation continues in vet service chains, giving suppliers captive outlets to trial biotech tools. Partnerships proliferate: Elanco joined with Medgene for rapid H5N1 dairy cattle vaccines; United Therapeutics coordinates with transplant centers for gene-edited organ studies. Start-ups such as Loyal and Ginkgo Bioworks target longevity and synthetic biology niches, challenging incumbents by carving specialized use cases that could scale.

Data ownership becomes a strategic lever. Firms connecting diagnostic feeds with breeding decisions amass proprietary datasets that refine AI models, raising switching costs. Investment in cloud security and privacy protocols now influences tender outcomes as clients demand compliant data pipelines across the animal biotechnology market.

Global Animal Biotechnology Industry Leaders

Boehringer Ingelheim

Elanco Animal Health Incorporated

Merck & Co., Inc.

Virbac S.A.

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dechra gains FDA clearance for Otiserene, a single-dose otitis externa therapy showing 71.3% effectiveness versus 26.3% for placebo.

- February 2025: United Therapeutics secures FDA approval for clinical trials that transplant kidneys from gene-modified pigs into six patients, with expansion to 50 participants planned.

- February 2025: Elanco partners with Medgene to commercialize an H5N1 vaccine for dairy cattle targeting 973 affected herds across 17 states.

- February 2025: Loyal’s LOY-002 earns FDA RXE acceptance, enrolling 1,000 senior dogs in the largest veterinary longevity study to date.

Global Animal Biotechnology Market Report Scope

As per the scope of the report, animal biotechnology refers to the branch of biotechnology, which deals with the molecular biology techniques for producing genetically engineered animals (whose genomes are modified), to make them suitable for pharmaceutical, industrial, or agricultural applications. The animal biotechnology market is segmented by Product Type (Diagnostic Tests, Reproductive & Genetic Products, Vaccines, and Drugs), Application (Development of Animal Pharmaceuticals, Food Safety, and Drug Development, Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Biologics |

| Diagnostics |

| Drugs |

| Nutrition |

| Reproductive & Genetic |

| Disease Diagnosis |

| Preventive Care & Treatment |

| Research & Development |

| Livestock Animals | Cattle |

| Swine | |

| Poultry | |

| Other Livestock Animals | |

| Companion Animals | Dogs |

| Cats | |

| Equine | |

| Other Companion Animals |

| Laboratories |

| Point-of-care testing |

| Veterinary Hospitals & Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Biologics | |

| Diagnostics | ||

| Drugs | ||

| Nutrition | ||

| Reproductive & Genetic | ||

| By Application | Disease Diagnosis | |

| Preventive Care & Treatment | ||

| Research & Development | ||

| By Animal Type | Livestock Animals | Cattle |

| Swine | ||

| Poultry | ||

| Other Livestock Animals | ||

| Companion Animals | Dogs | |

| Cats | ||

| Equine | ||

| Other Companion Animals | ||

| By End-User | Laboratories | |

| Point-of-care testing | ||

| Veterinary Hospitals & Clinics | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which breakthrough technology is currently reshaping commercial livestock breeding in animal biotechnology?

CRISPR-based gene editing is driving a shift from traditional selection to precision engineering by creating disease-resistant animals and enabling traits that improve productivity and welfare.

How are artificial-intelligence platforms influencing genetic improvement programs?

AI tools analyze massive genomic datasets to predict optimal mating pairs and embryo selections, shortening breeding cycles and unlocking trait gains that were previously unattainable through conventional methods.

What role do point-of-care molecular diagnostics play in veterinary practice today?

Portable PCR and other rapid tests let veterinarians detect pathogens in minutes at the clinic or farm, making treatment decisions faster and supporting real-time surveillance networks that help contain outbreaks.

Why are established animal-health companies investing heavily in platform technologies rather than single products?

Platform approaches—such as modular RNA vaccine systems—allow firms to pivot quickly to new diseases, reduce time-to-market, and create recurring revenue streams across multiple therapeutic areas.

What is the biggest non-technical obstacle facing gene-edited food animals?

Public acceptance remains the primary hurdle; consumer skepticism and retailer policies can restrict market access even in regions with favorable regulatory approvals.

How is Asia-Pacific emerging as a strategic production hub for animal biotechnology?

The region offers large livestock populations, expanding pet ownership, and competitive manufacturing costs, encouraging firms to establish R&D and production facilities closer to high-growth end-markets.

Page last updated on: