Angola Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

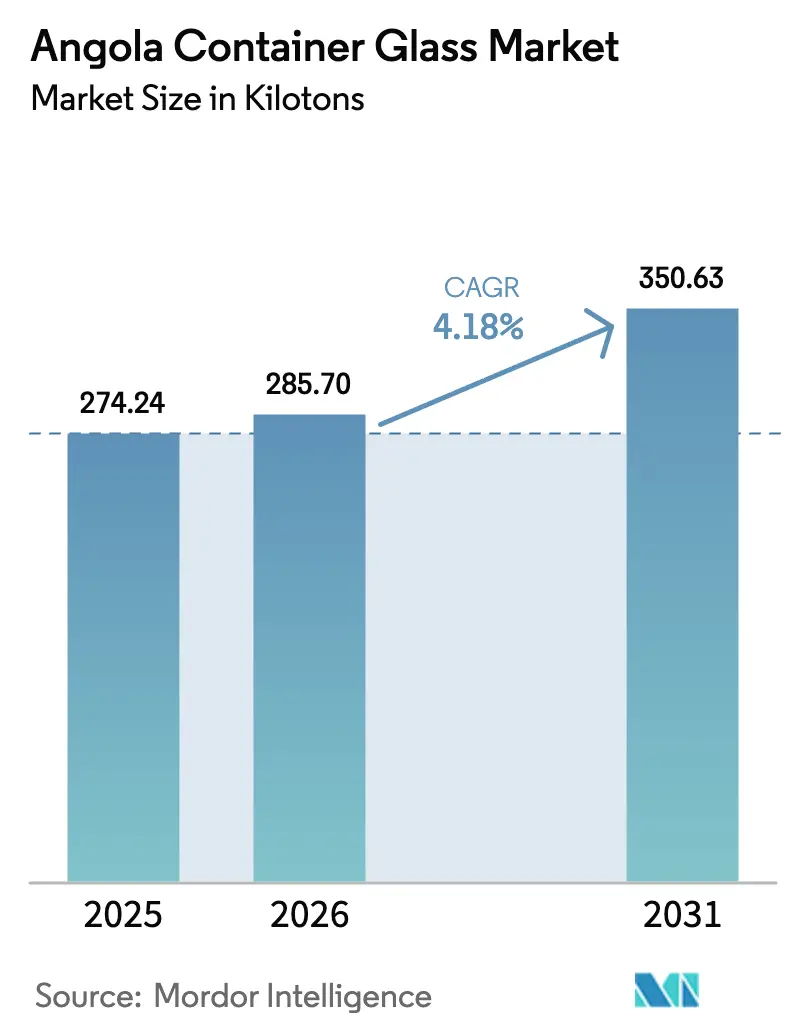

| Base Year Market Size (2025) | 274.24 kilotons |

| Market Volume (2026) | 285.7 kilotons |

| Market Volume (2031) | 350.63 kilotons |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

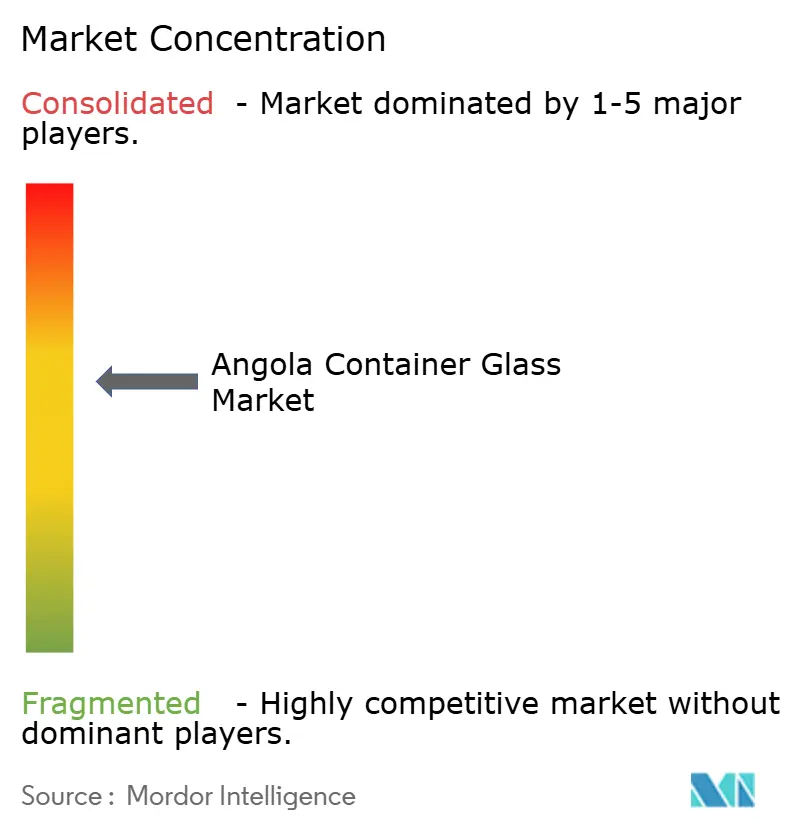

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angola Container Glass Market Analysis by Mordor Intelligence

Angola container glass market size in 2026 is estimated at 285.7 kilotons, growing from 2025 value of 274.24 kilotons with 2031 projections showing 350.63 kilotons, growing at 4.18% CAGR over 2026-2031. This growth pace mirrors the government’s economic diversification policies, import substitution incentives, and sustained consumption gains in Luanda’s urban core. Rising discretionary spending on premium beer, wine, and spirits boosts unit demand for flint and amber bottles, while expanded cold-chain retail networks strengthen glass uptake in chilled juices and condiments. At the supply level, the Lobito Corridor rail-and-port upgrade promises lower inbound freight costs for soda ash and furnace parts, partly offsetting the volatility in energy prices. Meanwhile, ongoing work on high-purity silica deposits could pave the way for domestic raw material sourcing that shields producers from foreign currency constraints and offers a buffer against global commodity shocks.

Key Report Takeaways

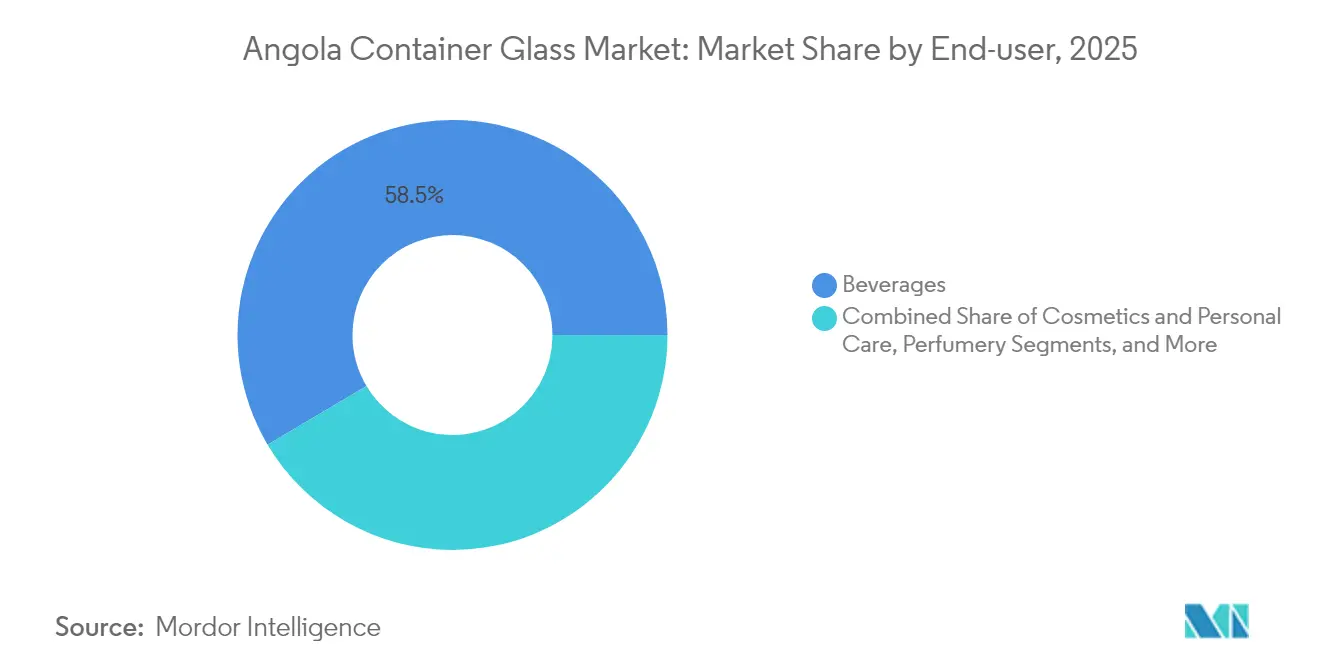

- By end-user, the Angola container glass market size for the cosmetics and personal care segment is projected to grow at a 5.62% CAGR between 2026-2031.

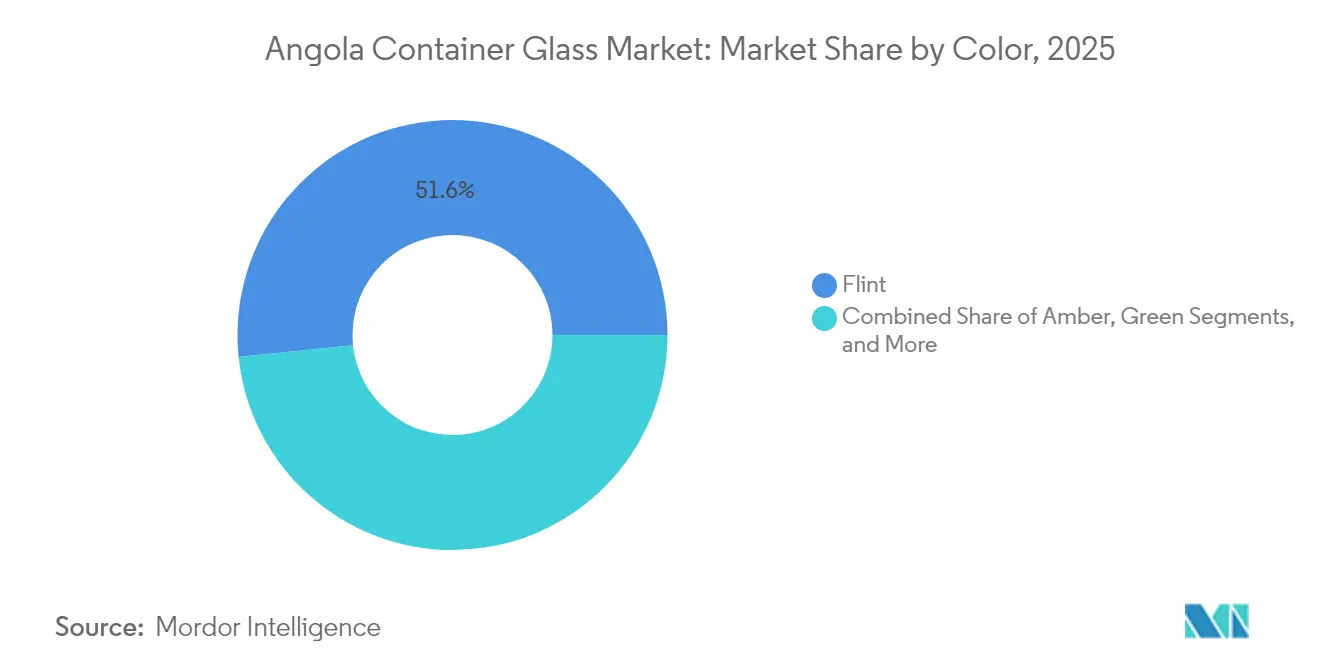

- By color, Flint captured 51.63% of the Angola container glass market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Angola Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium beverages fueling glass packaging uptake | +1.2% | National - strongest in Luanda | Medium term (2-4 years) |

| Government push for sustainable and recyclable packaging solutions | +0.8% | National - early adoption in Luanda | Long term (≥ 4 years) |

| Expanding middle-class and urbanization elevating packaged food consumption | +1.0% | National - pronounced in Luanda, Benguela, Huambo | Medium term (2-4 years) |

| Lobito Corridor logistics upgrades slashing soda-ash and bottle import costs | +0.7% | National - western provinces benefit first | Medium term (2-4 years) |

| Tax incentives and duty exemptions on packaging equipment encouraging local investment | +0.5% | National - industrial zones | Long term (≥ 4 years) |

| Discovery of high-purity silica deposits enabling domestic glass raw-material sourcing | +0.4% | Interior provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium Beverages Fueling Glass Packaging Uptake

Rapid premiumization in Angola’s beer and spirits categories is resulting in a noticeable shift toward glass formats that convey quality and preserve flavor integrity. Urban consumers in Luanda tend to gravitate toward 330 ml and 750 ml flint bottles that showcase product clarity, while local breweries, such as Sodiba, earmark substantial capital for glass procurement to keep pace with the double-digit growth of craft beer.[1]Expresso, “Luanda Leaks. Fábrica da cerveja Sagres em Angola arrisca falência após arresto de bens de Isabel dos Santos,” expresso.pt Cross-promotional tie-ins between hospitality venues and upscale beverage brands further elevate throughput volumes for the Angola container glass market, especially during festive seasons when import flows spike. The resulting pull-through stimulates bottle-maker capacity utilization, nudging furnace run rates closer to breakeven thresholds and justifying investments in oxygen-fuel burners that cut energy intensity.

Government Push for Sustainable and Recyclable Packaging Solutions

Executive Decree No. 64/23 mandates tamper-evident seals on alcoholic beverages and imposes six-month minimum shelf-life standards, implicitly favoring glass due to its inert chemistry and excellent barrier properties.[2]Trade.gov, “Angola - Labeling/Marking Requirements,” trade.gov Complementary stimulus arrives via accelerated depreciation on continuous-process equipment, materially improving internal rates of return for furnace rebuilds. Collectively, these directives signal a policy shift toward closed-loop packaging ecosystems that align with the broader circular economy agenda, nudging retailers and fillers to specify more returnable bottles. Over the long haul, alignment between sustainability credentials and regulatory compliance cements Glass’s value proposition versus PET in premium segments of the Angola container glass market.

Expanding Middle-Class and Urbanization Elevating Packaged Food Consumption

Angola’s rising urban household incomes are bolstering demand for shelf-stable jams, sauces, and edible oils, which are presented in clear flint jars that highlight freshness cues. Formal retailers, such as Shoprite and Kero, which are now expanding beyond Luanda into Benguela and Huambo, view locally sourced glass as a hedge against exchange-rate swings while satisfying provenance labeling requirements. Moreover, consumer-facing marketing emphasizes health and safety attributes associated with non-leaching glass containers, thereby building brand loyalty among younger families. These dynamics reinforce a steady uptick in order volumes and strengthen importer confidence in multi-year supply contracts with domestic converters.

Lobito Corridor Logistics Upgrades Slashing Soda-Ash and Bottle Import Costs

The 1,300 km Lobito rail concession, backed by USD 553 million in U.S. development financing and USD 200 million from South Africa’s development bank, seeks to clip transit times and port dwell costs for inbound raw materials. Early engineering estimates point to freight savings of 15-20 USD per ton on imported soda ash once double-stack service commences, shaving variable costs by up to 4% for producers located near Benguela. On the outbound side, smoother west-east connectivity unlocks export lanes into Democratic Republic of Congo mining districts, where bottled beverages and condiment lines represent new offtake channels. Over the medium term, these logistical efficiencies help dampen landed-cost inflation, giving Angola's container glass market participants a sharper competitive edge against regional imports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from PET and other lightweight packaging | -0.9% | National - cost-sensitive tiers | Short term (≤ 2 years) |

| Chronic energy supply disruptions elevating furnace operating costs | -1.1% | National - industrial corridors | Short term (≤ 2 years) |

| Foreign-currency shortages hindering import of critical raw materials and spare parts | -0.8% | National | Medium term (2-4 years) |

| Low cullet collection rates outside Luanda inflating production cost base | -0.6% | Interior provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Energy Supply Disruptions Elevating Furnace Operating Costs

Only 30% of the population has access to the grid, prompting glassmakers to maintain diesel backup sets that increase energy bills by up to 40% during blackout episodes. Thermal cycling caused by grid trips shortens furnace lifespan, accelerating rebuild schedules and depreciation charges. Planned tariff liberalization could triple electricity costs over the next two years, eroding gross margins just as firms weigh oxy-fuel retrofits. Smaller players lacking captive power solutions may curtail production or pivot to import-sourced supply models, temporarily constricting domestic output in the Angola container glass market.

Foreign-Currency Shortages Hindering Import of Critical Raw Materials and Spare Parts

Central-bank hard-currency auctions have shrunk to under USD 800 million per month, compelling firms to queue for allocations and negotiate cash-in-advance terms with overseas suppliers.[3]Privacy Shield Framework, “Angola - Methods of Payment,” privacyshield.gov Extended lead times for soda ash, refractories, and platinum bushings inject inventory risk and can trigger costly unplanned downtime. Moreover, 50% customs deposits on temporary imports tie up working capital, disincentivizing pilot equipment trials that could lift energy efficiency. These constraints perpetuate higher cost structures and delay capacity upgrades across the Angola container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Beverages Sustain Volume Leadership, Cosmetics Propel Incremental Growth

The beverages segment captured 58.52% of the Angola container glass market share in 2025, driven by strong beer and carbonated soft drink throughput in Luanda’s hospitality sector. Amber bottles dominate lager lines because of UV-blocking attributes, while clear flint vessels reinforce premium cues in spirits and craft-soda niches. The segment’s entrenched cold-chain infrastructure reduces breakage risk, encouraging distributors to opt for glass despite the cost advantages of PET. Non-alcoholic beverages, such as functional juices, also favor glass for perceived health benefits, safeguarding demand continuity even in price-sensitive areas. Beverage-brand marketing around heritage and authenticity amplifies this pull, further entrenching the Angola container glass market in on-premise and take-home occasions.

Cosmetics and personal care, though still smaller in tonnage, are advancing at a 5.62% CAGR through 2031, outstripping all other categories in relative terms. Upscale fragrance houses insist on heavy-wall flint bottles for tactile luxury, and emerging local skincare labels emulate this packaging language to elevate brand equity. Urban middle-class consumers signal readiness to trade up for imported serums and foundations, putting upward pressure on average unit prices. Rising e-commerce penetration widens geographic reach, compelling fulfillment centers to adopt double-wall mailers that mitigate transit shocks and preserve glass adoption. Pharmaceutical demand, particularly for liquid nutraceuticals packaged in amber forms, adds a further buffer against cyclical swings, supporting predictable batch sizes for domestic converters.

By Color: Flint Conveys Purity, Amber Captures Growth in Sensitive Applications

Flint glass led the Angola container glass market in 2025, with a 51.63% share, leveraging its clarity to showcase product color and purity cues across beer, spirits, and gourmet food lines. Marketing campaigns for premium spring water in Luanda position crystal-clear bottles as lifestyle statements, reinforcing demand resilience even amid rising PET penetration. Production economics also favor flint, given its simpler coloring agents and easier cullet blending, which lower per-ton cost by up to 7% relative to specialty tints.

Amber volumes, however, are expanding at a brisk 5.03% CAGR through 2031, primarily driven by the adoption of pharmaceuticals and craft beer. The color meets stringent photoprotection standards required for active ingredients, and new over-the-counter supplement brands view amber vials as a regulatory shorthand for stability. Breweries aiming to move upmarket capitalize on amber’s heritage associations, pairing it with embossed logos and crown-finish closures that enhance shelf presence. Improved furnace-color changeover technology now enables shorter campaign runs, allowing converters to respond faster to seasonal swings in amber demand without compromising throughput in flint lines.

Geography Analysis

Luanda Province underpinned nearly four-fifths of Angola container glass market volumes in 2025, anchored by its eight-million-strong urban consumer base and high density of beverage fillers. The capital’s monopoly over import gateways, storing roughly 78% of maritime cargo, delivers scale economies that compress landed costs for cullet and finished bottles. Distributor networks radiate from Viana Industrial Zone, enabling same-day truck deliveries that minimize stock-holding expenses for downtown retailers and hospitality venues.

Benguela and Lobito constitute the fastest-growing cluster thanks to the Lobito Corridor rail rejuvenation, which promises to cut transit time to the Copperbelt and stimulate value-added agro-processing hubs. Early-mover retailers have mapped warehouse footprints in Lobito to capture spillover demand from construction worker camps and mining operations. The Angola container glass market size in this corridor is projected to outstrip the national growth average by 170 basis points once the double-stack service normalizes, timetable reliability improves, and reefer-box capacity expands.

Interior provinces remain logistically challenging due to rugged road conditions and limited cold-chain assets, which inflate handling costs and increase breakage risk, prompting traders to lean toward lightweight substitutes. Informal markets account for 70% of rural food sales, where sachet formats outperform heavier jars. Still, targeted government subsidies for rural retail modernization and the possibility of satellite cullet buyback depots could, in time, chip away at supply-chain penalties and broaden the geographic footprint of the Angola container glass market.

Competitive Landscape

Domestic manufacturing is headlined by EMBALVIDRO, whose 600-ton-per-day furnace aligns with the strategic needs of majority shareholder Sodiba Brewery. The vertically integrated setup secures bottle supply for Sagres and Luandina labels, capturing the downstream margin that would otherwise be ceded to import agents. International suppliers, including Portuguese contract molders, serve premium segments that demand intricate embossing or short color runs, but face foreign exchange allocation bottlenecks that stretch lead times to 120 days. Joint-venture proposals with raw-material concession holders are under discussion to underwrite furnace rebuilds with local silica feedstock, signaling a gradual unlocking of capex once policy clarity on mining royalties arrives.

Competition intensity remains moderated by high entry barriers: a full greenfield furnace typically exceeds USD 90 million, and payback horizons lengthen when factoring in diesel backup investment. Consequently, second-hand furnace transactions and modular cold-end upgrades dominate the capital budget committees. Strategic moves center on energy-efficiency retrofits, such as regenerator checker-brick redesigns that trim specific fuel consumption by up to 8%, alongside pulsed-air cooling systems that increase throughput between repair shutdowns. Certification to ISO 22000 and HACCP standards further differentiates incumbents, winning trust from multinationals establishing co-packing lines in Luanda.

Consolidation prospects hinge on macrovolatility: local credit spreads remain in the high teens, restricting leverage for M&A. Nonetheless, several private equity funds have initiated preliminary discussions with family-owned cullet collectors to develop integrated collection-to-melt platforms. Should these deals close, the Angola container glass industry could see improved cullet ratios above the current 15%, thereby lowering the energy load per ton melted and enhancing its greenhouse-gas credentials, an increasingly salient purchasing criterion for export-oriented beverage groups.

Angola Container Glass Industry Leaders

EMBALVIDRO-INDÚSTRIA (SU), LDA

Vidrul - Angolan Glass Factory

Krones Angola Lda.

Beta Glass Plc

Didactic Africa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Africa Policy Research Institute confirmed USD 4-6 billion in committed funding for the Lobito Corridor, including new spurs toward Zambia that will streamline raw-material inflows.

- January 2025: Angola introduced a 25% headline corporate tax alongside accelerated depreciation for multi-shift plants, cutting payback periods for continuous furnaces.

- December 2024: IANORQ finalized 150 food-safety and packaging standards, reinforcing technical barriers that favor compliant glass producers.

- September 2025: Development Bank of Southern Africa cleared USD 200 million for Lobito rail rehabilitation, complementing USD 553 million from the U.S. International Development Finance Corporation.

Angola Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Angola container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How fast is the Angola container glass market expected to grow toward 2031?

The market is projected to advance at a 4.18% CAGR, moving from 285.7 kilotons in 2026 to 350.63 kilotons by 2031.

Which end-user category dominates current demand?

Beverages account for 58.52% of 2025 volume because breweries and soft-drink firms favor glass for product integrity and premium positioning.

Where is demand growth the strongest geographically?

The Benguela-Lobito corridor is poised for the fastest expansion once rail upgrades cut inbound raw-material and outbound freight costs.

What is the biggest operational challenge for local producers?

Intermittent electricity supply raises furnace operating costs and forces reliance on expensive diesel generators.

How do government incentives affect new capacity investments?

Accelerated depreciation on continuous-process equipment and duty exemptions on select machinery materially shorten payback periods for furnace rebuilds.

Which glass color segment is gaining momentum?

Amber is expanding at a 5.03% CAGR through 2031, driven by pharmaceutical and premium beer applications that require ultraviolet protection.

Page last updated on: