Congo Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

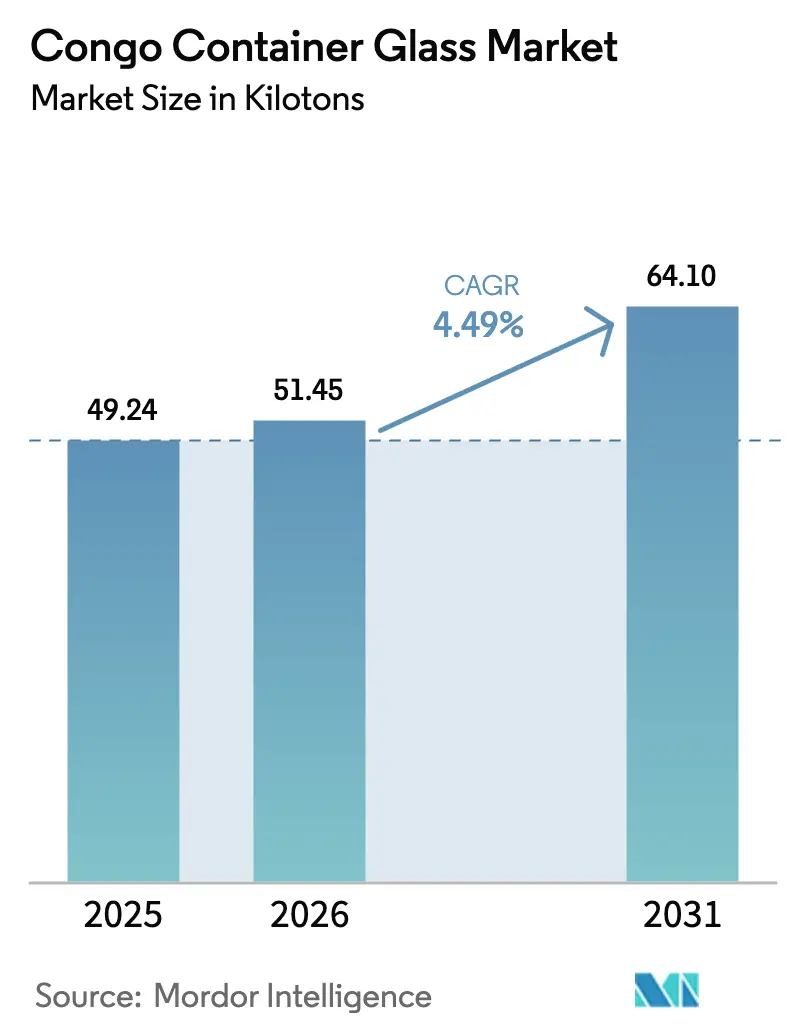

| Base Year Market Size (2025) | 49.24 kilotons |

| Market Volume (2026) | 51.45 kilotons |

| Market Volume (2031) | 64.1 kilotons |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Congo Container Glass Market Analysis by Mordor Intelligence

The Congo container glass market size in 2026 is estimated at 51.45 kilotons, growing from 2025 value of 49.24 kilotons with 2031 projections showing 64.1 kilotons, growing at 4.49% CAGR over 2026-2031. Urban consumers in Kinshasa and Lubumbashi are trading up to glass-packaged beer, spirits, and soft drinks as household incomes rise and premium brands seek to enhance their shelf appeal. Brand owners value glass for its tamper-evident features and product integrity, which help fight counterfeit alcohol and align with incoming single-use plastic curbs. Import dependence persists because domestic furnace capacity is limited, and poor road links from Matadi port inflate freight costs. However, investors such as Boukin SARL are expanding local melt capacity to shorten lead times and hedge against foreign-exchange swings. Growing interest in electric-furnace technology and the use of recycled cullet targets lower carbon footprints, providing suppliers with fresh opportunities to differentiate themselves on sustainability while serving the expanding beverage core of the Congo container glass market.

Key Report Takeaways

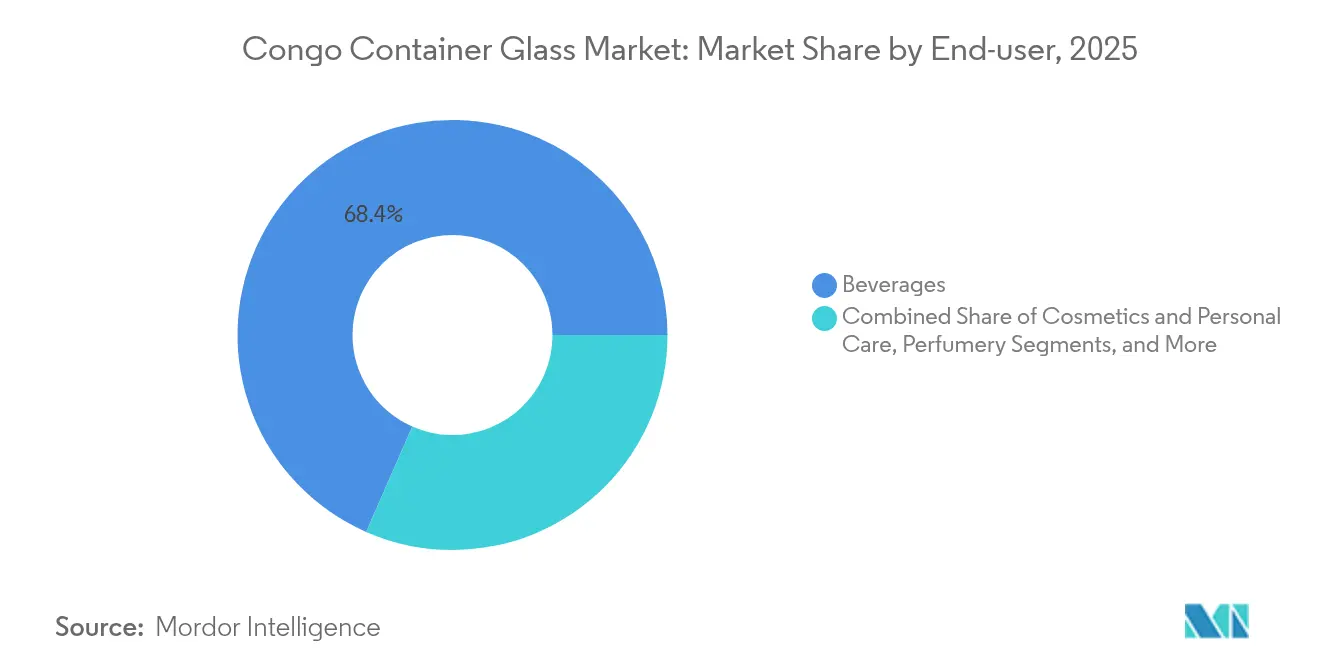

- By end-user, beverages captured 68.42% of the Congo container glass market share in 2025.

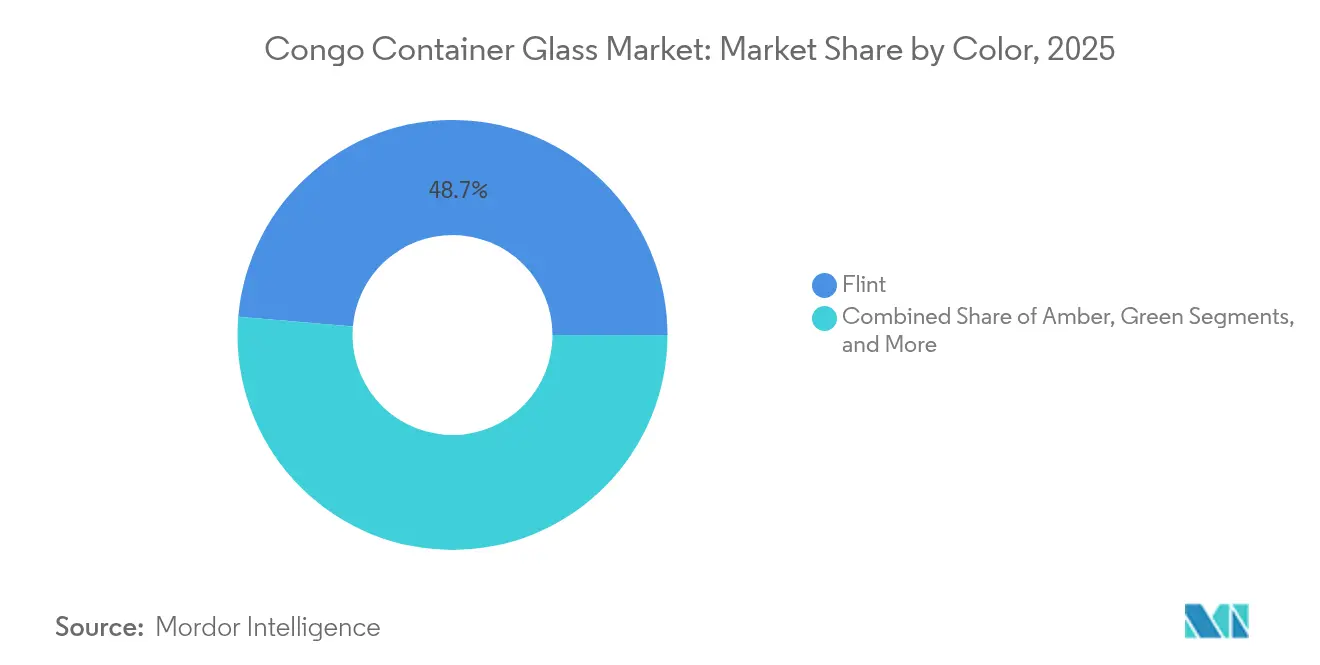

- By color, the Congo container glass market for amber glass is projected to grow at a 5.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Congo Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of beer and spirits packaging | +1.2% | Kinshasa, Lubumbashi urban centers | Medium term (2-4 years) |

| Rising urban middle class driving glass-pack adoption | +0.9% | Major Congolese cities, spillover to secondary urban areas | Long term (≥4 years) |

| Government ban on single-use plastics | +0.7% | National, with early implementation in Kinshasa | Short term (≤2 years) |

| Capacity expansion of Boukin SARL furnace line | +0.5% | Kinshasa production hub, regional distribution | Medium term (2-4 years) |

| Cold-chain growth enabling juice and dairy glass demand | +0.4% | Urban centers with infrastructure development | Long term (≥4 years) |

| Niche craft-perfume start-ups seeking high-end glass | +0.2% | Kinshasa luxury market, export-oriented production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumisation of Beer and Spirits Packaging

Glass increasingly underpins premium alcohol strategies in Congo’s main cities. Breweries and distillers position long-neck bottles and thick-base flasks as proof of authenticity, a critical cue in markets where illicit refilling threatens margins. Retailers report that shoppers equate heavy glass with craftsmanship, a perception that encourages trade-ups from sachet liquor or PET formats. Imported spirits brands often mirror global pack formats, prompting local fillers to emulate the same look to remain competitive. As disposable income increases, consumers are willing to accept moderate price premiums when the bottle conveys status and ensures tamper safety. Regulators also favor glass because embossing and engraving facilitate tax-stamp compliance, thereby reinforcing demand during the forecast period.

Rising Urban Middle Class Driving Glass-Pack Adoption

Kinshasa alone now hosts more than 12 million residents, and census data show a growing cohort earning formal salaries that support lifestyle upgrades. This cohort prizes hygienic, visually appealing packaging for condiments, honey, and table sauces, categories that historically used recycled plastic. Branded food processors seize the chance to launch square glass jars that stack efficiently on limited shelf space, improving retail economics. Greater internet penetration exposes shoppers to global packaging aesthetics, and social media amplifies the association between clear glass and product purity. Volume aggregation in dense urban districts offsets glass’s freight penalties, letting distributors absorb city-to-store costs more easily than rural hauls.

Government Ban on Single-Use Plastics

Draft decrees circulated in 2024 target thin-wall carrier bags before expanding to include beverage containers, mirroring policies already in effect in East Africa. Even a phased rollout pushes bottlers to prequalify glass suppliers so they can pivot when enforcement becomes tighter. International franchise soft-drink operators are reassessing returnable-glass bottling lines to safeguard franchise rights and satisfy global ESG scorecards. Municipal waste audits highlight plastic litter along the Congo River, adding public pressure. Because alternative bio-plastics remain costly, glass stands out as the commercially proven substitute that meets shelf-life and carbonation thresholds without requiring retooling of fillers.

Capacity Expansion of Boukin SARL Furnace Line

Boukin SARL’s upgrade increases local melt output by approximately 30,000 tons per year, a step that reduces Matadi-to-Kinshasa import trucking and cuts lead times by four weeks for core beer bottles. Beverage groups negotiating multi-year contracts welcome the predictable pricing that local soda ash supply and cullet streams bring. The project creates technical apprenticeships, aligning with government plans to boost industrial skill bases. Proximity also unlocks quick design tweaks: brand managers can roll out commemorative embossing within a single production shift rather than waiting for overseas molds. Lower inventory buffers free up cash for marketing, reinforcing glass uptake among fast-moving categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cheaper PET and HDPE alternatives | -1.1% | National, stronger in price-sensitive rural markets | Short term (≤2 years) |

| Fragility and high logistics cost of glass | -0.8% | Transport corridors, remote distribution areas | Long term (≥4 years) |

| Foreign-exchange volatility inflating soda-ash imports | -0.6% | National production, import-dependent supply chains | Medium term (2-4 years) |

| Informal recycling sector limiting cullet quality | -0.4% | Urban waste-collection areas, manufacturing centers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cheaper PET and HDPE Alternatives

Price gaps widen whenever crude oil benchmarks dip, making virgin PET bottles notably cheaper on a per-unit basis than flint glass. Small water bottlers often lack the capital for sturdy crates and opt for thin-wall PET that can withstand rough rural transport without breaking. Import tariffs on finished plastic bottles are lower than duties on bulk cullet, skewing economics. Retailers also favor PET for ease of stacking in cramped stalls. Unless glass suppliers can establish returnable loops or leverage carbon footprint marketing, cost-conscious consumers will continue to default to plastic in the near term.

Fragility and High Logistics Cost of Glass

Weight penalties translate into higher diesel expenditures, especially on the Matadi–Kinshasa corridor, where potholes extend transit times to three days during the rainy season.[1]UN Conference on Trade and Development, “Étude Diagnostique sur l’Intégration du Commerce – RDC,” unctad.org Breakage rates of 2-3% erode already thin distributor margins. Specialized pallets and dividers raise packaging costs before the bottle even reaches a filler. Rural wholesalers often lack forklifts, forcing them to handle goods manually, which heightens break risks and deters them from stocking glass-packed SKUs. Even in cities, congestion ups driver overtime, multiplying total logistics bills relative to PET.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Market Foundation

The beverages segment commanded 68.42% of the Congo container glass market share in 2025, underscoring its role as the volume anchor for the Congo container glass market. Breweries, spirits distillers, and carbonated-soft-drink fillers rely on flint and amber bottles to convey authenticity, withstand pasteurization, and preserve flavor. Local beer brands, such as Bralima and Bracongo, refresh their label graphics every season, yet retain the same returnable bottle, reinforcing consumer familiarity while extending the asset's life. Imported spirits labels mirror global pack formats, creating steady demand for premium flasks even during fluctuations in exchange rates. Seasonal consumption spikes around Independence Day force distributors to secure buffer inventory months in advance, locking in a predictable baseline for furnace utilization across the forecast horizon.

Cosmetics and personal care, although still small, are projected to post a 5.51% CAGR to 2031, the fastest within the Congo container glass market. Urban beauty brands bundle serums and creams in frosted vials to differentiate from mass-market plastics and to justify premium pricing. Glass’s impermeability protects volatile essential oils from oxidation, a feature that marketers often showcase in social media tutorials. Pharmacy chains stock imported hair-oil droppers that educate shoppers about precise dosing, indirectly elevating expectations for local products to adopt similar formats. Rising middle-class spending on grooming, therefore, unlocks incremental tonnage growth even though beverages will continue to dominate absolute kilograms sold.

By Color: Flint Glass Leads Transparency Demand

Flint glass accounted for 48.65% of the Congo's container glass market size in 2025, reflecting consumer preference for product visibility and regulators’ insistence on transparent packaging for certain pharmaceuticals. Clear beer and ready-to-drink cocktail launches add fresh volume, as brand owners seek shelf appeal that highlights the liquid hues. High-purity silica requirements make flint costlier than colored alternatives; yet, fillers accept the premium when transparency drives impulse purchases. Pharmacies stock vitamin concoctions in small flint bottles to reassure buyers of dosage accuracy, reinforcing the material’s trust halo. Supermarket chains also favor clear condiment jars, allowing shoppers to inspect the texture before purchase, a key driver of repeat sales in congested aisles.

Amber glass is projected to expand at a 5.12% CAGR through 2031 as brewers scale up lager production and perfumers seek UV shielding. Craft-beer start-ups opt for stubby amber bottles to evoke heritage and minimize light-struck off-flavors, ensuring consistent taste even after long hauls from Kinshasa to remote mining camps. Spirits fillers emboss crests onto amber flasks to elevate perceived value without changing liquid formulations. Because amber allows for higher cullet percentages, furnace operators can lower their energy use, a benefit they highlight when negotiating supply contracts with ESG-oriented multinationals. Meanwhile, niche aromatherapy oils adopt miniature amber droppers, adding high-margin but low-weight orders that enhance batch economics for bottle makers.

Geography Analysis

Kinshasa accounts for well over half of the Congo's container glass market annual throughput, supported by a dense retail network and proximity to the country’s only operational bottle-making furnace. Supermarkets in Gombe and Limete districts allocate entire aisles to returnable beer crates, shortening shopper dwell time and encouraging bulk purchases. Lubumbashi follows as a distant second node, leveraging mining salaries to sustain premium spirits volumes despite the 2-day road journey from the capital. Distributors zone their fleets along the Route Nationale 1 corridor, timing convoys to avoid flood-related closures that can add 30% to delivery costs during peak rain.

Market penetration in secondary cities, such as Kisangani, Mbuji-Mayi, and Bukavu, remains low because freight surcharges inflate shelf prices; plastic dominates until per-capita income rises. Nonetheless, donor-funded cold-chain pilots in Bukavu are testing glass-packaged yogurt, hinting at future beachheads once refrigeration outages drop. Port limitations at Matadi hinder import flow, forcing some fillers to reroute via Pointe-Noire, Republic of Congo, which adds customs overhead but sometimes saves time when Matadi berths are congested. Currency fluctuations also influence geographic allocation, as distributors direct scarce glass inventory toward wealthier districts where shoppers are more willing to tolerate price swings.

The government plans to operationalize the Maluku special economic zone by 2028, which could alter this map. A new furnace inside the zone would transport soda ash by rail from neighboring Angola, reducing inland freight and rebalancing the supply toward the center of the country. If realized, the shift could lift the Congo container glass market size for interior provinces by making bottle prices more uniform. Cross-border traders in Kasumbalesa already shuttle empties back to Zambia, where full lines exist, creating an informal loop that reveals pent-up demand for glass once transport friction is alleviated.

Competitive Landscape

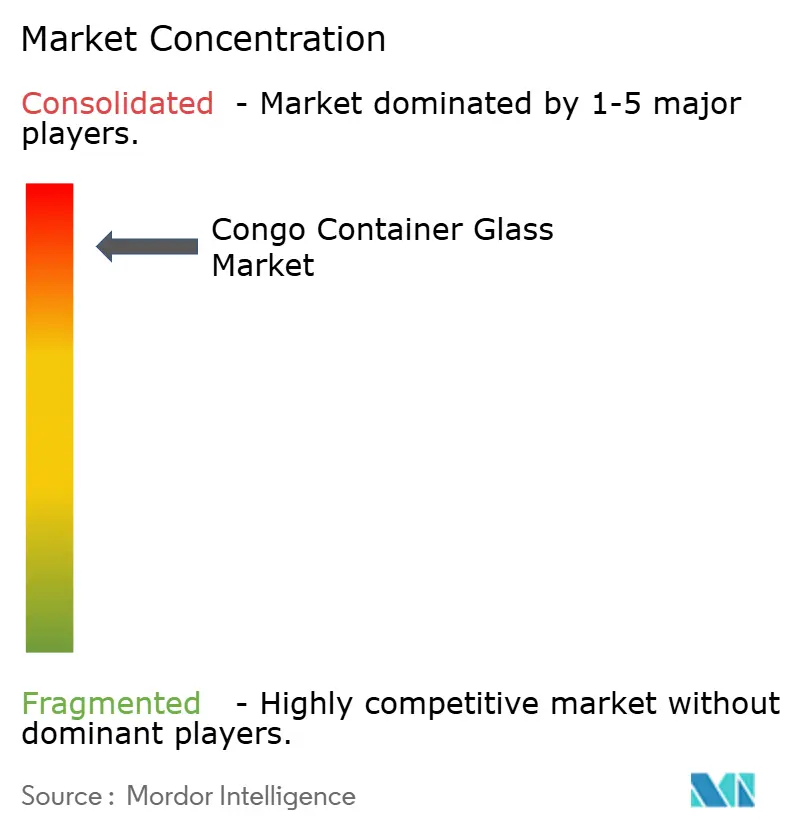

The supply remains fragmented, with no single player exceeding 20% of the Congolese container glass market share, giving buyers leverage in annual tender negotiations. Boukin SARL operates the only high-volume furnace in Kinshasa, yet it still imports molds and crown finishes from Europe, maintaining modest capital intensity but long lead times. Traders such as IBO Glass aggregate Chinese bottles for cosmetics fillers that need small runs, while Saverglass targets super-premium spirits with decorated flasks air-shipped in palletized cartons. Because few suppliers offer cradle-to-grave design services locally, brand owners often split contracts between a glassmaker and a separate decorator, diluting vendor stickiness.

Strategic moves in 2024 included Ardagh Group’s announcement of a Sub-Saharan furnace-maintenance program that could release surplus amber capacity into Congo via regional brokers. Verallia publicized its all-electric furnace trial in France and signaled interest in licensing the technology to African partners, a step that could help Congolese producers align with low-carbon procurement targets of multinational beverage clients.[3]Verallia, “2024 First-Half Financial Report,” verallia.com Meanwhile, O-I Glass appointed a new CEO with a mandate to expand into underserved African growth pockets, stoking speculation about joint-venture talks with local beverage bottlers.

Competitive differentiation increasingly rests on logistics reliability and forex agility. Importers who can consolidate bottles with crown caps and cartons inside the same container save customers a second customs clearance, shaving seven days off port dwell time. Local players counter by offering flexible credit terms pegged to the Congolese franc, absorbing some exchange-rate risk to secure multi-year supply deals. Sustainability also shapes bids: suppliers promising 30% recycled-glass content win favor with global breweries as they pursue Scope 3 reductions. In this evolving field, scale alone is not decisive; nimbleness in design tweaks, customs paperwork, and recycling partnerships often tips the balance when brands award annual contracts.

Congo Container Glass Industry Leaders

Beta Glass plc

Ardagh Group S.A.

Hongxing Glass Congo SARL

Nampak Glass (Pty) Limited

XuzhouAnt Glass Products Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Verallia reported implementation of the world’s first 100% electric furnace for the glass-packaging industry at its Cognac facility with 180 tons/day capacity, demonstrating a technology pathway that cuts CO₂ emissions by around 60% compared with conventional furnaces.

- August 2024: The African Development Bank invested USD 20 million in African Infrastructure Investment Fund 4, targeting renewable energy, digital infrastructure, and logistics projects across Africa, including potential improvements to the glass-manufacturing supply chain through port and transport infrastructure development.

- July 2024: Ardagh Group reported scheduled furnace rebuilds and machinery repairs for Africa operations in Q2 2024, signaling ongoing capacity maintenance and possible expansion in African glass-packaging production facilities.

- June 2024: Swissta continued operations as a leading water-bottling company in Kinshasa, utilizing multiple glass container sizes: 375 ml, 750 ml, 1,500 ml, 5,000 ml, and 18,900 ml, which illustrate the local demand for glass packaging in beverage applications.

Congo Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Congo container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Congo container glass market in 2026?

It totals 51.45 kilotons and is projected to grow at a 4.49% CAGR to 2031.

Which end-use segment consumes the most glass containers in Congo?

Beverages led with 68.42% share, anchored by beer, spirits, and soft-drink fillers.

What color variant is gaining share the fastest?

Amber bottles are advancing at a 5.12% CAGR because brewers and distillers need UV protection.

Why are logistics costs a critical issue for glass suppliers?

Heavy, fragile bottles travel inland from Matadi port over poor roads, raising freight and breakage expenses.

How is government policy influencing packaging choices?

Draft bans on single-use plastics are nudging beverage and food brands toward returnable or recyclable glass.

Are there sustainability advances in local glass production?

Boukin SARL’s planned furnace upgrade and Verallia’s electric-furnace model signal moves toward lower-carbon melting technology.

Page last updated on: