Analytical Standards Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analytical Standards Market Analysis by Mordor Intelligence

The analytical standards market size was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.61 billion in 2026 to reach USD 2.13 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031). This trajectory underscores how demand has expanded from core pharmaceutical usage into food, environmental and forensic testing. Multijurisdictional guidelines such as ICH Q2(R2) and Q14, adopted in 2024, have reshaped validation rules, prompting laboratories to upgrade reference-material portfolios. Certified reference material (CRM) producers benefit as users seek products that satisfy new requirements for specificity, selectivity and traceability. Meanwhile, contract research organizations (CROs) concentrate procurement power, heightening volume purchases and price sensitivity across the analytical standards market. Intensifying environmental rules—most notably the U.S. EPA’s PFAS Method 1633—create fresh demand for matrix-matched CRMs that mimic complex field samples. Counterbalancing those drivers are supply-chain volatility for specialty chemicals and a severe shortage of skilled analysts, both of which constrain expansion.

Key Report Takeaways

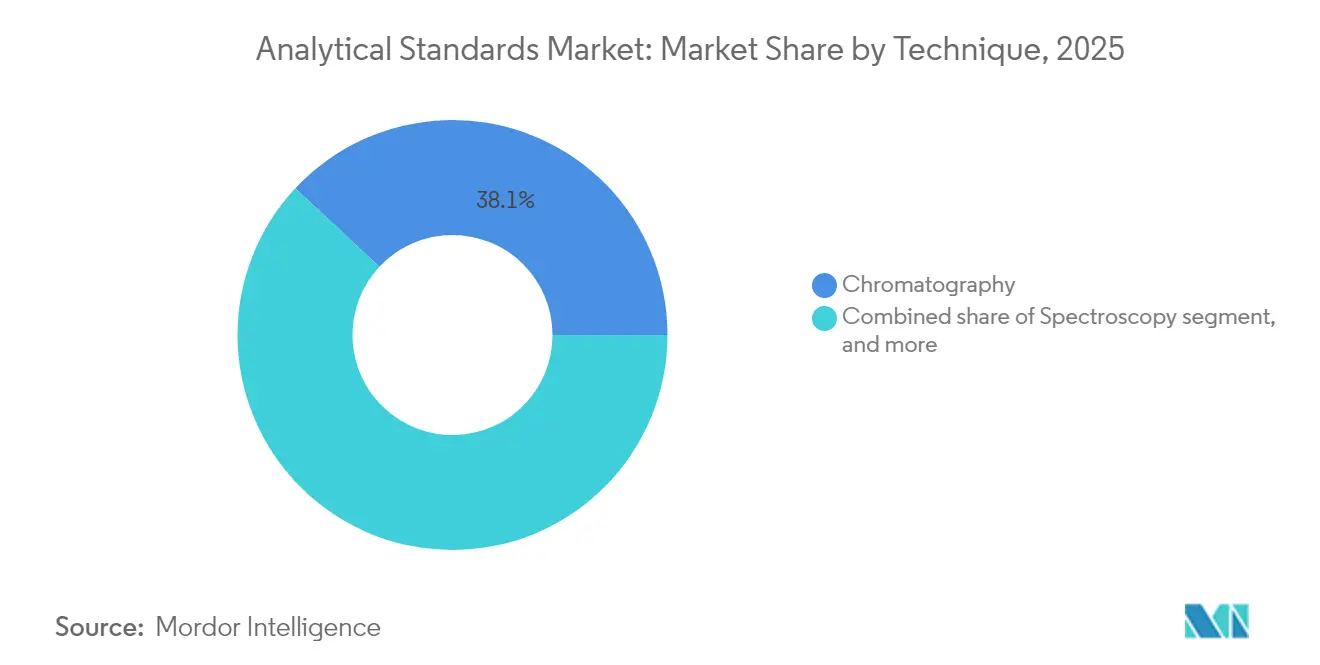

- By technique, chromatography held 38.05% of analytical standards market share in 2025; mass spectrometry is forecast to advance at a 7.38% CAGR through 2031.

- By product type, organic standards captured 60.72% of the analytical standards market size in 2025, while matrix-matched CRMs are set to post an 7.66% CAGR to 2031.

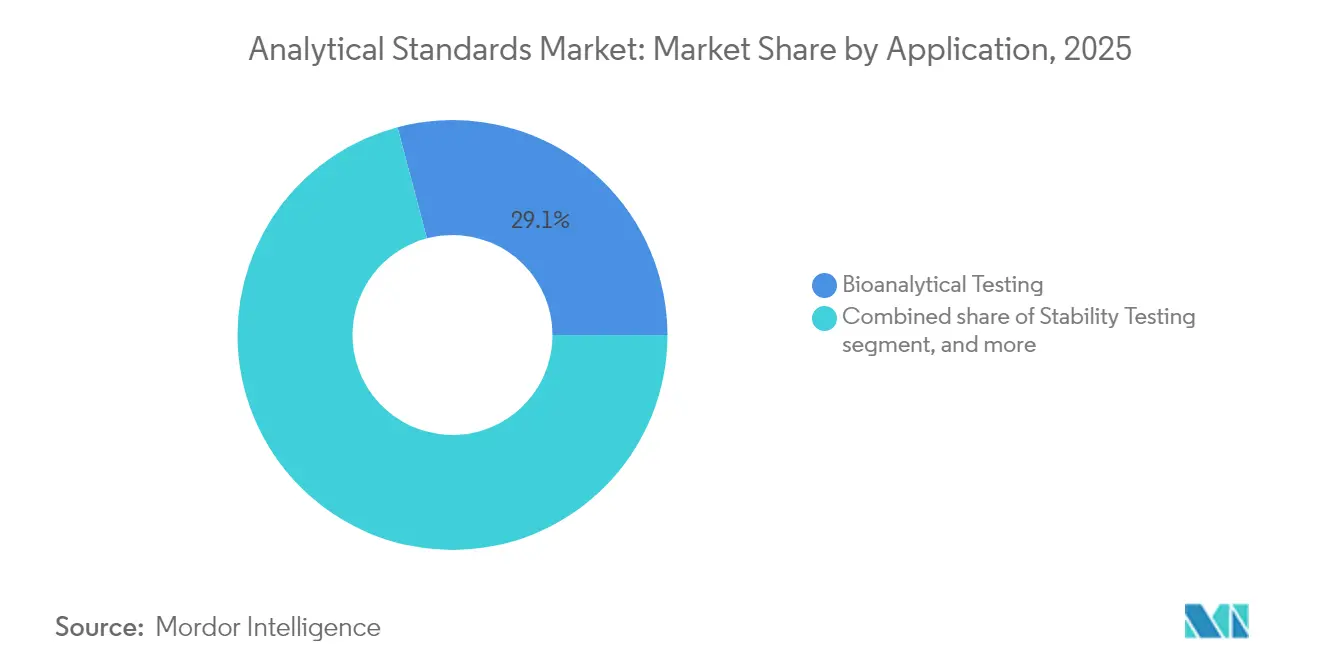

- By application, bioanalytical testing commanded 29.12% of the analytical standards market size in 2025; microbial and environmental testing is projected to expand at an 8.26% CAGR through 2031.

- By end-user, the pharmaceutical and biotechnology segment led with 41.86% revenue share in 2025, whereas forensics and toxicology is poised for an 8.05% CAGR to 2031.

- By geography, North America led with 39.20% revenue share in 2025, whereas Asia-Pacific is poised for an 6.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Analytical Standards Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global pharmaceutical and biotechnology expenditure | +1.8% | North America, Europe, Asia | Long term (≥ 4 years) |

| Stringent international quality and safety regulations | +1.5% | Global | Medium term (2-4 years) |

| Growth in contract research and testing organizations | +1.2% | Global, with APAC fastest | Medium term (2-4 years) |

| Emergence of personalized medicine and complex biologics requiring advanced reference standards | +1.3% | North America & Europe innovation hubs, APAC adoption | Long term (≥ 4 years) |

| Technological advancements in analytical instrumentation | +0.8% | North America & Europe R&D centers, APAC rollout | Short term (≤ 2 years) |

| Rising adoption of certified reference materials across industries | +0.6% | Regulated industries worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Pharmaceutical and Biotechnology Spend Escalation

Pharmaceutical outlays touched USD 1.64 trillion in 2024 and remain on track to reach USD 2.25 trillion by 2028, a trend that multiplies analytical runs needed for drug development, release and stability testing. Biotechnology outsourcing widens the effect as sponsors require CRO partners to maintain extensive CRM libraries for each study phase. The U.S. Food and Drug Administration cleared 50 new drugs in 2024 and anticipates roughly 70 approvals in 2025, each reliant on validated methods anchored by traceable reference materials[1]U.S. Food and Drug Administration, “CDER Drug Approvals 2024,” fda.gov. Oncology leads therapeutics value and demands ultra-high-purity standards to qualify complex biologics. Collectively these factors power sustained growth across the analytical standards market.

Stringent International Quality and Safety Regulations

ICH Q2(R2) and Q14 introduced lifecycle thinking to analytical procedure validation, mandating periodic revalidation whenever methods transfer between sites. Laboratories now require additional CRMs to demonstrate robustness across matrix, range and linearity assessments. Europe complements the shift through guidance on environmental risk and artificial-intelligence applications in medicines, expanding testing breadth[2]European Medicines Agency, “Guideline on Artificial Intelligence in Medicinal Products,” ema.europa.eu. Fifty-two authorities participating in the Pharmaceutical Inspection Co-operation Scheme (PIC/S) are aligning good-manufacturing-practice audits, creating unified demand for high-quality reference materials. In the United States, the FDA’s Quality Management Maturity program underscores automation, further tightening calibration and verification needs that only certified standards can meet.

Expansion of Contract Research and Testing Organizations

Leading CROs such as IQVIA and Thermo Fisher’s PPD division generated double-digit revenue growth in 2024 as sponsors shifted fixed costs into outsourced models. Nearly 37% of laboratories designate analytical testing as their top outsourced activity, concentrating orders with service providers that in turn purchase standards in bulk. Chinese CROs including Wuxi AppTec and Pharmaron broaden global footprints, reinforcing Asia’s pull on CRM supply. The clustering effect improves forecast visibility for CRM vendors but raises expectations for just-in-time delivery and multi-compound custom blends.

Technological Advances in Analytical Instrumentation

Orbitrap Astral Zoom and Orbitrap Excedion Pro systems introduced in 2025 cut analysis time by 35% and lift throughput by 40%, allowing labs to analyze more samples per shift. Smaller injection volumes and higher mass accuracy favor CRMs with lower uncertainty, spurring premium-priced offerings. Artificial-intelligence data workflows reduce manual review yet require rigorously characterized performance-qualification standards to ensure algorithm reliability. Instrument automation also builds the case for synthetic multicomponent reference mixes that can serve dozens of methods through autodilution modules.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of high-purity standards and instrumentation | -1.4% | Global, with acute effect in emerging markets | Medium term (2-4 years) |

| Shortage of skilled analytical personnel | -1.1% | Severe in North America & Europe | Long term (≥ 4 years) |

| Complex multijurisdictional regulatory compliance | -1.0% | Global | Medium term (2-4 years) |

| Supply chain vulnerabilities for specialty chemicals | -0.9% | Global, most disruptive in Asia-Pacific manufacturing | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of High-Purity Standards and Instrumentation

Premium CRMs entail multi-stage purification, isotopic characterization and ISO 17034 audits, elevating unit prices beyond many small laboratories’ budgets. Advanced LC-MS, GC-MS and ICP-MS platforms needed to exploit those standards have list prices easily topping USD 1 million, stretching capital allocations. Tariff discussions related to semiconductor supply add additional cost uncertainty for detectors and optics. As a result, some labs defer upgrades or lengthen CRM replacement cycles, tempering growth in the analytical standards market[3]SEMATECH, “Semiconductor Supply Chain Tariff Analysis,” sematech.org.

Shortage of Skilled Analytical Personnel

Vacancy surveys show more than 46% open positions in clinical labs during 2024, while retirements loom large in cytology and blood banking. Analytical chemist roles are forecast to grow 6% through 2032, yet academic programs yield too few graduates to fill demand. Salary compression, pandemic-era burnout and lengthy training pipelines worsen attrition. Staffing gaps cap instrument utilization and occasionally force reliance on contract testing, indirectly slowing in-house CRM consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Mass-Spectrometry Innovation Accelerates Precision Applications

Chromatography retained 38.05% of analytical standards market share in 2025 thanks to its cross-sector versatility. Meanwhile, mass spectrometry is projected to log a 7.38% CAGR to 2031, buoyed by Orbitrap, time-of-flight and ion-mobility advances that improve speed and sensitivity. The analytical standards market size attached to mass-spectrometry methods is anticipated to expand steadily as oncology, neurology and metabolomics studies demand ever lower limits of detection. New platforms such as Orbitrap Astral Zoom deliver 10 Hz scan rates while cutting solvent use, magnifying laboratories’ demand for multianalyte CRMs that streamline calibration. Spectroscopy and titrimetry maintain niche relevance; Karl Fischer titration remains irreplaceable for moisture assays of drug substances and depends on traceable water standards certified to 0.1% uncertainty.

By Product Type: Matrix-Matched CRMs Earn Regulatory Preference

Organic CRMs covered 60.72% of total revenues in 2025, yet the fastest expanding slice is matrix-matched materials with an 7.66% CAGR forecast. Environmental authorities insist on standards blended into wastewater, soil or serum backgrounds to replicate ion-suppression effects. That need pushes CRM producers to master homogenization and long-term stability studies across complex matrices. Inorganic standards keep a foothold through heavy-metal surveillance in food, soil and recycled plastics. Distinct classification between CRMs and working standards grows sharper as ISO 17034 proliferates; only CRMs offer legally defensible traceability, making them indispensable for regulated submissions.

By Application: Environmental Testing Surges Amid PFAS Scrutiny

Bioanalytical procedures accounted for 29.12% of 2025 revenue, but microbial and environmental testing shows the highest momentum with an 8.26% CAGR outlook. The analytical standards market size tied to PFAS, PCBs and emerging contaminants climbs rapidly as water utilities and remediation firms race to meet stricter discharge limits. In pharmaceuticals, raw-material ID and batch release rely on authenticated reference materials for potency and impurity profiling, creating steady baseline demand. Circular-economy initiatives add new use cases—such as heavy-metal screening in recycled PET—further lifting consumption of multi-element CRMs.

By End-User: Forensics Drives Rapid-Screening Innovation

Pharmaceutical and biotechnology firms retained 41.86% of 2025 turnover, reflecting exhaustive in-house and outsourced testing needs. Forensics and toxicology, however, will outpace with an 8.05% CAGR as workplace drug monitoring and narcotics enforcement intensify. Methods like ambient ionization-MS can scan a hair sample in 1 minute, but still depend on robust calibration curves anchored by CRMs covering opioids, stimulants and novel psychoactive substances. Food-and-beverage labs retain stable demand, especially where PFAS and mycotoxin limits converge across jurisdictions.

Geography Analysis

North America held 39.20% revenue share in 2025 thanks to entrenched pharma manufacturing and a mature regulatory climate. Laboratories across the United States are early adopters of ICH Q2(R2) lifecycle validation, accelerating CRM refresh cycles.

Europe sustains high penetration via EMA-driven harmonization and a strong culture of accredited reference materials. The analytical standards market size in Asia-Pacific is primed for a 6.36% CAGR through 2031, underpinned by China and India scaling GMP facilities and embracing PIC/S membership. Singapore’s biopharma clusters and South Korea’s push into cell-and-gene therapy add incremental pull.

South America and the Middle East witness rising investment in food safety and petrochemical testing, creating entry points for CRM suppliers that can localize inventory and technical support.

Competitive Landscape

The analytical standards industry remains moderately fragmented, yet consolidation is accelerating. Thermo Fisher Scientific plans USD 40-50 billion for acquisitions and recently agreed to buy Solventum’s Purification & Filtration unit for USD 4.1 billion, extending downstream bioprocess coverage.

Waters Corporation’s USD 17.5 billion merger with BD’s biosciences business will create a combined entity spanning chromatography, clinical diagnostics and cellular analysis. Agilent reinforces its position via the USD 925 million BIOVECTRA purchase and the Infinity III LC launch that embeds self-diagnostic software to simplify compliance.

Bruker’s timsMetabo platform showcases innovation in 4D-metabolomics, slashing solvent consumption by 95% while boosting compound-annotation confidence. Mid-tier specialists compete effectively in matrix-matched CRMs where agility and custom formulation trump sheer scale.

Analytical Standards Industry Leaders

Agilent Technologies

Merck KGaA (Sigma-Aldrich)

Waters Corporation

LGC Group

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Waters and Becton Dickinson unveiled a USD 17.5 billion merger creating the sector’s largest analytical-instrument group.

- June 2025: Thermo Fisher launched Orbitrap Astral Zoom and Orbitrap Excedion Pro, improving scan speed by 35% and throughput by 40%.

- May 2025: Bruker introduced timsMetabo for 4D-metabolomics with Mobility Range Enhancement.

- February 2025: Thermo Fisher agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion.

- October 2024: Agilent launched Infinity III LC Series featuring InfinityLab Assist Technology.

- September 2024: Agilent opened a CLIA-certified Biopharma CDx Services Lab in California.

Global Analytical Standards Market Report Scope

As per the report's scope, analytical standards are used to confirm the presence of a specific analyte in a mixture of components. These standards help measure the purity and quality of the formulations, drugs, and biomarkers to increase the precision of an analytical procedure and calibrate various analytical equipment. The Analytical Standards Market is Segmented by Technique (Chromatography, Spectroscopy, Titrimetry, Physical Properties Tests, and Other Techniques), Product Type (Organic and Inorganic), Application (Bioanalytical Testing, Stability Testing, Raw Material Testing, Microbial Testing, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Chromatography |

| Spectroscopy |

| Mass Spectrometry |

| Titrimetry |

| Physical-Properties Tests |

| Other Techniques |

| Organic Standards |

| Inorganic Standards |

| Matrix-Matched/Certified Reference Materials |

| Bioanalytical Testing |

| Stability Testing |

| Raw-Material & Batch-Release Testing |

| Microbial & Environmental Testing |

| Other Applications |

| Pharmaceutical & Biotechnology |

| Food & Beverage |

| Environmental & Water |

| Forensics & Toxicology |

| Chemicals & Petrochemicals |

| Academic & Contract Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Rest of Middle East |

| By Technique | Chromatography | |

| Spectroscopy | ||

| Mass Spectrometry | ||

| Titrimetry | ||

| Physical-Properties Tests | ||

| Other Techniques | ||

| By Product Type | Organic Standards | |

| Inorganic Standards | ||

| Matrix-Matched/Certified Reference Materials | ||

| By Application | Bioanalytical Testing | |

| Stability Testing | ||

| Raw-Material & Batch-Release Testing | ||

| Microbial & Environmental Testing | ||

| Other Applications | ||

| By End-User | Pharmaceutical & Biotechnology | |

| Food & Beverage | ||

| Environmental & Water | ||

| Forensics & Toxicology | ||

| Chemicals & Petrochemicals | ||

| Academic & Contract Labs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the projected size of the analytical standards market by 2031?

The analytical standards market size is forecast to reach USD 2.13 billion by 2031 based on a 5.82% CAGR.

Which technique segment is expanding the fastest?

Mass spectrometry leads growth with a projected 7.38% CAGR through 2031, propelled by oncology and precision-medicine applications.

Why are matrix-matched certified reference materials gaining traction?

Regulators now expect standards to mimic real-world sample backgrounds, making matrix-matched CRMs essential for accurate PFAS, pesticide and mycotoxin assays.

Which region shows the highest growth potential?

Asia-Pacific is set for a 6.36% CAGR as China and India align with PIC/S guidelines and scale pharmaceutical manufacturing.

How does the talent shortage impact laboratories?

Vacancies exceeding 46% in clinical labs restrict instrument utilization and push facilities toward outsourcing, influencing purchasing patterns for CRMs.

What recent deal significantly reshaped the competitive landscape?

Waters Corporation’s USD 17.5 billion merger with BD’s biosciences arm formed the largest analytical-instrumentation combination to date.

Page last updated on: