Amphibious Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 279.34 Million |

| Market Size (2031) | USD 488.70 Million |

| Growth Rate (2026 - 2031) | 11.84% CAGR |

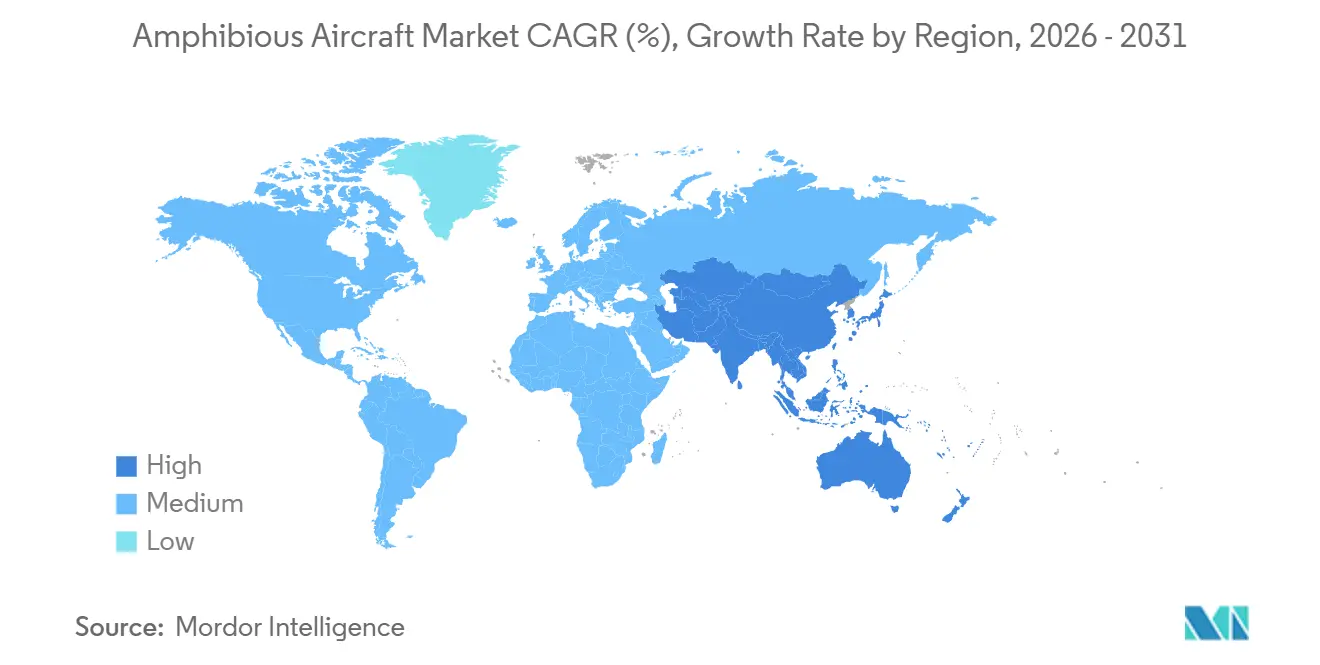

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amphibious Aircraft Market Analysis by Mordor Intelligence

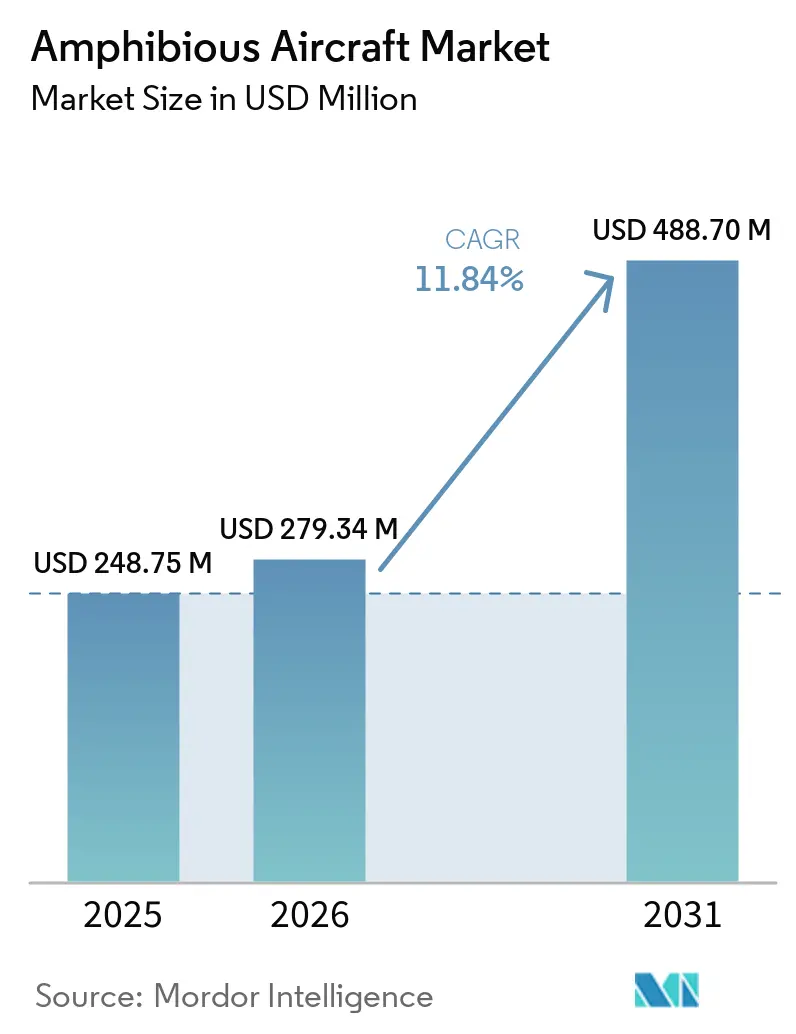

The amphibious aircraft market size is expected to grow from USD 248.75 million in 2025 to USD 279.34 million in 2026 and is forecasted to reach USD 488.70 million by 2031 at 11.84% CAGR over 2026-2031. Operators are responding to tight supply and long delivery lead times by placing early deposits and locking multi-year service contracts, a pattern reinforced by new production approvals and planned capacity ramps across key programs. China’s AG600 production certification in June 2025 positioned the country as the only mass producer of 60-tonne amphibious aircraft for firefighting and maritime patrol, strengthening near-term availability for public agencies. European agencies kept 2028 deliveries for their coordinated firefighter fleet plans, highlighting a near-term supply imbalance and supporting firm pricing for available airframes. Asia-Pacific connectivity programs and airport investments are expanding the opportunity set for inter-island passenger services and logistics, attracting new operator orders and regional fleet plans in the amphibious aircraft market. Announced aircraft commitments by regional seaplane operators add to the growth pipeline across tourism and essential services, supporting consistent utilization and route development.

Key Report Takeaways

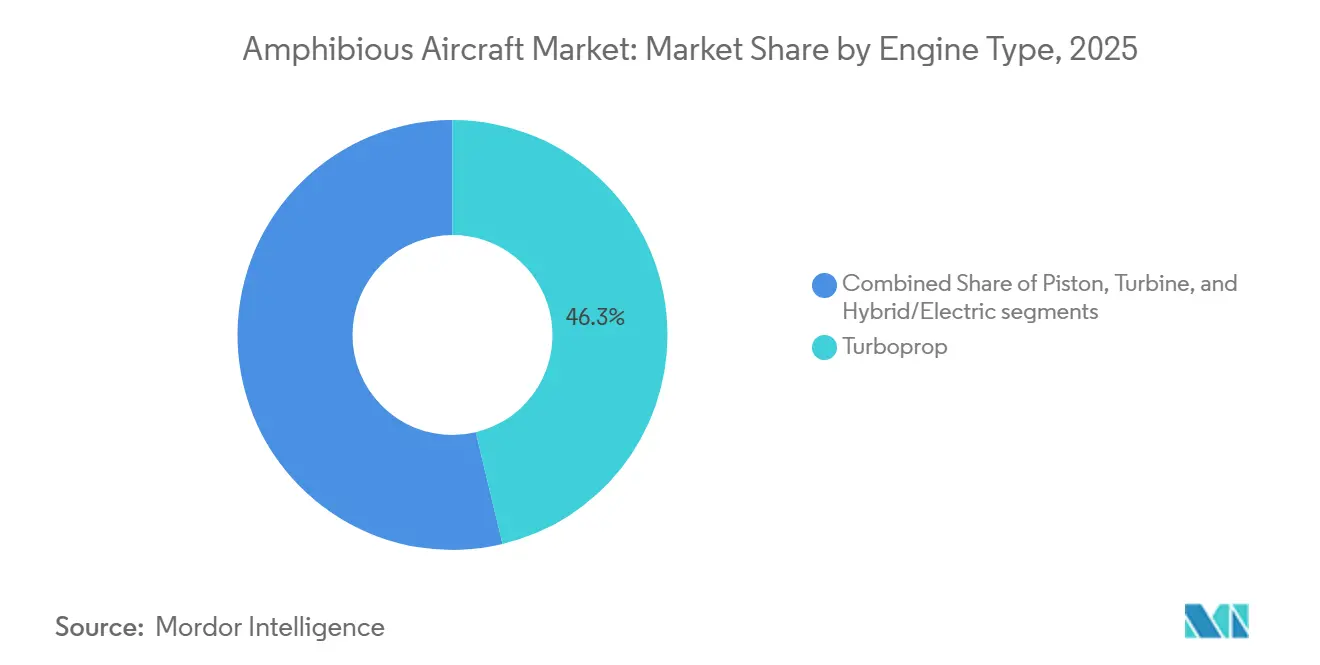

- By engine type, turboprop platforms led the amphibious aircraft market with 46.26% market share in 2025, while hybrid/electric propulsion is projected to expand at a 15.45% CAGR through 2031.

- By seating capacity, aircraft with fewer than 10 seats commanded a 53.45% share in 2025, and more than 20-seat variants are set to grow at a 14.67% CAGR through 2031.

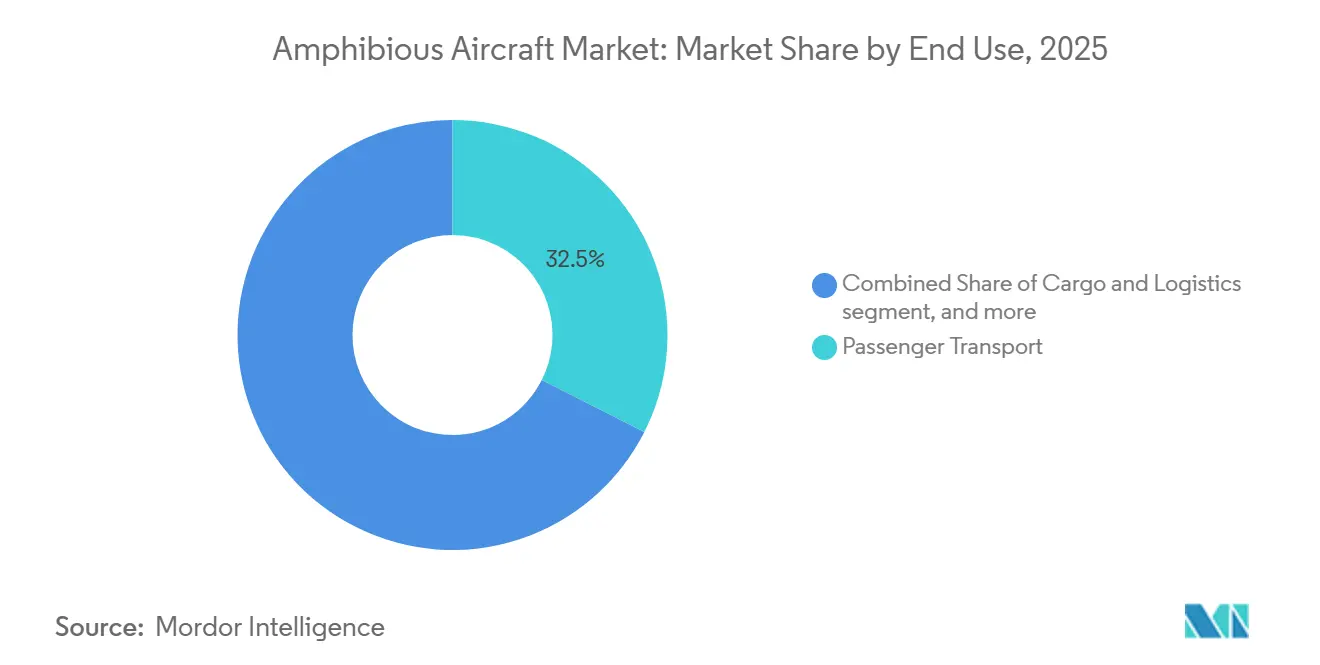

- By end use, passenger transport accounted for 32.45% of the amphibious aircraft market in 2025, and firefighting/search and rescue (SAR) is forecasted to grow at a 14.23% CAGR through 2031.

- By geography, North America retained a 36.78% share of the amphibious aircraft market size in 2025, while Asia-Pacific is projected to record a 14.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Amphibious Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for rapid-response aerial firefighting platforms | 2.8% | Global, with pronounced impact in North America, Europe, and Australia | Medium term (2-4 years) |

| Growing tourism and inter-island passenger connectivity services | 2.3% | Asia-Pacific core, spill-over to Middle East and Caribbean | Medium term (2-4 years) |

| Technological advancements improving operational efficiency and lifecycle costs | 2.1% | Global | Medium term (2-4 years) |

| Development of hybrid-electric amphibious aircraft for sustainable operations | 1.9% | Europe and Asia-Pacific early adoption, North America follow-on | Long term (≥ 4 years) |

| Expansion of coastal surveillance and maritime patrol investments | 1.6% | Asia-Pacific, Middle East, select European coastal states | Long term (≥ 4 years) |

| Government-backed development of seaplane corridors and water-based aviation infrastructure | 1.2% | India, Indonesia, Philippines, Thailand, and Mediterranean Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Rapid-Response Aerial Firefighting Platforms

European coordination for seasonal wildfire response advanced with a 2025 pre-positioned fleet of 22 aircraft under the rescEU mechanism, which confirms sustained public budget support for aerial suppression capacity. Canada’s DHC-515 production schedule signals a planned delivery window beginning in 2028 for European customers, which indicates firm multi-year demand but also a near-term shortfall, supporting stronger pricing power for available platforms. China’s AG600 received production certification in June 2025, a milestone that creates domestic supply for large-capacity amphibious firefighting missions and maritime response, reducing reliance on imports for public safety agencies. These elements reinforce the view that the amphibious aircraft market benefits from strong multi-year commitments and procurement visibility tied to public safety outcomes.

Growing Tourism and Inter-Island Passenger Connectivity Services

Asia-Pacific seaplane tourism showed rising engagement with market participants reporting growing revenue and route density, with the Maldives serving as a scaled benchmark for high-frequency operations and resort transfers. Malaysia’s first commercial approvals for amphibious operations and delivery of a Cessna Grand Caravan EX Amphibian validated the regulatory and operational pathway for tourism links between urban centers and resort islands.[1]Textron Aviation, “Grand Caravan EX Amphibian Delivery in Malaysia,” Textron Aviation, media.txtav.com Operator investments in Southeast Asia signaled confidence in archipelagic connectivity as seaplane fleets expand through multi-aircraft commitments and route launches. Emerging hybrid-electric platforms are gaining traction with operators focused on reducing fuel burn and noise, which align with ESG mandates and local community acceptance of waterfront operations. These factors, together, support steady route development and aircraft commitments in the amphibious aircraft market across both leisure and essential transport profiles.

Expansion of Coastal Surveillance and Maritime Patrol Investments

China’s AG600 program established certified production for maritime response and patrol missions, thereby increasing the availability of large amphibious platforms for coastal surveillance in Asia. European initiatives to expand water aerodromes and coordinated maritime operations are advancing, including procedures aligned with local maritime safety agencies to streamline test flights and operational uptake at key coastal sites. Industry roadmaps from established manufacturers and emerging entrants include variants for maritime surveillance and SAR, extending platform utility beyond tourism and firefighting. Airport infrastructure plans across the region emphasize multimodal connectivity, including water-based operations where geographic conditions permit, positioning the amphibious aircraft market for expanded coastal applications. As these frameworks mature, public agencies and contracted operators gain mission flexibility across surveillance, logistics, and rescue in complex littoral environments.

Technological Advancements Improving Operational Efficiency and Lifecycle Costs

Corrosion-resistant materials and protective coatings in the DHC-515 aim to reduce maintenance burdens typical of saltwater operations, thereby supporting higher availability and more predictable lifecycle costs. Hybrid-electric architectures under development promise substantial reductions in fuel burn and noise, addressing emissions targets and community concerns near coastal urban areas. Manufacturers are planning phased propulsion transitions from sustainable liquid fuels to hybrid-electric, then to all-electric or hydrogen, as certification pathways and energy densities advance. Partnerships between airframe developers and hydrogen-electric system providers are advancing through multi-year flight test programs that support future certification roadmaps. Retrofit programs that electrify proven turboprop models create a near-term route to lower operating costs and fleet decarbonization while leveraging existing maintenance ecosystems. These advances collectively enhance the competitiveness of the amphibious aircraft market by reducing direct operating costs and improving community acceptance for water-aerodrome development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition costs and corrosion-driven maintenance challenges | -1.4% | Global, particularly operators in saltwater environments | Short term (≤ 2 years) |

| Stringent certification processes and specialized pilot training requirements | -0.9% | Global, with higher friction in markets lacking established seaplane training infrastructure | Medium term (2-4 years) |

| Operational limitations due to adverse sea and weather conditions | -0.7% | Coastal regions prone to high wave action and seasonal monsoons | Short term (≤ 2 years) |

| Increasing adoption of unmanned systems reducing certain military applications | -0.5% | North America and select Asia-Pacific defense forces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Costs and Corrosion-Driven Maintenance Challenges

Acquisition costs for new-build amphibious aircraft remain high relative to land-only platforms, which extends payback periods unless operators secure multi-year service contracts and steady utilization. Programs such as the DHC-515 emphasize corrosion protection and composite structures to better handle saltwater operations, helping reduce maintenance overheads that erode margins. Unit pricing reported for large-capacity firefighters underscores the capital-intensive nature of fleet expansion, compelling many agencies to stage procurement over multiple budget cycles. Operators mitigate cost risk through long-term contracts that allocate availability targets and seasonal surge provisions, thereby improving fleet economics in markets prone to wildfire seasons. Sustained OEM focus on maintainability, parts commonality, and digital support remains a key lever for reducing operating costs in the amphibious aircraft market.

Stringent Certification Processes and Specialized Pilot Training Requirements

Hybrid-electric and hydrogen power plant certifications, based on existing airworthiness standards, extend development timelines compared to conventional retrofits due to additional compliance requirements. Retrofit programs that start with proven airframes can compress time-to-market, yet still require extensive testing for new propulsion integration and water handling. Pilots need specific seaplane training and add-on ratings, which introduce additional time and cost for operators expanding into water-based missions. Training programs address water-landing dynamics, wind awareness, wave conditions, and glassy-water techniques to ensure operational safety. Concurrently, regulators and manufacturers are developing standardized guidelines for training, instructor qualifications, and maintenance procedures to facilitate seamless operator onboarding as new propulsion systems advance through certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Hybrid-Electric Thrust Gains Traction Amid Turboprop Maturity

Turboprop engines commanded a 46.26% share in 2025, and hybrid/electric propulsion is forecast to grow at a 15.45% CAGR through 2031 as operators pursue lower operating costs and reduced noise. The DHC-515 and widely deployed PT6A-powered amphibious aircraft remain the workhorses for firefighting and regional services due to ruggedness, fuel efficiency, and parts commonality.[2]De Havilland Aircraft of Canada Limited, “DHC-515 Specification Sheet,” De Havilland Canada, dehavilland.com China’s AG600 program adds scale at the heavy end of the mission spectrum, which broadens state and provincial options for large water-delivery and patrol roles. Hybrid-electric entrants are building order pipelines with operators targeting tourism and inter-island routes, linking ESG compliance to route economics. The transition involves turboprops anchoring current capacity, while the amphibious aircraft industry assesses hybrid systems for specific routes, prioritizing reduced noise and fuel consumption to enhance operational efficiency.

Over the forecast period, turboprop growth moderates as new-build supply fills planned replacements and public fleets adopt mixed propulsion types that fit mission range and cycle profiles. Retrofit programs that electrify proven turboprop airframes can shorten the path to operations by leveraging existing certification foundations and maintenance networks. Hydrogen-electric 19-seat demonstrators offer a long-term regional solution, contingent on advancements in energy storage and successful certification. This staged evolution keeps near-term reliability with turboprops while unlocking future routes and operations for hybrid and hydrogen variants within the amphibious aircraft market.

By Seating Capacity: Sub-10-Seat Dominance Yields to more than 20 Seat Regional Ambitions

Aircraft with less than 10 seats held a 53.45% share in 2025, reflecting the prevalence of Caravan and Twin Otter amphibious aircraft on tourism, utility, and community service routes with limited support infrastructure. The Grand Caravan EX Amphibian continues to extend its reach across Southeast Asia and similar geographies, benefiting from established training, parts, and pilot familiarity. Humanitarian and medevac operations further reinforce the utility of this class by ensuring year-round use that is less dependent on peak tourism. These dynamics continue to support high utilization in the amphibious aircraft market, where water access and short takeoff needs drive aircraft choice.

The more than 20-seat segment is projected to grow at a 14.67% CAGR through 2031 as operators target inter-island links that replace slower ferry travel and expand access. Hybrid-electric and hydrogen-ready airframes in this capacity range will target quieter operations and lower emissions, which supports broader access to waterfront terminals. As airport and water-aerodrome infrastructure improves, larger-capacity options can spread fixed costs across more seats, strengthening route economics across high-demand corridors in the amphibious aircraft market.

By End Use: Firefighting and SAR Outpace Passenger Growth Despite Tourism Volumes

Passenger transport accounted for 32.45% of demand in 2025, sustained by high-frequency island transfers and resort connectivity where water access and short run distances are essential. Tourism routes are complemented by remote-community services and charter operations that rely on small amphibious for flexible access and rapid turnarounds. The DHC-515 and similar platforms continue to attract public-sector interest for aerial firefighting missions, with deliveries scheduled later in the decade to European customers. China’s AG600 expands the heavy amphibious category for maritime response and wildfire suppression in Asia.

Firefighting/search and rescue (SAR) is forecasted to advance at a 14.23% CAGR through 2031, as public agencies raise readiness levels and coordinate seasonal capacity. EU-wide surge plans further institutionalize shared capacity, which benefits cross-border deployments during peak wildfire seasons.[3]Bridger Aerospace, “Joint Development Program Announcement,” Bridger Aerospace, bridgeraerospace.com Cargo and logistics roles remain a smaller slice of the total, but they provide steady demand in regions where runways are scarce or seasonal conditions limit ground access.

Geography Analysis

North America retained 36.78% of the amphibious aircraft market in 2025, supported by provincial water-bomber fleets in Canada and contracted capacity in the US. Delivery schedules for European DHC-515 units starting in 2028 show an active production pipeline that also influences North American availability and pricing. Regional operators favor proven turboprop airframes for mission reliability and maintainability, which supports consistent deployment across firefighting and utility roles. New conversion and retrofit options add future capacity to the region's fleet plan by leveraging existing aircraft families and common support networks.

Asia-Pacific is projected to grow at a 14.56% CAGR through 2031, driven by expanding inter-island networks and tourism flows that support seaplane services. Malaysia's regulatory approval and delivery of an amphibious Grand Caravan EX established a regional reference case for integration of water-based passenger links. China's AG600 program's launch into mass production has added domestic heavy amphibious capability for firefighting and maritime missions, accelerating supply for state operators. Operator orders for multi-aircraft commitments in Southeast Asia signal confidence in archipelagic connectivity and support fleet scaling in the amphibious aircraft market. Airport investment plans across the region indicate capacity and multimodal connectivity, including water-based operations where conditions permit.

The EU's 2025 readiness plan for aircraft and ground personnel underpins strong cross-border cooperation and highlights sustained budget support for aerial firefighting. The Middle East and Africa together remain a smaller share of global demand. Yet, they offer targeted opportunities in tourism and humanitarian services where water-access operations best align with local infrastructure.

Competitive Landscape

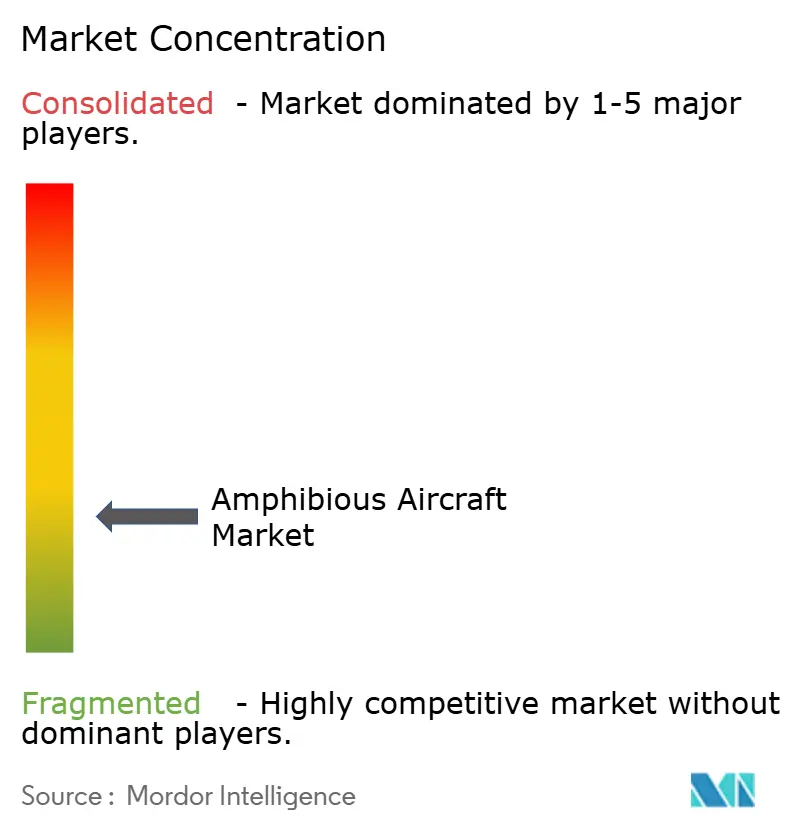

The amphibious aircraft market remains fragmented, with well-established OEMs and new entrants competing across firefighting, tourism, logistics, and maritime roles. De Havilland Aircraft of Canada Limited is advancing the DHC-515 program for deliveries beginning in 2028, serving a coordinated set of European customers and reinforcing the modernization of public-sector fleets. Textron Aviation’s amphibious Grand Caravan EX extends reach in Southeast Asia and similar geographies through strong dealer support and crew familiarity. China’s AG600 production certification positions AVIC to serve domestic heavy-amphibious needs at scale, which influences competitive dynamics in Asia for large firefighting and maritime aircraft.

Emerging entrants focus on hybrid-electric architectures, claiming high fuel efficiency and noise reduction, which align with ESG-driven routes and sensitive waterfront locales. Retrofit strategies led by electric conversion specialists aim to achieve time-to-market advantages by upgrading proven airframes rather than pursuing clean-sheet designs. Airport and water-aerodrome enhancements in Asia-Pacific are enabling operator fleets to scale, which supports additional competition across passenger and utility segments.

Program timelines matter for share capture as deliveries for traditional firefighting platforms cluster later in the decade, leaving capacity gaps that conversions and regional operators aim to fill. Purchasing activity by Southeast Asian seaplane operators confirms momentum for archipelagic connectivity and rising fleet sizes. Given fragmented demand and the entry of multiple propulsion concepts, OEMs will compete on lifecycle support, corrosion protection, and mission flexibility as much as on headline performance.

Amphibious Aircraft Industry Leaders

Dornier Seawings GmbH

De Havilland Aircraft of Canada Limited

ShinMaywa Industries, Ltd.

Aviation Industry Corporation of China, Ltd.

ICON Aircraft Inc. (Precision Aviation Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Australia's Amphibian Aerospace Industries (AAI), known for its amphibious aircraft serving both civil and military sectors, partnered with the Indian firm Apogee Aerospace to introduce its Albatross 2.0 in India. This collaboration coincides with India's heightened emphasis on seaplanes to enhance island connectivity. In line with this initiative, Apogee has placed an order for 15 seaplanes, sealing the deal at an impressive valuation of INR 3,500 crore (approx. USD 366 million).

- February 2025: JOLY Airlines, a South African start-up carrier, signed a Letter of Intent (LoI) for 30 ME-1A amphibious aircraft under development by Mallard Enterprises.

- July 2024: JEKTA Switzerland, developer of the zero-emissions PHA-ZE 100 amphibious aircraft, signed an agreement with Seaplane Asia to integrate 14 PHA-ZE 100 aircraft into the Southeast Asian operator's fleet.

- July 2024: FlyJet Aviation signed a Letter of Intent (LoI) with Mallard Aircraft to procure three ME-1A amphibious aircraft, enhancing its operational capabilities.

Global Amphibious Aircraft Market Report Scope

Amphibious aircraft are those that may land on both land and water. Some amphibious aircraft are seaplanes equipped with retractable wheels.

The amphibious aircraft market is segmented by engine type, seating capacity, end use, and geography. By engine type, the market is segmented into piston, turboprop, turbine, and hybrid/electric. By seating capacity, the market is segmented into less than 10 seats, 10 to 20 seats, and more than 20 seats. By end use, the market is segmented into passenger transport, cargo and logistics, fire-fighting/search and rescue (SAR), maritime patrol and surveillance, and military operations. The report also covers the market sizes and forecasts for the amphibious aircraft market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Piston |

| Turboprop |

| Turbine |

| Hybrid/Electric |

| Less than 10 seats |

| 10 to 20 seats |

| More than 20 seats |

| Passenger Transport |

| Cargo and Logistics |

| Firefighting/Search and Rescue (SAR) |

| Maritime Patrol and Surveillance |

| Military Operations |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Engine Type | Piston | ||

| Turboprop | |||

| Turbine | |||

| Hybrid/Electric | |||

| By Seating Capacity | Less than 10 seats | ||

| 10 to 20 seats | |||

| More than 20 seats | |||

| By End Use | Passenger Transport | ||

| Cargo and Logistics | |||

| Firefighting/Search and Rescue (SAR) | |||

| Maritime Patrol and Surveillance | |||

| Military Operations | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the amphibious aircraft market to 2031?

The amphibious aircraft market size is USD 248.75 million in 2025 and is projected to reach USD 488.70 million by 2031, at an 11.84% CAGR over 2026-2031.

Which engine type leads demand in amphibious platforms?

Turboprop aircraft lead with 46.26% share in 2025, while hybrid and electric propulsion are projected to post the fastest growth through 2031.

Which seating capacity segment is expanding the fastest?

Platforms with 20 or more seats are set to grow at a 14.67% CAGR, supported by inter-island routes seeking faster alternatives to ferries.

Which end-use application is expected to grow the fastest through 2031?

Firefighting/search and rescue (SAR) are forecasted to grow at 14.23% CAGR, reflecting stronger public investment in aerial suppression and emergency response.

Which regions are most important for near-term demand?

North America holds a 36.78% share in 2025, and Asia-Pacific is projected to grow at 14.56% CAGR, driven by archipelagic connectivity and infrastructure programs.

What factors most influence procurement cycles for amphibious fleets

Multi-year public contracts, production lead times, corrosion-resistant design, and emerging hybrid-electric options are key factors shaping procurement and total cost of ownership.

Page last updated on: