Ammonia Storage Tanks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

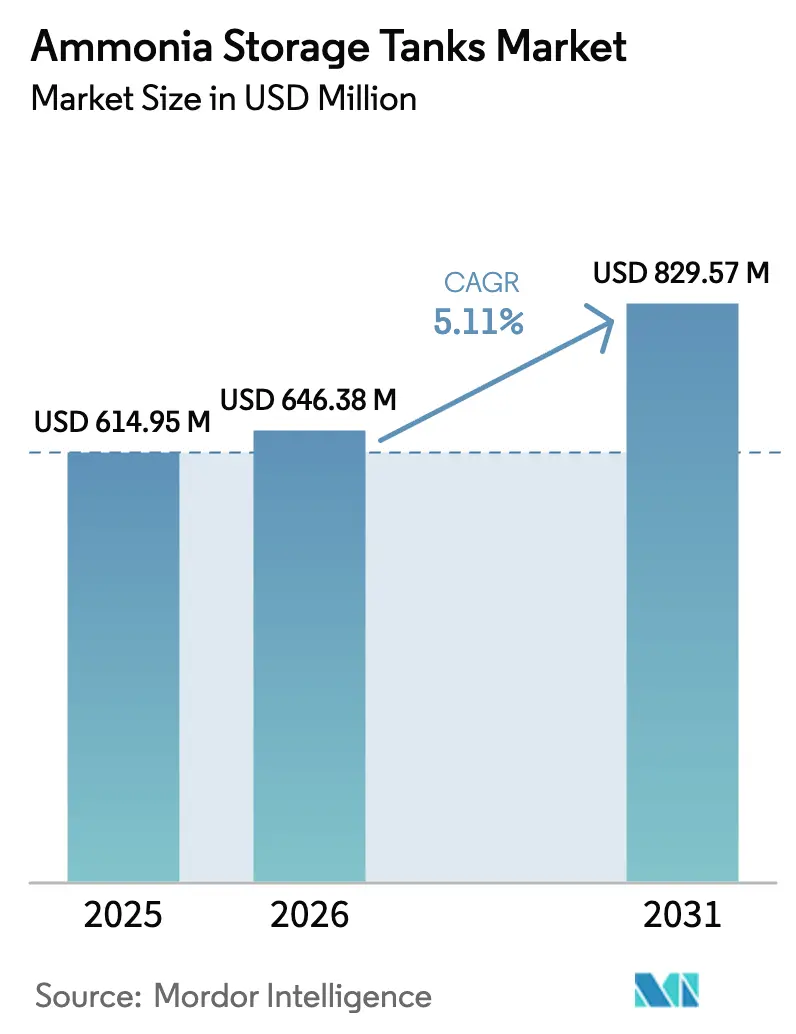

| Market Size (2026) | USD 646.38 Million |

| Market Size (2031) | USD 829.57 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

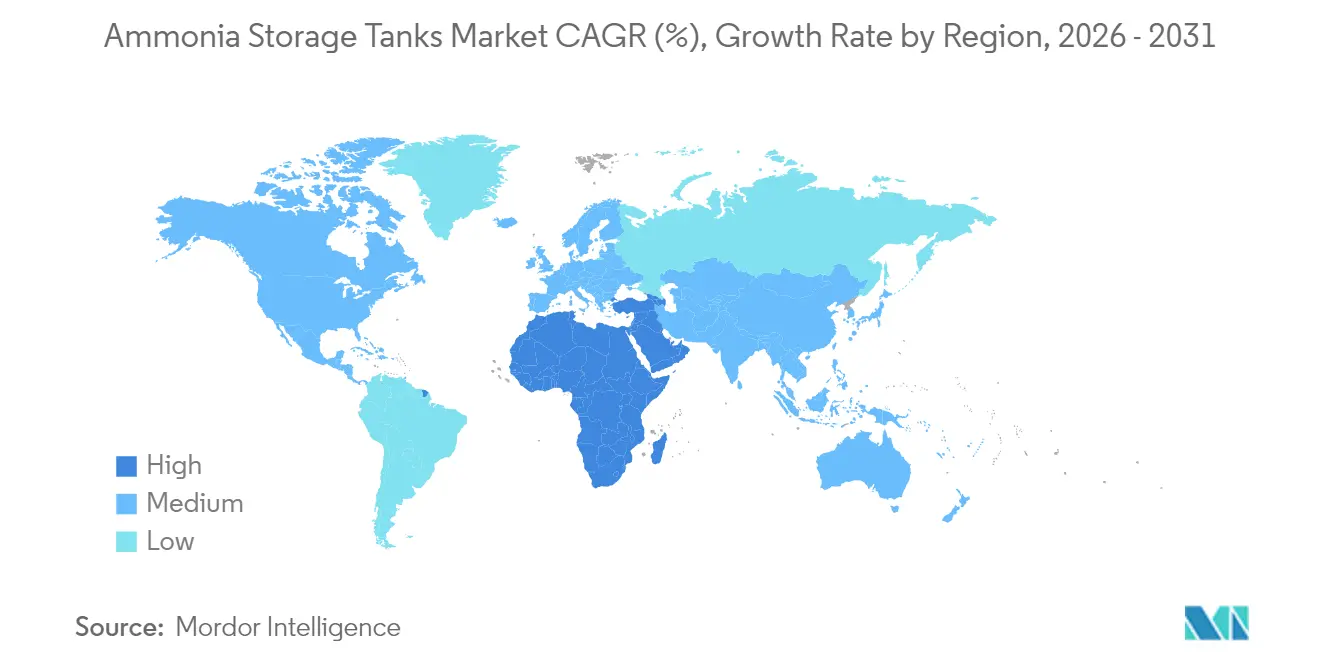

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ammonia Storage Tanks Market Analysis by Mordor Intelligence

Ammonia Storage Tanks market size in 2026 is estimated at USD 646.38 million, growing from 2025 value of USD 614.95 million with 2031 projections showing USD 829.57 million, growing at 5.11% CAGR over 2026-2031. This growth reflects the sector’s pivot from fertilizer-centric demand toward new energy vectors such as green ammonia, long-duration energy storage, and zero-carbon maritime bunkering. Increasing government decarbonization mandates, national hydrogen strategies, and large-scale renewable projects are accelerating capital spending on purpose-built storage infrastructure. Producers are also redesigning tank farms to accommodate stricter safety standards and higher purity requirements, especially for green ammonia that demands corrosion-resistant materials. Midstream and port operators, meanwhile, view ammonia storage as a gateway asset that links renewable production clusters with global shipping lanes, drawing sizeable investment commitments from integrated energy majors and specialized terminal developers[1]Royal Vopak, “Strategic Update 2025–2030,” vopak.com.

Key Report Takeaways

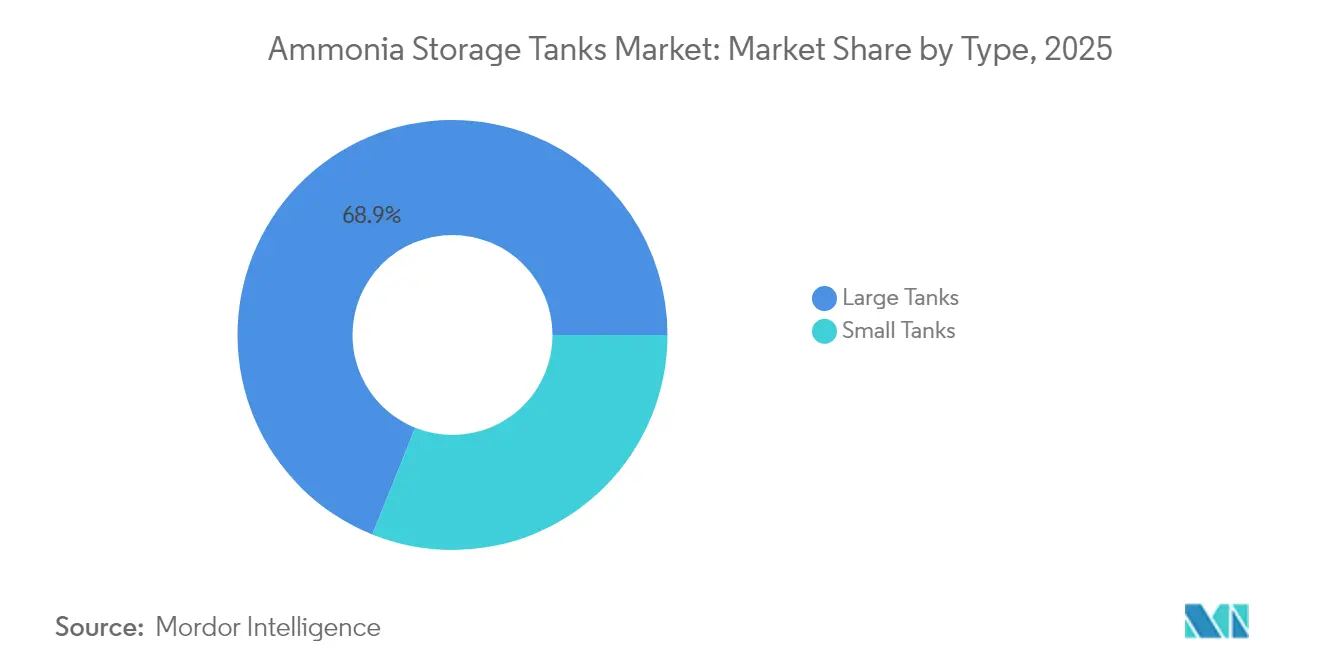

- By type, large tanks commanded 68.92% of the Ammonia Storage Tanks market share in 2025, whereas small tanks are forecast to expand at a 5.61% CAGR through 2031.

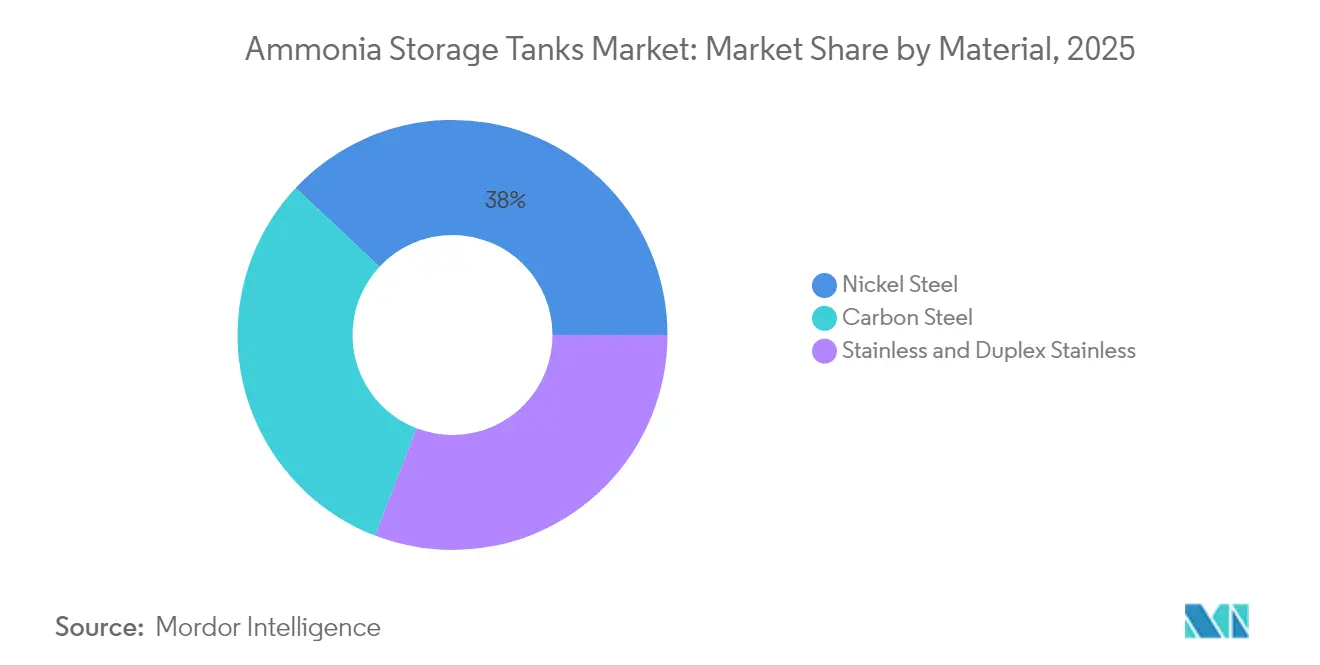

- By material, nickel steel held 38.02% of the Ammonia Storage Tanks market size in 2025, while stainless and duplex stainless steel are set to record a 5.83% CAGR between 2026 and 2031.

- By region, the Middle East and Africa accounted for 35.98% of global revenue in 2025 and is on track for the fastest 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ammonia Storage Tanks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for ammonia as maritime fuel | +1.2% | Global, with early adoption in Europe and Asia-Pacific | Medium term (2-4 years) |

| Asia-Pacific expansions at global ammonia terminals | +0.9% | Asia-Pacific core, spill-over to global trade routes | Short term (≤ 2 years) |

| Increasing adoption in nitro-fertilizer supply chains | +0.7% | Global, concentrated in agricultural regions | Long term (≥ 4 years) |

| National clean-hydrogen roadmaps prioritising ammonia storage | +0.8% | Europe, North America, Australia, Japan | Medium term (2-4 years) |

| Growth of modular green-ammonia bunkering hubs | +0.6% | Coastal regions globally, port cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Ammonia as Maritime Fuel

The International Maritime Organization’s emission targets have prompted shipowners to trial ammonia-fueled propulsion, generating immediate demand for dedicated bunkering tanks. A Norwegian floating bunker barge cleared in 2024 can transfer 416 loads annually, illustrating how ports integrate pressurized ammonia storage with rapid turnaround logistics. Because ammonia occupies 1.6–2.3 times more volume than heavy fuel oil at equal energy content, terminals must either enlarge existing tank farms or install new cylindrical units fitted with over-pressure protection and continuous vapor return headers. The Global Maritime Forum emphasized in its 2024 infrastructure review that timely storage and handling capacity deployment is essential for meeting net-zero milestones.

Asia-Pacific Expansions at Global Ammonia Terminals

Japan, South Korea, and India are commissioning import terminals that link regional fertilizer demand with emerging power-generation and shipping uses. IHI Corporation and Royal Vopak signed a joint development agreement in July 2025 to build an advanced terminal in Japan that combines refrigerated storage with on-site cracking to supply hydrogen to heavy industry. China’s plan to add over 5 million t of new ammonia output in 2025 necessitates buffer storage that can absorb production surges and seasonal fertilizer swings. Indian operator AVTL is replicating a brownfield model at Pipavav and JNPA that couples ammonia storage with multi-product jetties, reducing berth congestion and improving vessel scheduling.

Increasing Adoption in Nitro-Fertilizer Supply Chains

Elevated urea prices—still 40% above pre-conflict five-year averages in early 2025—have persuaded producers to build extra on-site ammonia inventory. Larger storage buffers allow plants to run optimally even when natural gas feedstock or CO₂ capture units experience outages. Rabobank’s 2025 fertilizer outlook observes that the sector retains 77% of global ammonia demand and will continue to anchor baseline consumption. National food-security policies reinforce this storage-led resilience mindset, such as Australia’s push for domestic urea production.

National Clean-Hydrogen Roadmaps Prioritizing Ammonia Storage

The European Union’s hydrogen strategy targets 10 million t y of renewable hydrogen imports by 2030 and singles out ammonia as the preferred carrier because of its high energy density and established transport codes. Germany, the Netherlands, and Norway have earmarked public funding to convert existing oil and LPG terminals into refrigerated ammonia hubs. The European Hydrogen Bank awarded grants in 2025 to seven projects, including Norway’s SkiGA facility that will incorporate 100,000 t y of cushioned storage for export supply. Similar incentives appear in the United States under the Inflation Reduction Act, where production tax credits for clean hydrogen improve project economics for integrated ammonia synthesis, storage, and cracking complexes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ammonia toxicity and leak-management costs | -0.8% | Global, particularly stringent in developed markets | Short term (≤ 2 years) |

| High CAPEX and multi-agency regulatory approvals | -1.1% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Shortage of certified welders/inspectors | -0.5% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ammonia Toxicity and Leak-Management Costs

Ammonia’s corrosive and toxic nature forces operators to install triple-barrier containment, rapid-acting fail-safe valves, and continuous gas detection networks. The U.S. Code of Federal Regulations under 49 CFR 173.315 restricts using copper, zinc, or silver alloys in wetted parts, increasing material costs for fittings and instrumentation. OSHA standard 1910.111 further mandates emergency ventilation and spill-containment hardware, pushing capital expenses beyond those of comparable LPG facilities[2]U.S. Department of Labor, “OSHA 1910.111 Storage and Handling of Anhydrous Ammonia,” osha.gov. Periodic acoustic-emission testing and hydrostatic revalidation add to lifecycle costs, influencing procurement decisions toward materials with proven fracture toughness.

High CAPEX and Multi-Agency Regulatory Approvals

The 2025 update to ASME BPVC Section VIII introduced a tiered approach that ties maximum allowable stress calculations to service fatigue factors, obliging design firms to recertify software and retrain engineers. API 510’s January 2025 edition extends periodic inspection to vessels below 1,000 psi if used in toxic service, which captures most ammonia storage spheres. Developers frequently navigate overlapping federal, state, and port authority reviews that can extend project lead times by 12–18 months, amplifying financing costs and deterring small investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Large Tanks Drive Industrial Applications

Large tanks captured 68.92% of the ammonia storage tanks market in 2025 as vertically integrated fertilizer complexes and emerging ammonia-fueled shipping corridors required capacities above 10,000 m³ for operational efficiency. They remain favored wherever extended residence time, centralized logistics, and economies of scale outweigh site constraints. Conversely, small tanks are projected for a 5.61% CAGR during 2026-2031. Distributed green-ammonia plants that co-locate with wind or solar farms prefer smaller, modular tanks that reduce permitting complexity and shorten construction cycles. The ammonia storage tanks market size for small tanks is forecast to rise steadily as ports adopt mobile bunkering skids and rural co-ops build localized fertilizer depots to shield farmers from supply shocks. In Minnesota, the RMI roadmap showed how localized production combined with 3,000 m³ pressurized bullets minimizes long-haul trucking and aligns storage volume with agronomic demand.

The large-tank segment benefits from retrofit opportunities at brownfield petrochemical sites where foundations and containment bunds are already in place. Operators upgrading to refrigerated anhydrous service can reuse civil works and integrate modern digital twins for integrity monitoring, preserving cost advantage over greenfield construction. Furthermore, upcoming blue-ammonia projects that incorporate carbon capture units favor oversized tanks to decouple synthesis rates from ship-load scheduling, enhancing export reliability. Thus, both tank classes will coexist, with project developers choosing scale or flexibility to match evolving offtake profiles across the ammonia storage tanks market.

By Material: Nickel Steel Dominates Amid Stainless Steel Growth

Nickel steel retained 38.02% share of the ammonia storage tanks market in 2025, owing to its long-standing acceptance for -33 °C storage and favorable toughness-to-cost ratio. Fabricators are familiar with their welding procedures, and design codes supply well-established stress-relief and post-weld heat treatment protocols. That familiarity translates into lower bid pricing and shorter project timelines, maintaining its hold on bulk fertilizer projects. Yet stainless and duplex stainless steel are forecast to grow at a 5.83% CAGR through 2031 as green-ammonia producers demand ultra-low impurity thresholds and extended inspection intervals. The ammonia storage tanks market size attributed to stainless steel is set to rise where owners prioritize corrosion resistance, hydrogen embrittlement mitigation, and compatibility with potential co-storage of ammonia derivatives.

Carbon steel remains prevalent for pressurized bullets under 500 m³, albeit growth is slowing because operators increasingly specify higher chrome or duplex grades to counter stress corrosion cracking. Academic studies investigating metal-halide sorbents and composite liners signal potential material disruption in the medium term. Nonetheless, code bodies such as ASME and API are cautious in approving novel alloys, meaning nickel and stainless steels will dominate until extensive field data validate emerging contenders.

Geography Analysis

The Middle East and Africa secured 35.98% revenue in 2025 and is expected to post a 6.05% CAGR to 2031, the fastest worldwide. Saudi Arabia’s NEOM megaproject, now 80% complete, embeds 1.2 million t y of green ammonia output supported by a cluster of refrigerated tanks that will function both as export buffers and inland offtake nodes. Egypt’s 600,000 t y ACWA Power complex follows a similar model, signaling the region’s ambition to dominate cross-basin trade into Europe and Asia. Abundant solar and wind resources underpin low-cost renewable electricity, allowing local developers to offer competitive free-on-board pricing while absorbing the added tank infrastructure costs.

Asia-Pacific combines entrenched fertilizer demand with rising clean-fuel imports. Japan’s upcoming IHI-Vopak terminal aims to displace coal in co-firing projects, dictating high-purity ammonia storage with advanced boil-off gas recovery. China’s capacity buildout obliges coastal provinces to construct new spheres to balance inland production oversupply each spring. India’s National Green Hydrogen Mission is also steering port trusts to allocate land banks for the ammonia storage tanks market, anticipating export flows toward Europe by 2030.

Europe’s trajectory is driven by policy enforcement rather than indigenous production. Germany, the Netherlands, and Belgium are converting oil terminals into ammonia gateways to meet renewable hydrogen quotas, with Vopak’s Antwerp energy park serving as a blueprint for integrated cracking, storage, and distribution.

North America exhibits steady but moderate growth as operators wrestle with complex permitting and community engagement, though US Gulf Coast refineries are upgrading existing LPG spheres to dual-service ammonia vessels. South America remains nascent; however, Brazil’s hydropower surplus offers a future green-ammonia export vector, prompting feasibility studies for dedicated storage by 2026.

Competitive Landscape

The Ammonia Storage Tanks market is moderately fragmented. Now integrated with Howden, Chart Industries leverages cryogenic expertise to supply prefabricated cold boxes and vapor handling, capturing contracts where owners favor single-vendor process guarantees. Thyssenkrupp Uhde capitalizes on its Haber-Bosch licensing footprint to bundle storage engineering with newbuild synthesis loops, a strategy reinforced by its 2024 partnership with Johnson Matthey on blue-ammonia solutions. With policy and capital converging, the ammonia storage tanks industry will likely experience selective consolidation as top players secure long-term service agreements tied to mega-projects.

Ammonia Storage Tanks Industry Leaders

Geldof

thyssenkrupp Uhde GmbH

McDermott

Royal Vopak

Matrix PDM Engineering

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Agropolychim signed a deal with Proton Ventures to design and construct a new liquid ammonia tank, boasting a storage capacity of 12,500 tons. This tank plays a crucial role in Agropolychim’s broader logistics expansion, which seeks to double its nitrogen fertilizer output and cater to the anticipated surge in ammonia demand.

- June 2025: Aegis Vopak Terminals Limited (AVTL) specializes in the operation of tank storage terminals dedicated to liquid products, with a robust network of storage tank terminals. At the established Pipavav site, AVTL is set to spearhead the development of a brownfield ammonia terminal. This new terminal is poised to streamline ammonia imports, catering to the vast fertilizer market.

Global Ammonia Storage Tanks Market Report Scope

Ammonia storage tanks feature a double containment design, ensuring that both the primary and secondary self-supporting containers can independently hold the stored liquid. Equipped with essential instrumentation, these tanks can effectively monitor and control both routine operations and emergencies. Typically, atmospheric ammonia storage tanks at distribution terminals and plant sites have a storage capacity of up to 50,000 tons. Two primary reasons drive the widespread acceptance of low-pressure ammonia storage. Firstly, it demands significantly less capital investment per unit volume. Secondly, it offers enhanced safety compared to spherical storage, which operates at pressures exceeding atmospheric levels. Given the extensive industrial production of ammonia, storing it at atmospheric pressure and -33°C has become a standard practice.

The ammonia storage tanks market is segmented by type and geography. On the basis of type, the market is segmented into small tanks and large tanks. The report covers market sizes and forecasts for ammonia storage tanks for 17 countries. For each segment, market sizing and forecasts have been done based on value (USD).

| Small Tanks |

| Large Tanks |

| Carbon Steel |

| Nickel Steel |

| Stainless and Duplex Stainless |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Small Tanks | |

| Large Tanks | ||

| By Material | Carbon Steel | |

| Nickel Steel | ||

| Stainless and Duplex Stainless | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the ammonia storage tanks market in 2031?

The market is expected to reach USD 829.57 million by 2031, reflecting a 5.11% CAGR from 2026.

Which region is currently the largest and fastest-growing in ammonia storage tanks?

Middle East and Africa leads with 35.98% revenue in 2025 and the highest 6.05% CAGR outlook to 2031.

Which tank type is expanding the quickest?

Small tanks are forecast to grow at a 5.61% CAGR as distributed green-ammonia projects favor modular capacity.

Why is stainless steel gaining traction in new ammonia tanks?

Green-ammonia applications need higher corrosion resistance and purity, pushing stainless and duplex steels to a 5.83% CAGR.

How do safety regulations affect project costs?

Expanded requirements under OSHA, ASME, and API increase design complexity, inspection frequency, and upfront CAPEX for new installations.

Page last updated on: