Low GWP Refrigerants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

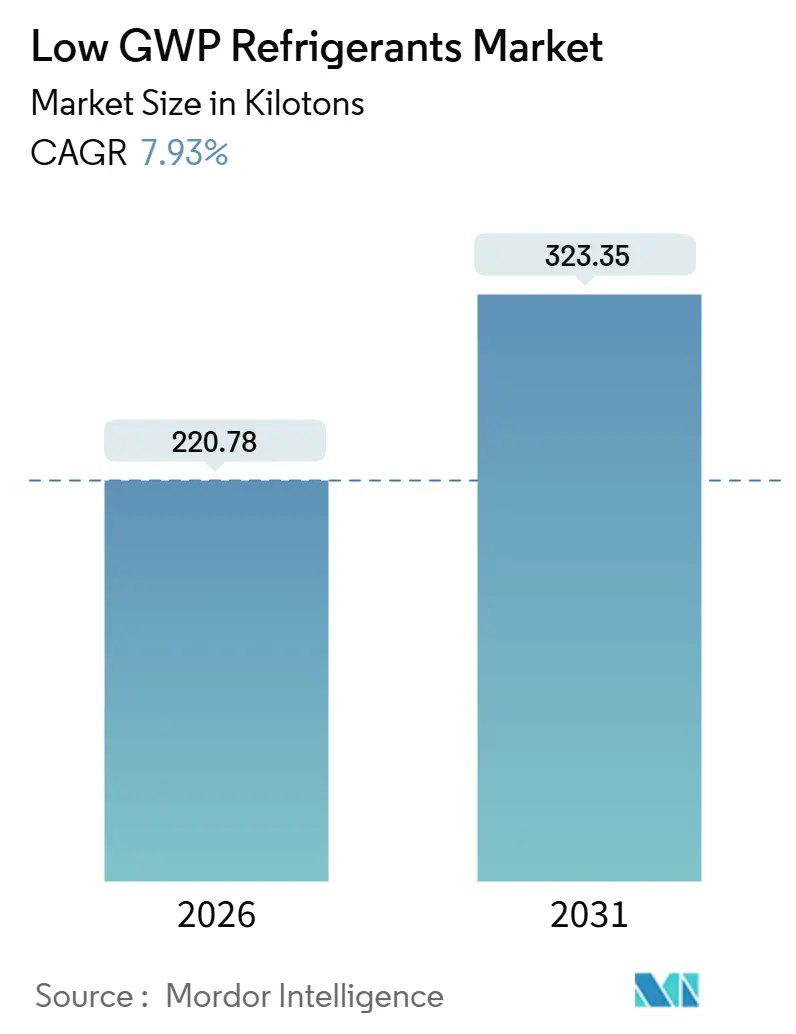

| Market Volume (2026) | 220.78 kilotons |

| Market Volume (2031) | 323.35 kilotons |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low GWP Refrigerants Market Analysis by Mordor Intelligence

The Low GWP Refrigerants Market size is estimated at 220.78 kilotons in 2026, and is expected to reach 323.35 kilotons by 2031, at a CAGR of 7.93% during the forecast period (2026-2031). Strong regulatory pressure in North America and Europe, combined with tightening Kigali phase-down targets, continues to compress the retirement window for high-GWP HFCs. Supply security has become a key competitive factor as feedstock shortages lift contract prices, while supermarket and data-center operators race to lock in long-term volumes. Technology readiness is improving, helped by safer A2L refrigerants and rising hydrocarbon charge limits that lower retrofit complexity. Early movers are extracting margin by pairing proprietary blends with high-efficiency compressors, closing multi-year contracts with food retailers, and partnering with hyperscalers testing liquid cooling.

Key Report Takeaways

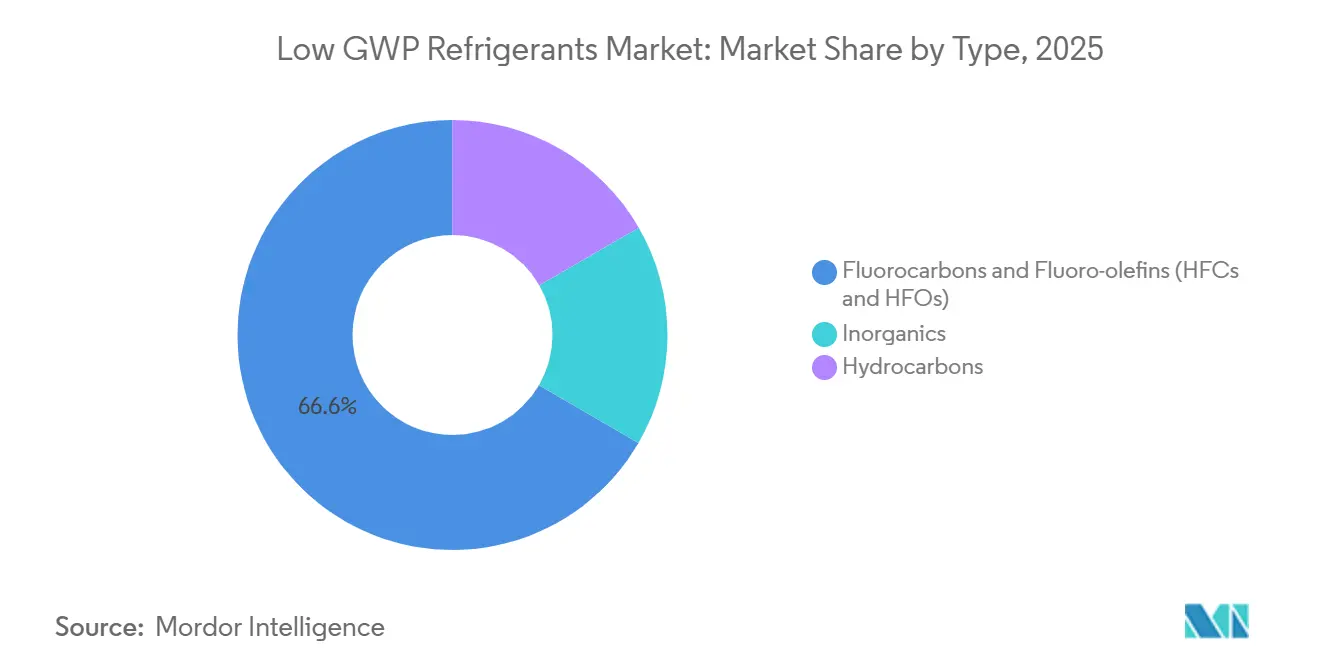

- By type, fluorocarbons and fluoro-olefins held 66.62% of the low-GWP refrigerants market share in 2025, and the segment is anticipated to grow with a 7.98% CAGR through 2031.

- By application, commercial refrigeration posted 45.56% of the low GWP refrigerants market size in 2025 and is expanding at an 8.14% CAGR through 2031.

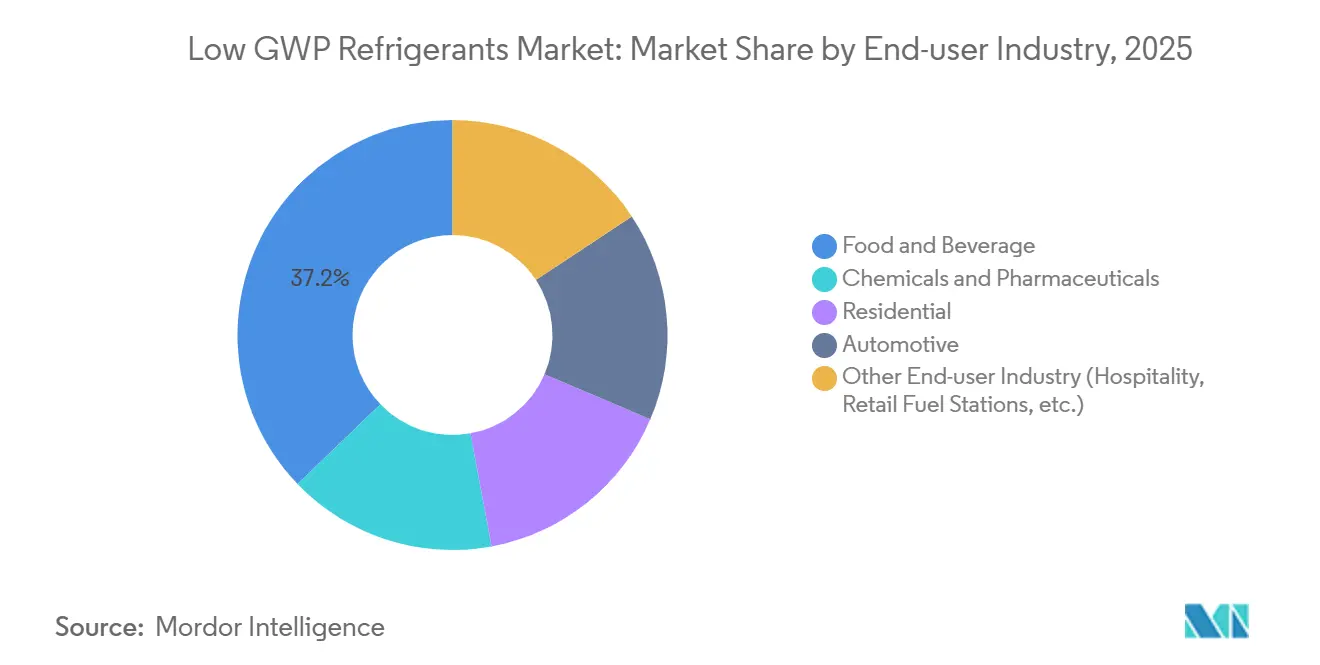

- By end-user industry, food and beverage commanded a 37.19% share of the low GWP refrigerants market size in 2025 while growing at a 7.97% CAGR to 2031.

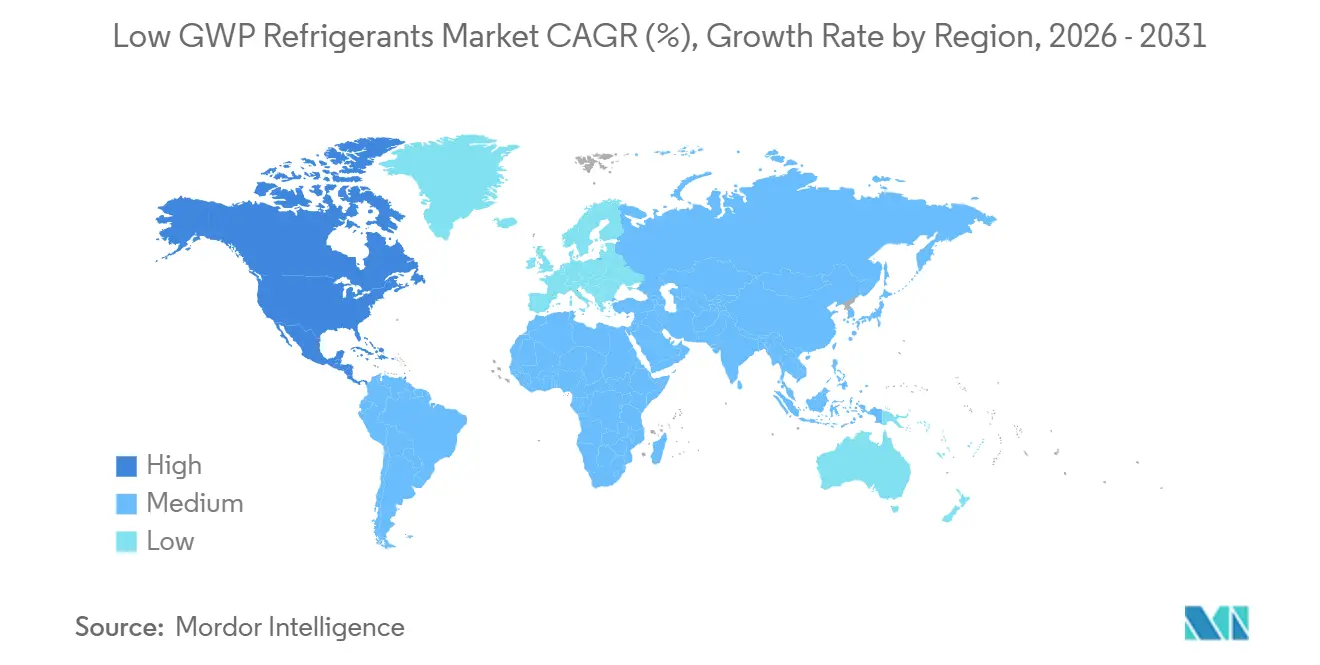

- By geography, North America led with 32.74% of the low GWP refrigerants market share in 2025 and is registering an 8.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low GWP Refrigerants Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations and low environmental impacts | +2.1% | Global, with accelerated enforcement in EU and North America | Short term (≤ 2 years) |

| Growing demand for eco-friendly HVAC systems | +1.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Increasing demand for energy-efficient cooling | +1.5% | Global, peak adoption in APAC and Middle East | Medium term (2-4 years) |

| Data-center liquid-cooling boom driving demand | +0.9% | North America, Europe, APAC emerging | Medium term (2-4 years) |

| Heat-pump incentive programs boosting hydrocarbon systems | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations And Low Environmental Impacts

The European Union trimmed allowable HFC quotas by 40% in 2024, forcing wholesalers to prioritize HFO blends and natural refrigerants in commercial equipment. The U.S. EPA’s AIM Act banned HFC-134a in new chillers starting January 2025, compelling supermarkets to retrofit 12,000 stores by 2028. Developed nations must cut HFC consumption 85% from 2011-2013 baselines by 2036 under the Kigali Amendment, creating supply scarcity that rewards early adopters holding long-term offtake contracts. ASHRAE reclassified R-32 and R-454B as A2L in 2024, enabling their use in residential heat pumps but requiring state-level code updates that only 18 U.S. states had enacted by December 2025.[1]ASHRAE, “Standard 34-2024 Designations and Safety Classifications,” ashrae.org Japan’s Fluorocarbon Emissions Control Law obliges annual leak checks on systems above 1,000 tons CO₂-e, accelerating the shift to low-charge HFO or natural systems in industrial cold storage.

Growing Demand For Eco-Friendly HVAC Systems

Net-zero goals are reshaping procurement; 68% of Fortune 500 companies target carbon neutrality by 2040, a milestone that requires low-GWP refrigerants in owned and leased buildings. Walmart earmarked USD 2.1 billion to upgrade 1,400 U.S. stores to CO₂ systems by 2030, citing a 20% energy cost cut and removal of 2.5 million tCO₂-e annually[2]Walmart Inc., “Sustainability Update August 2024,” corporate.walmart.com . ISO 5149 raised hydrocarbon charge limits to 500 g per circuit in 2024, permitting wider use of propane display cases without expensive ventilation retrofits. The U.S. General Services Administration now limits federal HVAC procurements to GWP below 700, favoring HFO-1234ze(E) chillers (gsa.gov). District cooling providers in Abu Dhabi installed 18 MW of low-GWP capacity during 2025, aligning with the emirate’s 2030 carbon-neutral plan.

Increasing Demand For Energy-Efficient Cooling

Variable-speed compressors paired with low-GWP refrigerants cut electricity use by up to 25% versus legacy R-22 systems in Asia-Pacific, easing grid constraints. India’s Bureau of Energy Efficiency enforced a 3.5 ISEER minimum for split ACs from January 2025, a level achievable only with R-32 or HFO blends. China allocated CNY 50 billion to upgrade cold-chain zones with ammonia and CO₂ equipment under its 14th Five-Year Plan. Data-center operators using HFO-1336mzz(Z) rear-door heat exchangers achieved a PUE below 1.15 in 2025 AI clusters.

Data-Center Liquid-Cooling Boom Driving Demand

Microsoft committed USD 1.2 billion to retrofit fifteen data centers with HFO liquid cooling by 2027. Single-phase immersion cooling with HFO-1336mzz(Z) lowers facility energy use by 40% and supports rack densities above 100 kW. Google’s Belgium pilot cut water consumption 25% by pairing HFO liquid circuits with dry coolers. Standardized manifold designs published by the Open Compute Project in March 2025 hasten vendor interoperability. Edge sites in tropical regions now deploy CO₂ chillers that exploit ambient conditions, lowering operating costs by 18% compared with CRAC units.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global HFO feedstock shortage and price volatility | −1.4% | Global, acute in APAC | Short term (≤ 2 years) |

| End-user safety concerns over mild flammability | −0.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Limited technician training for CO₂ systems | −0.6% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global HFO Feedstock Shortage And Price Volatility

The combined 45 kiloton HFO-1234yf output of Honeywell, Chemours, and Arkema could not satisfy 2025 demand, driving a 22% price jump in H1 2025. Honeywell’s Geismar plant outage trimmed 40% of North American supply for six weeks, delaying automotive model launches. Chemours’ Corpus Christi expansion will reach full capacity only in mid-2026 due to permitting delays, prolonging tightness. China’s 15% tariff on fluorochemical imports enforced in January 2025 added USD 3.50 per kg to landed costs, hurting local blenders. Smaller producers pivot to HFO-1234ze(E) but need equipment redesign, lengthening commercialization by two years.

End-User Safety Concerns Over Mild Flammability

Only 18 U.S. states adopted building codes for A2L refrigerants by December 2025, fragmenting national distribution. The 2024 IMC caps indoor A2L charges at 1.8 kg, limiting single-unit capacities for large residences. European insurers raised premiums to 12% for hydrocarbon kitchen systems despite ISO-5149 compliance. Japan requires annual inspections for CO₂ systems above 4 MPa, adding USD 1,000 in operating cost per supermarket. A 2024 AHRI survey found 34% of U.S. homeowners remain wary of flammable refrigerants, slowing uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fluorocarbons Dominate Amid Hydrocarbon Gains

Fluorocarbons and fluoro-olefins captured 66.62% of the low GWP refrigerants market share in 2025 and are on track for a 7.98% CAGR. Automotive mandates made R-1234yf standard across 52 million vehicles built in 2025. HFO-513A retrofits reduce chiller conversion costs by 30% compared with CO₂ upgrades. Hydrocarbons are rising; European manufacturers shipped 1.8 million propane heat-pump units in 2025 after ISO 5149’s charge-limit revision, broadening residential adoption. Inorganics remain niche; CO₂ racks account for 72% of new Swedish supermarkets, while ammonia prevails in industrial plants where safety protocols and centralized machine rooms mitigate toxicity concerns. Growth prospects hinge on easing HFO feedstock tightness and harmonizing hydrocarbon safety codes, both prerequisites for greater share displacement.

Fluorocarbon suppliers are tailoring blends such as R-455A for rooftop units in hot climates and R-515B for chiller applications that require A1 safety profiles. Hydrocarbon specialists focus on propylene and dimethyl ether prototypes that balance flammability and efficiency. Cross-category innovation is emerging; dual-loop systems pair CO₂ in medium-temperature cases with ammonia or propane in low-temperature circuits, cutting charge volumes and meeting GWP targets without proprietary HFOs.

By Application: Commercial Refrigeration Leads Retrofit Wave

Commercial refrigeration controlled 45.56% of the low GWP refrigerants market size in 2025 and is advancing at an 8.14% CAGR. Supermarket retrofits accelerated after the EPA scheduled a 2026 high-GWP ban for retail food systems, pushing chains to CO₂ racks or HFO-blend condensing units. European discounters favor propane plug-in cases that avoid centralized plant costs and leverage ISO-5149’s raised charge limits. Industrial users are adopting ammonia-CO₂ cascades that cut R-717 charge 80% while preserving sub-zero performance.

Domestic refrigeration is near full transition to isobutane in many regions due to energy-efficiency rules. Transport refrigeration trials CO₂ on cold-climate routes but relies on HFO-blends elsewhere, given ambient sensitivities. Precision cooling for data centers is a small but fast-growing niche; HFO-1336mzz(Z) rear-door exchangers could absorb 15 kilotons yearly by 2028 if hyperscalers standardize liquid designs.

By End-User Industry: Food And Beverage Drives Compliance Spend

Food and beverage accounted for 37.19% of the low GWP refrigerants market size in 2025, expanding at a 7.97% CAGR as cold-chain operators upgrade to meet food-safety and ESG requirements. The U.S. Food Safety Modernization Act pushes distributors toward connected low-GWP systems that enable continuous temperature monitoring. Nestlé is investing CHF 800 million to switch 240 plants to natural refrigerants by 2028, targeting a 40% Scope 1 reduction. Beverage lines now favor ammonia-water absorbers that recycle waste heat, trimming electricity use up to 30%.

Pharmaceutical plants rely on HFO blends in cleanrooms and ultra-cold freezers, with Pfizer standardizing on R-1234ze(E) for mRNA storage. Residential adoption is fueled by heat-pump incentives; propane units appeal in cold regions where performance at −15 °C is critical. Automotive AC remains a major offtake, transitioning almost entirely to R-1234yf. Hospitality and healthcare facilities are shifting to low-GWP chiller plants to meet corporate ESG targets, widening demand diversity.

Geography Analysis

North America commanded 32.74% of the 2025 volume and is growing at an 8.26% CAGR to 2031. EPA bans and IRA tax credits accelerate supermarket and residential conversions, while Canada’s carbon price and provincial rebates support commercial retrofits. Mexico lags due to weak enforcement, concentrating low-GWP adoption in export-oriented plants.

Europe cut HFC quotas by 40% in 2024, lifting spot prices by 18% and fast-tracking HFO and natural adoption. Germany issued EUR 3.5 billion in 2025 heat-pump grants, spurring 1.2 million residential sales with 28% propane share. Nordic nations favor CO₂ racks; Southern Europe leans on HFO-513A in warm climates. The U.K. mirrors EU controls but used transition flexibility to stockpile HFCs, temporarily easing supply constraints.

Asia-Pacific accelerates under HCFC phase-out schedules. China allocated CNY 50 billion to cold-chain upgrades, favoring ammonia and CO₂. India’s 3.5 ISEER rule pushes split AC makers toward R-32 and HFO blends. Japan’s JPY 120 billion heat-pump subsidy targets hospitality and food-service sectors with CO₂ or hydrocarbons. South America and the Middle East-Africa remain early-stage; uptake centers on multinationals able to finance capital-intensive low-GWP systems.

Competitive Landscape

The Low GWP refrigerants market is moderately consolidated, with top producers like Chemours, Honeywell, and Daikin driving innovation in HFO blends to meet GWP regulations. Daikin emphasizes the adoption of R-32 for its operational simplicity, while Honeywell and Arkema strengthen feedstock partnerships to address price volatility. HVAC OEMs, including Lennox and Johnson Controls, are prioritizing refrigerant-specific system optimization, launching low-GWP platforms designed for split systems and data centers. Emerging competitors in CO₂ racks and propane chillers are disrupting the market with modular, natural-refrigerant systems. Epta's acquisition of SET Refrigeración enhances its presence in the supermarket segment, while AI-powered leak detection and energy management platforms are creating new opportunities in the aftermarket sector.

Low GWP Refrigerants Industry Leaders

Daikin Industries, Ltd.

Honeywell International Inc.

The Chemours Company

Arkema S.A.

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Honeywell announced a USD 300 million expansion of its Geismar HFO-1234yf plant, adding 15 kilotons of capacity and cutting energy use 18% per kilogram of output.

- October 2025: Chemours secured EPA SNAP approval for Opteon XL20 (R-454C) in commercial ice machines and transport refrigeration, opening a 22-kiloton annual market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the low-global-warming-potential refrigerant market as all new fluids with a 100-year GWP below 750 sold worldwide for refrigeration, air-conditioning, and heat-pump duties. Covered chemistries include inorganics (ammonia, carbon dioxide), hydrocarbons (propane, isobutane), and new fluorinated blends such as HFOs and mildly flammable A2L HFC/HFO mixtures.

Scope exclusion: Reclaimed or recycled refrigerants and revenues from complete HVAC equipment are outside the study.

Segmentation Overview

- By Type

- Inorganics

- Hydrocarbons

- Fluorocarbons and Fluoro-olefins (HFCs and HFOs)

- By Application

- Commercial Refrigeration

- Industrial Refrigeration

- Domestic Refrigeration

- Other Applications

- By End-user Industry

- Food and Beverage

- Chemicals and Pharmaceuticals

- Residential

- Automotive

- Other End-user Industry (Hospitality, Retail Fuel Stations, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We spoke with gas distributors, OEM formulators, supermarket contractors, and regulators across North America, Europe, Asia, and the Gulf. Their guidance on average selling prices, A2L adoption timing, and stock-piling behavior tied secondary numbers to operating reality.

Desk Research

We built baseline supply, trade, and price grids from UN Comtrade, US EPA AIM allocations, the European F-Gas quota register, and Japan METI production surveys because these datasets report virgin kilograms by tariff code. Analysts then layered insights from the International Institute of Refrigeration, ASHRAE, the Kigali Cooling Efficiency Program, company 10-Ks, plus D&B Hoovers, Factiva, and Questel records to map technology shifts and patent momentum. The sources cited are illustrative, not exhaustive.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction of global production and net imports, which is then cleansed for double counts and corroborated with selective bottom-up supplier roll-ups and sampled ASP-by-type checks. Key drivers (Kigali phase-down milestones, new cold-chain capacity, residential AC penetration, typical charge size, and HFO price curves) feed a multivariate regression combined with scenario analysis to project demand through 2030, while missing data pockets are bridged with conservative, expert-validated assumptions.

Data Validation & Update Cycle

Outputs face arithmetic, variance, and outlier checks, after which senior analysts review and lock the file. Mordor refreshes the dataset annually and issues interim updates when quota changes or major plant events occur, and a final pass precedes every delivery.

Why Mordor's Low GWP Refrigerant Baseline Commands Reliability

Estimates in the public domain often diverge because firms vary their product basket, metric, and update cadence.

Key gap drivers include mixing reclaimed stock with virgin supply, using list prices without discounts, counting full HVAC systems, and sporadic refreshes. Mordor avoids these pitfalls by tracking virgin kilograms under 750 GWP only, valuing them with verified weighted ASPs, and rerunning the model after every regulatory step.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 204.71 kt (2025) | Mordor Intelligence | - |

| USD 8.7 bn (2024) | Global Consultancy A | Combines low-GWP and legacy HFCs, value metric, opaque splits |

| USD 32.57 bn (2024) | Industry Portal B | Includes reclaimed gases and HVAC hardware, aggressive ASP uplift |

| USD 28.76 bn (2023) | Market Tracker C | Omits inorganics, extrapolates only from AC shipments |

These comparisons show how scope creep or pricing shortcuts inflate totals. By sticking to a clear boundary and transparent variables, Mordor Intelligence provides a balanced, traceable baseline that strategic planners can rely on.

Key Questions Answered in the Report

What volume is the low GWP refrigerants market projected to reach by 2031?

The market is expected to attain 323.35 kilotons by 2031, growing at a 7.93% CAGR.

Which segment currently leads in market share?

Commercial refrigeration leads, holding 45.56% of 2025 volume.

Why are fluorocarbons still dominant despite regulatory pressure?

Automotive mandates for R-1234yf and drop-in HFO blends for chillers maintain high demand while supply shortages slow hydrocarbon substitution.

How do U.S. incentives influence residential heat-pump adoption?

The Inflation Reduction Act’s 25C tax credit drove 2.8 million heat-pump sales in 2025, with propane units gaining share in cold climates.

What is the main obstacle to CO₂ system adoption in emerging markets?

A shortage of trained technicians raises installation risk and delays supermarket conversions.

Which regions show the fastest market growth to 2031?

North America posts the highest regional CAGR at 8.26% due to aggressive EPA bans and tax credits.

Page last updated on: